Chapter 12 Cost Accumulation, Tracing, and Allocation

12-1

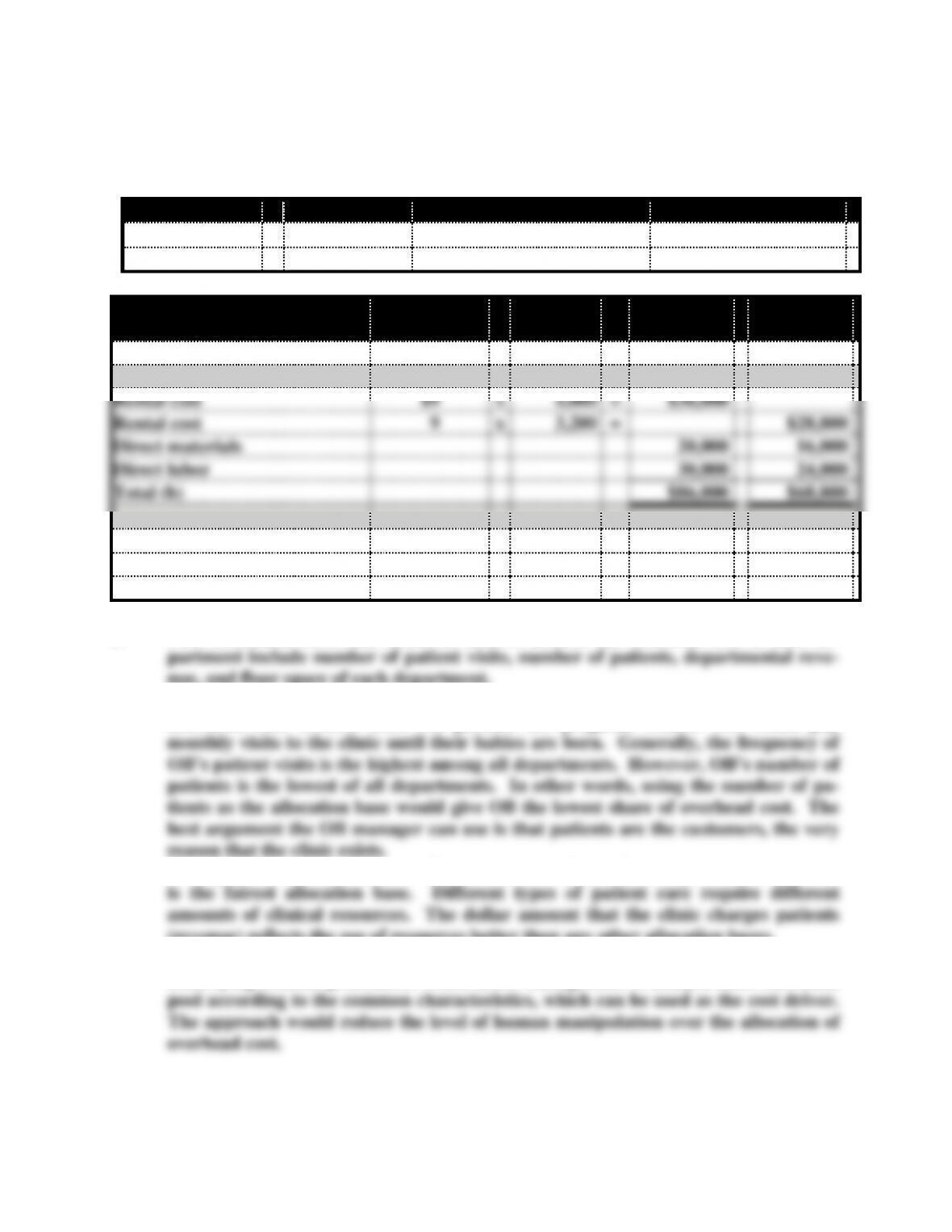

Exercise 12-12

The allocation rate is computed below:

Cost

÷

Base

Computation

Allocation Rate

Rental cost

÷

No. units

$360,000 ÷ 40,000 =

$9 per unit

Allocation

Rate

x

Weight

of Base

=

January

February

Number of units (a)

4,000

3,200

Rental cost

$9

x

4,000

=

$36,000

Rental cost

9

x

3,200

=

$28,800

Direct materials

20,000

16,000

Direct labor

30,000

24,000

Total (b)

$86,000

$68,800

Cost per unit [c =(b ÷ a)]

$21.50

$21.50

Price (c x 1.40)

$30.10

$30.10

Exercise 12-1

a. Four allocation bases that could be used to allocate the overhead cost to each de-

nue, and floor space of each department.

b. The manager of OB would most likely recommend the number of patients as the

allocation base because most OB patients are pregnant women who would pay

c. If the president cares about the financial health of the clinic, departmental revenue

(revenue) reflects the use of resources better than any other allocation bases.

d. Classifying overhead costs into separate pools based on the characteristics of the

underlying medical procedures would allow management to analyze each individual

Problem 12-14

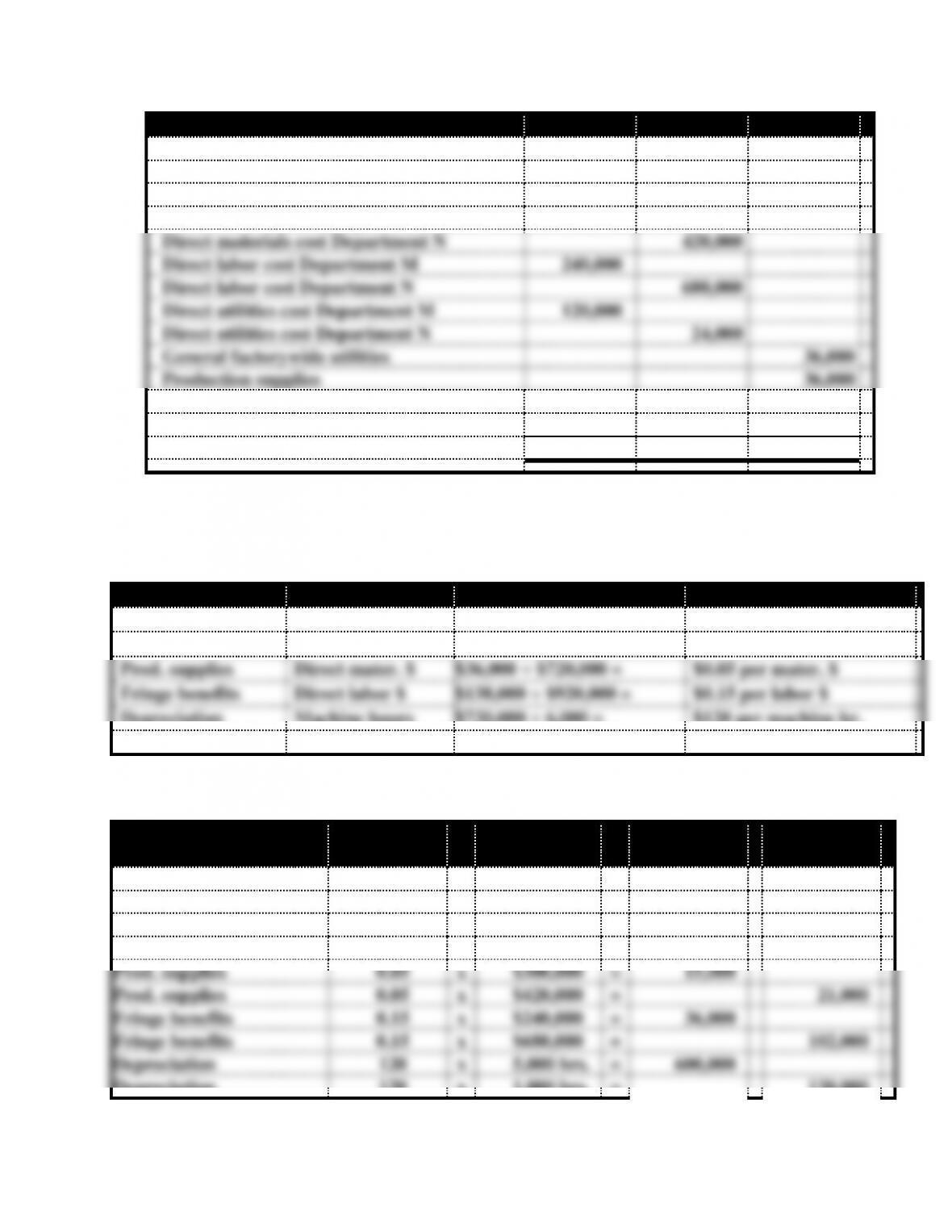

Chapter 12 Cost Accumulation, Tracing, and Allocation

12-2

Cost Assignment Categories

Dept. M

Dept. N

Indirect

Salary of V. P. of production division

$ 200,000

Salary of supervisor Department M

$ 80,000

Salary of supervisor Department N

$ 60,000

Direct materials cost Department M

300,000

Direct materials cost Department N

420,000

Direct labor cost Department M

240,000

Direct labor cost Department N

680,000

Direct utilities cost Department M

120,000

Direct utilities cost Department N

24,000

General factorywide utilities

36,000

Production supplies

36,000

Fringe benefits

138,000

Depreciation

720,000

Total costs

$740,000

$1,184,000

$1,130,000

b. The following bases were used to allocate the various indirect costs. Logical

arguments for other bases may be possible. The bases and computations used

herein are as follows:

Cost

Base

Computation

Allocation Rate

Salary of VP

No. of depts.

$200,000 ÷ 2 =

$100,000 per dept.

General utilities

Direct utility $

$36,000 ÷ $144,000 =

$0.25 per utility $

Prod. supplies

Direct mater. $

$36,000 ÷ $720,000 =

$0.05 per mater. $

Fringe benefits

Direct labor $

$138,000 ÷ $920,000 =

$0.15 per labor $

Depreciation

Machine hours

$720,000 ÷ 6,000 =

$120 per machine hr.

Problem 12-14 (continued)

Indirect

Costs

Allocation

Rate

x

Weight

of Base

=

Allocated

To Dept. M

Allocated

To Dept. N

Salary of VP

$100,000

x

1 dept.

=

$100,000

Salary of VP

100,000

x

1 dept.

=

$100,000

General utilities

0.25

x

$120,000

=

30,000

General utilities

0.25

x

$24,000

=

6,000

Prod. supplies

0.05

x

$300,000

=

15,000

Prod. supplies

0.05

x

$420,000

=

21,000

Fringe benefits

0.15

x

$240,000

=

36,000

Fringe benefits

0.15

x

$680,000

=

102,000

Depreciation

120

x

5,000 hrs.

=

600,000

Depreciation

120

x

1,000 hrs.

=

120,000

a.

Chapter 12 Cost Accumulation, Tracing, and Allocation

12-3

Total allocated cost

$781,000

$349,000

Department

M

N

Total direct cost

$ 740,000

$1,184,000

Total indirect cost

781,000

349,000

Total production costs (a)

$1,521,000

$1,533,000

Number of units (b)

2,000

4,000

Cost per unit (c = a ÷ b)

$ 760.50

$383.25

Price (c x 1.4)

$1,064.70

$536.55

Problem 12-15

a. The objective is to determine the cost of operating each department. According-

ly, the cost objects are Departments 1, 2, and 3.

Problem 12-15 (continued)

Cost

Base

Computation

Allocation Rate

Telephone exp.

Number of telephones

$15,000 ÷ 100 =

$150 per telephone

Supplies exp.

No. of faculty members

$24,000 ÷ 60 =

$400 per instructor

Office rent

Square footage

$720,000 ÷ 36,000

$20 per sq. foot

Janitorial services

Square footage

$144,000 ÷ 36,000

$4 per sq. foot

Dean’s salary

No. of departments

$150,000 ÷ 3

$50,000 per dept.

There are other logical cost drivers. For example, students may have chosen to

c.

Dept.

Cost to be

Allocated

Allocation

Rate

x

Weight

of Base

=

Amount

Allocated

1

Telephone exp.

$150

x

20

=

$3,000

2

Telephone exp.

150

x

30

=

4,500

3

Telephone exp.

150

x

50

=

7,500

Total

$15,000

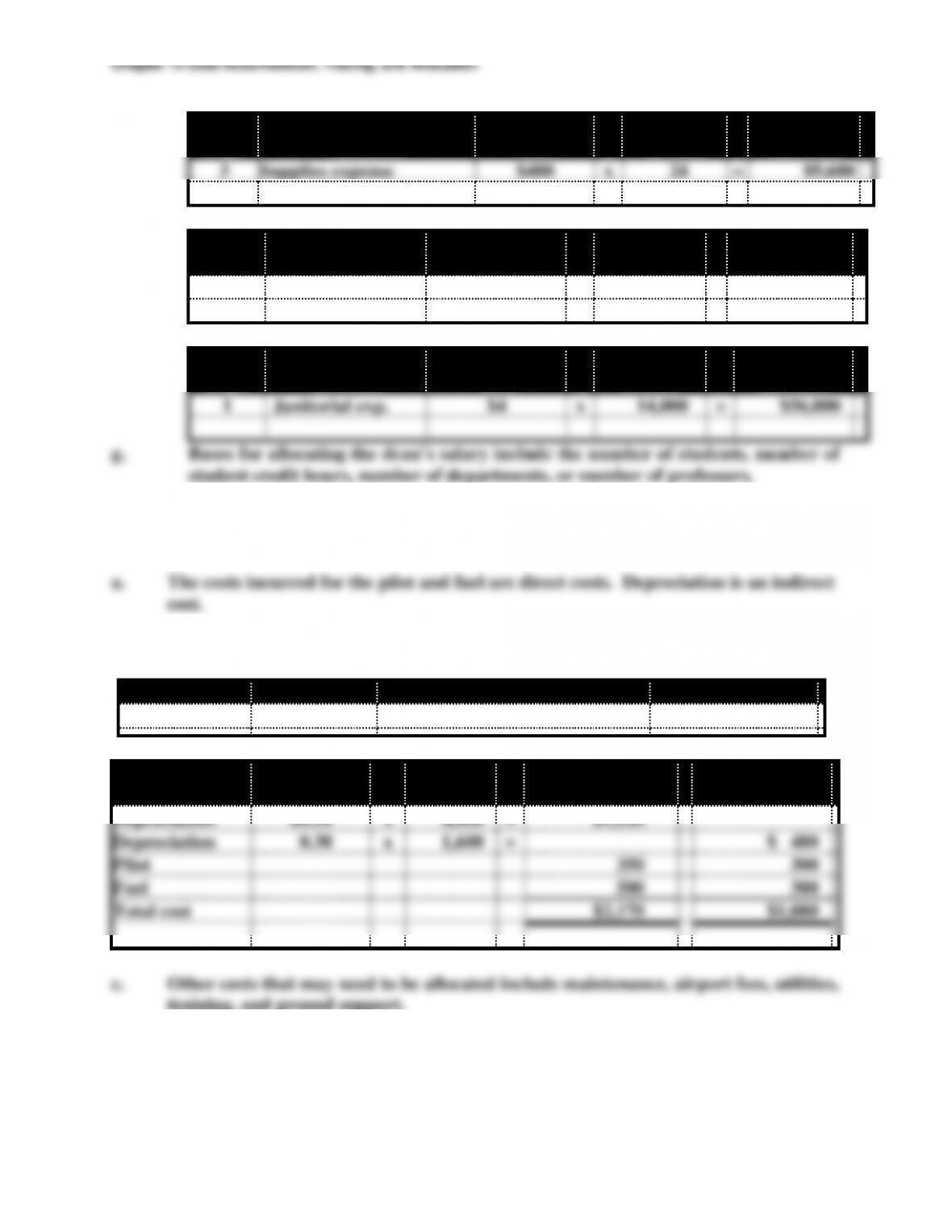

c.

12-4

d.

Dept.

Cost to be

Allocated

Allocation

Rate

x

Weight

of Base

=

Amount

Allocated

3

Supplies expense

$400

x

24

=

$9,600

e.

Dept.

Cost to be

Allocated

Allocation

Rate

x

Weight

of Base

=

Amount

Allocated

2

Office rent

$20

x

8,000

=

$160,000

f.

Dept.

Cost to be

Allocated

Allocation

Rate

x

Weight

of Base

=

Amount

Allocated

1

Janitorial exp.

$4

x

14,000

=

$56,000

Problem 12-16

b. The allocation rate for the depreciation is determined as follows:

Cost

Base

Computation

Allocation Rate

Depreciation

No. of miles

$6,000,000 ÷ 20,000,000 =

$0.30 per mile

Costs

Allocation

Rate

x

Weight

of Base

=

Chicago to

San Francisco

Chicago to

New York

Depreciation

$0.30

x

4,400

=

$1,320

Depreciation

0.30

x

1,600

=

$ 480

Pilot

350

300

Fuel

500

300

Total cost

$2,170

$1,080

training, and ground support.

Problem 12-17

Chapter 12 Cost Accumulation, Tracing, and Allocation

a. Changes in the number of tents inspected will not affect the total fixed inspection

b. There is an inverse relationship between the number of tents inspected and the

c. The inspector’s salary is an indirect cost. Since it is not related to the number of

units inspected, it cannot be traced to any particular unit.

d. First determine the allocation rate:

Cost

Base

Computation

Allocation Rate

Inspection

No. Tents

$60,000 ÷ 20,000

$3 per tent

Month

Allocation

Rate

x

Weight

of Base

=

Amount

Allocated

January

$3

x

1,600

=

$4,800

February

$3

x

1,200

=

3,600

Problem 12-18

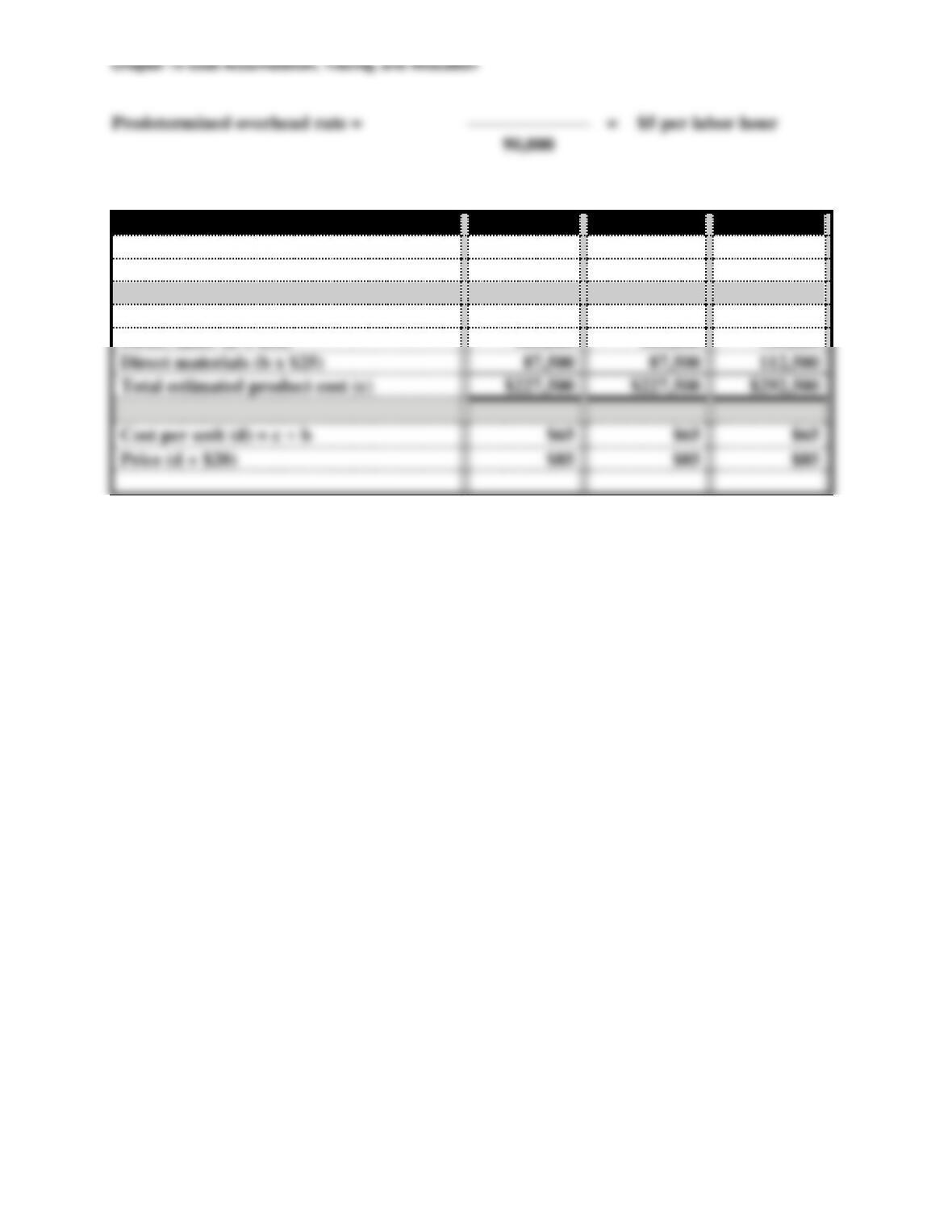

a. The items used to compute the predetermined overhead rate are:

Total Expected Overhead Costs = ($30,000 x 12) + $90,000 = $450,000

The rate is computed as follows:

Total expected overhead costs

––––––––––––––––––––––––––––––––

=

Predetermined overhead rate

Total expected labor hours

12-6

Predetermined overhead rate =

–––––––––––––

=

$5 per labor hour

90,000

b. c. & d.

January

March

August

Direct labor hours (a)

7,000

7,000

9,000

Units produced (b)

3,500

3,500

4,500

Allocated overhead cost (a x $5)

$ 35,000

$ 35,000

$ 45,000

Direct labor (b x $30)

105,000

105,000

135,000

Direct materials (b x $25)

87,500

87,500

112,500

Total estimated product cost (c)

$227,500

$227,500

$292,500

Cost per unit (d) = c ÷ b

$65

$65

$65

Price (d + $20)

$85

$85

$85

Chapter 12 Cost Accumulation, Tracing, and Allocation

12-7

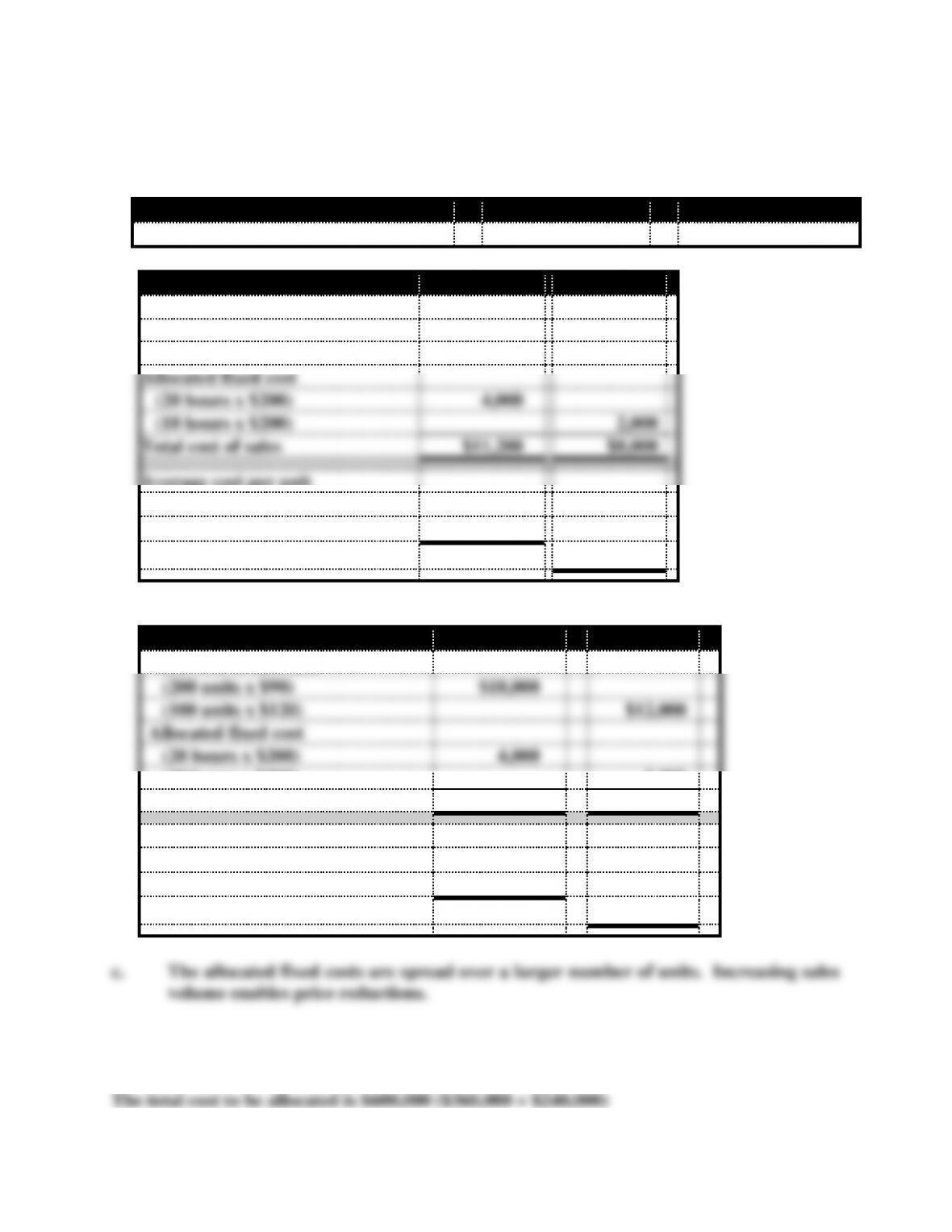

Problem 12-19

a. Determine the predetermined overhead allocation rate:

Total Estimated Overhead Cost

÷

Allocation Base

=

Allocation Rate

$6,000

÷

30 hours

=

$200 per hour

Software Package

EZRecords

ProOffice

Total cost of software

(80 units x $90)

$ 7,200

(50 units x $120)

$6,000

Allocated fixed cost

(20 hours x $200)

4,000

(10 hours x $200)

2,000

Total cost of sales

$11,200

$8,000

Average cost per unit

Total cost ÷ Number of units

($11,200 ÷ 80 units)

$140

($8,000 ÷ 50 units)

$160

b.

Software Package

EZRecords

ProOffice

Total cost of software

(200 units x $90)

$18,000

(100 units x $120)

$12,000

Allocated fixed cost

(20 hours x $200)

4,000

(10 hours x $200)

2,000

Total cost of sales

$22,000

$14,000

Average cost per unit

Total cost ÷ Number of units

($22,000 ÷ 200 units)

$110

($14,000 ÷ 100 units)

$140

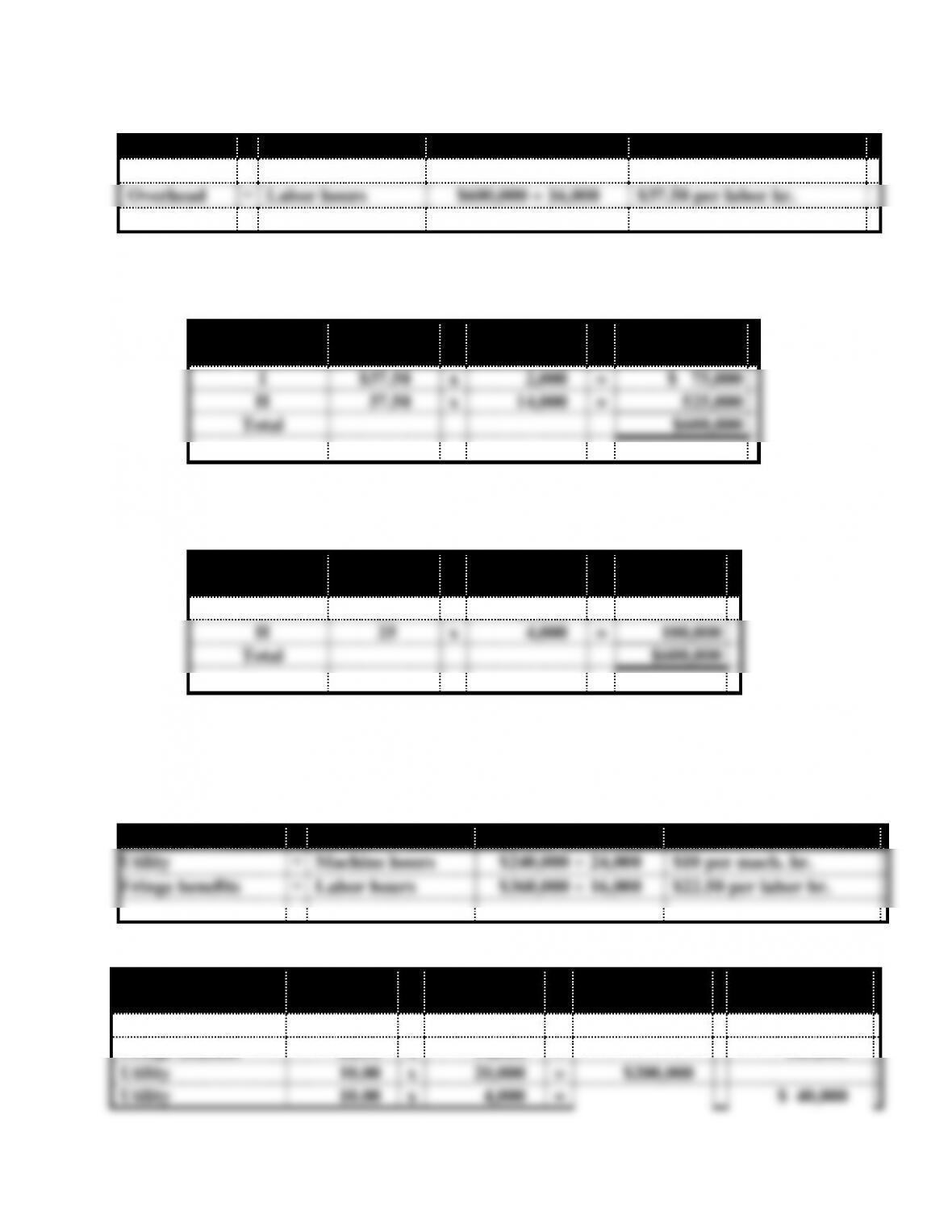

Problem 12-20

Computation of allocation rates for total overhead cost

The total cost to be allocated is $600,000 ($360,000 + $240,000)

Chapter 12 Cost Accumulation, Tracing, and Allocation

12-8

Cost

÷

Base

Computation

Allocation Rate

Overhead

÷

Machine hours

$600,000 ÷ 24,000

$25 per mach. hr.

Overhead

÷

Labor hours

$600,000 ÷ 16,000

$37.50 per labor hr.

a. Since Department I uses fewer labor hours, that base will minimize the amount of

overhead cost allocated to the department.

Department

Allocation

Rate

x

Weight

of Base

=

Allocated

Cost

I

$37.50

x

2,000

=

$ 75,000

II

37.50

x

14,000

=

525,000

Total

$600,000

b. Since Department II uses less machine hours, that base will minimize the amount of

overhead costs allocated to the department.

Department

Allocation

Rate

x

Weight

of Base

=

Allocated

Cost

I

$25

x

20,000

=

$500,000

II

25

x

4,000

=

100,000

Total

$600,000

Problem 12-20 (continued)

c. Since fringe benefit costs are driven by labor hours and utility costs are driven by

machine hours, it would be fair to allocate the individual costs using separate al-

location bases. Allocation rates using separate bases are shown below:

Cost

÷

Base

Computation

Allocation Rate

Utility

÷

Machine hours

$240,000 ÷ 24,000

$10 per mach. hr.

Fringe benefits

÷

Labor hours

$360,000 ÷ 16,000

$22.50 per labor hr.

Allocations for the respective departments:

Costs

Allocation

Rate

x

Weight

of Base

=

Department I

Department II

Fringe benefits

$22.50

x

2,000

=

45,000

Fringe benefits

22.50

x

14,000

=

315,000

Utility

10.00

x

20,000

=

$200,000

Utility

10.00

x

4,000

=

$ 40,000

Chapter 12 Cost Accumulation, Tracing, and Allocation

12-9

Total

$245,000

$355,000

d. The fringe benefits and utility costs have different cost drivers. In other words,

while machine usage is causing the company to incur utility cost, the number of