6-1

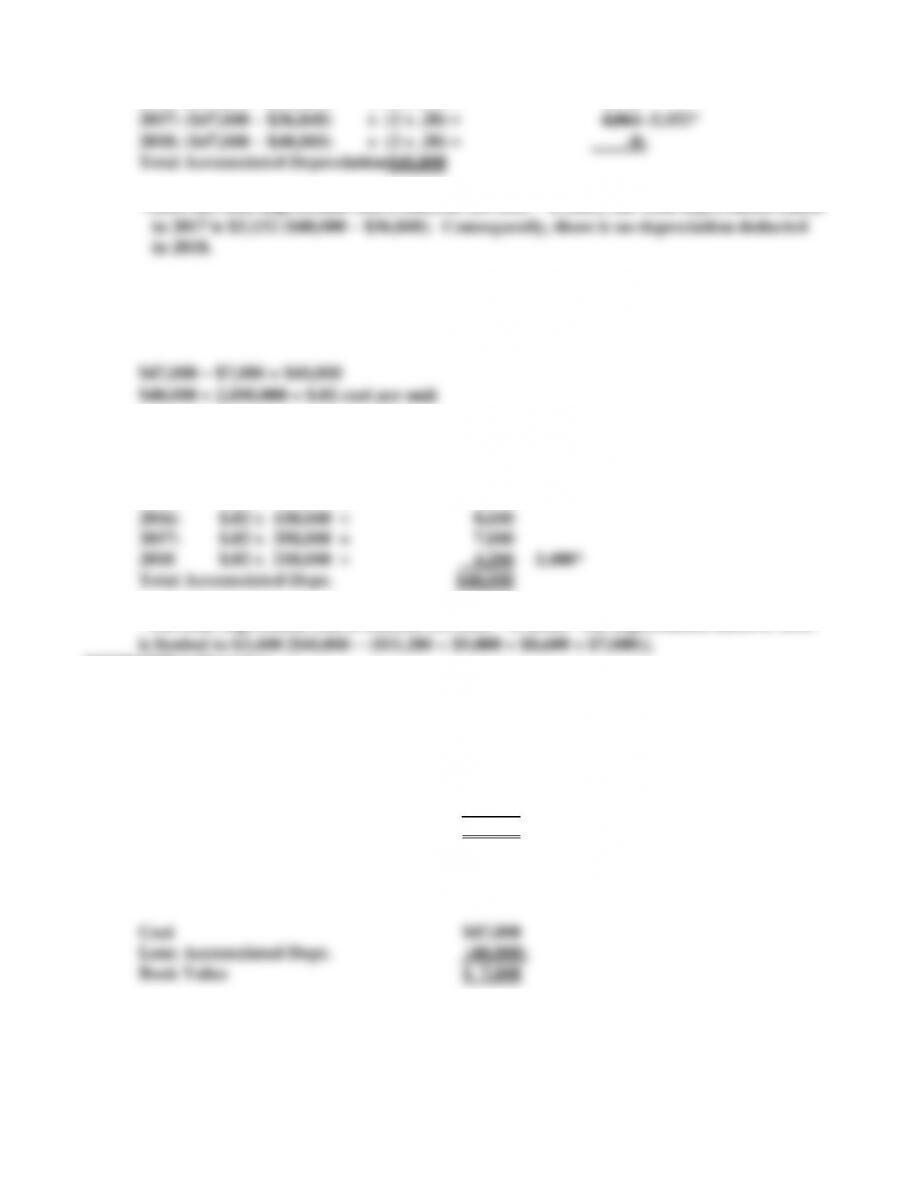

2016: ($47,000 − $30,080) x (2 x .20) = 6,768

*Since the total depreciable cost is $40,000 ($47,000 − $7,000), the total depreciation taken

b. Units-of-Production

(Cost − Salvage) Estimated Production = Depr. Cost per Unit

Annual Depreciation = Depr. Cost per Unit x Actual Annual Units

2014: $.02 x 560,000 = $11,200

2015: $.02 x 490,000 = 9,800

*The total depreciable cost is $40,000 ($47,000 − $7,000). The depreciation taken in 2018

EXERCISE 6-10 (cont.)

c. Calculation of Book Value

Double-Declining Balance

Cost $47,000

Less: Accumulated Depr. (40,000)

Book Value $ 7,000

Units-of-Production

Calculation of Gain

Units-of-

6-2

DDB Production

EXERCISE 6-11

a. Calculation of Depreciation:

Van Cost $35,000

Sales Tax & Title Fees 1,500

2014 Depreciation: $7,500

2015 Depreciation: $7,500

b. Cost $36,500

EXERCISE 6–12

a. Historical Cost $50,000

Less: Accumulated Depreciation (41,000)

Book Value $ 9,000

c. Net income would increase by $1,000, the amount of the gain, in the year of the sale.

d. Total assets would increase by $1,000, the amount of the gain. Cash would increase by

EXERCISE 6-13

Liken Enterprises

2015 Accounting Equation

6-3

Assets

=

Stockholders’ Equity

Event

Cash

Land

=

Common

Stock

+

Retained

Earnings

a.1

+22,500

(20,000)

=

2,500

b.1

+18,500

(20,000)

=

(1,500)

a. 1) See above.

b. (1) See above.

(2) Loss of $1,500 ($18,500 sales price

EXERCISE 6-14

Depreciation

Expense

2014: $72,500 − $12,500 = $60,000; $60,000 3 = $20,000

2016:

Cost $72,500

*revised salvage

**revised remaining life

2017: (Same as year 2016) $15,000EXERCISE 6-15

Shredding Machine:

Book value would still be $6,000; the $1,900 repair cost will be expensed.

Building:

6-4

EXERCISE 6–16

a.

Assets

=

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

+

Book Value of

Forklift

=

C. Stock

+

Ret. Ear.

15,000

+

80,000

=

45,000

+

50,000

NA

−

NA

=

NA

NA

( 9,000)

+

=

NA

+

(9,000)

NA

−

9,000

=

(9,000)

(9,000) OA

b.

Assets

=

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

+

Book Value of

Forklift

=

C. Stock

+

Ret. Ear.

15,000

+

80,000

=

45,000

+

50,000

NA

−

NA

=

NA

NA

( 9,000)

+

9,000

=

NA

+

NA

NA

−

NA

=

NA

(9,000) IA

c.

Assets

=

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

+

Book Value of Forklift

=

C. Stock

+

Ret. Ear.

15,000

+

80,000

=

45,000

+

50,000

NA

−

NA

=

NA

NA

( 9,000)

+

9,000

=

NA

+

NA

NA

−

NA

=

NA

(9,000) IA

EXERCISE 6-17

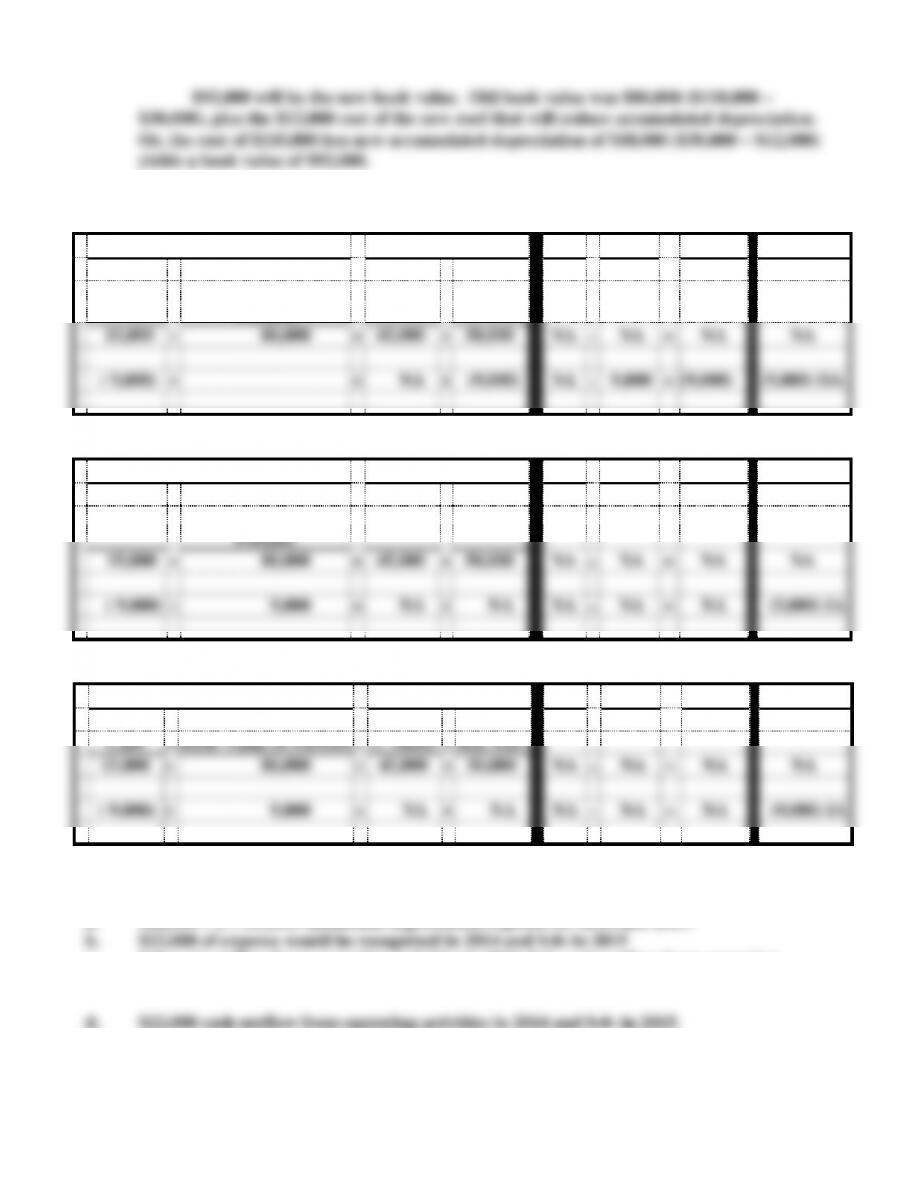

a. $22,000 2 = $11,000 additional depreciation expense for 2014 and 2015.

c. $-0- cash outflow from operating activities in 2014, $-0- cash outflow from operating

activities in 2015 (cash outflow in 2014 is from investing activities).

EXERCISE 6–18

6-5

b.

Depletion Calculation:

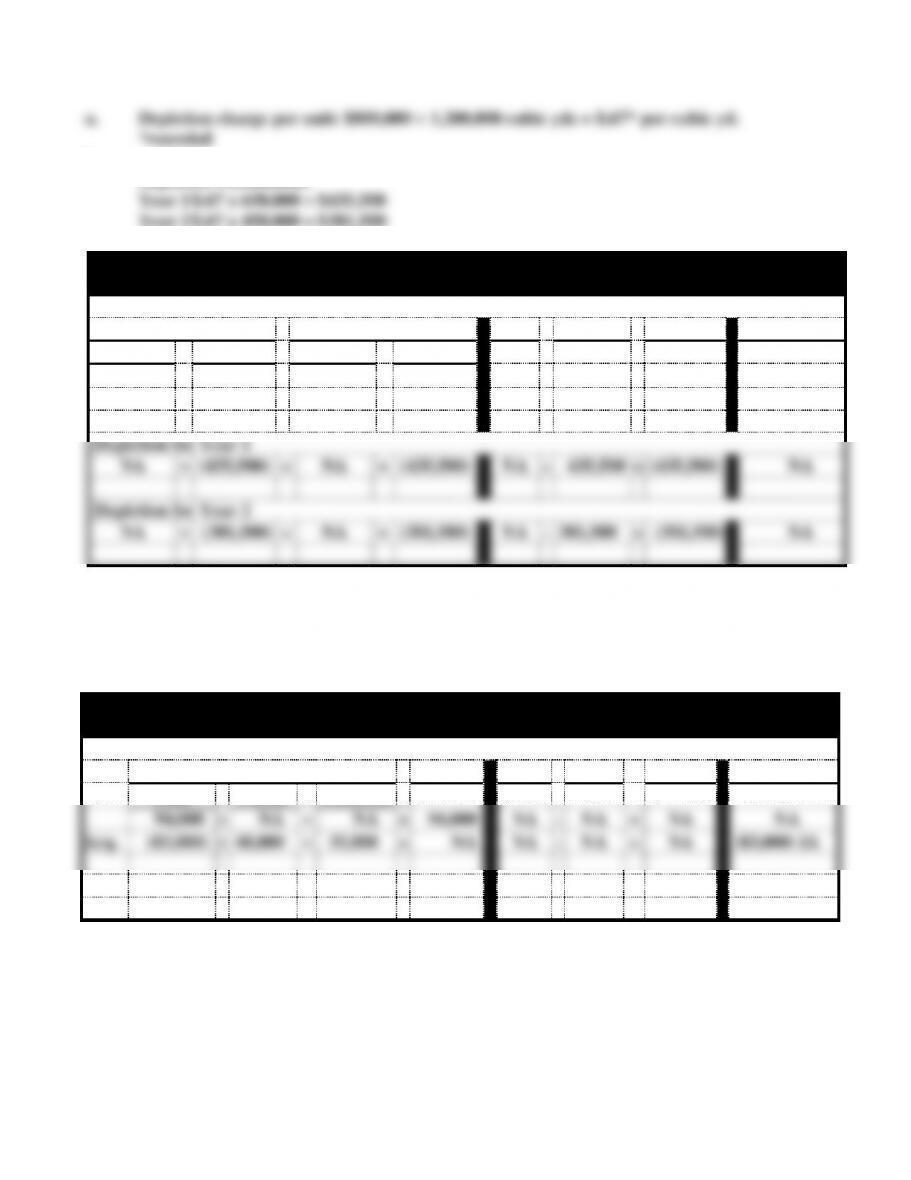

Year 2 $.67 x 450,000 = $301,500

Tishomingo Sand and Gravel

Statements Model

Assets

=

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

+

Sand Res.

=

C. Stock

+

Ret. Ear.

900,000

+

NA

=

900,000

+

NA

NA

−

NA

=

NA

NA

(800,000)

+

800,000

=

NA

+

NA

NA

−

NA

=

NA

(800,000) IA

Depletion for Year 1

NA

+

(435,500)

=

NA

+

(435,500)

NA

−

435,500

=

(435,500)

NA

Depletion for Year 2

NA

+

(301,500)

=

NA

+

(301,500)

NA

−

301,500

=

(301,500)

NA

EXERCISE 6–19

a. Patent $48,000 5 = $9,600 per year

The goodwill is not amortized.

b.

Pacart Manufacturing

Statements Model

Assets

=

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

+

Patent

+

Goodwill

=

94,000

+

NA

+

NA

=

94,000

NA

−

NA

=

NA

NA

Acq.

(83,000)

+

48,000

+

35,000

=

NA

NA

−

NA

=

NA

(83,000) IA

Pat.

NA

+

(9,600)

+

NA

=

(9,600)

NA

−

9,600

=

(9,600)

NA

6-6

EXERCISE 6-20

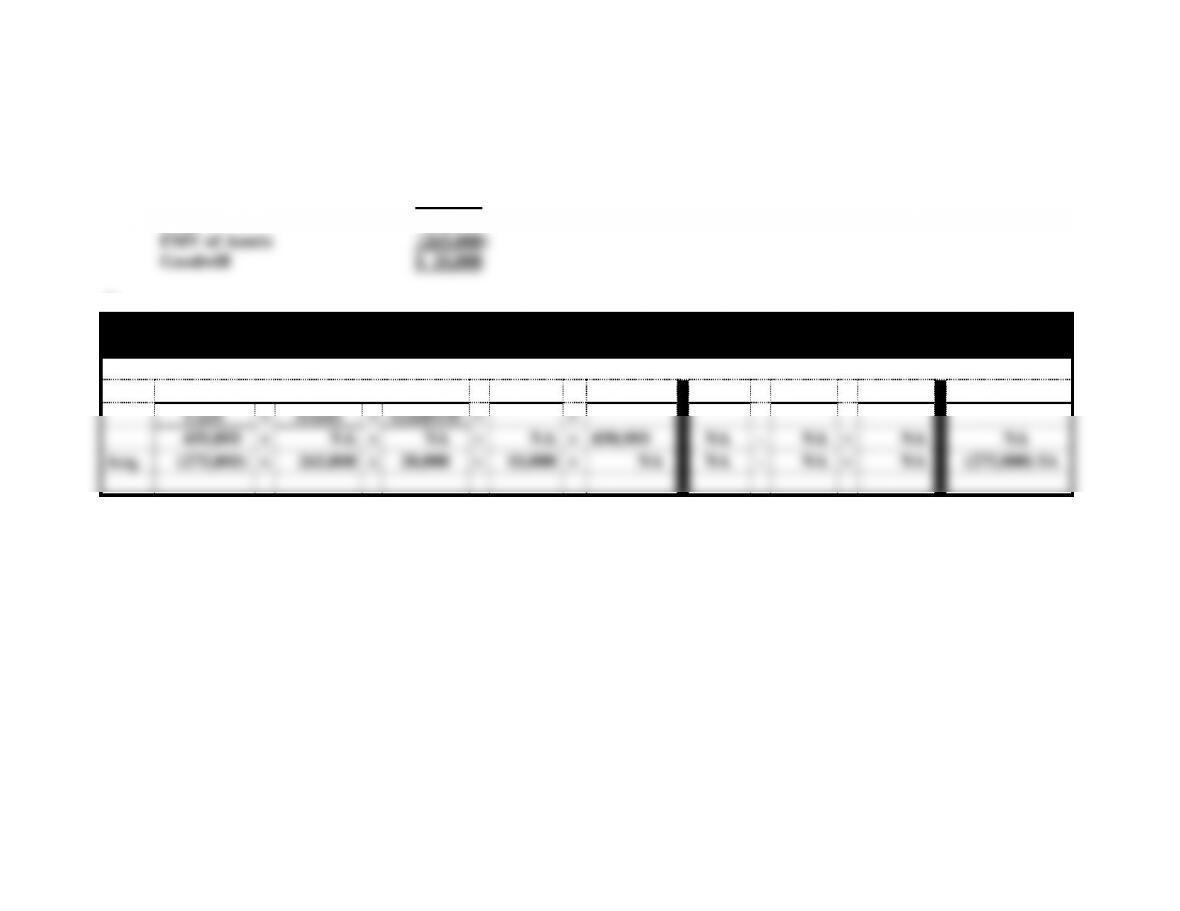

a. Acquisition Price:

Cash Paid $275,000

Liabilities Assumed 10,000

Total 285,000

b.

Yeates Supply Co.

Statements Model

Assets

=

Liab.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

+

Assets

+

Goodwill

=

+

450,000

+

NA

+

NA

=

NA

+

450,000

NA

−

NA

=

NA

NA

Acq.

(275,000)

+

265,000

+

20,000

=

10,000

+

NA

NA

−

NA

=

NA

(275,000) IA

6-7

EXERCISE 6-21

a. Depreciation expense as a percentage of sales:

b. Property, plant and equipment as a percentage of total assets:

c. Company 2 appears to be CSX since one would expect a rail transportation

d. The return on assets ratio (ROA) helps analysts evaluate how efficiently a company

is using its assets. This ratio is computed as: net income ÷ total assets. Although this ratio

Company 1: $57,198 ÷ $1,549,464 = 3.7%

Based on the comparative ROA’s, Company 2, CSX, seems to be managing its assets

more efficiently than American Greetings.

SOLUTIONS TO PROBLEMS – CHAPTER 6

PROBLEM 6-22

Office Equipment:

List Price $50,000

Discount ($50,000 x 1%) (500)

Basket Purchase:

Allocation is based on relative market values:

6-8

Asset

Fair Market

Value

Percent of

FMV

Purchase

Price

Allocated

Costs

Office Furniture

$48,000

60%

x

$70,000

=

$42,000

Copier

12,000

15%

x

70,000

=

10,500

Computers &

Printers

20,000

25%

x

70,000

=

17,500

Total

$80,000

100%

=

$70,000

Land and Building:

Land

Purchase Price $100,000

Demolition of Barn 7,000

Building

Construction Costs $310,00PROBLEM 6-23

a. Straight-line

Cost $25,000

Delivery Cost 500

Total 25,500

b. Units-of-Production

$25,500 − $1,500

1,000,000 = $.024 Per Copy

6-9

c. Double-Declining Balance

Accum. Depreciation Annual

(Cost − at Beginning of Period) x (2 x SL Rate) = Depreciation

Depreciation Calculation:

Straight Line:

Double-Declining Balance:

Company B

2014 ($64,000 − -0-) x (2 x .20) = $25,600

2015 ($64,000 − $25,600) x .4 = 15,360

Units-of-Production:

Company C Depr. Rate: $64,000 − $4,000

200,000 = $.30 per hour

*Limited to remaining depreciable cost: [$64,000 – ($56,700 + $4,000)].

6-10

PROBLEM 6-24 (cont.)

a. Company A – 2014

Revenue $30,000

Depreciation Expense (12,000)

Net Income $18,000

Company C – 2016

Revenue $30,000

Depreciation Expense (12,000)

Net Income $18,000

PROBLEM 6-24 (cont.)

c. Company A Accumulated Depreciation

2014 $12,000

Cost $64,000

6-11

Company B Accumulated Depreciation

2014 $25,600

Cost $64,000

Accumulated Depreciation (50,176)

Book Value $13,824

Company C Accumulated Depreciation

2014 $15,000

d. Company A: Sales (four years) $120,000

Retained Earnings – 2017 $ 72,000

Company B: Sales (four years) $120,000

Company C: Sales (four years) $120,000

Depreciation (four years) (56,700)

Retained Earnings – 2017 $ 63,300

e. The cash flow from operating activities will be the same for each company if income

tax is not considered. Depreciation expense is not a cash flow item.