Chapter 08 – Proprietorships, Partnerships, and Corporations

8-1

General Comments for Chapter 8

Proprietorships, Partnerships, and Corporations

Chapter 8 explains accounting for equity transactions. It describes the three primary forms of

business organizations (sole proprietorship, partnership, and corporation), along with advantages

and disadvantages of each. The chapter illustrates aspects of financial statement reporting

unique to each type of business organization. Finally, it covers common corporate equity topics,

such as par and stated value, issuing stock, common versus preferred stock, stock splits and

dividends, treasury stock, and the use of accounting information in making stock investment

decisions.

Detailed Outline of a Lesson Plan for Chapter 8

I. Demonstration Problem 8-1 illustrates reporting differences among proprietorships,

partnerships, and corporations.

A. Scenario 1. The statements for a proprietorship include two features you should

emphasize. First, the capital account combines the owner’s investments with

earnings that have been retained in the business. Second, proprietorship distributions

are called withdrawals.

B. Scenario 2. Point out that financial statements for a partnership are similar to those

for a proprietorship. Both forms combine capital acquisitions and retained earnings

into single accounts referred to as owners’ capital accounts. The only reporting

difference is that partnership statements present multiple capital accounts (one for

each partner). The amounts in the capital accounts represent the proportionate share

of each partner’s claim on assets.

C. Scenario 3. The financial statements for corporations reflect several differences from

those for proprietorships and partnerships. First, distributions are called dividends.

Next, capital acquisitions and retained earnings are reported in separate accounts.

The owners’ interest in the business is called common stock. You can easily explain

the idea of representing ownership interests with common stock certificates by

referring to them as a type of receipt that recognizes the owners’ contribution of

assets to the business.

II. Demonstration Problem 8-2 illustrates accounting for additional paid-in capital in

excess of par value. You should discuss par value, stated value, and no-par stock before

working the problem. Use the problem to illustrate how contributed capital is divided

into par value and additional paid-in capital in the accounting records. The problem also

illustrates cash dividends, stock dividends, and stock splits. Discuss these issues before

you work the problem.

The problem illustrates seven events. Students should record each event in a

financial statements model. Proceed through the problem step by step. Distribute a copy

Chapter 08 – Proprietorships, Partnerships, and Corporations

8-2

of the work paper to your students and have them work along with you. Explain how

each event affects the statements differently.

III. Introduce preferred stock. Define the terms cumulative and noncumulative with

respect to preferred stock dividends. Use Demonstration Problem 8-3 to illustrate

allocating dividends between common and preferred shareholders.

IV. Use Demonstration Problem 8-4 to illustrate the effects of treasury stock

transactions on financial statements. This problem requires recording five events in a

financial statements model. We again suggest you distribute a copy of the work paper to

students and have them work along with you as you demonstrate how each event affects

the financial statements.

V. Time considerations and homework assignments. Allow at least two hours of class

time to cover owners’ equity and the four demonstration problems. Use Problem 8-18 to

reinforce how financial statement presentation reflects business structure. Problem 8-20

requires students to record a variety of stock and dividend transactions. Use Exercise 8-

11 to reinforce computing cumulative preferred dividends. Treasury stock is covered in

Problems 8-19 and 8-21.

Demonstration Problems for Chapter 8

Demonstration Problem 8-1: Forms of Business Organization

Assume a business was started on January 1, 2014 when it acquired $60,000 cash from its

owner(s). During 2014 the company generated $29,000 of cash service revenue, incurred

$19,000 of cash expenses, and distributed $4,000 cash to the owner(s).

Required

Prepare an income statement, a statement of changes in equity, and a balance sheet for each of

the three alternative scenarios described below. The statement of changes in equity is called a

capital statement for proprietorships and partnerships. It is called a statement of changes in

stockholders’ equity for corporations.

1. Sally Russell formed the business as a sole proprietorship.

2. Carl Link and Bill Morgan established the business as a partnership. Link contributed 60

percent of the capital and Morgan contributed the remaining 40 percent. The partners

agreed to share profits and make withdrawals in proportion to their capital investments.

3. The business was established as a corporation. It issued 1,000 shares of no-par common

stock for $60 per share.

Demonstration Problem 8- 2: Equity Transactions

Chapter 08 – Proprietorships, Partnerships, and Corporations

8-4

4. Purchased 500 shares of Griffin stock (treasury stock) at a price of $10 per share.

5. Sold (reissued) 200 shares of the treasury stock at a price of $13 per share.

Required

Record the events in a financial statements model.

SOLUTIONS TO

DEMONSTRATION PROBLEMS

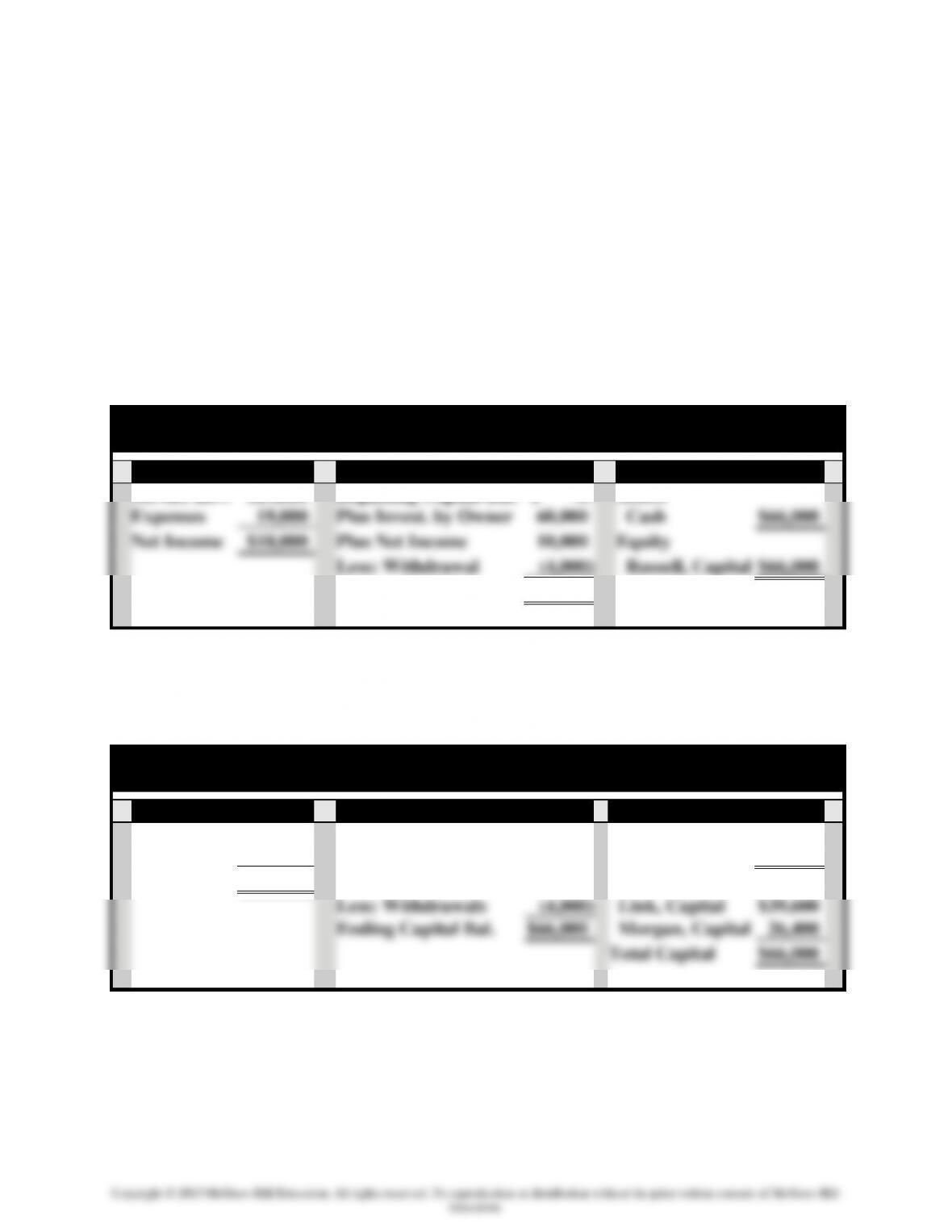

Demonstration Problem 8-1: Solution, Scenario 1

Financial Statements for Russell Sole Proprietorship

For 2014

Income Statement

Capital Statement

Balance Sheet, 12/31

Service Rev.

$29,000

Beginning Capital Bal.

$ -0-

Assets

Expenses

19,000

Plus Invest. by Owner

60,000

Cash

$66,000

Net Income

$10,000

Plus Net Income

10,000

Equity

Less: Withdrawal

(4,000)

Russell, Capital

$66,000

Ending Capital Bal.

$66,000

Demonstration Problem 8-1: Solution, Scenario 2

Financial Statements for Link/Morgan Partnership

For 2014

Income Statement

Capital Statement

Balance Sheet, 12/31

Service Rev.

$29,000

Beginning Capital Bal.

$ -0-

Assets

Expenses

19,000

Plus Invest. by Owners

60,000

Cash

$66,000

Net Income

$10,000

Plus Net Income

10,000

Partners’ Capital

Less: Withdrawals

(4,000)

Link, Capital

$39,600

Ending Capital Bal.

$66,000

Morgan, Capital

26,400

Total Capital

$66,000

Chapter 08 – Proprietorships, Partnerships, and Corporations

8-5

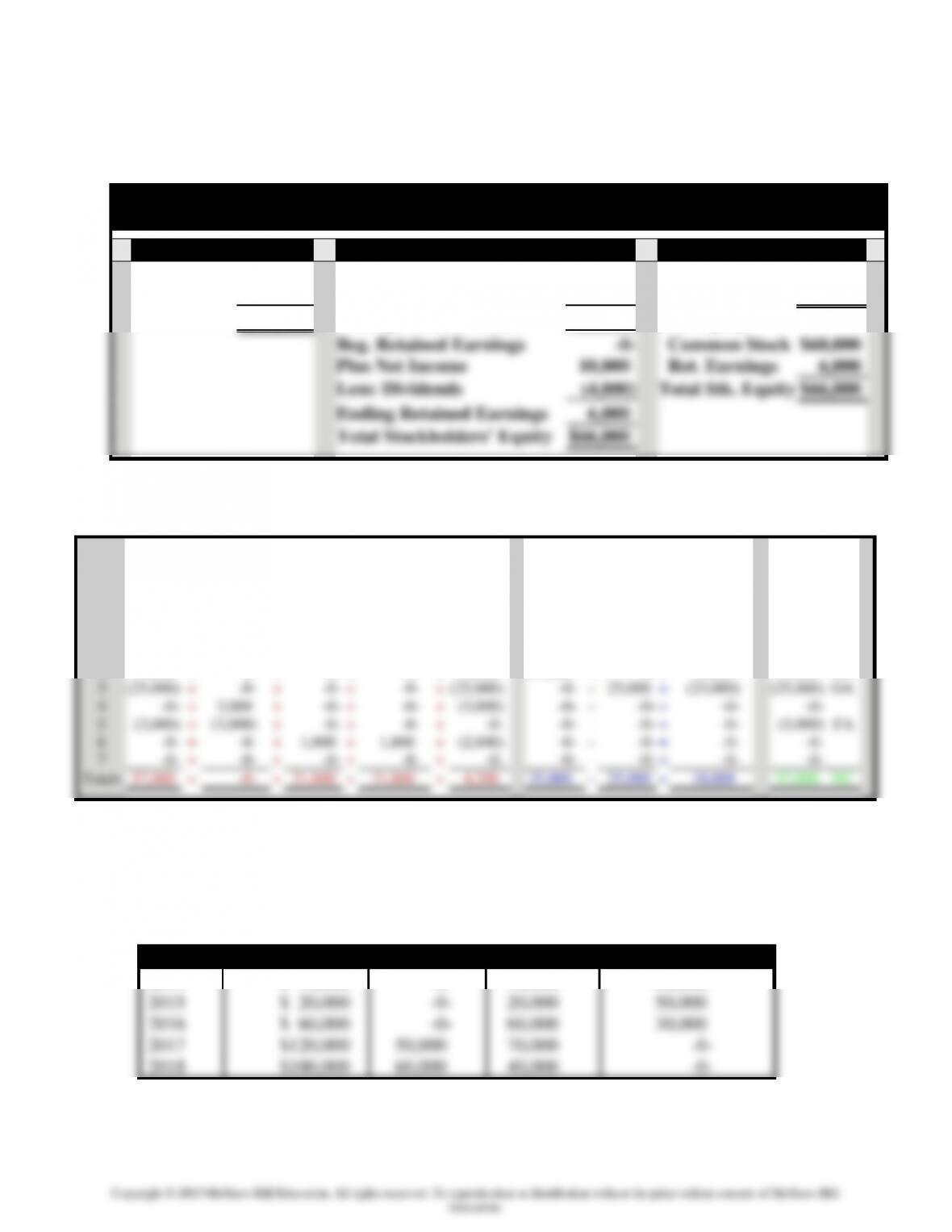

Demonstration Problem 8-1: Solution, Scenario 3

Financial Statements for Corporation

For 2014

Income Statement

Statement of Changes in Stk. Equity

Balance Sheet, 12/31

Service Rev.

$29,000

Beginning Common Stock

$ -0-

Assets

Expenses

19,000

Plus Common Stock Issued

60,000

Cash

$66,000

Net Income

$10,000

Ending Common Stock

60,000

Stk. Equity

Beg. Retained Earnings

-0-

Common Stock

$60,000

Plus Net Income

10,000

Ret. Earnings

6,000

Less: Dividends

(4,000)

Total Stk. Equity

$66,000

Ending Retained Earnings

6,000

Total Stockholders’ Equity

$66,000

Demonstration Problem 8- 2: Solution

Assets

=

Liabilities

+

Stockholders’ Equity

Event

Cash

=

Dividends

Payable

+

C. Stock

Par

Value

+

Additional

Paid-in

Capital

+

Retained

Earnings

Revenue

−

Expense

=

Net Income

Cash Flow

Beg.

Bal.

-0-

=

-0-

+

-0-

+

-0-

+

-0-

-0-

–

-0-

=

-0-

-0-

1

50,000

=

-0-

+

20,000

+

30,000

+

-0-

-0-

–

-0-

=

-0-

50,000 FA

2

35,000

=

-0-

+

-0-

+

-0-

+

35,000

35,000

–

-0-

=

35,000

35,000 OA

3

(25,000)

=

-0-

+

-0-

+

-0-

+

(25,000)

-0-

–

25,000

=

(25,000)

(25,000) OA

4

-0-

=

3,000

+

-0-

+

-0-

+

(3,000)

-0-

–

-0-

=

-0-

-0-

5

(3,000)

=

(3,000)

+

-0-

+

-0-

+

-0-

-0-

–

-0-

=

-0-

(3,000) FA

6

-0-

=

-0-

+

1,000

+

1,800

+

(2,800)

-0-

–

-0-

=

-0-

-0-

7

-0-

=

-0-

+

-0-

+

-0-

+

-0-

-0-

–

-0-

=

-0-

-0-

Totals

57,000

=

-0-

+

21,000

+

31,800

+

4,200

35,000

–

25,000

=

10,000

57,000 NC

Demonstration Problem 8- 3: Solution, part a.

Cumulative Preferred

Year

Total Dividends

To Common

To Preferred

Dividends in Arrears

2014

$ 10,000

-0-

10,000

30,000

2015

$ 20,000

-0-

20,000

50,000

2016

$ 60,000

-0-

60,000

30,000

2017

$120,000

50,000

70,000

-0-

2018

$100,000

60,000

40,000

-0-

Chapter 08 – Proprietorships, Partnerships, and Corporations

8-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

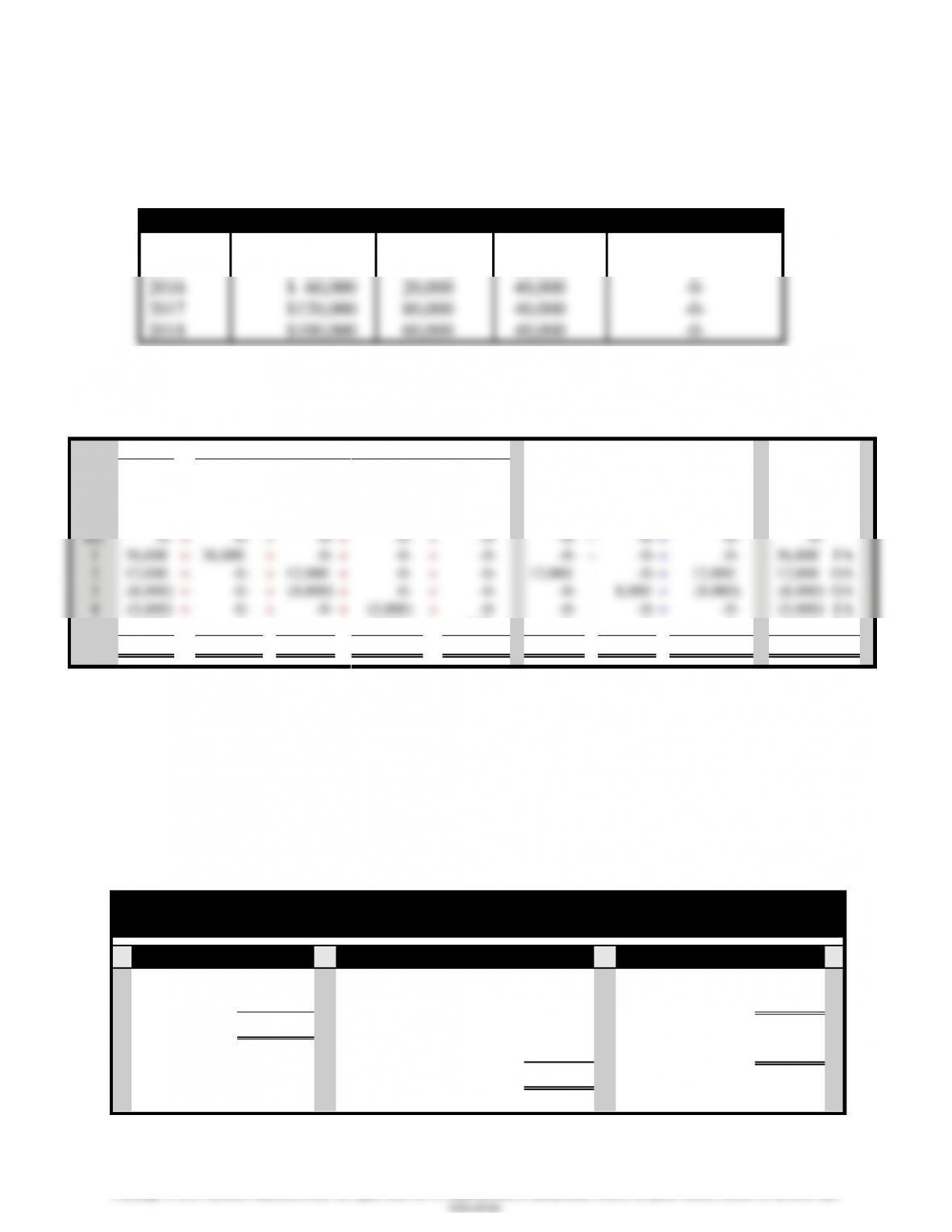

Demonstration Problem 8- 3: Solution, part b.

Noncumulative Preferred

Year

Total Dividends

To Common

To Preferred

Dividends in Arrears

2014

$ 10,000

-0-

10,000

-0-

2015

$ 20,000

-0-

20,000

-0-

2016

$ 60,000

20,000

40,000

-0-

2017

$120,000

80,000

40,000

-0-

2018

$100,000

60,000

40,000

-0-

Demonstration Problem 8- 4: Solution

Assets

=

Stockholders’ Equity

Event

Cash

=

No–par

C. Stock

+

Retained

Earnings

+

Treasury

Stock

+

Paid-in

Capital

Tres. Stk

Revenue

−

Expense

=

Net Income

Cash Flow

Beg.

Bal.

-0-

=

-0-

+

-0-

+

-0-

+

-0-

-0-

–

-0-

=

-0-

-0-

1

36,000

=

36,000

+

-0-

+

-0-

+

-0-

-0-

–

-0-

=

-0-

36,000 FA

2

12,000

=

-0-

+

12,000

+

-0-

+

-0-

12,000

–

-0-

=

12,000

12,000 OA

3

(8,000)

=

-0-

+

(8,000)

+

-0-

+

-0-

-0-

–

8,000

=

(8,000)

(8,000) OA

4

(5,000)

=

-0-

+

-0-

+

(5,000)

+

-0-

-0-

–

-0-

=

-0-

(5,000) FA

5

2,600

=

-0-

+

+

2,000

+

600

-0-

–

-0-

=

-0-

2,600 FA

Totals

37,600

=

36,000

+

4,000

+

(3,000)

+

600

12,000

–

8,000

=

4,000

37,600 NC

WORK PAPERS FOR

DEMONSTRATION PROBLEMS

Demonstration Problem 8-1: Work Paper, Scenario 1

Financial Statements for Russell Sole Proprietorship

For 2014

Income Statement

Capital Statement

Balance Sheet, 12/31

Service Rev.

Beginning Capital Bal.

Assets

Expenses

Plus Invest. by Owner

Cash

Net Income

Plus Net Income

Equity

Less: Withdrawal

Russell, Capital

Ending Capital Bal.

Chapter 08 – Proprietorships, Partnerships, and Corporations

8-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Demonstration Problem 8-1: Work Paper, Scenario 2

Financial Statements for Link/Morgan Partnership

For 2014

Income Statement

Capital Statement

Balance Sheet

Service Rev.

Beginning Capital Bal.

Assets

Expenses

Plus Invest. by Owners

Cash

Net Income

Plus Net Income

Partners’ Capital

Less: Withdrawals

Link, Capital

Ending Capital Bal.

Morgan, Capital

Total Capital

Demonstration Problem 8-1: Work Paper, Scenario 3

Financial Statements for Corporation

For 2014

Income Statement

Statement of Changes in Stk. Equity

Balance Sheet, 12/31

Service Rev.

Beginning Common Stock

Assets

Expenses

Plus Common Stock Issued

Cash

Net Income

Ending Common Stock

Stk. Equity

Beg. Retained Earnings

Common Stock

Plus Net Income

Ret. Earnings

Less: Dividends

Total Stk. Equity

Ending Retained Earnings

Total Stockholders’ Equity

Demonstration Problem 8- 2: Work Paper

Assets

=

Liabilities

+

Stockholders’ Equity

Event

Cash

=

Dividends

Payable

+

C. Stock

Par

Value

+

Additional

Paid-in

Capital

+

Retained

Earnings

Revenue

−

Expense

=

Net Income

Cash Flow

Beg.

Bal.

=

+

+

+

–

=

1

=

+

+

+

–

=

2

=

+

+

+

–

=

3

=

+

+

+

–

=

4

=

+

+

+

–

=

5

=

+

+

+

–

=

6

=

+

+

+

–

=

Chapter 08 – Proprietorships, Partnerships, and Corporations

8-8

7

=

+

+

+

–

=

Totals

57,000

=

-0-

+

21,000

+

31,800

+

4,200

35,000

–

25,000

=

10,000

57,000 NC

Demonstration Problem 8- 3: Work Paper, part a.

Cumulative Preferred

Year

Total Dividends

To Common

To Preferred

Dividends in Arrears

2014

$ 10,000

2015

$ 20,000

2016

$ 60,000

2017

$120,000

2018

$100,000

Demonstration Problem 8- 3: Work Paper, part b.

Noncumulative Preferred

Year

Total Dividends

To Common

To Preferred

Dividends in Arrears

2014

$ 10,000

2015

$ 20,000

2016

$ 60,000

2017

$120,000

2018

$100,000

Demonstration Problem 8- 4: Work Paper

Assets

=

Stockholders’ Equity

Event

Cash

=

No–par

C. Stock

+

Retained

Earnings

+

Treasury

Stock

+

Paid-in

Capital

Tres. Stk

Revenue

−

Expense

=

Net Income

Cash Flow

Beg.

Bal.

=

+

+

+

–

=

1

=

+

+

+

–

=

2

=

+

+

+

–

=

3

=

+

+

+

–

=

4

=

+

+

+

–

=

5

=

+

+

+

–

=

Totals

37,600

=

36,000

+

4,000

+

(3,000)

+

600

12,000

–

8,000

=

4,000

37,600 NC

Quiz Questions for Chapter 8

Chapter 08 – Proprietorships, Partnerships, and Corporations

1. The ZZ Corporation had the following shares of stock outstanding at December 31, 2014: Common Stock,

$50 par value, 40,000 shares outstanding; and Preferred Stock, 6 percent, $100 par value, cumulative, 10,000

shares outstanding. Dividends for 2012 and 2013 were in arrears. On December 31, 2014, ZZ declared total

cash dividends of $250,000. The total amounts payable to preferred stockholders and common stockholders,

respectively, are:

a. $60,000 / $190,000.

b. $120,000 / $130,000.

c. $125,000 / $125,000.

d. $180,000 / $70,000.

Use the following information to answer the next four questions. The Kramer Company was started when it

issued 200 shares of $5 par value common stock at a market price of $20 per share. The company repurchased 10

shares at a market price of $15 per share. Later the company reissued 5 shares at a market price of $20 per share.

At the end of the first year of operations the company’s equity included $1,200 of retained earnings in addition to its

contributed capital.

2. The original issue of 200 shares of stock would

a. increase cash by $4,000 / increase common stock by $4,000.

b. increase cash by $4,000 / increase common stock and paid-in capital in excess of par value by $1,000 and

$3,000, respectively.

c. decrease cash by $4,000 / increase common stock by $4,000.

d. increase cash by $1,000 / increase common stock by $1,000.

3. The entry to record the purchase of the 10 shares of the company’s own stock would

a. decrease assets / decrease equity.

b. decrease assets / increase equity.

c. decrease assets / increase treasury stock.

d. both a and c.

4. What effect would reissuing the 5 shares have on the company’s paid-in capital from treasury stock transac-

tions account?

a. No effect.

b. Increase additional paid-in capital by $100.

c. Increase additional paid-in capital by $25.

d. Decrease additional paid-in capital by $75.

5. The total amount of stockholders’ equity at the end of the first year would be

a. $5,150.

b. $5,200.

c. $1,200.

d. none of the above.

6. Which of the following is an advantage of the corporate form of business organization?

a. double taxation.

b. amount of regulation.

c. limited liability.

d. entrenched management.

8-10

7. Jan Irving started a proprietorship on January 1, 2014 with a $1,000 cash contribution to the business. During

the first year of operations the company generated $5,000 of cash revenue and incurred $2,000 of cash ex-

penses. Also, Jan withdrew $500 from the business. At the end of 2014 the balance in the Jan Irving, Capital

account was

a. $1,000.

b. $3,000.

c. $3,500.

d. $4,000.

8. ABC Company is authorized to issue 100,000 shares of common stock. The company issued 60,000 shares

of common stock and later repurchased 15,000 shares of its own common stock. How many shares are out-

standing?

a. 60,000.

b. 45,000.

c. 100,000.

d. 40,000.

9. An 8 percent stock dividend on 12,000 shares of outstanding common stock with a par value of $20 per share

and a market value of $60 a share will have what effect on the accounting equation?

a. Increase common stock by $57,600.

b. Increase cash by $38,400.

c. Decrease retained earnings by $19,200.

d. Decrease retained earnings by $57,600.

10. Which of the following statements concerning a two-for-one stock split is true?

a. The number of shares outstanding will decrease.

b. The market price of the stock would be expected to increase.

c. The company’s assets will decrease.

d. The amount of stockholders’ equity is not affected.

11. EFG Company paid cash to purchase treasury stock. Which of the following reflects how this event affects

the company’s financial statements?

Assets

=

Liab.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

a.

−

NA

−

NA

NA

NA

− FA

b.

+ −

NA

NA

NA

NA

NA

− OA

c.

−

NA

−

NA

+

−

− FA

d.

+ −

NA

NA

NA

+

−

− OA

12. ZGAR Company distributed a stock dividend. Which of the following reflects how this event affects the

company’s financial statements?

Assets

=

Liab.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

a.

−

NA

−

NA

NA

NA

NA

b.

NA

NA

+ −

NA

NA

NA

NA

c.

−

NA

−

NA

+

−

− FA

d.

NA

NA

+ −

NA

NA

NA

− FA

Solutions to Quiz Questions

Chapter 08 – Proprietorships, Partnerships, and Corporations

8-11

Question

Answer

1

D

2

B

3

D

4

C

5

A

6

C

7

C

8

B

9

D

10

D

11

A

12

B

Summary Outline of a Lesson Plan for Chapter 8

I. Use Demonstration Problem 8-1 to illustrate reporting differences among

proprietorships, partnerships, and corporations.

II. Demonstration Problem 8-2 illustrates accounting for additional paid-in capital in

excess of par value.

III. Introduce preferred stock. Use Demonstration Problem 8-3 to illustrate allocating

dividends between common and preferred shareholders.

IV. Use Demonstration Problem 8-4 to illustrate the effects of treasury stock

transactions on financial statements.

V. Time considerations and homework assignments. Allow approximately two hours of

class time to cover the four demonstration problems. Use Problem 8-18 to reinforce how

financial statement presentation reflects business structure. Problem 8-20 requires

students to record a variety of stock and dividend transactions. Use Exercise 8-11 to

reinforce computing cumulative preferred dividends. Treasury stock is covered in

Problems 8-19 and 8-21.