Chapter 16 Planning for Capital Investments

16-1

a (1)

Cash Inflow

Table Value*

Present Value

Year 1

$ 360,000

0.892857

$ 321,429

Year 2

502,500

0.797194

400,590

Year 3

865,000

0.711780

615,690

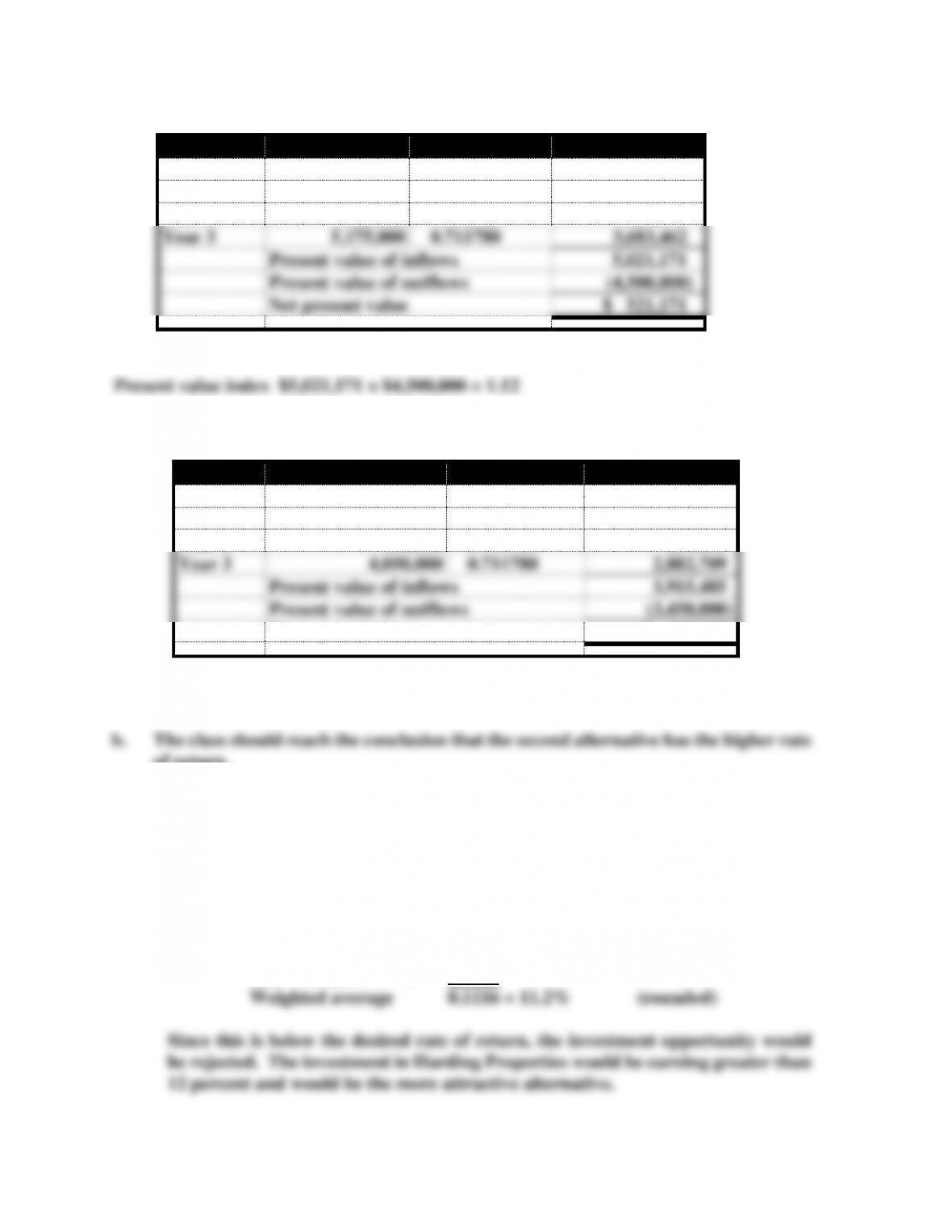

Year 3

5,175,000

0.711780

3,683,462

Present value of inflows

5,021,171

Present value of outflows

(4,500,000)

Net present value

$ 521,171

*Table 1, n = 1– 3, r = 12%

Present value index $5,021,171 ÷ $4,500,000 = 1.12

Summit Apartments

a (2)

Cash Inflow

Table Value

Present Value

Year 1

$ 290,000

0.892857

$ 258,929

Year 2

435,000

0.797194

346,779

Year 3

600,000

0.711780

427,068

Year 3

4,050,000

0.711780

2,882,709

Present value of inflows

3,915,485

Present value of outflows

(3,450,000)

Net present value

$ 465,485

Present value index $3,915,485 ÷ $3,450,000 = 1.13

of return.

ATC 16-2 (continued)

c. It would certainly affect the decision. If EREIC decides to invest in Summit

Apartments, roughly 23 percent ($1,050,000 ÷ $4,500,000) of the invested funds

would be earning a low 5 percent return. The remainder of the investment would

earn a return of more than 12 percent. The weighted average return would be

approximately:

0.05

x

0.23

=

0.0115

0.13

x

0.77

=

0.1001

Weighted average

0.1116 = 11.2%

(rounded)

Chapter 16 Planning for Capital Investments

16-2

d. There is no definitive answer to this question. However, it should be noted that

all of the future cash flows represent estimates that are uncertain. The possibility

ATC 16-3

a. Ten, (note, there are 2 stores opening in Denver). There were 108 stores as of the

b. 2010 = $22,434 (thousands), 2011 = $76,580, 2012 = $172,616. No, there would also

be the costs of working capital items, such as inventory and receivables. Note from

c. The cash to fund new investments in capital expenditures came from financing

ATC 16-4

The student’s response should recognize the fact that planning techniques for capital

investment are only as good as the estimated data that are used in the analysis. With respect

to discounted cash flow techniques, the discount rate or desired rate of return is usually

raised when the data involve a great deal of uncertainty. Even so, investing remains a matter

variable that goes into the decision making process.

In the case of Webb Publishing, the opportunity to purchase a printing company would be

more suitable to analysis with the planning techniques of capital investments. This is so

because the cash flows are more predictable. However, this does not mean that the printing

Chapter 16 Planning for Capital Investments

16-3

ATC 16-5

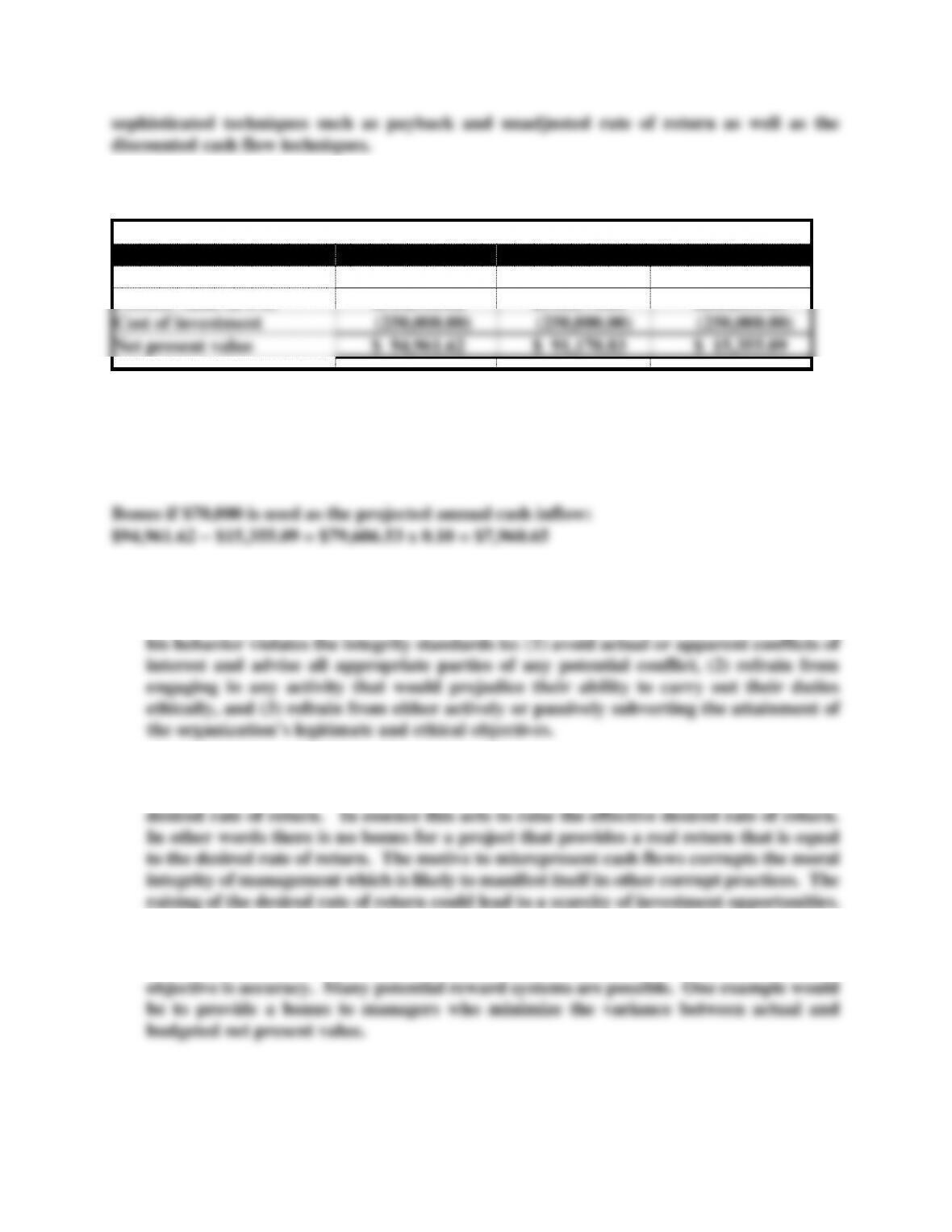

a.

Present Value Table Factor (a) 3.790787 (Table 2, 10%, 5 Years)

Actual

Projected

Projected

Cash inflows (b)

$91,000

$90,000

$70,000

Present value (a x b)

$344,961.62

$341,170.83

$265,355.09

Cost of investment

(250,000.00)

(250,000.00)

(250,000.00)

Net present value

$ 94,961.62

$ 91,170.83

$ 15,355.09

ATC 16-5 (continued)

Bonus if $90,000 is used as the projected annual cash inflow:

$94,961.62 − $91,170.83 = $3,790.79 x 0.10 = $379.08

b. Mr. Holt may not be a member of the Institute of Management Accountants and

therefore may not be bound by the organization’s ethical standards though he is clearly

unethical. Regardless, his behavior is in violation of many of the standards including:

c. The bonus plan encourages managers to consistently underestimate cash inflows and to

reject investment opportunities for which real cash flows approach the company’s

d. The bonus plan should seek to motivate accuracy in reporting. A motive to

underestimate cash flows is just as detrimental as a motive to overestimate. The