12. What amount of sales in dollars must Boxware achieve each month in order to break even?

a. $95,000

b. $190,000

c. $285,000

d. $380,000

13. How many units per month must Boxware sell in order to make a $110,000 profit?

a. 500

b. 1,000

c. 1,500

d. 2,000

Use the following information to answer the next three questions: Derek’s Drum Depot (DDD)

wants to add a new line of drumsticks to its product line. The following data apply to the new

drumsticks line.

Budgeted sales 30,000 sets per year

Sales price $5 per set

Variable costs $3 per set

Fixed costs $10,000 per year

14. The break-even point for the new line is _______ sets per year.

a. 500 sets

b. $5,000

c. 15,000 sets

d. 5,000 sets

15. The margin of safety for DDD is

a. 83%

b. 15,000 sets

c. 19%

d. 6,000 sets

16. How many sets of drumsticks must DDD sell to make a profit of $50,000 on the new line?

a. 2,000 units

b. 10,000 units

c. 20,000 units

d. 30,000 units

Use the following data for Fireware Software Corporation to answer the next three questions:

Sales price per unit $44.95

Variable manufacturing cost per unit $17.03

Variable sales commissions per unit $ 3.20

Variable shipping expense per unit $ 1.14

Fixed administrative cost, per month $12,200

Other fixed costs, per month $2,269

Average production 2,100 units per month

17. What is the amount of contribution margin per unit, based on this information?

a. $21.37

b. $23.58

c. $27.92

d. $24.72

18. How many units must Fireware sell in order to break even? (round to the nearest whole unit)

a. 308

b. 500

c. 614

d. 620

19. How many units must Fireware sell in order to make a $50,000 profit? (Round to the nearest whole unit.)

a. 505

b. 1,090

c. 1,708

d. 2,734Solutions to Quiz Questions

Question

Answer

1

A

2

B

3

C

4

D

5

B

6

C

7

C

8

B

9

C

10

B

11

A

12

A

13

C

14

D

15

A

16

D

17

B

18

C

19

D

Demonstration Problems for Chapter 11

Demonstration Problem 11-1

Applying Cost Behavior Concepts to Business Decisions

Art On Tour, Inc. (AOTI) contracts with artists to exhibit their work to the public. AOTI has

agreed to pay a well known artist a $20,000 commission for the right to exhibit his work for one

month.

Required

Part a – Identifying Cost Behavior

1. Determine the total commission cost and the commission cost per person if 1,000, 2,000, or

4,000 people attend the exhibition. Is the commission cost fixed or variable?

2. AOTI sells to patrons books illustrating the artist’s work. The books cost AOTI $5 each.

Determine the total cost of books and the cost per person if 1,000, 2,000, or 4,000 people attend

the exhibition and wish to purchase the books. Is the book cost fixed or variable?

Part b – Operating Leverage and Risk/Reward Relationship

1. AOTI pays an artist a $20,000 commission. It sells 4,000 tickets at $6 each. Prepare an income

statement. Then prepare revised income statements assuming 10 percent more than 4,000 and

10 percent fewer than 4,000 patrons attend the exhibition. Calculate the percentage changes

in revenue and net income if attendance increases or decreases 10 percent.

2. Alternatively, AOTI pays the artist a commission of $5 per ticket sold. It sells 4,000 tickets at

$6 each. Prepare an income statement. Then prepare revised income statements assuming 10

percent more than 4,000 and 10 percent fewer than 4,000 patrons attend the exhibition.

Calculate the percentage change in revenue and net income if attendance increases or decreases

10 percent.

Part c —Fixed and Variable Cost Definitions are Context Sensitive

1. AOTI pays the artist a commission of $20,000 per exhibition. What is the total commission

cost and the commission cost per person if 1,000, 2,000, or 4,000 people attend the exhibition?

(Same as part a.1.)

2. AOTI pays the artist a commission of $20,000 per exhibition. What is the total commission

cost and the commission cost per exhibition if AOTI sponsors 1, 2, or 3 exhibitions?

Demonstration Problem 11-2 Effect of Cost Structure

My Company / Your Company

My Company and Your Company provide rafting tours on Big Bear River. My Company pays

tour guides fixed salaries. It budgets salaries expense at $160,000 per year. Your Company pays

tour guides $40 per rafter served. Rafters are charged $50 per tour. Both companies expect to

carry approximately 4,000 rafters during the year.

Required

a. Prepare budgeted annual income statements for the two companies.

b. In an effort to lure rafters away from Your Company, My Company lowers the price per rafter

to $39. Prepare revised income statements for both companies. Assume that My Company

serves 6,000 rafters who each pay $39 per tour, while Your Company serves only 2,000 rafters

who pay $50 per tour.

c. Assume you are president of Your Company. Offer defensive strategies.

d. Suppose Your Company matches the $39 price set by My Company. Prepare income

statements for both companies assuming that each company serves 4,000 customers.

Demonstration Problem 11-3 Effect of Operating Leverage

Sharon Virgil owns a delivery service company. She charges customers $10 per delivery. The

company’s variable expenses average $2 per delivery and fixed costs are $600 per month. Ms.

Virgil provided 100 deliveries during the most recent month.

Required

a. Prepare an income statement using a contribution margin format.

b. Determine the magnitude of operating leverage. Use your answer to determine the percentage

change in net income if sales increase by 10%.

c. Assume that sales increase by 10% (deliveries increase to 110). Prepare a contribution margin

format income statement assuming 110 deliveries. Calculate the percentage change in net income

and compare your answer with your solution to part b.

Demonstration Problem 11-4 Cost-Volume-Profit Analysis

Jeff Jamail is evaluating a business opportunity to sell cookware at trade shows. Mr. Jamail can

buy the cookware at a wholesale cost of $210 per set. He plans to sell the cookware for $350 per

set. He estimates fixed costs such as plane fare, booth rental cost, and lodging to be $5,600 per

trade show.

Required

a. Determine the number of cookware sets Mr. Jamail must sell at a trade show to break even

(zero profit or loss). Use the following structure to answer this question:

(1) Contribution Margin Per Unit Approach:

a. Determine the amount of the contribution margin per unit.

b. Explain that when the total contribution margin is sufficient to pay for the fixed cost,

Mr. Jamail will break even. Show the computation of break-even in units.

c. Show how to compute the break-even point in number of dollars using the break-even

point in units and the selling price.

d. Confirm the results by preparing an income statement.

(2) Contribution Margin Ratio Approach.

a. Calculate the contribution margin ratio.

b. Use the ratio to calculate the break-even point in sales dollars, then use the results and

the selling price to calculate the break-even point in units.

(3) Equation Approach.

a. Calculate the break-even point in units.

b. Calculate the break-even point in sales dollars.

b. Assume Mr. Jamail desires to earn a profit of $4,900 per show.

(1) Determine the sales volume in units (sets of cookware) necessary to earn the desired profit.

(2) Determine the sales volume in dollars necessary to earn the desired profit.

(3) Using the contribution margin format, prepare an income statement to confirm your

answers to parts 1 and 2.

c. Determine the margin of safety between the sales volume at the break-even point and the sales

volume required to earn the desired profit. Determine the margin of safety both in sales

dollars and as a percentage.

d. After researching the market, Mr. Jamail concludes that the $350 per set selling price is too

high. Customers will likely pay only $310 per set. Mr. Jamail believes he can obtain a cost

reduction from his supplier of $20 per set (variable cost drops from $210 per set to $190 per

set) and still provide the level of quality required to achieve a sales volume of 75 sets. Under

these circumstances, what amount of fixed costs can Mr. Jamail incur and still obtain the

target profit of $4,900? Support your answer with appropriate computations.

Demonstration Problem 11-1 Solution

a.1.

Number of People Attending (a)

1,000

2,000

4,000

Total Commission Cost (b)

$20,000

$20,000

$20,000

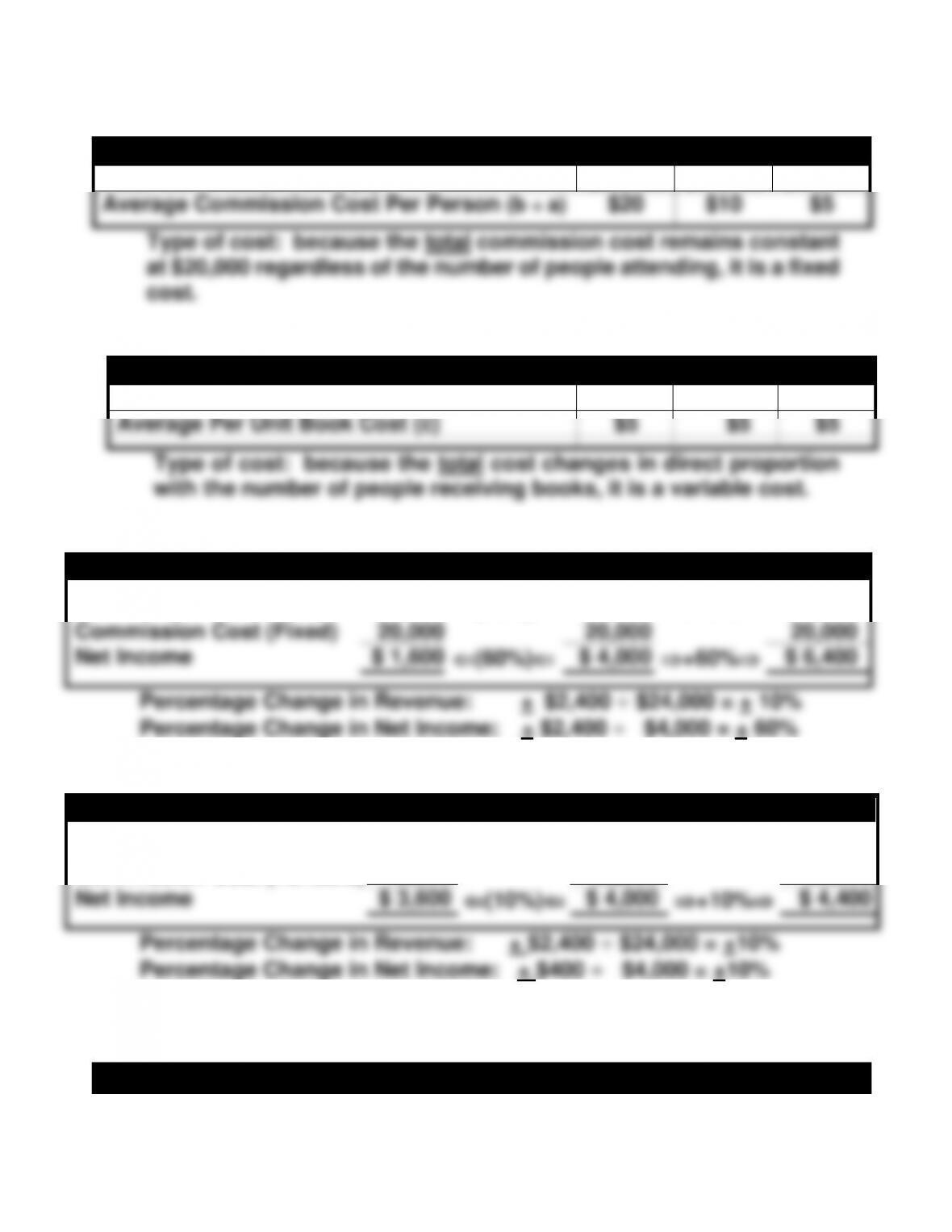

Average Commission Cost Per Person (b ÷ a)

$20

$10

$5

Type of cost: because the total commission cost remains constant

at $20,000 regardless of the number of people attending, it is a fixed

cost.

a.2.

Number of People Attending (a)

1,000

2,000

4,000

Total Cost of Books [b=(a x c)]

$5,000

$10,000

$20,000

Average Per Unit Book Cost (c)

$5

$5

$5

Type of cost: because the total cost changes in direct proportion

with the number of people receiving books, it is a variable cost.

b.1.

Number of Tickets Sold

3,600

% Change

4,000

% Change

4,400

Revenue ($6 Per Ticket)

$21,600

(10%)

$24,000

+10%

$26,400

Commission Cost (Fixed)

20,000

20,000

20,000

Net Income

$ 1,600

(60%)

$ 4,000

+60%

$ 6,400

Percentage Change in Revenue: + $2,400 ÷ $24,000 = + 10%

Percentage Change in Net Income: + $2,400 ÷ $4,000 = + 60%

b.2.

Number of Tickets Sold

3,600

% Change

4,000

% Change

4,400

Revenue ($6 Per Ticket)

$21,600

(10%)

$24,000

+10%

$26,400

Commission Cost (Variable)

18,000

20,000

22,000

Net Income

$ 3,600

(10%)

$ 4,000

+10%

$ 4,400

Percentage Change in Revenue: + $2,400 ÷ $24,000 = +10%

Percentage Change in Net Income: + $400 ÷ $4,000 = +10%

Demonstration Problem 11-1 Solution continued

c.1. (Same as part a.1.)

Number of People Attending (a)

1,000

2,000

4,000

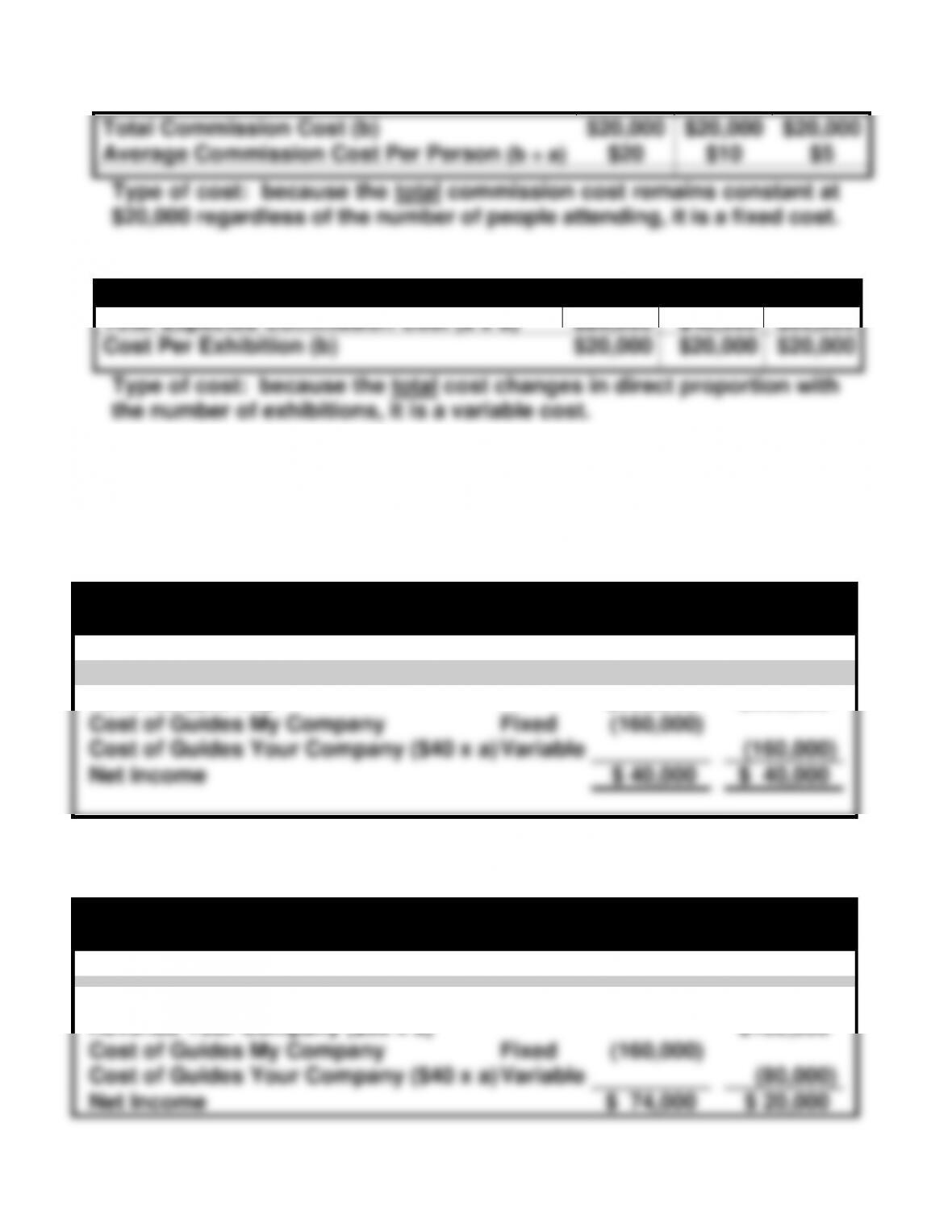

Total Commission Cost (b)

$20,000

$20,000

$20,000

Average Commission Cost Per Person (b ÷ a)

$20

$10

$5

Type of cost: because the total commission cost remains constant at

$20,000 regardless of the number of people attending, it is a fixed cost.

c.2.

Number of Exhibitions (a)

1

2

3

Total Expected Commission Cost (a x b)

$20,000

$40,000

$60,000

Cost Per Exhibition (b)

$20,000

$20,000

$20,000

Type of cost: because the total cost changes in direct proportion with

the number of exhibitions, it is a variable cost.

Note carefully, a given cost (the artist’s commission) can be fixed or

variable depending upon the context.Demonstration Problem 11-2

Solution

a.

My

Company

Your

Company

Number of Rafters (a)

4,000

4,000

Revenue ($50 x a)

$200,000

$200,000

Cost of Guides My Company

Fixed

(160,000)

Cost of Guides Your Company ($40 x a)

Variable

(160,000)

Net income

$ 40,000

$ 40,000

b.

My

Company

Your

Company

Number of Rafters (a)

6,000

2,000

Revenue My Company ($39 x a)

$234,000

Revenue Your Company ($50 x a)

$100,000

Cost of Guides My Company

Fixed

(160,000)

Cost of Guides Your Company ($40 x a)

Variable

(80,000)

Net Income

$ 74,000

$ 20,000

My Company was able to increase total revenue because the decrease

in price was offset by an increase in volume. In other words, 6,000

customers paying $39 each produce more revenue ($234,000) than do

Company out of business. My Company stands to gain an additional

$78,000 ($39 x 2,000) of revenue when it takes over Your Company’s

c.

The most common strategy students offer is to create product

differentiation. Many variations of this strategy are possible. Your

Company could use a different type of raft, travel different routes,

Students also commonly suggest cutting costs by paying the tour

guides less. Students often offer strategies involving employees

Occasionally someone suggests a merger. The merged company

could retain the salaried tour guides and dismiss those paid on a

The response that applies most directly to the subject of cost behavior

is for Your Company to match My Company’s price and hold firm. As

d.

My

Company

Your

Company

Number of Rafters (a)

4,000

4,000

Revenue ($39 x a)

$156,000

$156,000

Cost of Guides My Company

Fixed

(160,000)

Cost of Guides Your Company ($40 x a)

Variable

(160,000)

Net Loss

$ (4,000)

$ (4,000)

Demonstration Problem 11-3 Solution

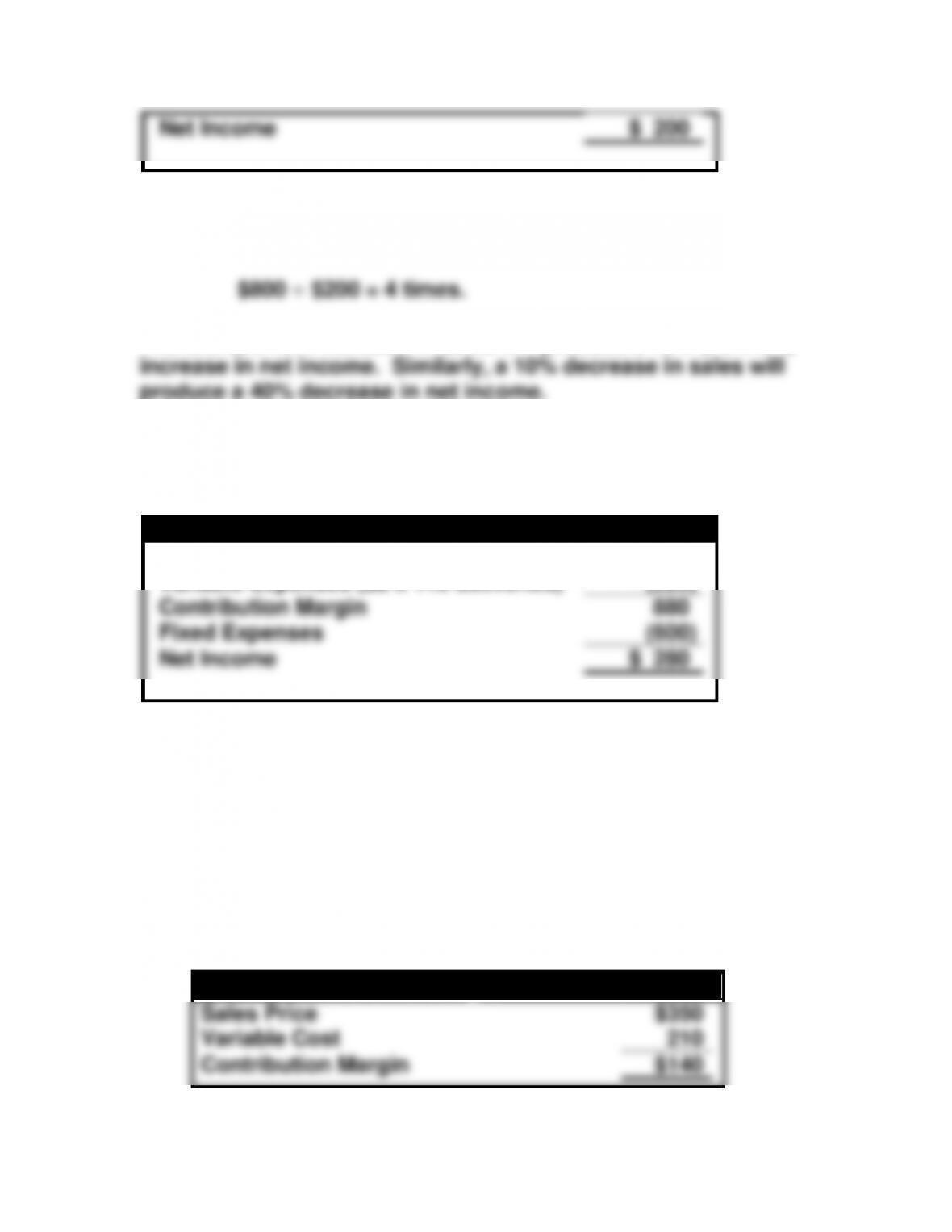

a. Income Statement Using a Contribution Margin Format, Volume

of 100 Deliveries

Revenue ($10 x 100 deliveries)

$1,000

Variable Expenses ($2 x 100 deliveries)

(200)

Contribution Margin

800

Fixed Expenses

(600)

Net Income

$ 200

b. Magnitude of Operating Leverage = Contribution Margin ÷ Net

Income:

Therefore, a 10% increase in sales will produce a 40% (10% x 4)

c. Income Statement Using a Contribution Margin Format, Volume

of 110 Deliveries

Revenue ($10 x 110 deliveries)

$1,100

Variable Expenses ($2 x 110 deliveries)

(220)

Contribution Margin

880

Fixed Expenses

(600)

Net Income

$ 280

(Alternative Net Income − Base Net Income) ÷ Base

($280 − $200) ÷ $200 = 40%

The answer to part c confirms the answer determined in part b.

Demonstration Problem 11-4 Solution

a. Break-even point

(1) Contribution Margin Per Unit Approach

(a) Determine the contribution margin per unit.

Per Unit Contribution Margin

Sales Price

$350

Variable Cost

210

Contribution Margin

$140

(b) When the total contribution margin is sufficient to pay for the

fixed costs, Mr. Jamail will break even. The number of units

required to break even can be computed as follows:

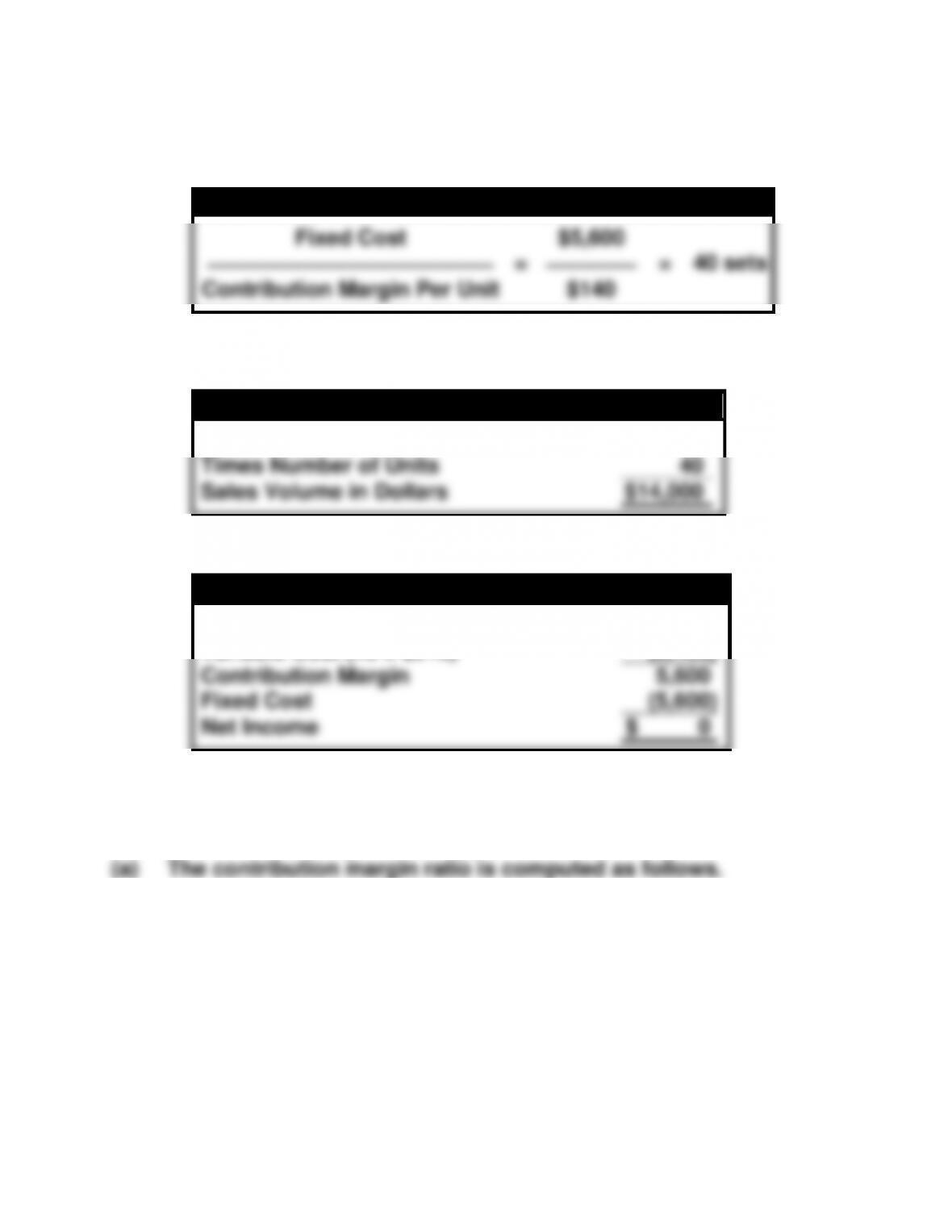

Formula for Computation of Break-Even Point in Units

Fixed Cost

$5,600

⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯

=

⎯⎯⎯⎯

=

40 sets

Contribution Margin Per Unit

$140

(c) The break-even point in number of dollars can be computed as

follows:

Break-Even Point in Sales Dollars

Sales Price Per Unit

$ 350

Times Number of Units

40

Sales Volume in Dollars

$14,000

(d) Confirm the results by preparing an income statement.

Income Statement

Sales (40 x $350)

$14,000

Variable Cost (40 x $210)

(8,400)

Contribution Margin

5,600

Fixed Cost

(5,600)

Net Income

$ 0

Demonstration Problem 11-4 Solution continued

(2) Contribution Margin Ratio Approach