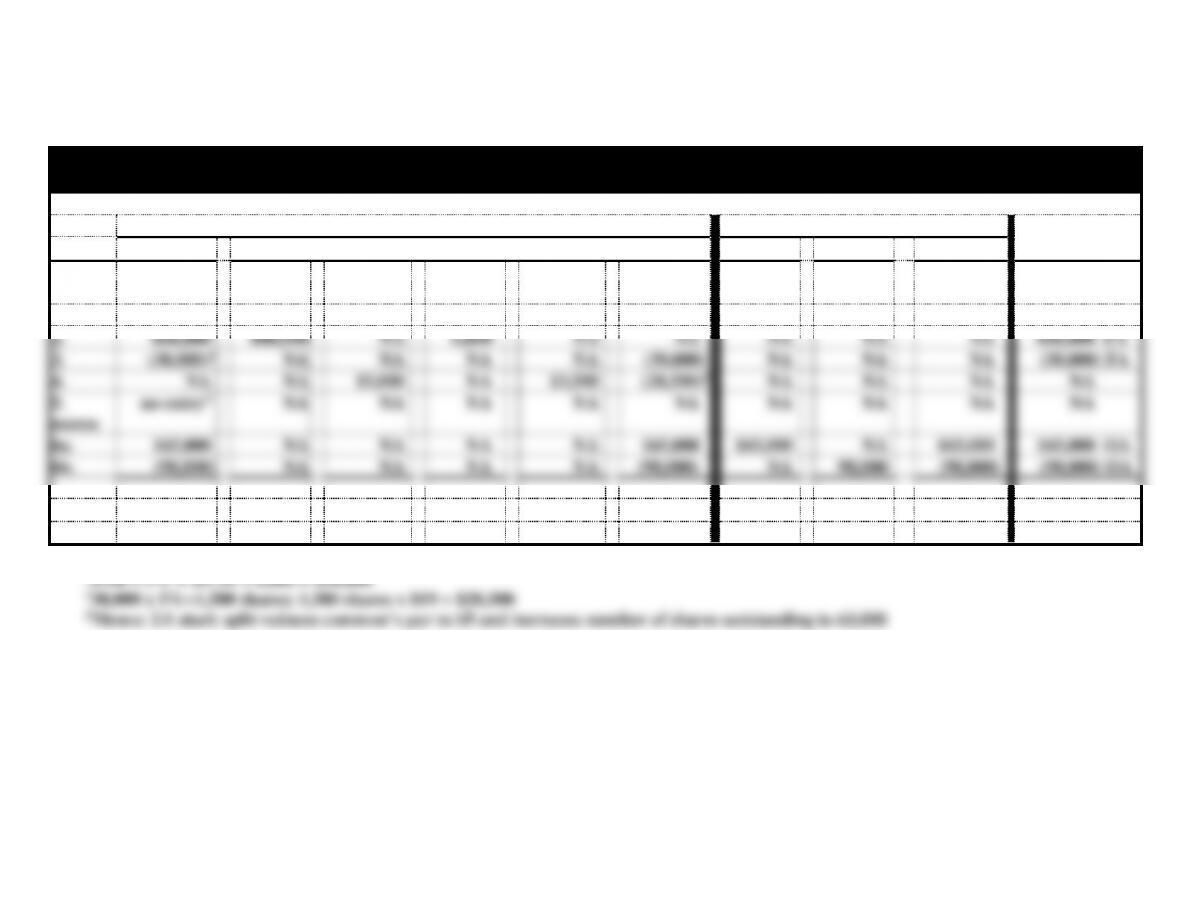

8-1

PROBLEM 8-22

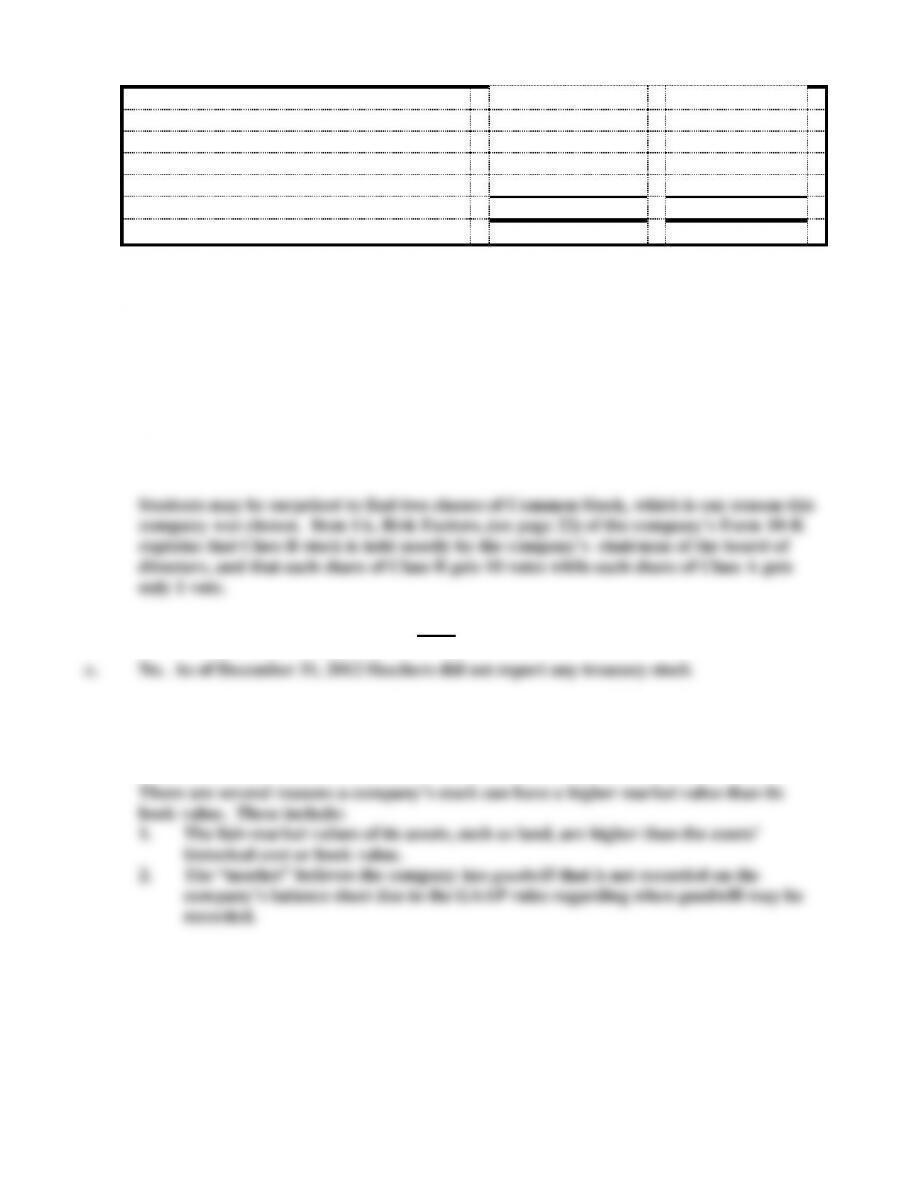

a. NC = Net Change in Cash

Concord Corp.

Statements Model For 2014

Balance Sheet

Income Statement

Statement of

Event

Assets

=

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Pfd. Stk.

+

Com. Stk.

+

PIC in

Exc. PS

+

PIC in

Exc. CS

+

Ret. Earn

1.

450,000

NA

300,000

NA

150,000

NA

NA

NA

NA

450,000 FA

2.

606,000

600,000

NA

6,000

NA

NA

NA

NA

NA

606,000 FA

3.

(30,000)1

NA

NA

NA

NA

(30,000)

NA

NA

NA

(30,000) FA

4.

NA

NA

15,000

NA

13,500

(28,500)2

NA

NA

NA

NA

5.

memo

no entry3

NA

NA

NA

NA

NA

NA

NA

NA

NA

6a.

165,000

NA

NA

NA

NA

165,000

165,000

NA

165,000

165,000 OA

6b.

(98,000)

NA

NA

NA

NA

(98,000)

NA

98,000

(98,000)

(98,000) OA

Totals

1,093,000

=

600,000

+

315,000

+

6,000

+

163,500

+

8,500

165,000

−

98,000

=

67,000

1,093,000 NC

1$100 x 5% = $5; $5 x 6,000 = $30,000

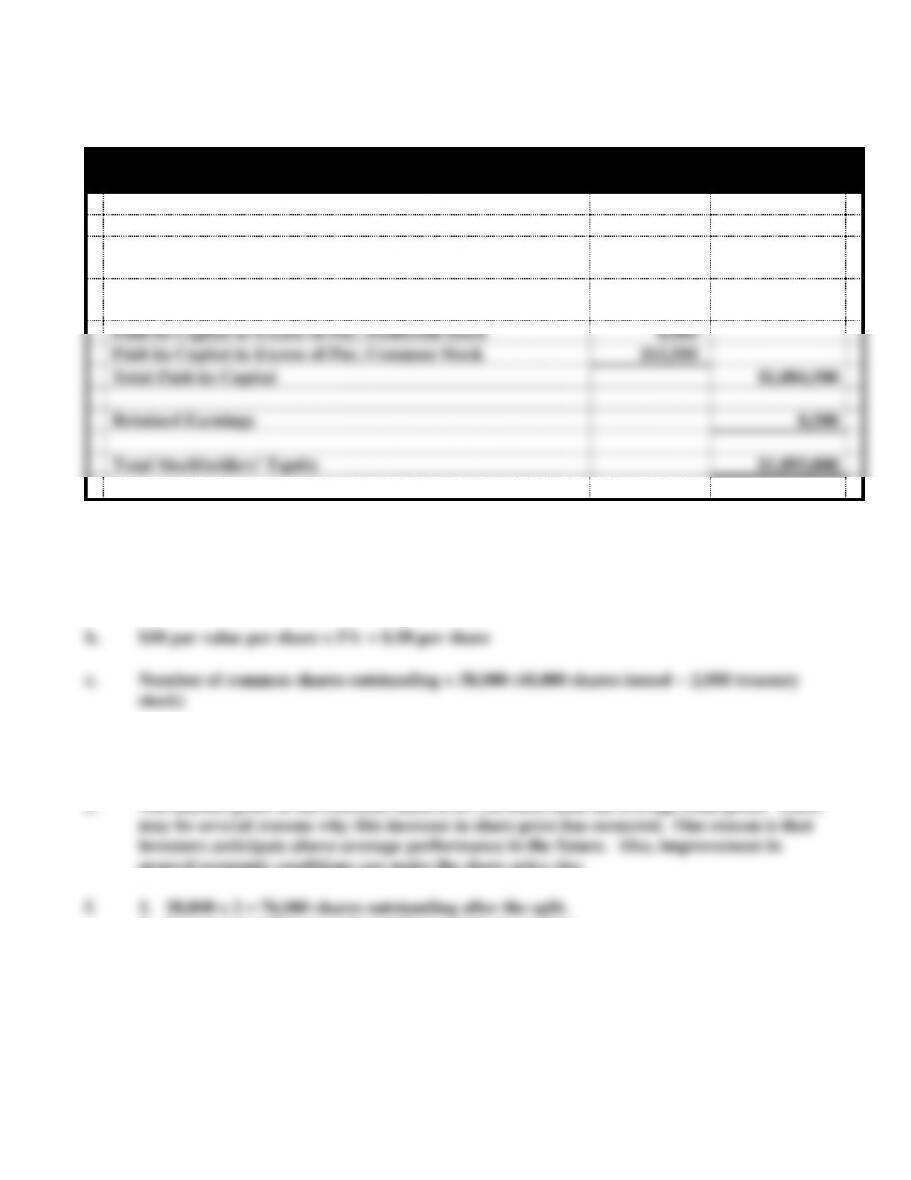

8-2

PROBLEM 8-22 (cont.)

b.

Concord Corp.

December 31 2014

Stockholders’ Equity

Preferred Stock, $100 par value, 5%, 6,000

shares issued and outstanding

$600,000

Common Stock, $5, par, 63,000 shares issued and

outstanding

315,000

Paid-In Capital in Excess of Par, Preferred Stock

6,000

Paid-In Capital in Excess of Par, Common Stock

163,500

Total Paid-In Capital

$1,084,500

Retained Earnings

8,500

Total Stockholders’ Equity

$1,093,000

PROBLEM 8-23

a. $400,000 40,000 shares = $10 per share

d. $800,000 + $100,000 = $900,000;

$900,000 40,000 shares = $22.50 per share

e. The market price of the common stock is $17.50 more than the average issue price. There

general economic conditions can make the share price rise.

2. No amount will be transferred from retained earnings.

3. Theoretically, the market price will be $20 ($40 2).

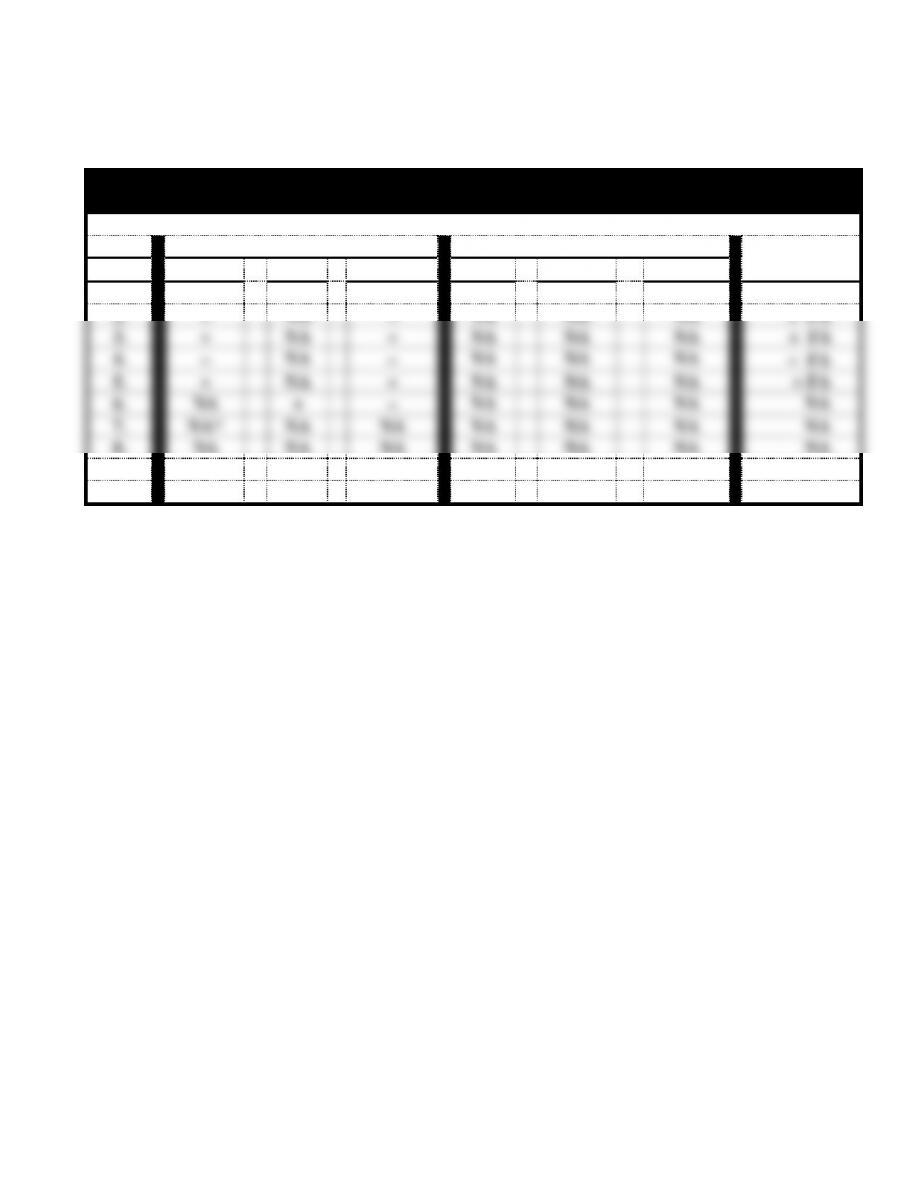

8-3

PROBLEM 8-24

Baskin Inc.

Statements Model

Balance Sheet

Income Statement

Statement of

Event

Assets

=

Liab.

+

S. Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

1.

+

NA

+

NA

NA

NA

+ FA

2.

+

NA

+

NA

NA

NA

+ FA

3.

+

NA

+

NA

NA

NA

+ FA

4.

−

NA

−

NA

NA

NA

− FA

5.

+

NA

+

NA

NA

NA

+ FA

6.

NA

+

−

NA

NA

NA

NA

7.

NA*

NA

NA

NA

NA

NA

NA

8.

NA

NA

NA

NA

NA

NA

NA

9.

NA

NA

NA

NA

NA

NA

NA

10.

−

−

NA

NA

NA

NA

− FA

*No entry: memo record of change in par value and # of shar

8-4

Solutions to Analyze, Think, Communicate

ATC 8-1

All dollar amounts are in millions.

a. The par value of Targets’ common stock is $.0833 (8.33 cents), according to its balance

sheet.

female.

d. Target’s statement of cash flows shows that $1,875 was spent to purchase its own stock in

treasury stock.

ATC 8-2

Wendy’s and Harley-Davidson data are in thousands, Coke data are in millions.

b. Wendy’s stated value per share:

$3,412 341,266 = $.01 per share

c. Wendy’s average issue price of common stock:

Coca-Cola’s average issue price of common stock:

2012 : ($3,412 + $1,066,069) i.e., $1,069,481 341,266 = $3.13

2011: ($3,391 + $ 968,392) i.e., $ 971,783 339,107 = $2.87

8-5

d. Wendy’s shares of stock outstanding at end of year:

2012: 470,424 − 78,051 = 392,373

2011: 470,424 − 80,700 = 389,724

ATC 8-2 (cont.)

Coca-Cola’s stock outstanding at end of year:

2012: 7,040 − 2,571 = 4,469

e. Wendy’s average cost per share of treasury stock:

2012: $382,926 78,051 = $4.91

f. Two of the companies appeared to be profitable because their retained earnings increased

g. One can determine the amount of increase in retained earnings, which is caused by profit,

8-6

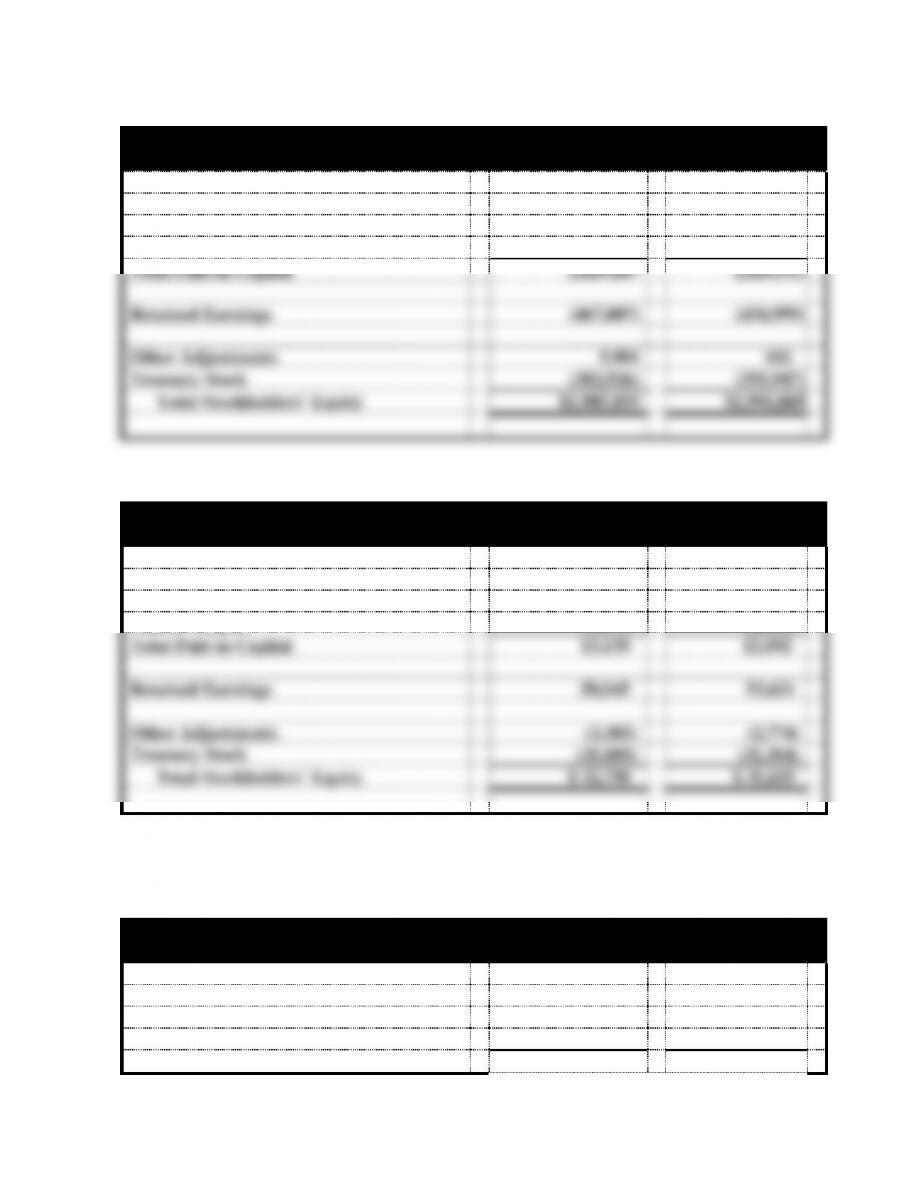

ATC 8-2 (cont.)

h.

Wendy’s

(in thousands)

Stockholders’ Equity

2012

2011

Common Stock

$ 47,042

$ 47,042

Capital in Excess of Stated Value

2,782,765

2,779,871

Total Paid-in Capital

2,829,807

2,826,913

Retained Earnings

(467,007)

(434,999)

Other Adjustments

5,981

102

Treasury Stock

(382,926)

(395,947)

Total Stockholders’ Equity

$1,985,855

$1,996,069

Cola-Cola

(in millions)

Stockholders’ Equity

2012

2011

Common Stock

$ 1,760

$ 1,760

Capital Surplus

11,379

10,332

Total Paid-in Capital

13,139

12,092

Retained Earnings

58,045

53,621

Other Adjustments

(3,385)

(2,774)

Treasury Stock

(35,009)

(31,304)

Total Stockholders’ Equity

$ 32,790

$ 31,635

ATC 8-2 h. (cont.)

Harley Davidson

(in thousands)

Stockholders’ Equity

2012

2011

Common Stock

$ 3,412

$ 3,391

Additional Paid-in Capital

1,066,069

968,392

Total Paid-in Capital

1,069,481

971,783

8-7

Retained Earnings

7,306,424

6,824,180

Other Adjustments

(607,678)

(476,733)

Treasury Stock

(5,210,604)

(4,898,974)

Total Stockholders’ Equity

$ 2,557,623

$ 2,420,256

ATC 8-3

This solution is based on the company’s From10-K for the fiscal year ended December 31, 2012,

and amounts are in thousands, except for per share amounts.

a. As of December 31, 2012, Skechers’ total shareholders’ equity was $919,089. There were

39,021 shares of Class A Common Stock outstanding and 11,274 shares of Class A

Common Stock outstanding, for a total of 50,295 shares of common stock. This resulted

in a book value per share of $18.27. ($919,089 ÷ 50,295 shares) = $18.27.)

b. The par value of common stock is .1 cents per share.

d. (Though not asked for in the problem, note that on March 4, 2013, the first trading day

after the company filed its 2012 Form 10-K, Skechers’ stock was selling for $21.03 per

share, versus its book value of $18.27)

ATC 8-4

Note to Instructor: The factors given below are only selected factors and not meant to be all

inclusive.

MEMO

TO: Jim and Scott

FROM:

The advantages and disadvantages of the partnership and the corporate forms of business

organizations are shown below.

Partnership:

Advantages: Easy to form;

Not subject to many of the federal and state regulations imposed

Corporation:

Advantages: Separate legal entity; the owner’s liability is limited to investment;

Continuity of life; i.e., the corporation does not dissolve at the death,

etc. of owners;

Ownership is easily transferred;

ATC 8-5

a.

1. Converting to an accelerated method of depreciation would increase expense on the

income statement thereby decreasing net income and the stockholders’ equity section (i.e.,

2. Increasing the receivables expected to be uncollectible would increase the amount of bad

debt expense on the income statement with the resultant effect of reducing net income,

8-9

3. Increasing the percentage of estimated warranty claims would increase warranty expense

in the current period. This action would reduce net income and stockholders’ equity (i.e.,

retained earnings) on the balance sheet. Other balance sheet accounts affected would be

warranties payable, which would increase liabilities for the period.

b. Stinson’s actions would cause an increase in stockholders’ equity in subsequent

period’s earnings would be transferred to management through the bonus system.

ATC 8-5 (cont.)

c. The managers of a company are hired to make decisions that are in the best interest of the

stockholders (the owners of the company). They should make decisions that increase the

value of stockholders’ equity, not decisions that increase their own personal worth.

strategies are unethical. She is not doing her job, which is to look after the stockholders’

interest.

d. If bonuses were tied to stock prices, management would be motivated to make decisions

e. Since the company is expected to report a loss, the price earnings ratio cannot be

computed. Accordingly, Stinson’s strategy would not affect the price-earnings ratio.