Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

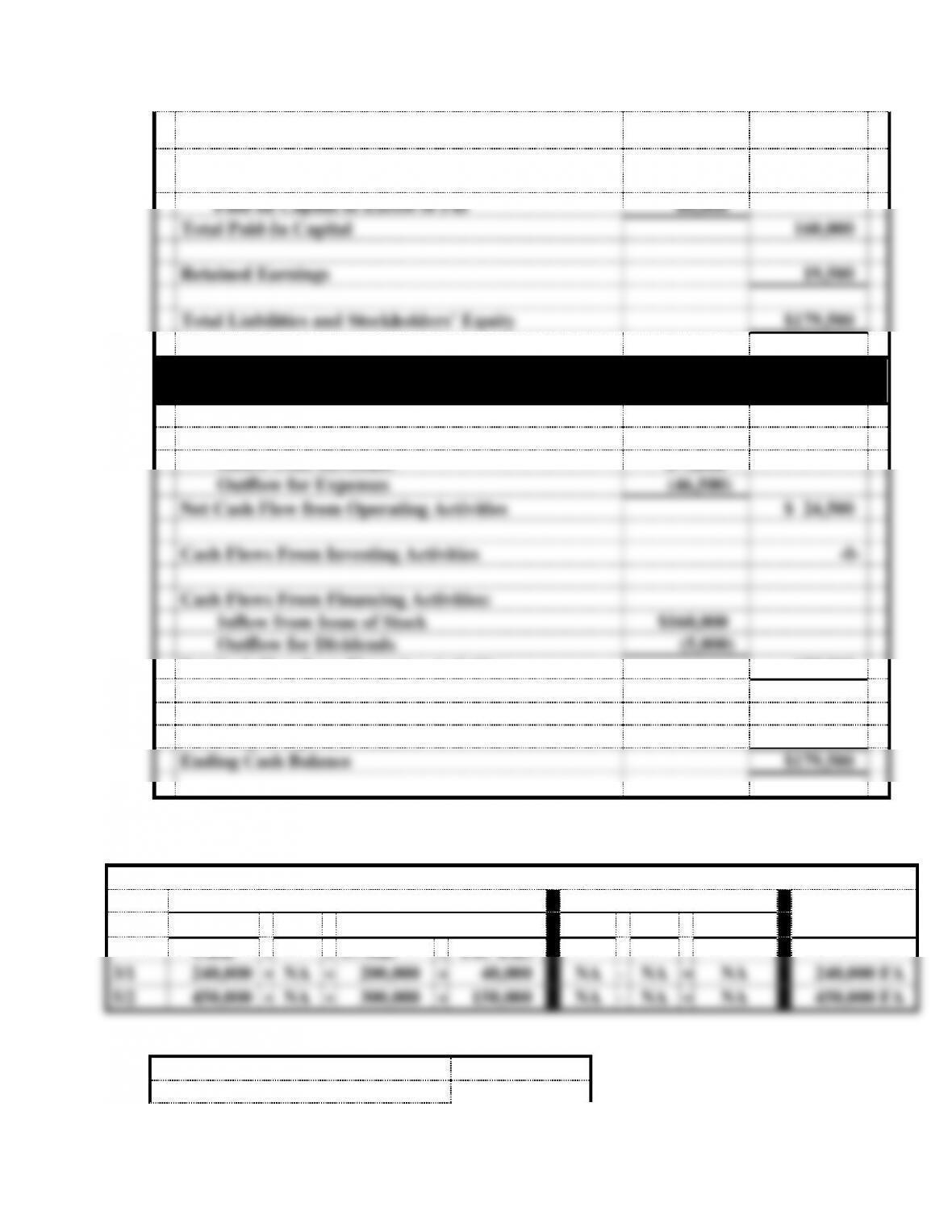

Stockholders’ Equity

Common Stock, $10 par value,

10,000 shares issued and outstanding

$100,000

Paid-In Capital in Excess of Par

60,000

Total Paid-In Capital

160,000

Retained Earnings

19,500

Total Liabilities and Stockholders’ Equity

$179,500

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash Flows From Operating Activities:

Inflow from Revenues

$71,000

Outflow for Expenses

(46,500)

Net Cash Flow from Operating Activities

$ 24,500

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Inflow from Issue of Stock

$160,000

Outflow for Dividends

(5,000)

Net Cash Flow from Financing Activities

155,000

Net Change in Cash

179,500

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$179,500

EXERCISE 8-4

a.

Balance Sheet

Income Statement

Stmt. of

Event

Assets

=

Liab

+

Stkholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

=

+

C. Stk.

+

PIC Exc.

3/1

240,000

=

NA

+

200,000

+

40,000

NA

−

NA

=

NA

240,000 FA

5/2

450,000

=

NA

+

300,000

+

150,000

NA

−

NA

=

NA

450,000 FA

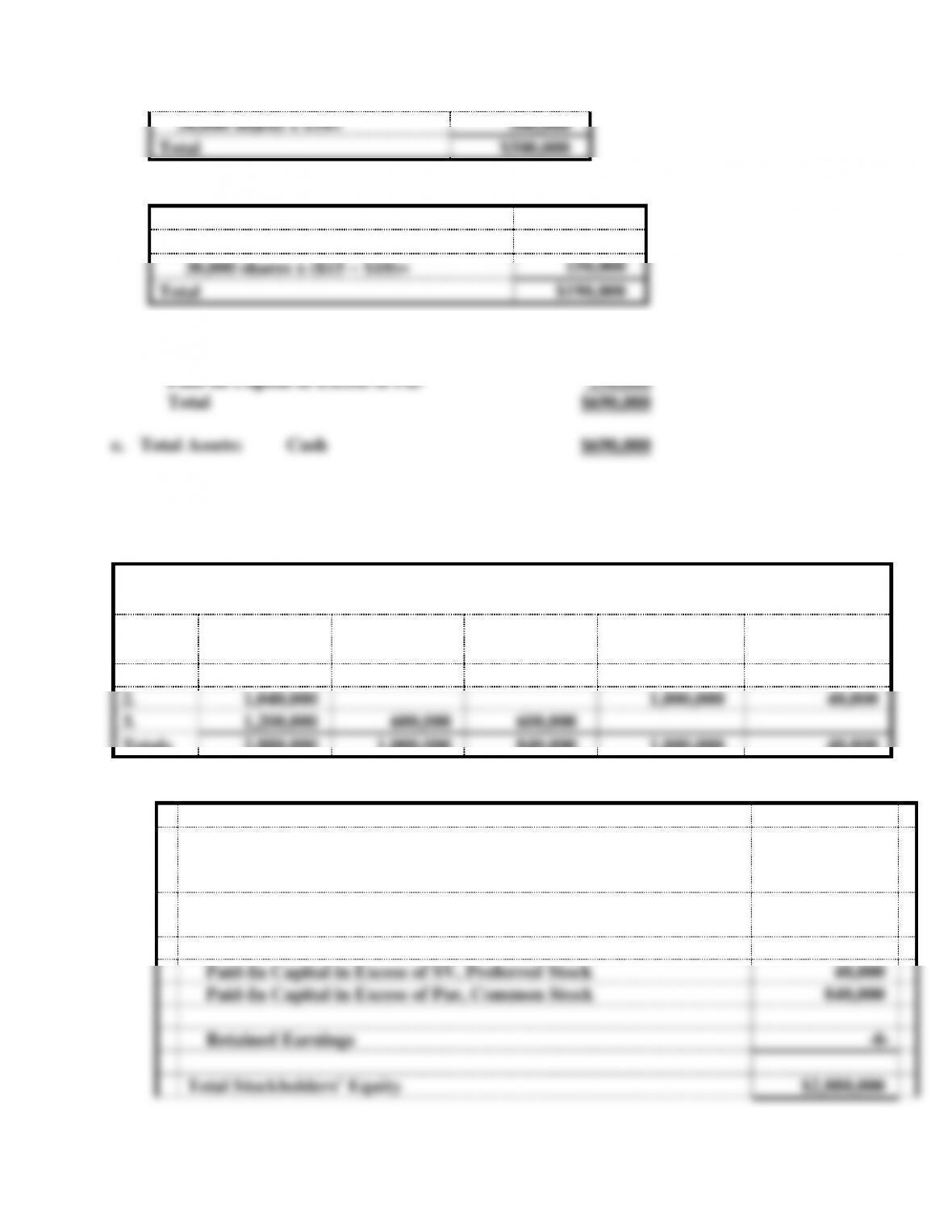

b.

Common Stock:

20,000 shares x $10=

$200,000

30,000 shares x $10=

300,000

Total

$500,000

c.

Paid-In Capital in Excess of Par

20,000 shares x ($12 − $10)=

$ 40,000

30,000 shares x ($15 − $10)=

150,000

Total

$190,000

d. Total Paid-In Capital:

Common Stock $500,000

EXERCISE 8-5

Summary of Transactions

Event

Cash

Received

Common

Stock

PIC in Excess

CS

Preferred Stock

PIC in Excess

PS

1.

640,000

400,000

240,000

2.

1,040,000

1,000,000

40,000

3.

1,200,000

600,000

600,000

Totals

2,880,000

1,000,000

840,000

1,000,000

40,000

Stockholders’ Equity:

Preferred Stock, $50 stated value, 4% cumulative class A, 100,000

shares authorized, 20,000 shares issued and outstanding

$1,000,000

Common Stock, $10 par value, 500,000 shares authorized, 100,000

shares issued and outstanding

1,000,000

Paid-In Capital in Excess of SV, Preferred Stock

40,000

Paid-In Capital in Excess of Par, Common Stock

840,000

Retained Earnings

-0-

Total Stockholders’ Equity

$2,880,000

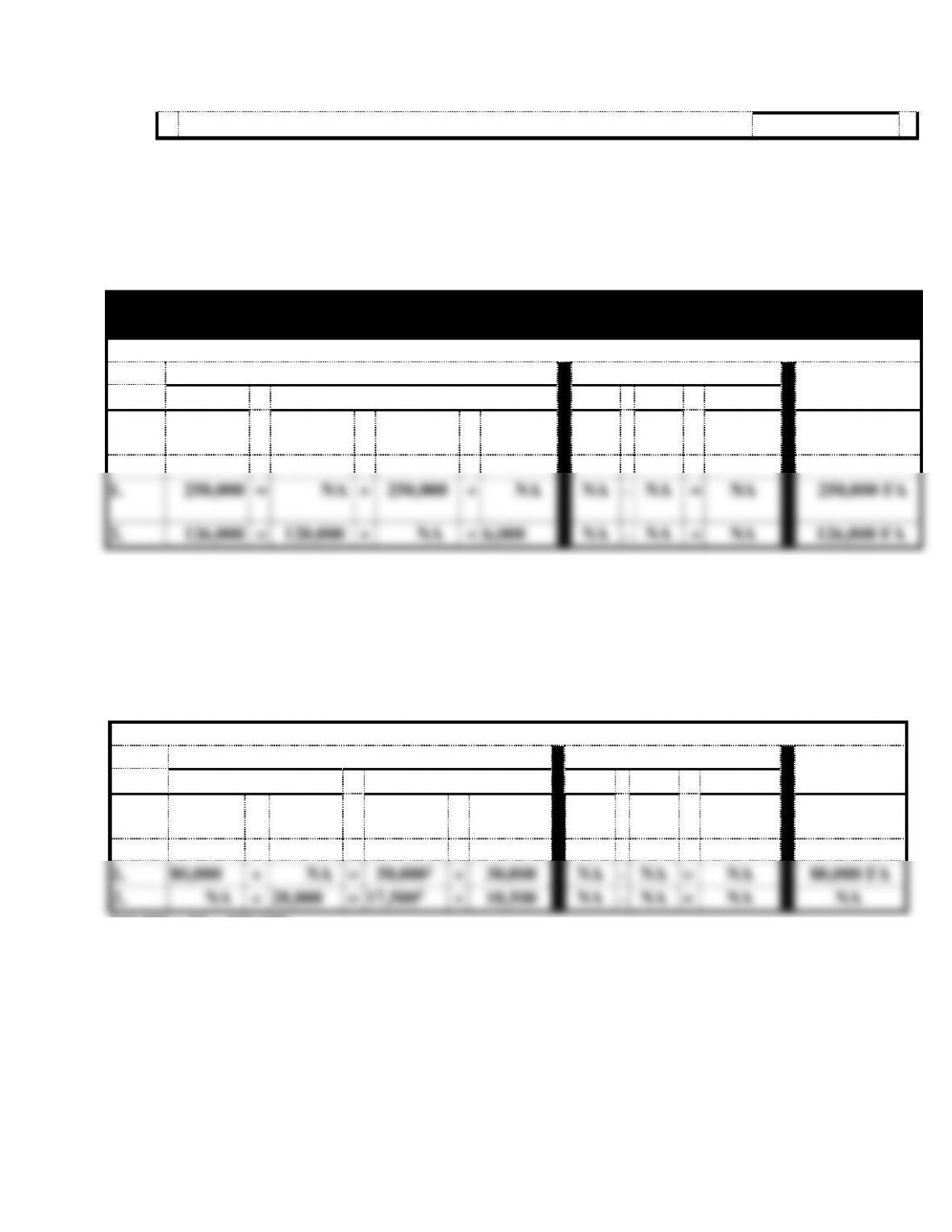

EXERCISE 8-6

Bailey Corporation

Statements Model

Balance Sheet

Income Statement

Stmt. of

Event

Assets

=

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

=

Pref.

Stock

+

No-Par

C. Stock

+

PIC in

Excess

1.

250,000

=

NA

+

250,000

+

NA

NA

−

NA

=

NA

250,000 FA

2.

126,000

=

120,000

+

NA

+

6,000

NA

−

NA

=

NA

126,000 FA

EXERCISE 8-7

a. 3,500 shares x $8 market value per share of stock = $28,000

b.

Balance Sheet

Income Statement

Stmt. of

Event

Assets

=

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Cash

+

Van

=

Com. Stk.

+

PIC Exc.

1.

80,000

+

NA

=

50,0001

+

30,000

NA

−

NA

=

NA

80,000 FA

2.

NA

+

28,000

=

17,5002

+

10,500

NA

−

NA

=

NA

NA

110,000 x $5 = $50,000

2 3,500 x $5 = $17,500

EXERCISE 8-8

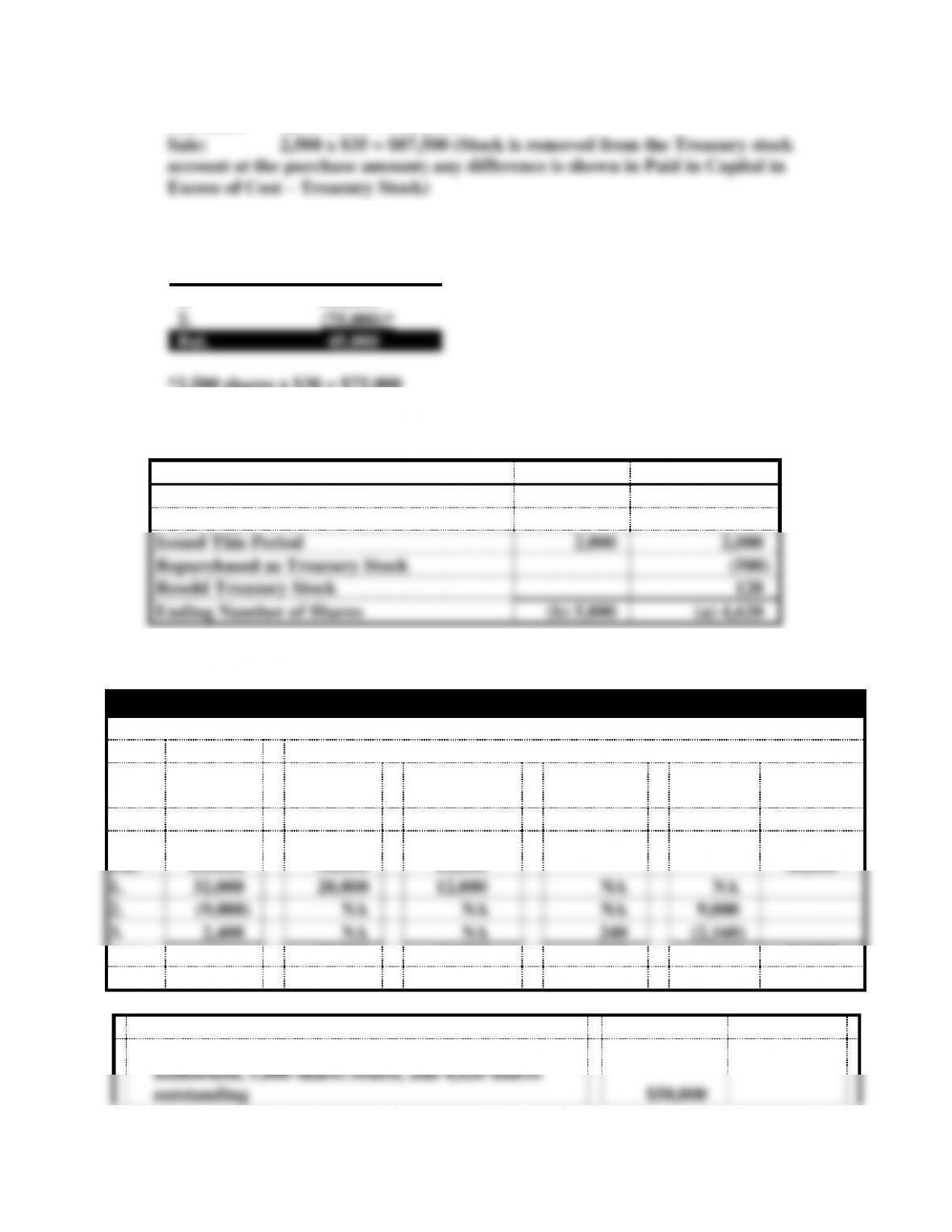

Transactions:

Purchase: 4,000 x $30 = $120,000

Treasury Stock

1. 120,000

2. (75,000)*

Bal. 45,000

*2,500 shares x $30 = $75,000

EXERCISE 8-9

a. & b.

Common Stock

Issued

Outstanding

Beginning Number of Shares

3,000

3,000

Issued This Period

2,000

2,000

Repurchased as Treasury Stock

(500)

Resold Treasury Stock

120

Ending Number of Shares

(b) 5,000

(a) 4,620

c.

Wise Corporation Accounting Equation

Event

Assets

=

Stockholders’ Equity

Cash

=

Comm

Stock

+

PIC in Excess

CS

+

PIC in

Excess TS

−

Treasury

Stock

Retained

Earnings

Beg.

Bal.

xxxxxx

30,000

12,000

46,000

1.

32,000

20,000

12,000

NA

NA

2.

(9,000)

NA

NA

NA

9,000

3.

2,400

NA

NA

240

(2,160)

Bal.

xxxxxx

50,000

24,000

240

6,840

46,000

d.

Stockholders’ Equity

Common Stock, $10 par value, 50,000 shares

authorized, 5,000 shares issued, and 4,620 shares

outstanding

$50,000

Paid-In Capital in Excess of Par, Common

24,000

Paid-In Capital in Excess of Cost, TS

240

Total Paid-In Capital

$74,240

Retained Earnings

46,000

Less: Treasury Stock

(6,840)

Total Stockholders’ Equity

$113,400

EXERCISE 8-10

Balance Sheet

Income Statement

Statement

Date

Assets

=

Liab.

+

Com.

Stk.

+

Ret. Ear.

Rev

−

Exp.

=

Net Inc.

of

Cash Flows

10/1

NA

=

50,000

+

NA

+

(50,000)

NA

−

NA

=

NA

NA

11/1

NA

=

NA

+

NA

+

NA

NA

−

NA

=

NA

NA

12/15

(50,000)

=

(50,000)

+

NA

+

NA

NA

−

NA

=

NA

(50,000) FA

EXERCISE 8-11

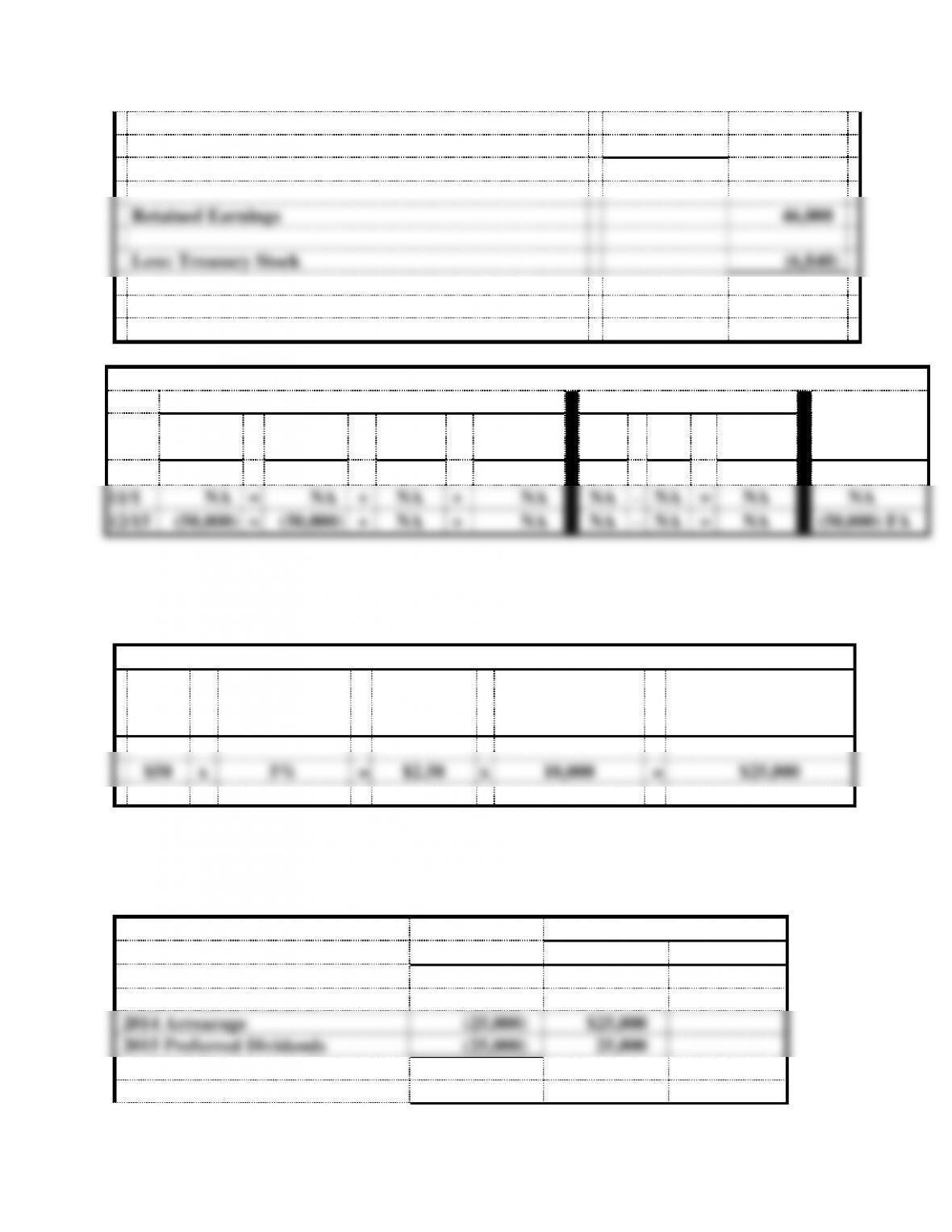

Computation of Preferred Dividends:

Par

x

Dividend %

=

Dividend per

Share

x

Number of Shares

Outstanding

=

Total Preferred

Dividends for Year

$50

x

5%

=

$2.50

x

10,000

=

$25,000

a. Dividend arrearage as of January 1, 2015: $25,000 (one year)

b.

Dist. to Shareholders

Amount

Preferred

Common

Total Dividend Declared

$65,000

2014 Arrearage

(25,000)

$25,000

2015 Preferred Dividends

(25,000)

25,000

Available for Common Shs.

15,000

Distributed to Common

(15,000)

$15,000

Total Distribution

$50,000

$15,000

EXERCISE 8-12

Computation of Dividends to Be Paid:

Preferred Stock

$100 par value x 4% x 8,000 shares=

$32,000

Common Stock

$.50 x 200,000 shares =

100,000

Total Dividend

$132,000

EXERCISE 8-13

Distribution of Dividend:

Distributed to Shareholders

Preferred

Common

Total Dividend Declared

$150,000

Preferred Arrearage*

(60,000)

$60,000

Current Preferred Dividend*

(60,000)

60,000

Available for Common

30,000

Distributed to Common

(30,000)

$30,000

Total

$120,000

$30,000

*$100 x 4% x 15,000 Shares = $60,000

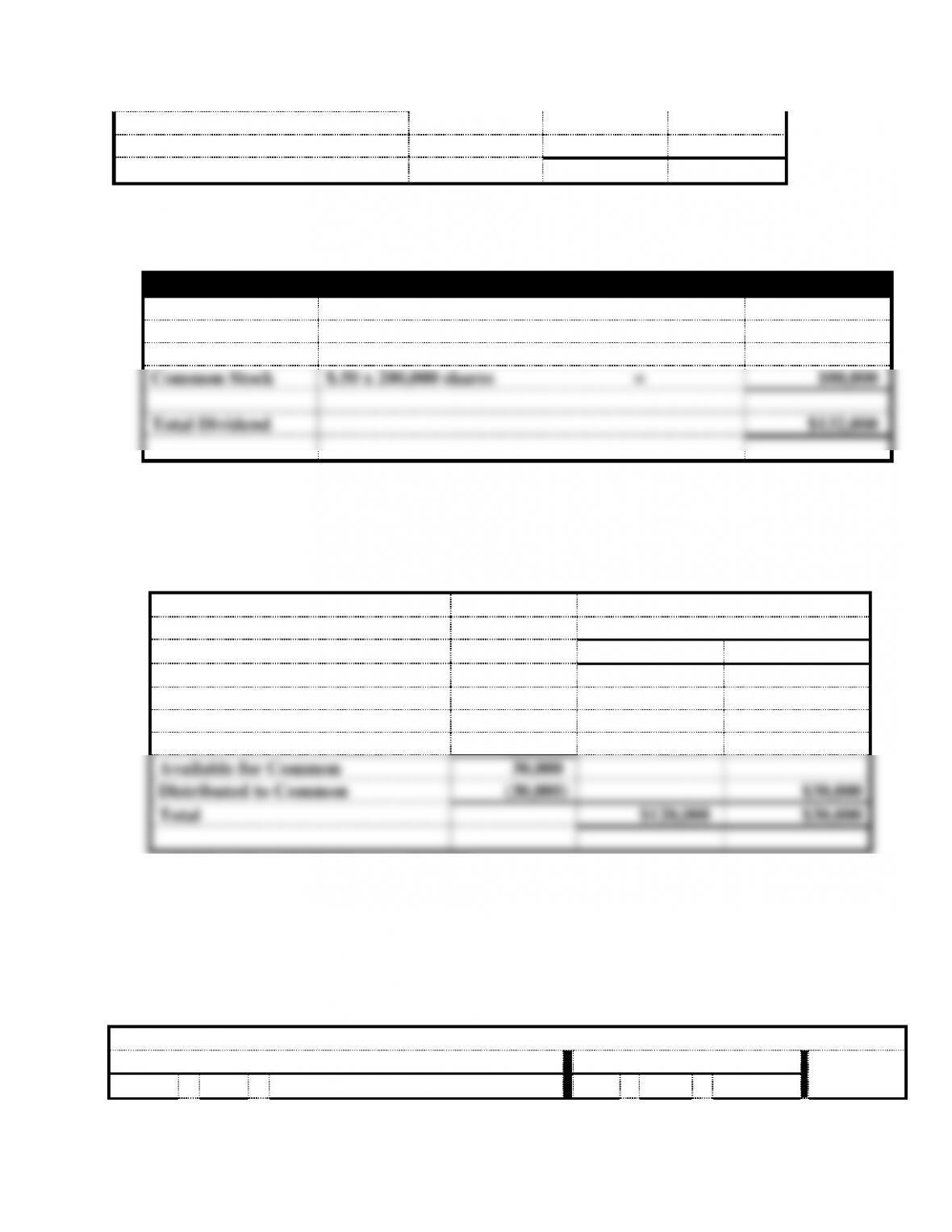

EXERCISE 8-14

a. (20,000 shares x .04) = 800 shares; 800 shares x $30 = $24,000

b.

Balance Sheet

Income Statement

Stmt. of

Assets

=

Liab

+

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Com. Stk.

+

PIC. Ex.

+

Ret. Ear.

NA

=

NA

+

8,000

+

16,000

+

(24,000)

NA

−

NA

=

NA

NA

EXERCISE 8-15

a. No formal entry would be made in the accounting records. A memo entry would

b. 200,000 shares x 3 = 600,000 total shares outstanding

c. Theoretically, the market value per share would be reduced to $80 ($240 3) after

EXERCISE 8-16

a. The price per share of Super Drugs should increase substantially. This increase is a

result of the expectation of future profits. The approval of the new drug signals that

profits should be substantially higher in the future.

c. The income statement will not be affected when the announcements are made. Only

when revenues increase will net income be affected.

PROBLEM 8-17

Note: The memo incorporates a schedule showing the after-tax cash flows under each form

of ownership and discusses LLCs.

Memo

As requested, this memo describes the advantages and disadvantages of the partnership

versus corporate forms of business ownership.

Advantages

Disadvantages

Partnership

• Ease of formation

• Less regulation

• Lower effective tax rate

• Limited life

• Mutual agency

• Unlimited liability

Corporation

• Unlimited life

• Limited liability

• Capital easier to acquire &

ownership easily

transferred

• More regulation

• Higher effective tax rate

The most important of these advantages and disadvantages relate to taxation and owner’s

liability.PROBLEM 8-17 (cont.)

The schedule below illustrates the after-tax cash flows under each form:

Partnership

Corporation

Income before taxes

$200,000

$200,000

Tax at entity level

-0-

(50,000)

Net income distributed to

owners

200,000

150,000

Less: Individual income tax

(35%)

(70,000)

(52,500)

After-tax cash flow

$130,000

$ 97,500

After-tax cash flow available

to each investor

$130,000 5 =

$26,000

$97,500 5 =

$19,500

Effective tax rate (total tax

paid to total earnings)

($70,000 $200,000)

=35%

($102,500 $200,000)

=51.25%

The corporate form limits the potential liability of owners. Creditors of partnerships may

Limited liability companies (LLCs) offer many of the benefits associated with corporate

PROBLEM 8-18

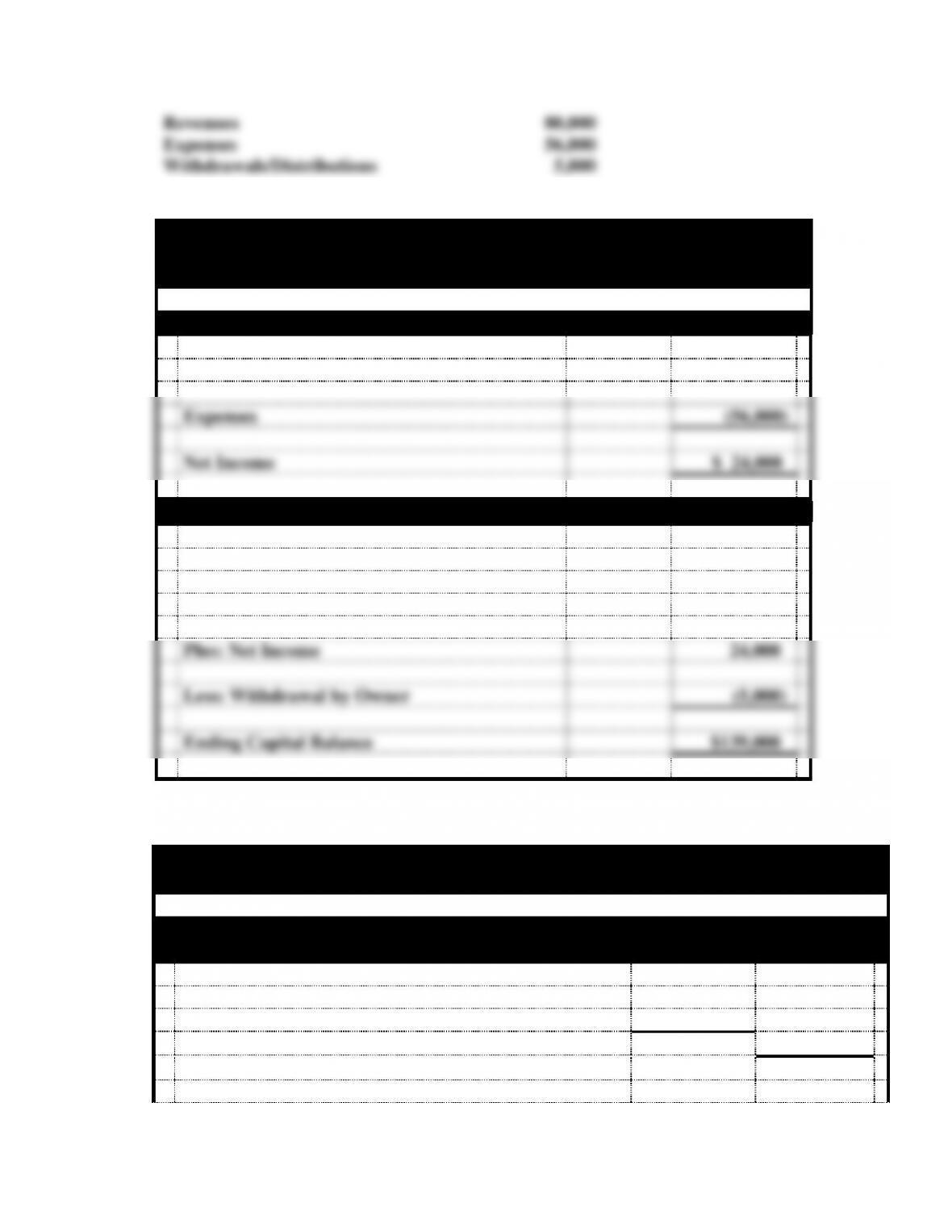

Transactions

Cash Acquired from Owners

$120,000

Revenues

80,000

Expenses

56,000

Withdrawals/Distributions

5,000

a. Sole Proprietorship

Auto Spa Company

Financial Statements

For the Year Ended December 31, 2014

Income Statement

Revenues

$ 80,000

Expenses

(56,000)

Net Income

$ 24,000

Capital Statement

Beginning Capital Balance

$ -0-

Plus: Capital Acquired from Owner

120,000

Plus: Net Income

24,000

Less: Withdrawal by Owner

(5,000)

Ending Capital Balance

$139,000

PROBLEM 8-18 a. (cont.)

Auto Spa Company

Financial Statements

Balance Sheet

As of December 31, 2014

Assets

Cash

$139,000

Total Assets

$139,000

Liabilities

$ -0-

Equity

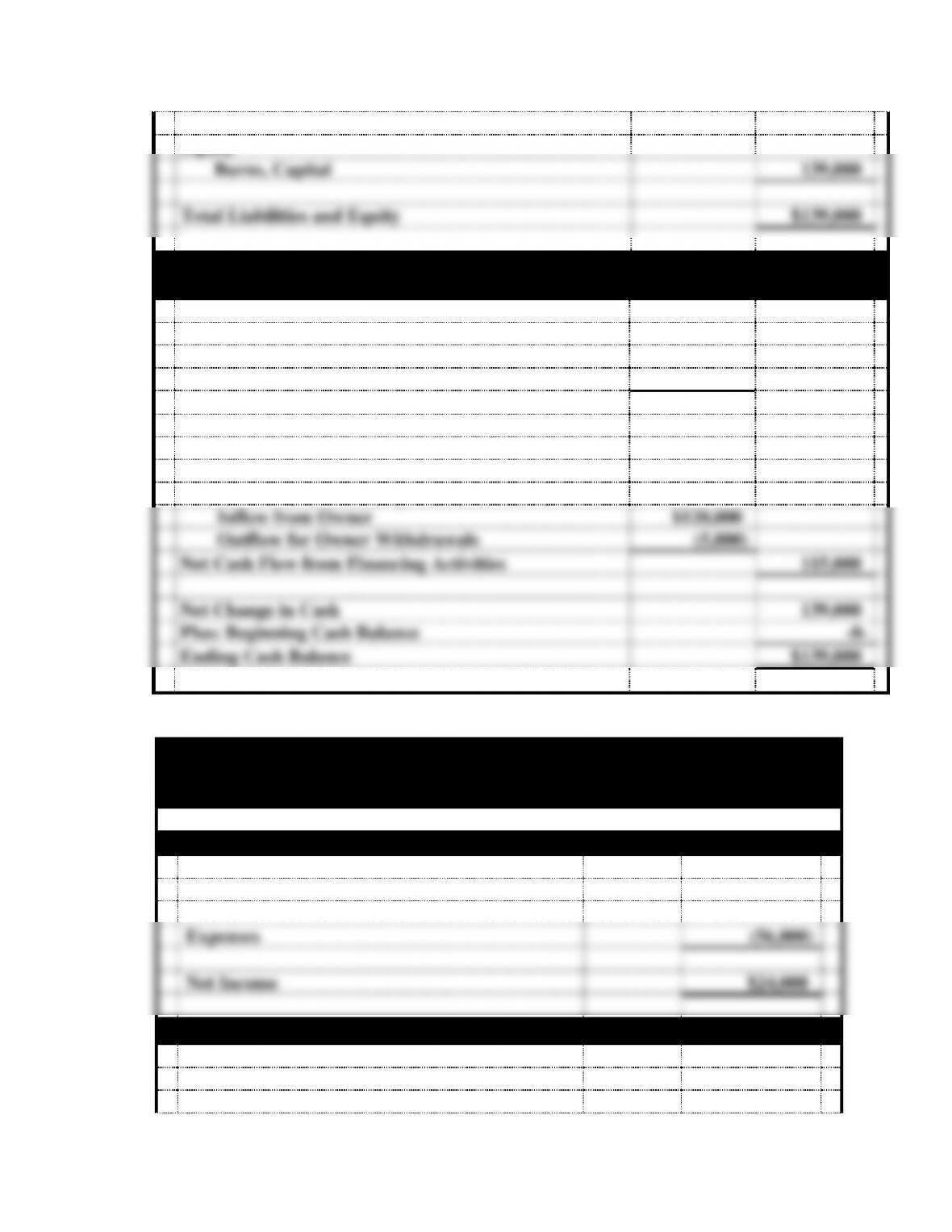

Burns, Capital

139,000

Total Liabilities and Equity

$139,000

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash Flows From Operating Activities:

Inflow from Revenues

$ 80,000

Outflow for Expenses

(56,000)

Net Cash Flow from Operating Activities

$ 24,000

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Inflow from Owner

$120,000

Outflow for Owner Withdrawals

(5,000)

Net Cash Flow from Financing Activities

115,000

Net Change in Cash

139,000

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$139,000

PROBLEM 8-18 (cont.)

b. Partnership

Auto Spa Company

Financial Statements

For the Year Ended December 31, 2014

Income Statement

Revenues

$80,000

Expenses

(56,000)

Net Income

$24,000

Capital Statement

Beginning Capital Balance

$ -0-

Plus: Capital Acquired from Owners

120,000

Plus: Net Income

24,000

Less: Withdrawals by Owners

(5,000)

Ending Capital Balance

$139,000

Prepared for the instructor’s use:

Analysis of Capital Accounts:

Moore

Pounds

Total

Beginning Capital Balance

$ -0-

$ -0-

$ -0-