Chapter 15 – Performance Evaluation

15-1

d. Suppose Murdoch changes its performance assessment measure from ROI to residual

income (RI). Murdoch’s desired rate of return is 14%. Under these circumstances,

should Hydride’s manager accept or reject the opportunity to invest the additional

$4,000,000 in machinery as described in requirement c?

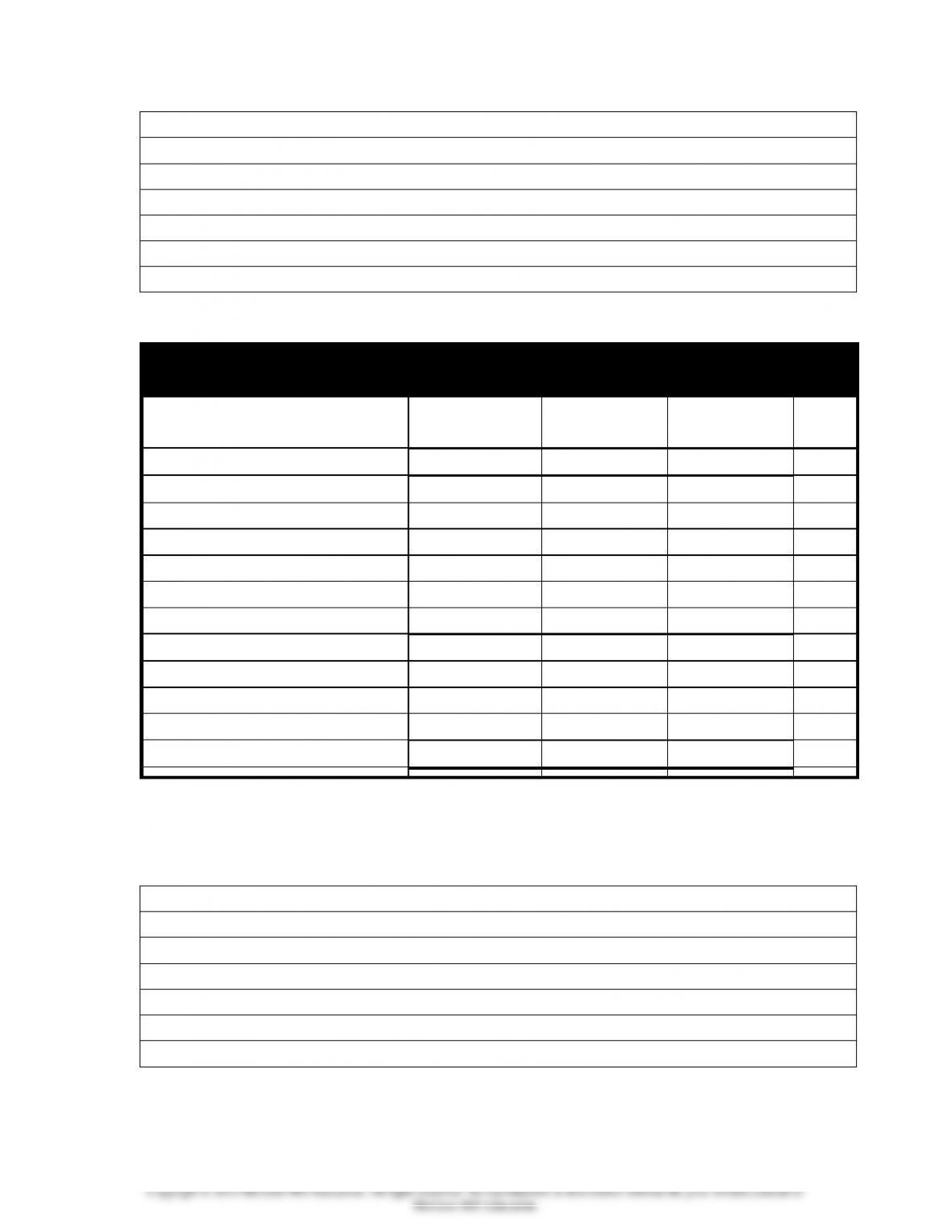

Demonstration Problem 15-1 Solution

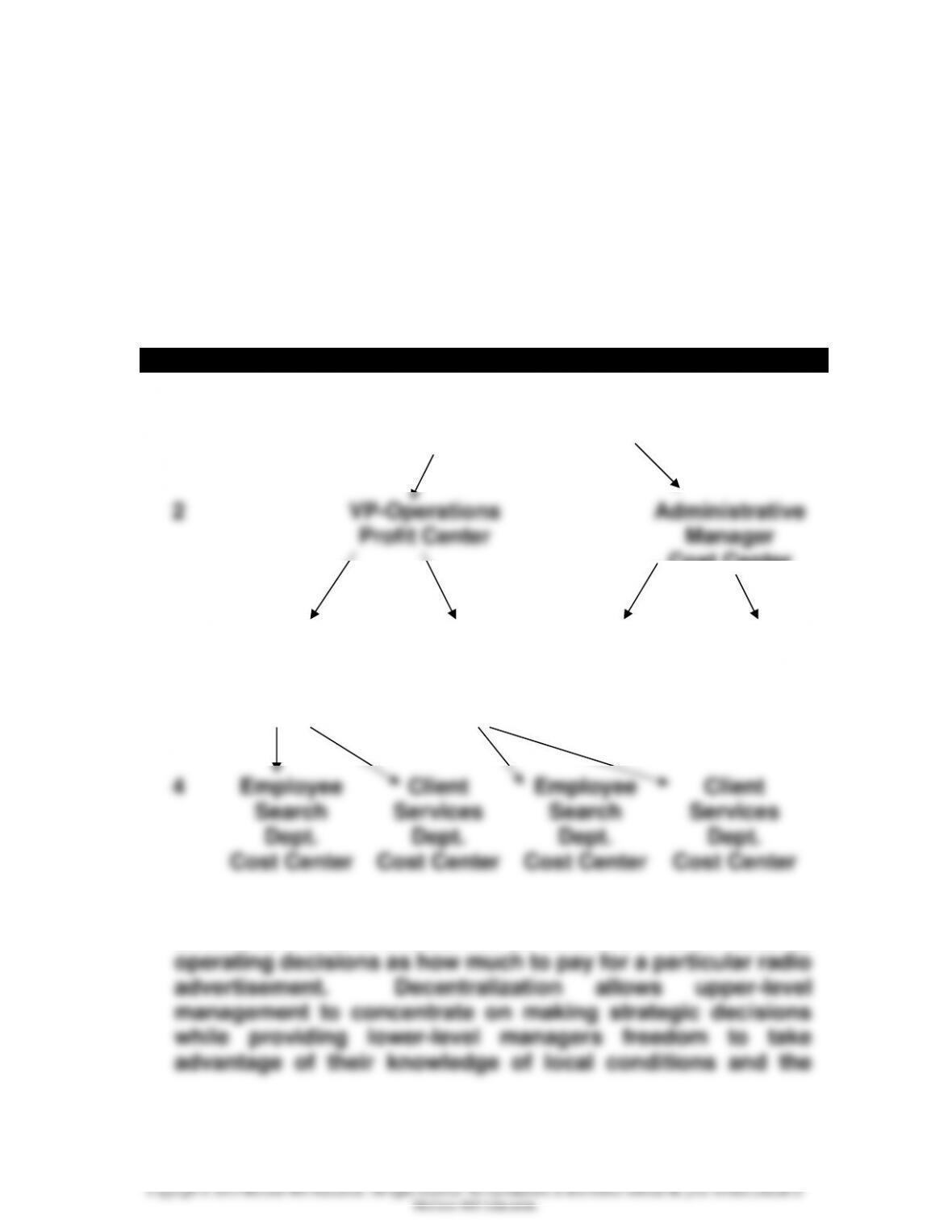

a. b.

Organization Chart

Level

1

CEO—Company Headquarters

Investment Center

2

VP-Operations

Profit Center

Administrative

Manager

Cost Center

3

Clerical

Services

Division

Profit Center

Computer

Services

Division

Profit Center

Secretarial

Labor Pool

Cost Center

Advertising

Manager

Cost Center

4

Employee

Search

Dept.

Cost Center

Client

Services

Dept.

Cost Center

Employee

Search

Dept.

Cost Center

Client

Services

Dept.

Cost Center

c. No. Because LiPari exhibits a decentralized organization

structure, the CEO should not be involved in such detailed

Chapter 15 – Performance Evaluation

15-2

experience.Demonstration Problem 15-2 Solution

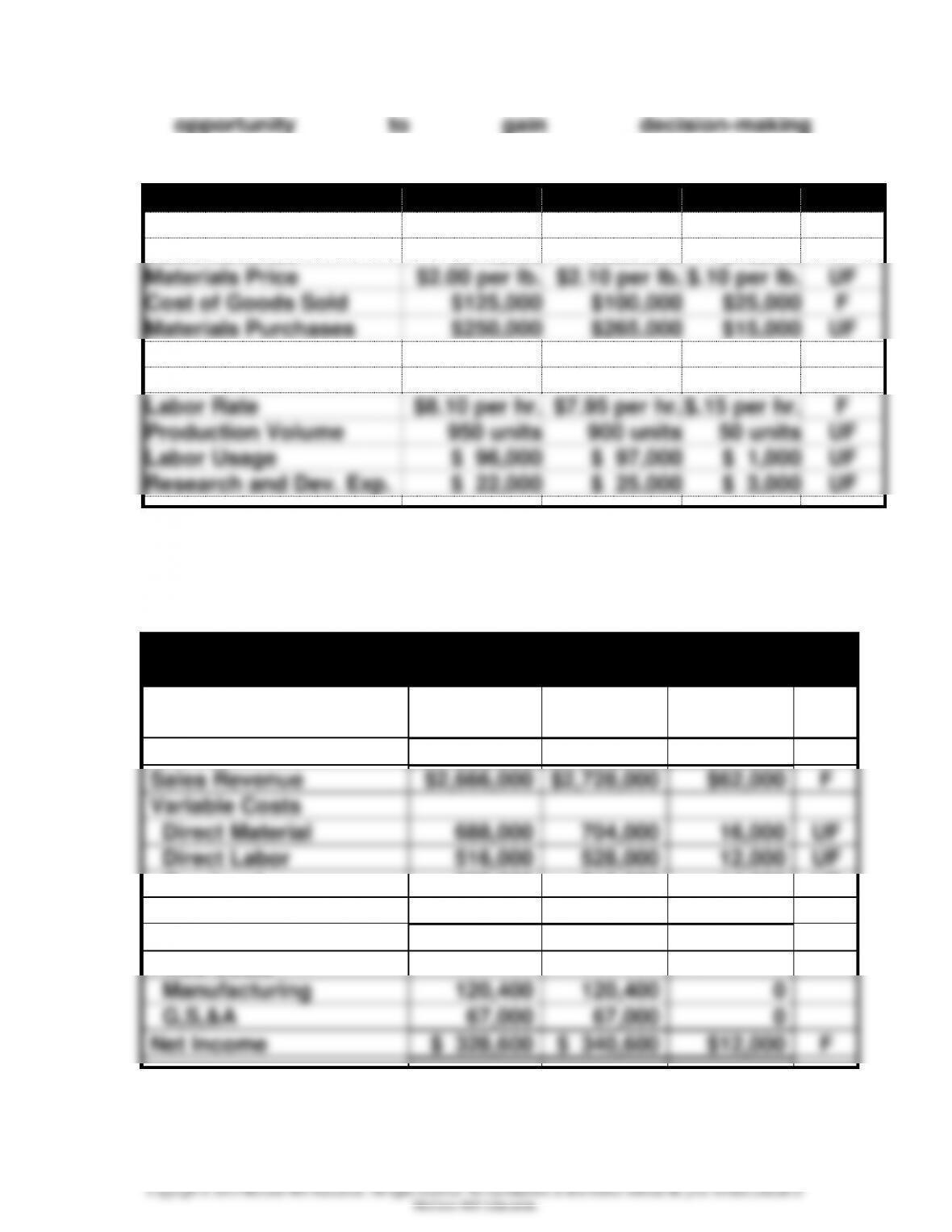

Item

Budget

Actual

Variance

F or UF

Selling and Admin. Exp.

$ 29,000

$ 27,000

$ 2,000

F

Sales Revenue

$310,000

$325,000

$15,000

F

Materials Price

$2.00 per lb.

$2.10 per lb.

$.10 per lb.

UF

Cost of Goods Sold

$125,000

$100,000

$25,000

F

Materials Purchases

$250,000

$265,000

$15,000

UF

Materials Usage

6,000 lbs.

5,800 lbs.

200 lbs.

F

Sales Price

$550 each

$500 each

$50 each

UF

Labor Rate

$8.10 per hr.

$7.95 per hr.

$.15 per hr.

F

Production Volume

950 units

900 units

50 units

UF

Labor Usage

$ 96,000

$ 97,000

$ 1,000

UF

Research and Dev. Exp.

$ 22,000

$ 25,000

$ 3,000

UF

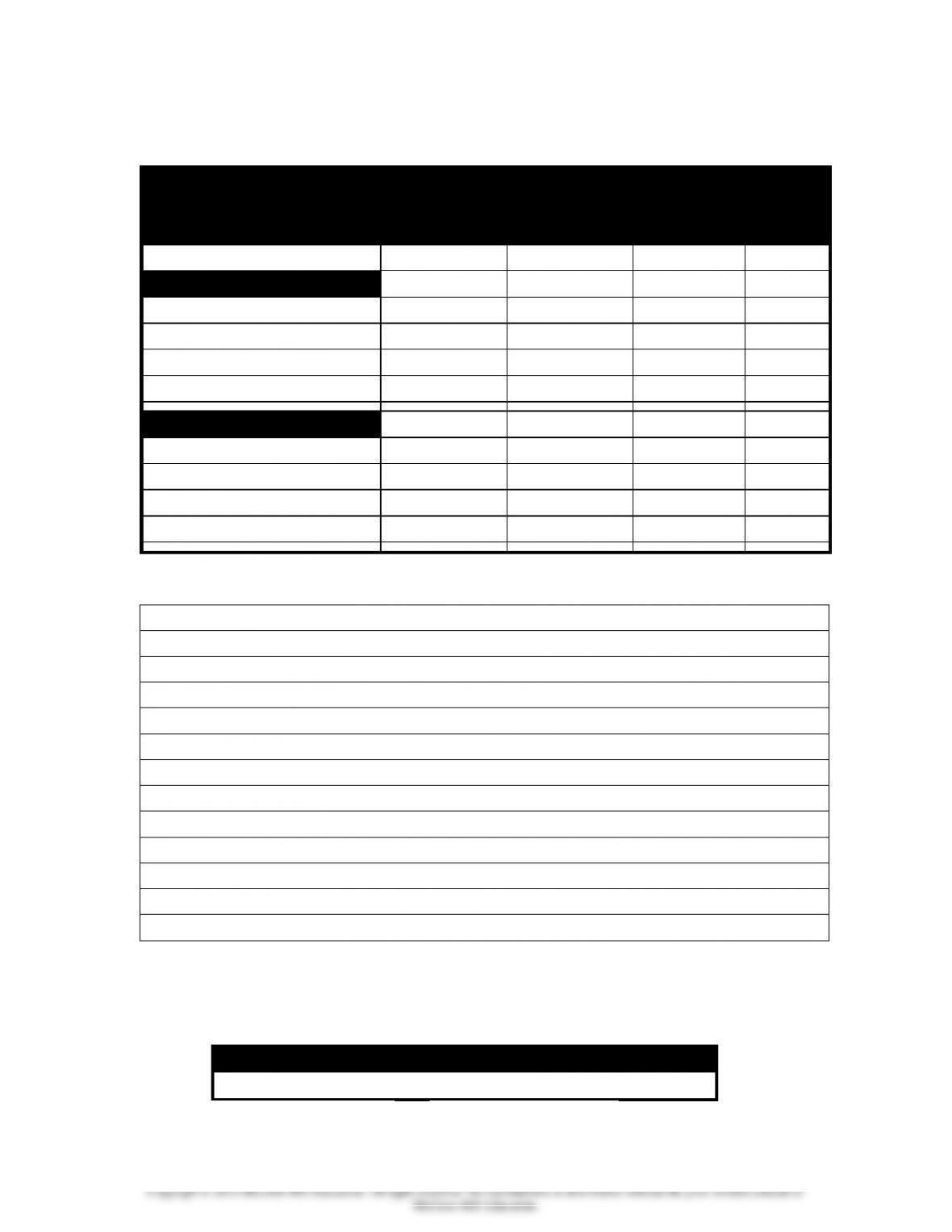

Demonstration Problem 15-3 Solution

a. b.

Western Chair Company

Static Budget, Flexible Budget, Volume Variances

Static

Budget

Flexible

Budget

Volume

Variances

F or

UF

Number of Units

43,000

44,000

1,000

F

Sales Revenue

$2,666,000

$2,728,000

$62,000

F

Variable Costs

Direct Material

688,000

704,000

16,000

UF

Direct Labor

516,000

528,000

12,000

UF

Overhead

602,000

616,000

14,000

UF

G,S,&A

344,000

352,000

8,000

UF

Contribution Margin

516,000

528,000

12,000

F

Fixed Costs

Manufacturing

120,400

120,400

0

G,S,&A

67,000

67,000

0

Net Income

$ 328,600

$ 340,600

$12,000

F

Chapter 15 – Performance Evaluation

15-3

Demonstration Problem 15-3 Solution continued

b. The 1,000-unit favorable volume variance is usually

to higher than expected sales revenue.

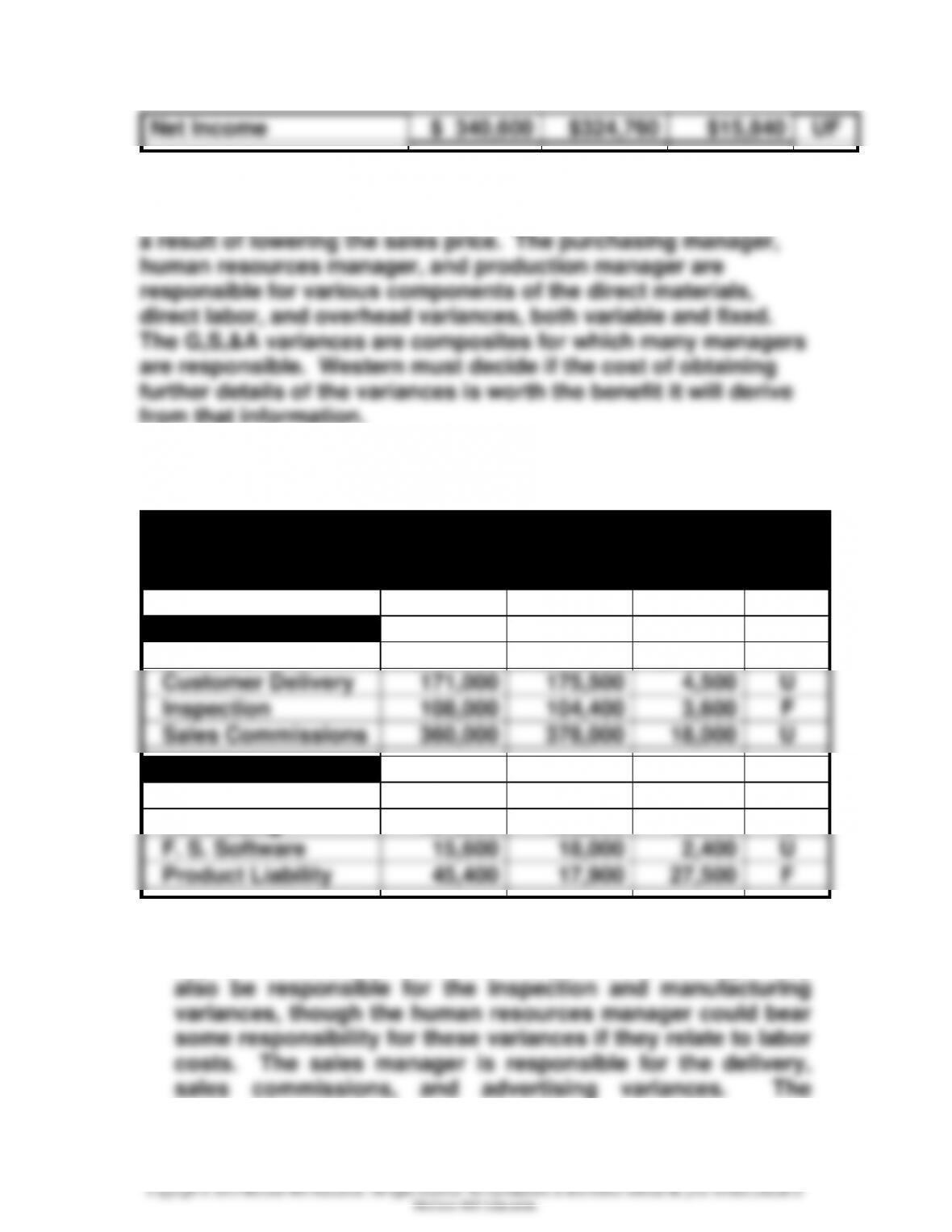

The production manager is responsible for many of the

manufacturing cost variances. The purchasing manager and

human resources manager also share some of the responsibility

necessarily caused increased production costs.

The G,S,&A variance is a composite for which many managers

from that information. Demonstration Problem 15-3

Solution continued

c.

Western Chair Company

Flexible Budget, Actual Results, Flexible Budget Variances

Flexible

Budget

Actual

Results

Flex. Bud.

Variances

F or

UF

Number of Units

44,000

44,000

0

Sales Revenue

$2,728,000

$2,640,000

$88,000

UF

Variable Costs

Direct Material

704,000

718,960

14,960

UF

Direct Labor

528,000

480,480

47,520

F

Overhead

616,000

624,800

8,800

UF

G,S,&A

352,000

308,000

44,000

F

Contribution Margin

528,000

507,760

20,240

UF

Fixed Costs

Manufacturing

120,400

114,000

6,400

F

G,S,&A

67,000

69,000

2,000

UF

Chapter 15 – Performance Evaluation

15-4

Net Income

$ 340,600

$324,760

$15,840

UF

The marketing manager is responsible for the sales revenue

variance. In this instance, it appears sales volume increased as

from that information.

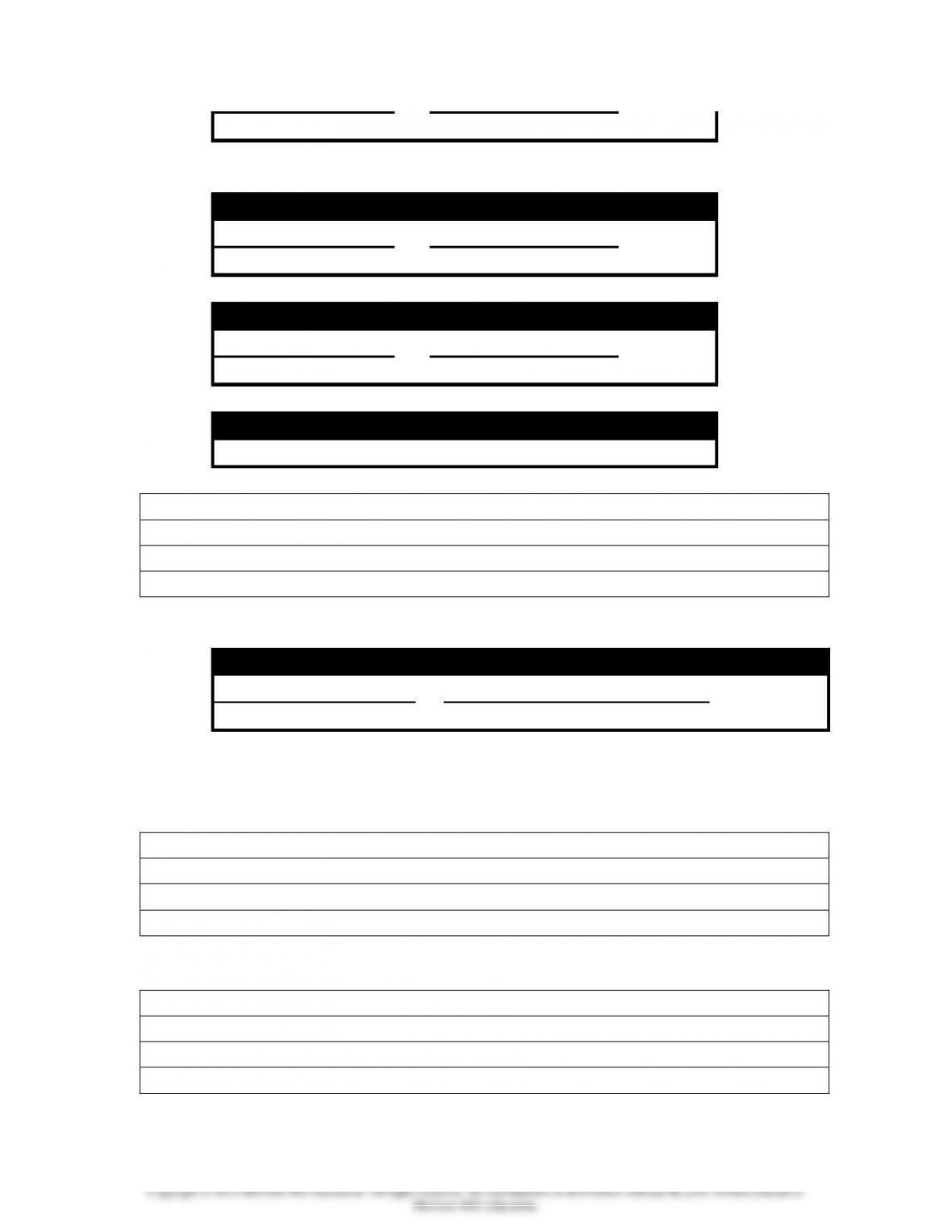

Demonstration Problem 15-4 Solution

a.

Sweeney Company

Responsibility Report

For 2014

Budget

Actual

Variance

F or U

Variable Costs:

Materials

$1,980,000

$1,962,000

$18,000

F

Customer Delivery

171,000

175,500

4,500

U

Inspection

108,000

104,400

3,600

F

Sales Commissions

360,000

378,000

18,000

U

Fixed Costs:

Manufacturing

720,000

708,000

12,000

F

Advertising

107,000

120,000

13,000

U

F. S. Software

15,600

18,000

2,400

U

Product Liability

45,400

17,900

27,500

F

b. The purchasing and production managers should be able to

explain the materials variance. The production manager may

Chapter 15 – Performance Evaluation

15-5

information services or accounting departments can probably

explain the variance related to financial statement software.

Demonstration Problem 15-5 Solution

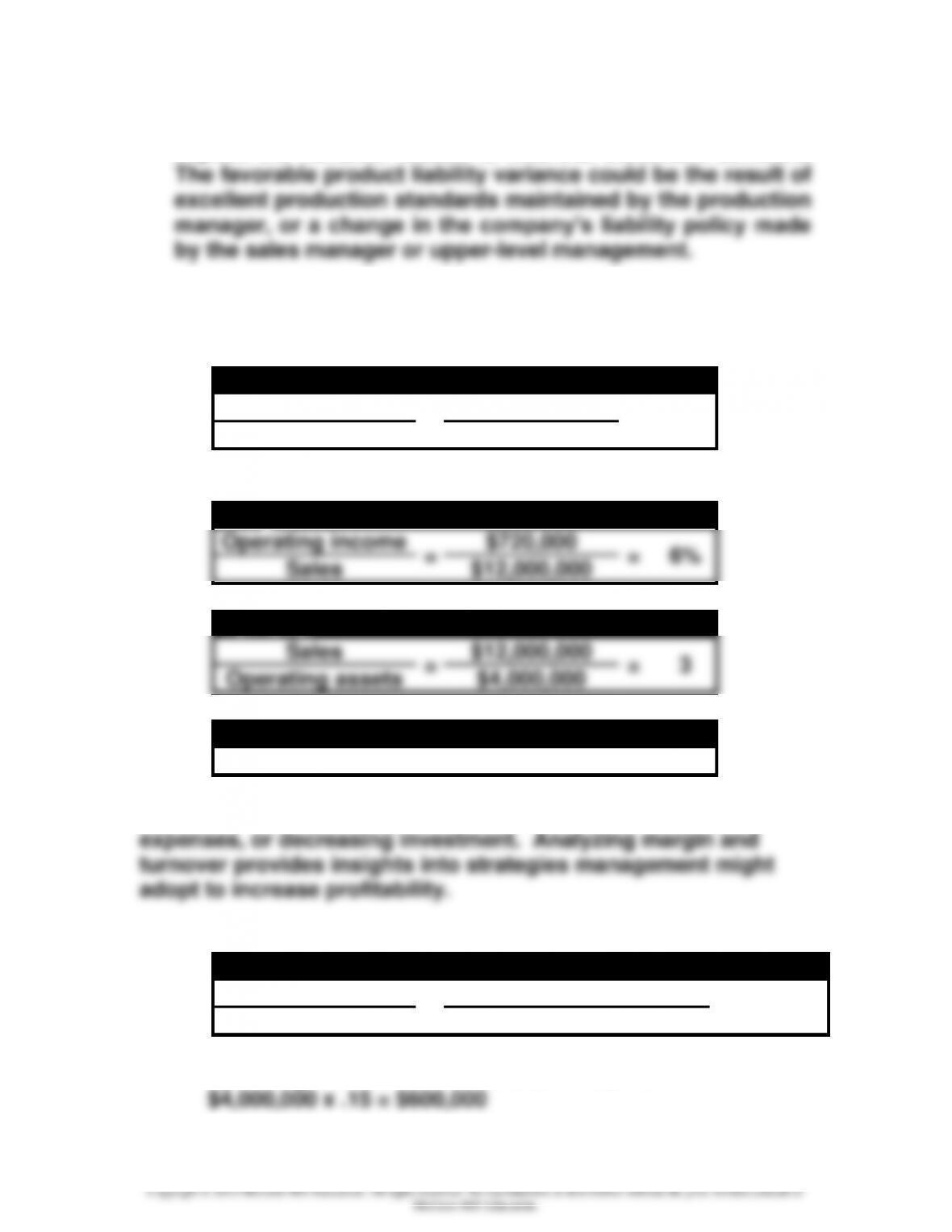

a.

ROI for Hydride Division

Operating income

=

$720,000

=

18%

Operating assets

$4,000,000

b.

Margin

Operating income

=

$720,000

=

6%

Sales

$12,000,000

Turnover

Sales

=

$12,000,000

=

3

Operating assets

$4,000,000

Margin

x

Turnover

=

ROI

6%

x

3

=

18%

Management can increase ROI by increasing sales, reducing

c.

Hydride Division ROI with Additional Investment

Operating income

=

$720,000 + $600,000*

=

16.5%

Operating assets

$4,000,000 + $4,000,000

*Operating income from additional investment:

Chapter 15 – Performance Evaluation

15-6

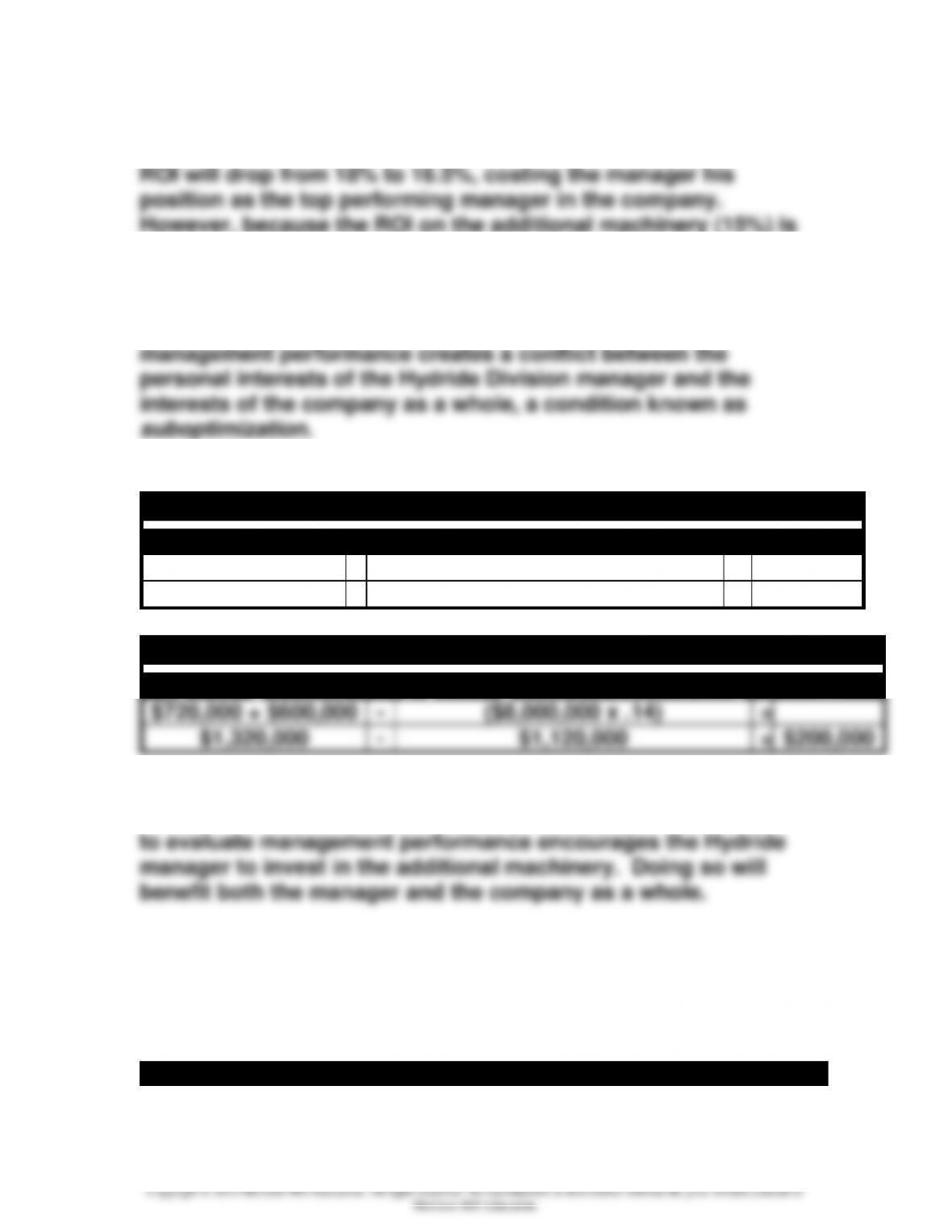

If Hydride’s manager buys the additional machinery, Hydride’s

However, because the ROI on the additional machinery (15%) is

Demonstration Problem 15-5 Solution continued

higher than the company-wide ROI (14%), the company’s overall

ROI would increase with the investment. Using ROI to evaluate

d.

Residual Income without Additional Investment

Operating income

–

(Operating assets x Desired ROI)

=

RI

$720,000

–

($4,000,000 x .14)

=

$720,000

–

$560,000

=

$160,000

Residual Income with Additional Investment

Operating income

–

(Operating assets x Desired ROI)

=

RI

$720,000 + $600,000

–

($8,000,000 x .14)

=

$1,320,000

–

$1,120,000

=

$200,000

If Hydride’s manager buys the additional machinery, Hydride’s

residual income will increase by $40,000. Using residual income

Demonstration Problem 15-1 Work Papers

a. b.

Organization Chart

Level

Chapter 15 – Performance Evaluation

15-7

1

2

3

4

c.

Demonstration Problem 15-2 Work Paper

Item

Budget

Actual

Variance

F or UF

Selling and Admin. Exp.

$ 29,000

$ 27,000

Sales Revenue

$310,000

$325,000

Materials Price

$2.00 per lb.

$2.10 per lb.

Cost of Goods Sold

$125,000

$100,000

Chapter 15 – Performance Evaluation

15-8

Materials Purchases

$250,000

$265,000

Materials Usage

6,000 lbs.

5,800 lbs.

Sales Price

$550 each

$500 each

Labor Rate

$8.10 per hr.

$7.95 per hr.

Production Volume

950 units

900 units

Labor Usage

$ 96,000

$ 97,000

Research and Dev. Exp.

$ 22,000

$ 25,000

Demonstration Problem 15-3 Work Papers

a. b.

Western Chair Company

Static Budget, Flexible Budget, Volume Variances

Static

Budget

Flexible

Budget

Volume

Variances

F or

UF

Number of Units

Sales Revenue

Variable Costs

Direct Material

Direct Labor

Overhead

G,S,&A

Contribution Margin

Fixed Costs

Manufacturing

G,S,&A

Net Income

Demonstration Problem 15-3 Work Papers continued

b.

Chapter 15 – Performance Evaluation

15-9

c.

Western Chair Company

Flexible Budget, Actual Results, Flexible Budget Variances

Flexible

Budget

Actual

Results

Flex. Bud.

Variances

F or

UF

Number of Units

Sales Revenue

Variable Costs

Direct Material

Direct Labor

Overhead

G,S,&A

Contribution Margin

Fixed Costs

Manufacturing

G,S,&A

Net Income

Demonstration Problem 15-3 Work Papers continued

c.

Demonstration Problem 15-4 Work Papers

Chapter 15 – Performance Evaluation

15–10

a.

Sweeney Company

Responsibility Report

For 2014

Budget

Actual

Variance

F or U

Variable Costs:

Materials

Customer Delivery

Inspection

Sales Commissions

Fixed Costs:

Manufacturing

Advertising

F. S. Software

Product Liability

b.

Demonstration Problem 15-5 Work Papers

a.

ROI for Hydride Division

=

=

Chapter 15 – Performance Evaluation

15–11

b.

Margin

=

=

Turnover

=

=

Margin

x

Turnover

=

ROI

x

=

c.

Hydride Division ROI with Additional Investment

Operating income

=

=

Operating assets

*Operating income from additional investment:

Demonstration Problem 15-5 Work Papers continued

c.