2-1

EXERCISE 2-16

a.

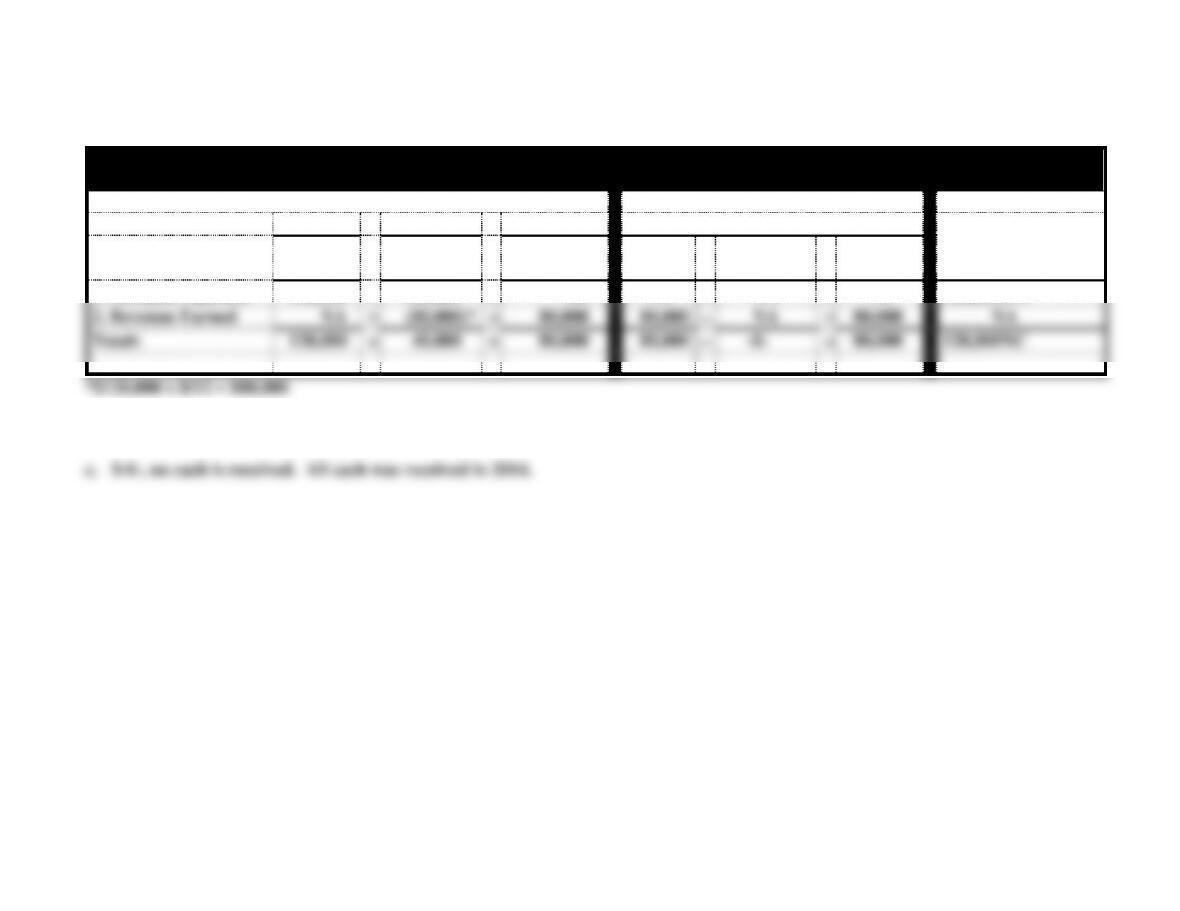

Ed Arnold Personal Financial Planning

Horizontal Statements Model for 2014

Assets

=

Liabilities

+

Stk. Equity

Income Statement

Statement

Event

Cash

=

Unearned

Revenue

+

Retained

Earnings

Rev.

−

Exp.

=

Net

Income

of

Cash Flows

1. Advance Payment

120,000

=

120,000

+

NA

NA

−

NA

=

NA

120,000OA

2. Revenue Earned

NA

=

(80,000)*

+

80,000

80,000

−

NA

=

80,000

NA

Totals

120,000

=

40,000

+

80,000

80,000

−

-0-

=

80,000

120,000NC

b. Revenue that will be recognized in 2015 is $40,000, the remainder of the unearned revenue.

2-2

EXERCISE 2-17

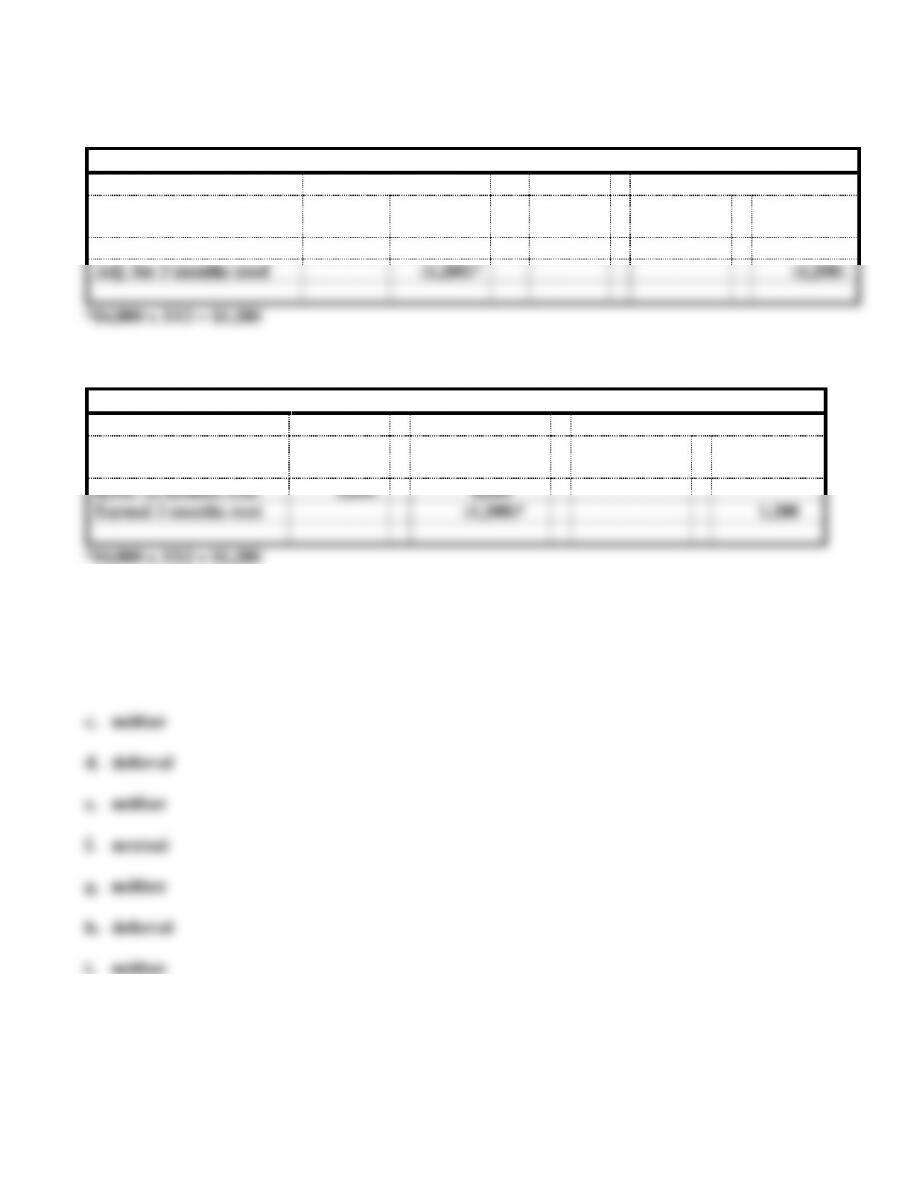

a.

Caldonia Company Accounting Equation – 2014

Event

Assets

=

Liab.

+

Stockholders’ Equity

Cash

Prepaid

Rent

=

+

Common

Stock

+

Retained

Earnings

Paid 12 months rent

(4,800)

4,800

Adj. for 3 months used

(1,200)*

(1,200)

b.

East Alabama Rentals Accounting Equation – 2014

Event

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

=

Unearned

Revenue

+

Common

Stock

+

Retained

Earnings

Recd. 12 months rent

4,800

4,800

Earned 3 months rent

(1,200)*

1,200

*$4,800 x 3/12 = $1,200

EXERCISE 2-18

a. accrual

b. accrual

j. deferral

k. accrual

2-3

EXERCISE 2-19

Note: There are many examples of events that illustrate the required effects. An example is

given of each event.

a. Recognized revenue on account. The asset is either Cash or Accounts Receivable.

b. Recognized revenue where the cash had been received in advance. The liability is Unearned

Revenue

long-lived asset that is depreciated or amortized.

EXERCISE 2-20

b. The temporary accounts (Revenue, Expense, and Dividends) are closed at the end of each

c. The relationship between the beginning and ending balances in the Retained Earnings

accounts is:

Beginning Retained Earnings Balance (January 1, 2014) ?

+ Net Income (Revenue $15,100 − Expenses 9,200) 5,900

− Dividends (1,500)

the time of recognition. The balance in the Retained Earnings account on June 30, 2014 is

the same as it was on January 1, 2014 which is $15,000.

2-4

EXERCISE 2-21

a.

Event

Requires year-end adjusting

entry?

1.

No

2.

Yes

3.

No

4.

Yes

5.

No

6.

No

7.

No

8.

No

9.

Yes

10.

No

b. Adjusting entries are recorded before closing entries. Adjusting entries are required to

update the accounts so that the correct amounts of income and expenses are recognized.

2-5

EXERCISE 2-22

a.

Permanent Accounts

Cash

Notes Payable

Land

Common Stock

Retained Earnings

Temporary (Nominal) Accounts

Revenue

Expenses

Dividends

b.

Beginning Retained Earnings

$5,200

Add: Revenue

7,000

Less: Expenses

(4,200)

Less: Dividends

(1,000)

Ending Retained Earnings

$7,000

c.

Computation of Net Income

Revenue

$7,000

Less: Expenses

(4,200)

Net Income

$2,800

d. Net income is only the current year’s net income. Retained Earnings is an accumulation of

net income over the life of the business less any dividends that have been paid over the years.

EXERCISE 2-23

a.

Account

Classification

1. Service Revenue

T

2. Dividends

T

3. Common Stock

P

4. Notes Payable

P

5. Cash

P

6. Rent Expense

T

7. Accounts Receivable

P

8. Utilities Expense

T

9. Prepaid Insurance

P

10. Retained Earnings

P

b. The four stages of the accounting cycle are:

recording transactions

The first stage of the cycle must be recording accounting data in accounts to put it into usable

form. Once the accounting data is summarized in the accounts, adjustments are made to

accounting period.

EXERCISE 2-24

a. Directly matched

EXERCISE 2-25

a.

Event

Classification

1.

FA

2.

OA

3.

OA

4.

NA

5.

OA

6.

NA

7.

NA

8.

OA

2-7

9.

FA

10.

OA

b.

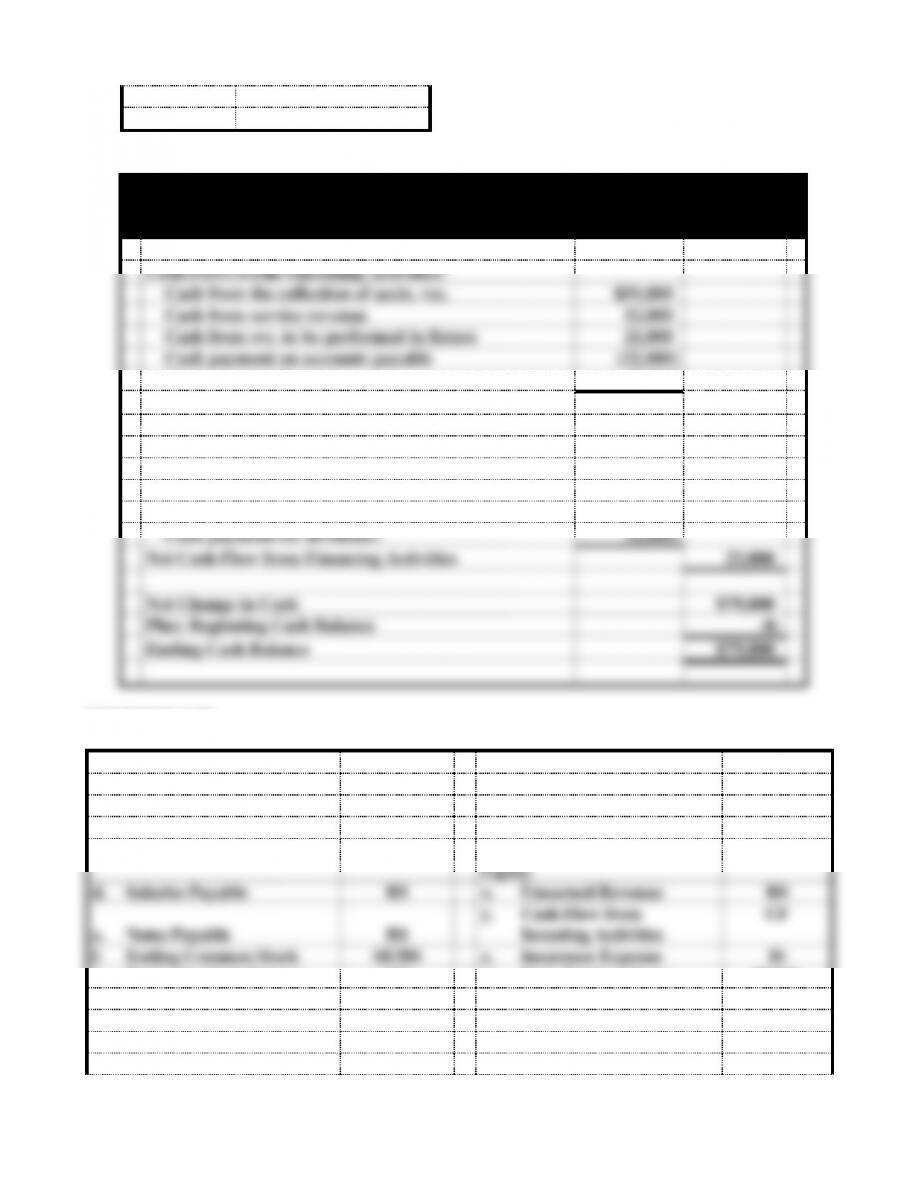

Blair Company

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash Flows From Operating Activities:

Cash from the collection of accts. rec.

$51,000

Cash from service revenue

12,000

Cash from svc. to be performed in future

21,000

Cash payment on accounts payable

(22,000)

Cash payment for rent

(7,200)

Net Cash Flow from Operating Activities

$54,800

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Cash receipt from stock issue

$30,000

Cash payment for dividends

(5,000)

Net Cash Flow from Financing Activities

25,000

Net Change in Cash

$79,800

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$79,800

EXERCISE 2-26

Item/Account

Statement

Item/Account

Statement

a. Consulting Revenue

IS

u. Rent Expense

IS

b. Market Value of Land

NA

v. Salary Expense

IS

c. Supplies Expense

IS

w. Total Stockholders’

Equity

BS/SE

d. Salaries Payable

BS

x. Unearned Revenue

BS

e. Notes Payable

BS

y. Cash Flow from

Investing Activities

CF

f. Ending Common Stock

SE/BS

z. Insurance Expense

IS

g. Beginning Cash Balance

CF

aa. End. Retained Earn.

BS/SE

h. Prepaid Rent

BS

bb. Interest Revenue

IS

i. Net Change in Cash

CF

cc. Supplies

BS

j. Land

BS

dd. Beg. Retained Earn.

SE

k. Operating Expenses

IS

ee. Utilities Payable

BS

l. Total Liabilities

BS

ff. Cash Flow from

Financing Activities

CF

m. “As of” Date Notation

BS

gg. Accounts Receivable

BS

n. Salaries Expense

IS

hh. Prepaid Insurance

BS

o. Net Income

IS/SE

ii. Ending Cash Balance

BS/CF

p. Service Revenue

IS

jj. Utilities Expense

IS

q. Cash Flow from

Operating Activities

CF

kk. Accounts Payable

BS

r. Operating Income

IS

ll. Beg. Common Stock

SE

s. Interest Receivable

BS

mm. Dividends

SE/CF

t. Interest Revenue

IS

nn. Total Assets

BS

EXERCISE 2-27

Horizontal Statement Model

Stk. Equity

Income Statement

Type of

Com.

Ret.

Net

Cash

Event

Event

Assets

=

Liab.

+

Stock

+

Earn.

Rev.

−

Exp.

=

Inc.

Flows

a.

AE

I/D

NA

NA

NA

NA

NA

NA

D

IA

b.

AS

I

NA

I

NA

NA

NA

NA

I

FA

c.

AE

I/D

NA

NA

NA

NA

NA

NA

I

OA

d.

AU

D

NA

NA

D

NA

I

D

D

OA

e.

CE

NA

I

NA

D

NA

I

D

NA

f.

AS

I

I

NA

NA

NA

NA

NA

NA

g.

AS

I

NA

NA

I

I

NA

I

NA

h.

AE

I/D

NA

NA

NA

NA

NA

NA

D

OA

i.

AU

D

NA

NA

D

NA

I

D

NA

j.

AS

I

NA

NA

I

I

NA

I

I

OA

k.

AU

D

D

NA

NA

NA

NA

NA

D

OA

l.

AU

D

NA

NA

D

NA

NA

NA

D

FA

m.

AU

D

NA

NA

D

NA

I

D

NA

n.

CE

NA

I

NA

D

NA

I

D

NA

o.

AU

D

D

NA

NA

NA

NA

NA

D

OA

p.

AS

I

I

NA

NA

NA

NA

NA

I

OA

q.

AS

I

NA

NA

I

I

NA

I

NA

EXERCISE 2-28

Net Income

Cash Flow from

Operating Activities

Event

Direction of

Change

Amount of

Change

Direction of

Change

Amount of

Change

a.

NA

NA

NA

NA

b.

Increase

$20,000

Increase

$15,000

c.

Decrease

1,2001

Decrease

4,800

d.

Increase

5,0002

Increase

12,000

e.

Decrease

5,000

NA

NA

f.

NA

NA

NA

NA

g.

Increase

9,200

Increase

9,200

h.

Decrease

1,2003

Decrease

1,500

i.

Decrease

2,200

Decrease

2,200

1$4,800 x 3/12 = $1,200

2$12,000 x 5/12 = $5,000

3$2,000 − $800 = $1,200

EXERCISE 2-29

Note: These are only sample transactions. Other similar transactions will satisfy the

requirements of this exercise.

a. The business invested cash by purchasing a building.

Collected accounts receivable.

b. Purchased land with a note (liability).

Purchased supplies on account.

2-10

Recorded the liability for the utility bill received, but not due until the next period.

f. The business issued common stock to its owners.

EXERCISE 2-30

a. Asset Source

b. Asset Use

c. Asset Source

d. Claims Exchange

j. Asset Exchange

EXERCISE 2-31

Note: These are only sample transactions. Other similar transactions will satisfy the

requirements of this exercise.

a. Payment of rent expense; payment of other operating expense.

b. Payment of accounts payable; payment of dividends.

2-11

c. Received a note receivable in exchange for the sale of a delivery van.

d. Collection of accounts receivable; purchase of land.

e. Proceeds of a loan; issue of common stock.