11-8

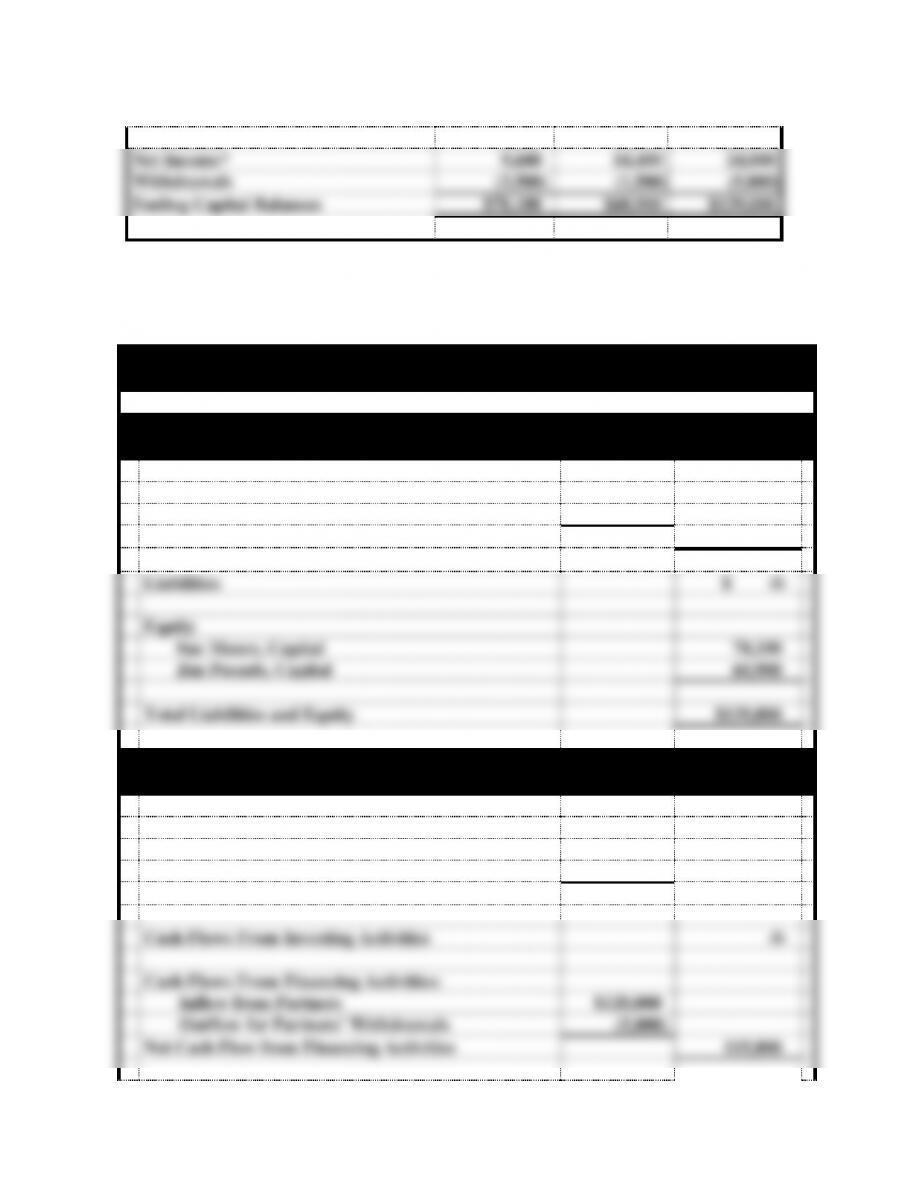

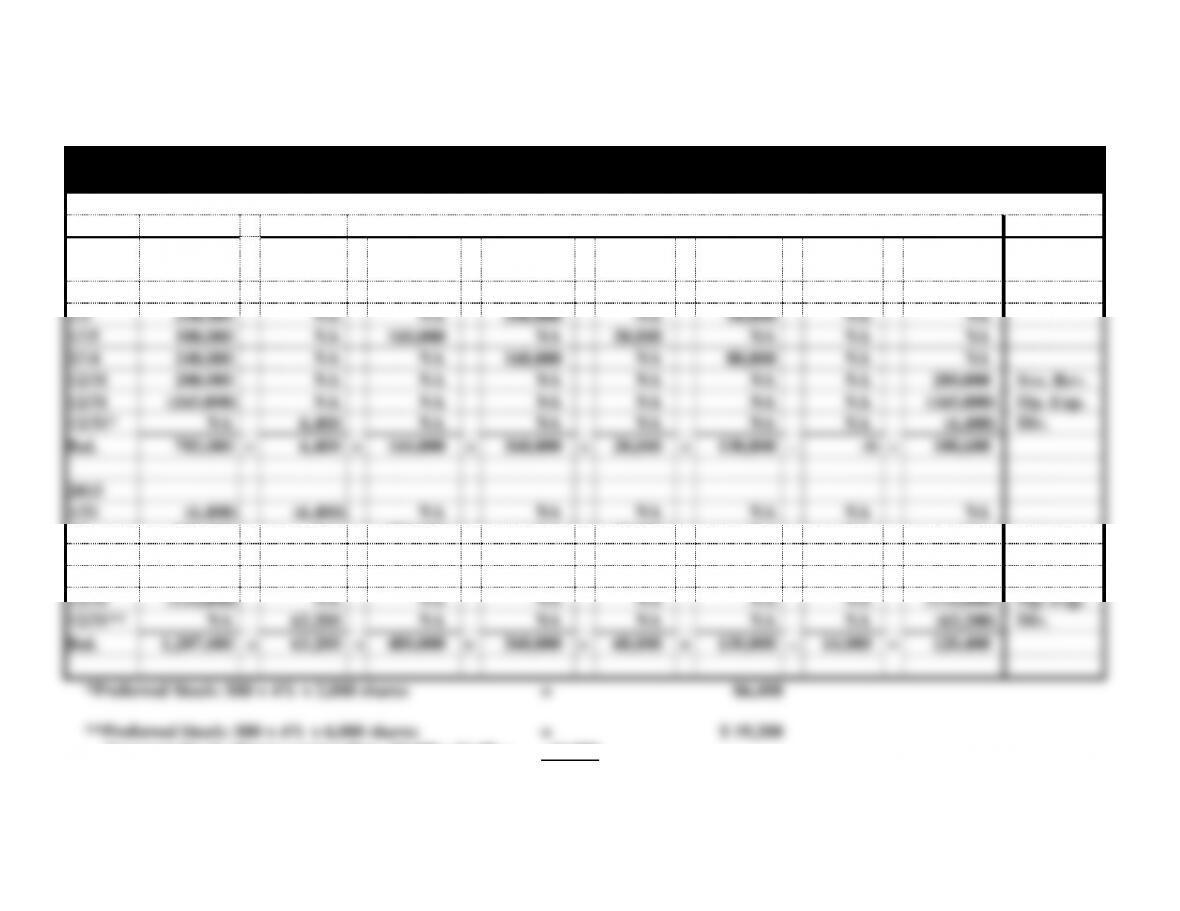

Investments

72,000

48,000

120,000

Net Income*

9,600

14,400

24,000

Withdrawals

(3,500)

(1,500)

(5,000)

Ending Capital Balances

$78,100

$60,900

$139,000

*Moore: $24,000 x 40% = $9,600

Pounds: $24,000 x 60% = $14,400

PROBLEM 8-18 b. (cont.)

Auto Spa Company

Financial Statements

Balance Sheet

As of December 31, 2014

Assets

Cash

$139,000

Total Assets

$139,000

Liabilities

$ -0-

Equity

Sue Moore, Capital

78,100

Jim Pounds, Capital

60,900

Total Liabilities and Equity

$139,000

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash Flows From Operating Activities:

Inflow from Revenues

$ 80,000

Outflow for Expenses

(56,000)

Net Cash Flow from Operating Activities

$ 24,000

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Inflow from Partners

$120,000

Outflow for Partners’ Withdrawals

(5,000)

Net Cash Flow from Financing Activities

115,000

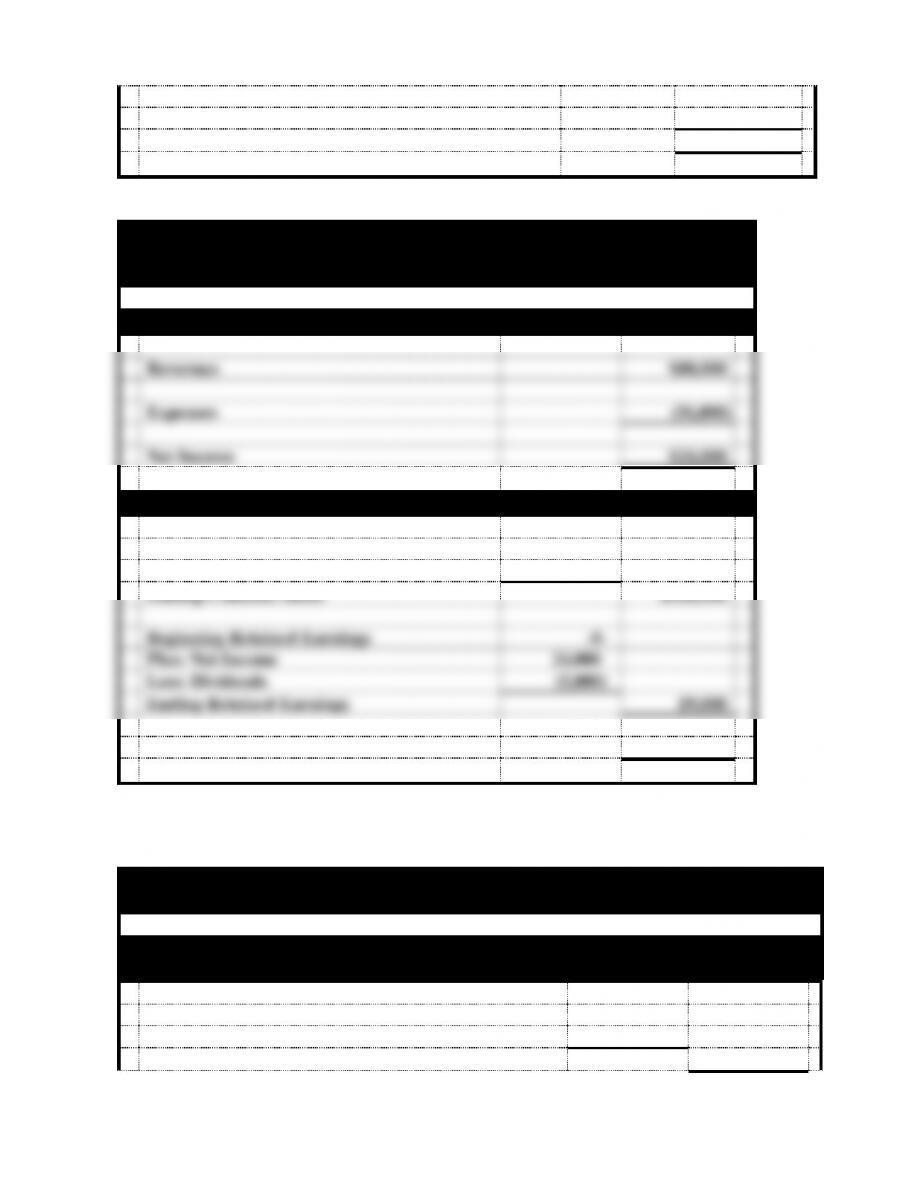

11-9

Net Change in Cash

139,000

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$139,000

PROBLEM 8-18 (cont.)

c. Corporation

Auto Spa, Inc.

Financial Statements

For the Year Ended December 31, 2014

Income Statement

Revenues

$80,000

Expenses

(56,000)

Net Income

$24,000

Statement of Changes in Stockholders’ Equity

Beginning Common Stock

$ -0-

Plus: Issuance of Common Stock

120,000

Ending Common Stock

$120,000

Beginning Retained Earnings

-0-

Plus: Net Income

24,000

Less: Dividends

(5,000)

Ending Retained Earnings

19,000

Total Stockholders’ Equity

$139,000

PROBLEM 8-18 c. (cont.)

Auto Spa, Inc.

Financial Statements

Balance Sheet

As of December 31, 2014

Assets

Cash

$139,000

Total Assets

$139,000

11–10

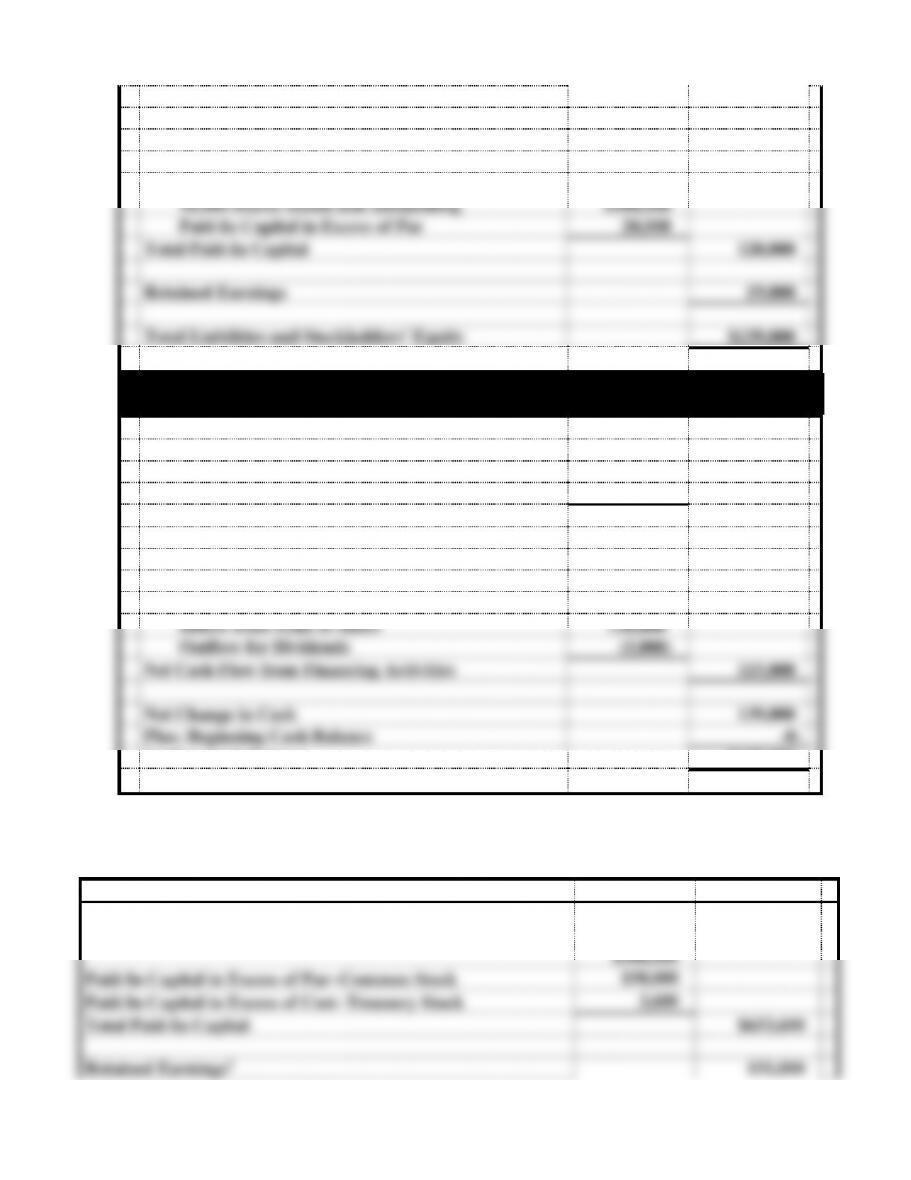

Liabilities

$ -0-

Stockholders’ Equity

Common Stock, $10 par value,

10,000 shares issued and outstanding

$100,000

Paid-In Capital in Excess of Par

20,000

Total Paid-In Capital

120,000

Retained Earnings

19,000

Total Liabilities and Stockholders’ Equity

$139,000

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash Flows From Operating Activities:

Inflow from Revenues

$80,000

Outflow for Expenses

(56,000)

Net Cash Flow from Operating Activities

$ 24,000

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Inflow from Issue of Stock

120,000

Outflow for Dividends

(5,000)

Net Cash Flow from Financing Activities

115,000

Net Change in Cash

139,000

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$139,000

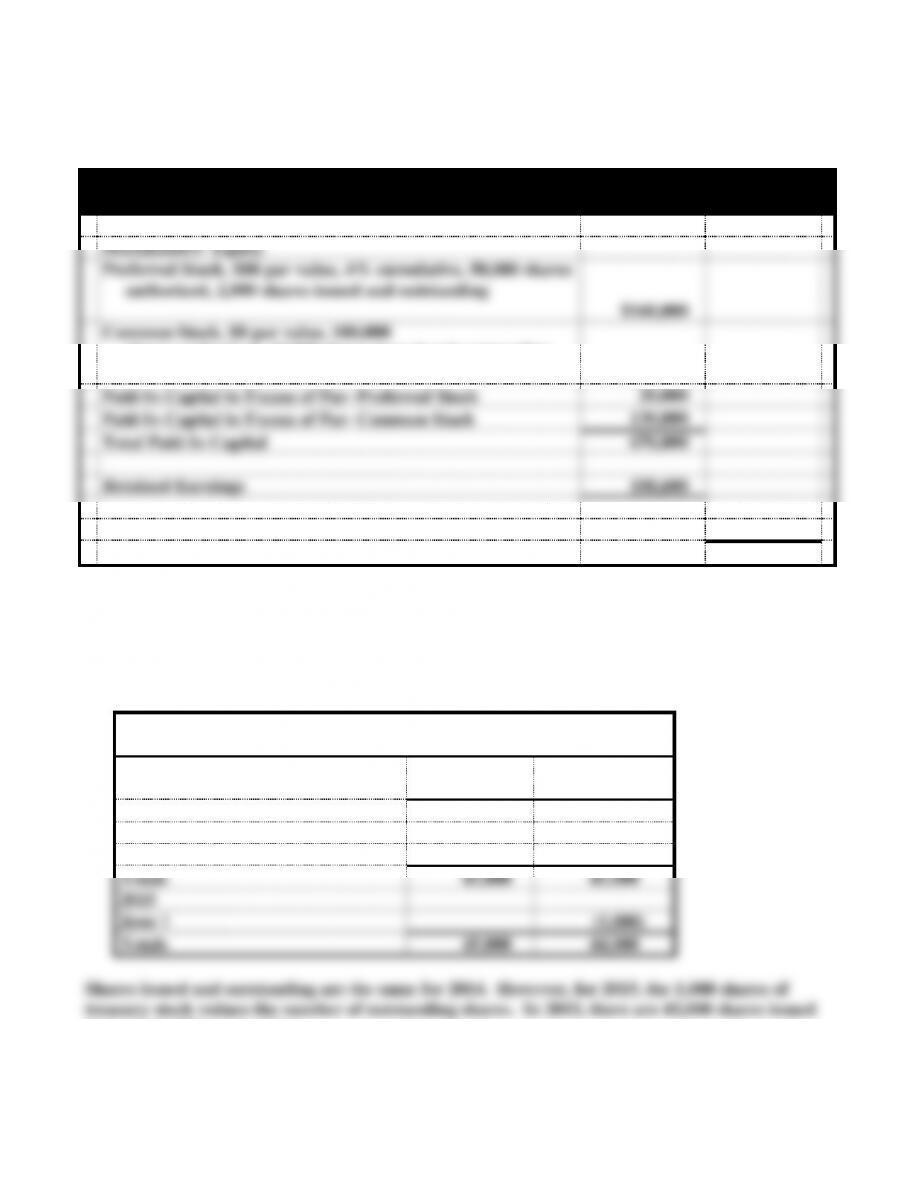

PROBLEM 8-19

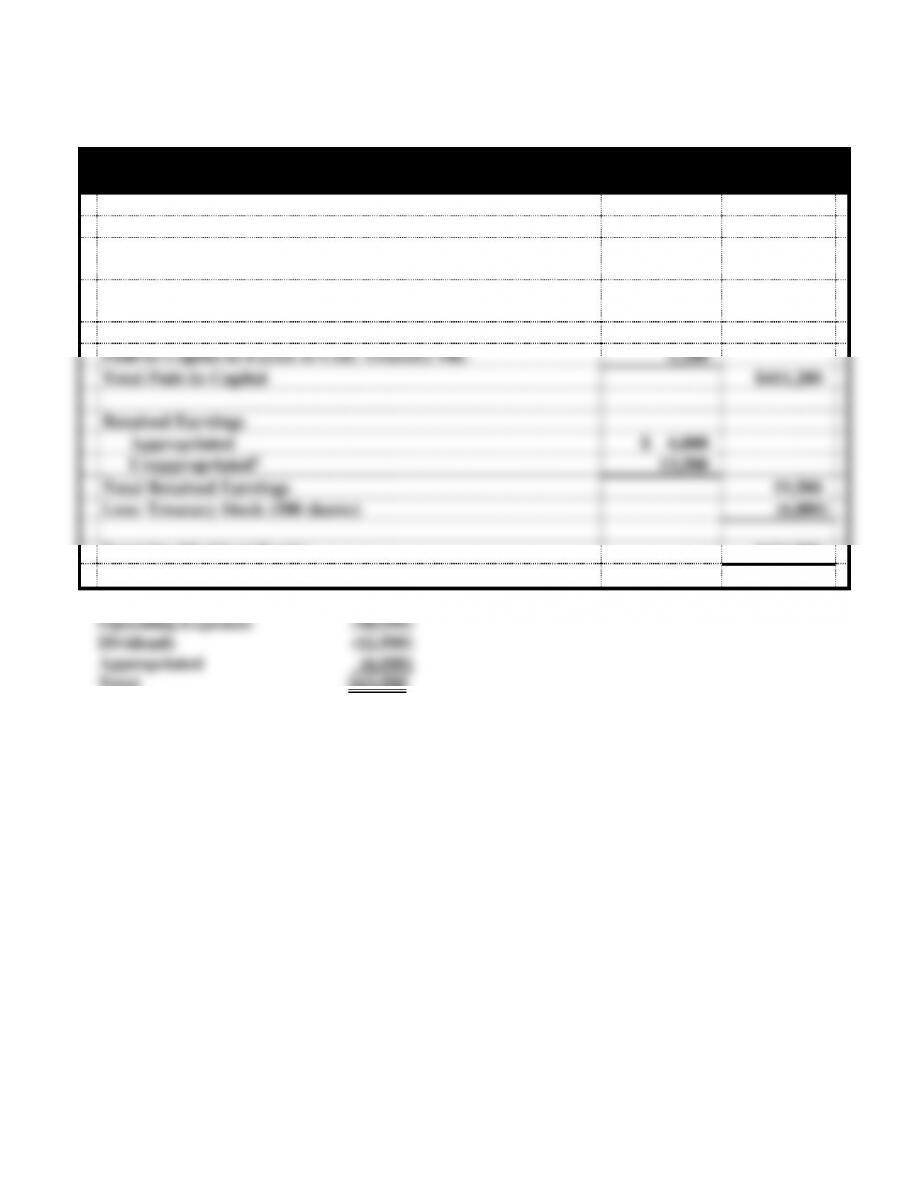

Stockholders’ Equity

Common Stock, $10 par value, 100,000 shares authorized,

50,000 shares issued, and 49,200 shares outstanding

$500,000

Paid-In Capital in Excess of Par−Common Stock

150,000

Paid-In Capital in Excess of Cost−Treasury Stock

3,600

Total Paid-In Capital

$653,600

Retained Earnings1

151,000

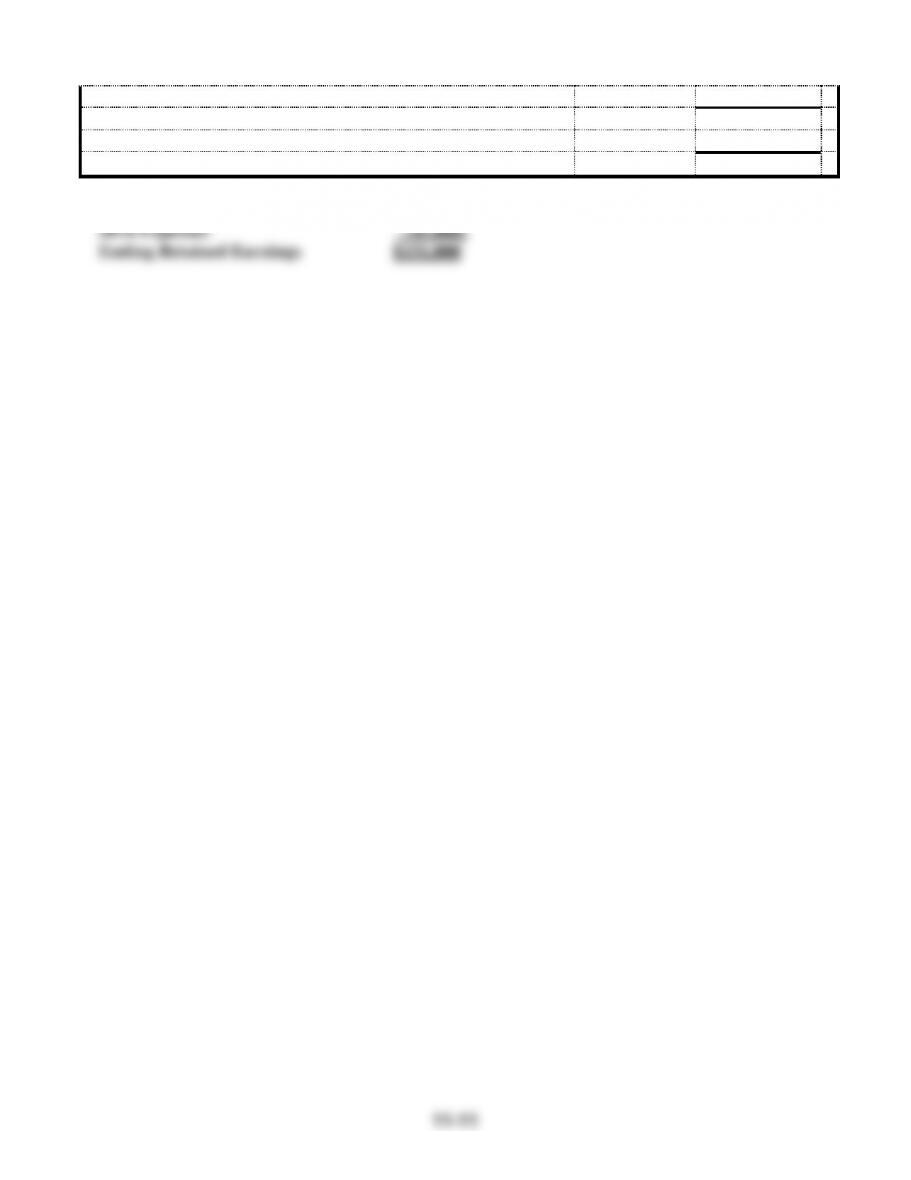

Less: Treasury Stock (800 shares)

(12,000)

Total Stockholders’ Equity

$792,600

1 Beginning Retained Earnings $120,000

2014 Revenues 72,000

8-12

PROBLEM 8-20

a.

Malard Corporation

Accounting Equation

Event

Assets

=

Liabilities

Stockholders’ Equity

Cash

=

Div. Pay.

+

Pfd. Stk.

+

Com. Stk.

+

PIC in

Exc. PS

+

PIC in

Exc. CS

−

Treasury

Stock

+

Ret. Earn.

Acct. Title

R/E

2014

1/2

250,000

NA

NA

200,000

NA

50,000

NA

NA

1/15

180,000

NA

160,000

NA

20,000

NA

NA

NA

2/14

240,000

NA

NA

160,000

NA

80,000

NA

NA

12/31

280,000

NA

NA

NA

NA

NA

NA

280,000

Svc. Rev.

12/31

(165,000)

NA

NA

NA

NA

NA

NA

(165,000)

Op. Exp.

12/31*

NA

6,400

NA

NA

NA

NA

NA

(6,400)

Div.

Bal.

785,000

=

6,400

+

160,000

+

360,000

+

20,000

+

130,000

−

-0-

+

108,600

2015

1/31

(6,400)

(6,400)

NA

NA

NA

NA

NA

NA

3/1

368,000

NA

320,000

NA

48,000

NA

NA

NA

6/1

(14,000)

NA

NA

NA

NA

NA

14,000

NA

12/31

185,000

NA

NA

NA

NA

NA

NA

185,000

Svc. Rev.

12/31

(110,000)

NA

NA

NA

NA

NA

NA

(110,000)

Op. Exp.

12/31**

NA

63,200

NA

NA

NA

NA

NA

(63,200)

Div.

Bal.

1,207,600

=

63,200

+

480,000

+

360,000

+

68,000

+

130,000

−

14,000

+

120,400

*Preferred Stock: $80 x 4% x 2,000 shares = $6,400

**Preferred Stock: $80 x 4% x 6,000 shares = $ 19,200

Common Stock: Shares outstanding, 44,000 x $1.00 = 44,000

Total Dividend $63,200

8-13

PROBLEM 8-20 (cont.)

b.

2014

Malard Coproration

December 31, 2014

Stockholders’ Equity

Preferred Stock, $80 par value, 4% cumulative, 50,000 shares

authorized, 2,000 shares issued and outstanding

$160,000

Common Stock, $8 par value, 100,000

shares authorized, 45,000 shares issued and outstanding

360,000

Paid-In Capital in Excess of Par−Preferred Stock

20,000

Paid-In Capital in Excess of Par−Common Stock

130,000

Total Paid-In Capital

670,000

Retained Earnings

108,600

Total Stockholders’ Equity

$778,600

PROBLEM 8-20 c. (cont.)

c.

Schedule provided for use of instructor.

Schedule of Number of

Shares of Common Stock

Shares Issued

Shares

Outstanding

2014

Jan. 2

25,000

25,000

Feb. 14

20,000

20,000

Totals

45,000

45,000

2015

June 1

(1,000)

Totals

45,000

44,000

but only 44,000 outstanding.

8-14

PROBLEM 8-20 (cont.)

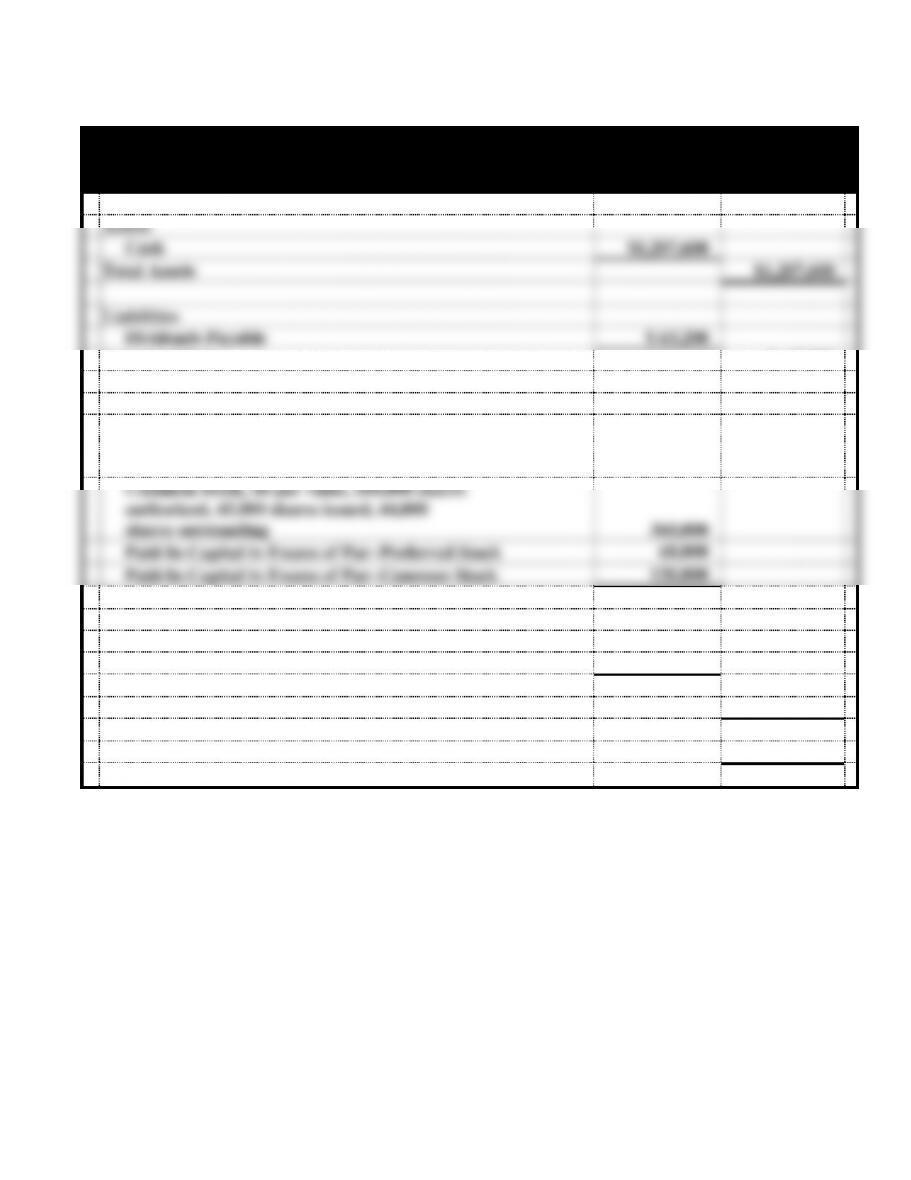

c.

Malard Corporation

Balance Sheet

As of December 31, 2015

Assets

Cash

$1,207,600

Total Assets

$1,207,600

Liabilities

Dividends Payable

$ 63,200

Total Liabilities

$ 63,200

Stockholders’ Equity

Preferred Stock, $80 par value, 4%

cumulative, 50,000 shares authorized,

6,000 shares issued and outstanding

$480,000

Common Stock, $8 par value, 100,000 shares

authorized, 45,000 shares issued, 44,000

shares outstanding

360,000

Paid-In Capital in Excess of Par−Preferred Stock

68,000

Paid-In Capital in Excess of Par−Common Stock

130,000

Total Paid-In Capital

1,038,000

Retained Earnings

120,400

Less: Treasury Stock

(14,000)

Total Stockholders’ Equity

1,144,400

Total Liabilities and Stockholders’ Equity

$1,207,600

8-15

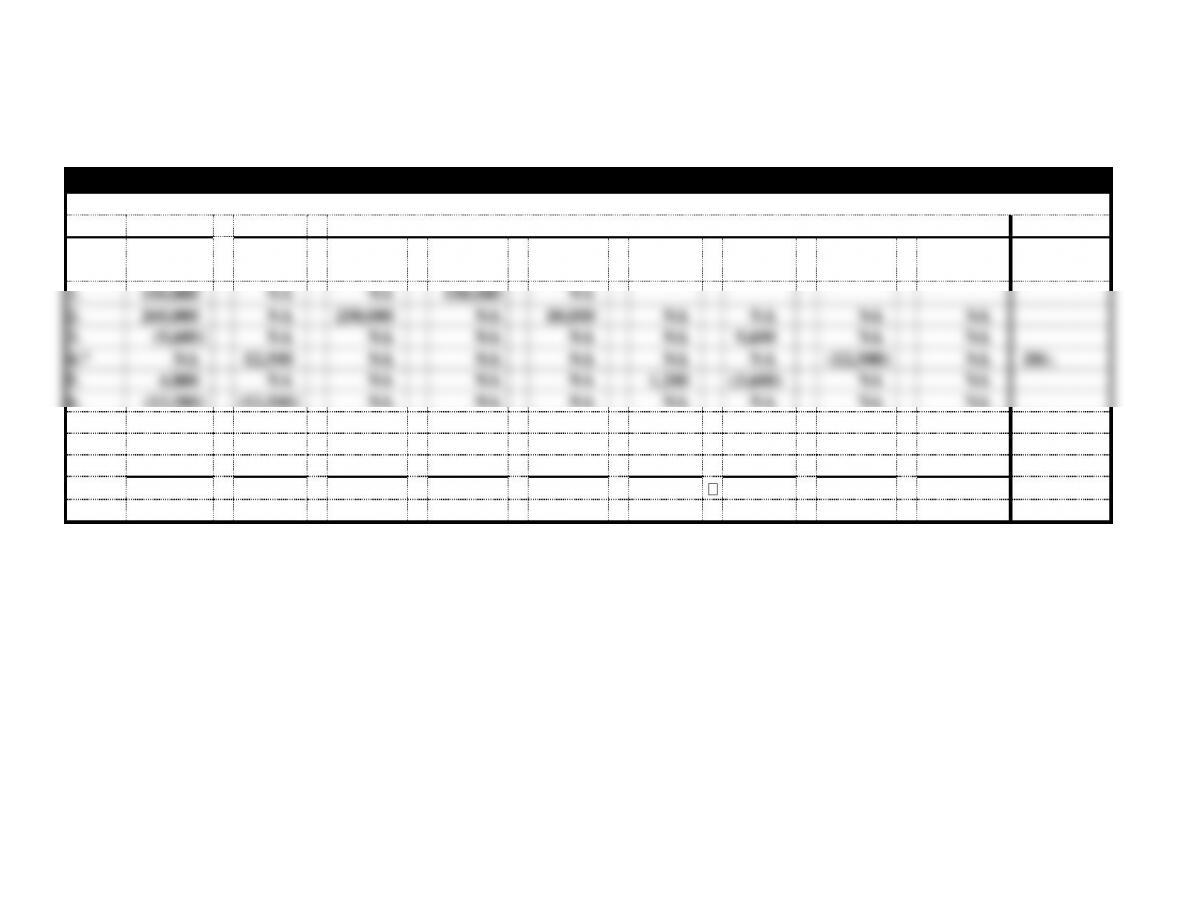

PROBLEM 8-21

a.

Prairie Corp. Accounting Equation 2014

Event

Assets

=

Liab.

Stockholders’ Equity

Cash

=

Div.

Pay.

+

Pfd. Stk.

+

Com. Stk.

+

PIC in

Exc. PS

+

PIC in

Exc. TS

−

Treas.

Stock

+

Ret.

Earn.

+

App. Ret.

Earn.

Acct. Title

R/E

1.

150,000

NA

NA

150,000

NA

2.

260,000

NA

250,000

NA

10,000

NA

NA

NA

NA

3.

(9,600)

NA

NA

NA

NA

NA

9,600

NA

NA

4.*

NA

12,500

NA

NA

NA

NA

NA

(12,500)

NA

Div.

5.

4,800

NA

NA

NA

NA

1,200

(3,600)

NA

NA

6.

(12,500)

(12,500)

NA

NA

NA

NA

NA

NA

NA

7a.

80,000

NA

NA

NA

NA

NA

NA

80,000

NA

Rev.

7b.

(48,000)

NA

NA

NA

NA

NA

NA

(48,000)

NA

Op. Exp.

8.

NA

NA

NA

NA

NA

NA

NA

(6,000)

6,000

Totals

424,700

=

-0-

+

250,000

+

150,000

+

10,000

+

1,200

6,000

+

13,500

+

6,000

*$50 x 5% = $2.50; $2.50 x 5,000 = $12,500

11–16

PROBLEM 8-21 (cont.)

b.

Prairie Corp.

December 31, 2014

Stockholders’ Equity

Preferred Stock, $50 stated value, 5,000 shares issued and

outstanding

$ 250,000

Common Stock, $10 par value, 15,000 shares

issued, and 14,500 shares outstanding

150,000

Paid-In Capital in Excess of Stated Value Pref. Stk.

10,000

Paid-In Capital in Excess of Cost, Treasury Stk.

1,200

Total Paid-In Capital

$411,200

Retained Earnings

Appropriated

$ 6,000

Unappropriated1

13,500

Total Retained Earnings

19,500

Less: Treasury Stock (500 shares)

(6,000)

Total Stockholders’ Equity

$424,700

1 Service Revenue $80,000

Total $13,500