9-1

Answers to Questions

1. Ratios and trends are useful tools for analyzing financial statements because they give

the analyst a basis for comparing companies of different sizes and characteristics.

2. “Liquidity” is the short-term ability to convert assets to cash or some form useful for

3. Horizontal analysis is a tool for comparing the behavior of items over several periods by

4. This ratio provides information about how rapidly a company is selling its inventory.

Inventory turnover is generally calculated as:

Costs of Goods Sold

5. The current ratio presents the number of dollars of current assets to each dollar of

6. Absolute amounts are often insufficient because companies are of different sizes, thus

7. ROI is a measure of income as a percentage of the total capital employed by the

8. a) Debt to equity ratio: Total Liabilities

—————————————-—–

Total Stockholders’ Equity

9-2

9. Because earnings per share is a combination of “net income” and “average shares

outstanding,” problems in either part affect the outcome. Net income contains many

10. ROI: Net Income

———————

Total Assets

This is the simplest manner of calculating ROI, but many companies and analysts

return on normal operations.

11. Information overload refers to a situation where users of information are overwhelmed

with facts to the point that the desired information is obscured.

12. Price-earnings ratio = Market Price per Share

––––––––––––––––––––––––

Earnings per Share

The PE ratio is a measure of the market price of a share of stock expressed as a

benefits received by stockholders.

13. Some environmental factors that should be considered are (1) the size of the company;

14. Accounting principles are the major determinants of the methods used to account for

assets, liabilities, expenses, and revenues. In analyzing financial statements, the user

9-3

Exercise 9-1

a.

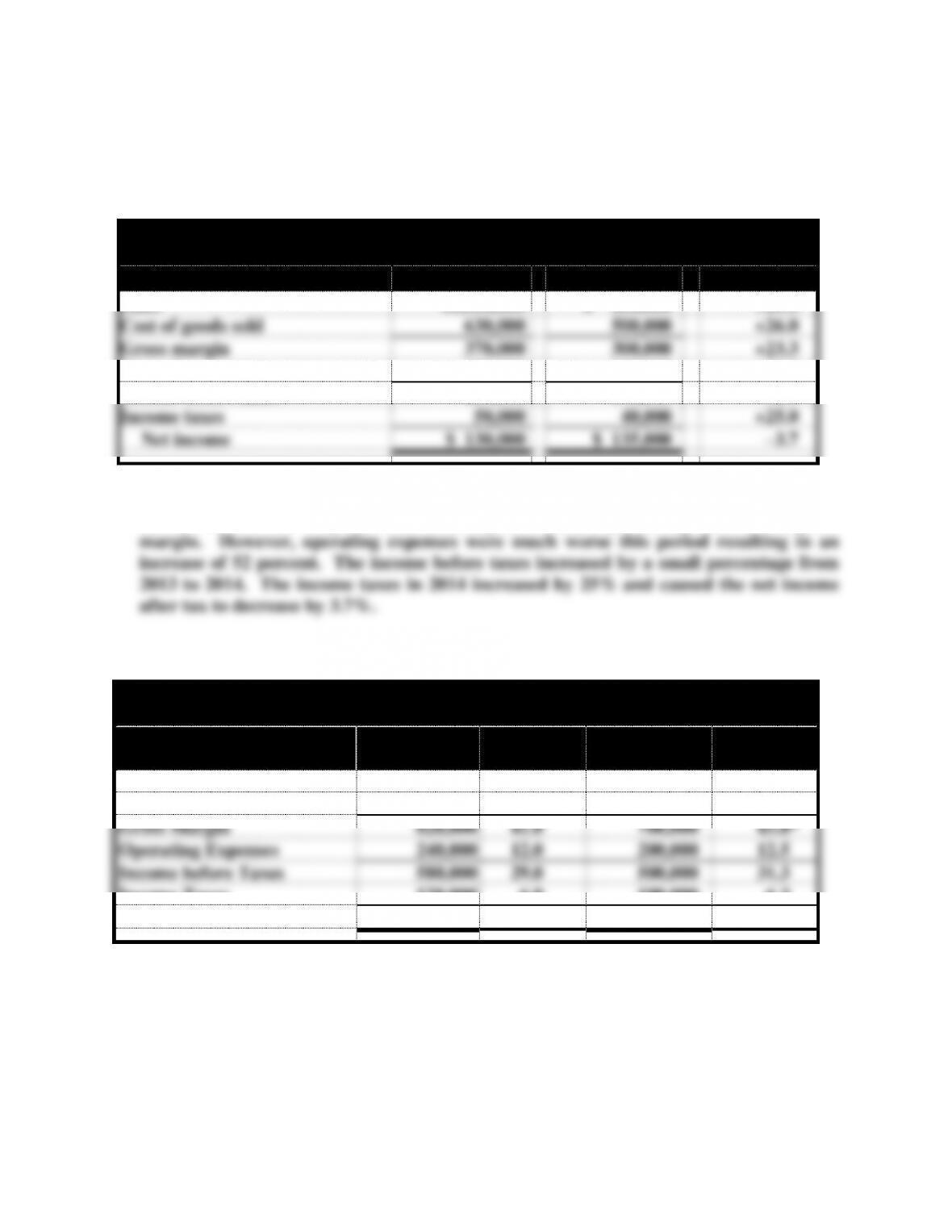

Hall Corporation

Income Statements

2014

2013

% Change

Sales

$1,000,000

$ 800,000

+25.0

Cost of goods sold

630,000

500,000

+26.0

Gross margin

370,000

300,000

+23.3

Operating expenses

190,000

125,000

+52.0

Income before taxes

180,000

175,000

+2.9

Income taxes

50,000

40,000

+25.0

Net income

$ 130,000

$ 135,000

–3.7

b. The sales of Hall increased by 25 percent for the year with a greater percentage

increase in the cost of goods sold, resulting in a smaller percentage increase in gross

Exercise 9-2

Jordan Company

Vertical Analysis of Income Statements

2015

% of

Sales

2014

% of

Sales

Sales

$2,000,000

100.0%

$1,600,000

100.0%

Cost of Goods Sold

1,180,000

59.0

900,000

56.3

Gross Margin

820,000

41.0

700,000

43.8*

Operating Expenses

240,000

12.0

200,000

12.5

Income before Taxes

580,000

29.0

500,000

31.3

Income Taxes

120,000

6.0

100,000

6.3

Net Income

$ 460,000

23.0

$ 400,000

25.0

*With rounding error

Exercise 9-3

a. Horizontal Analysis

9-4

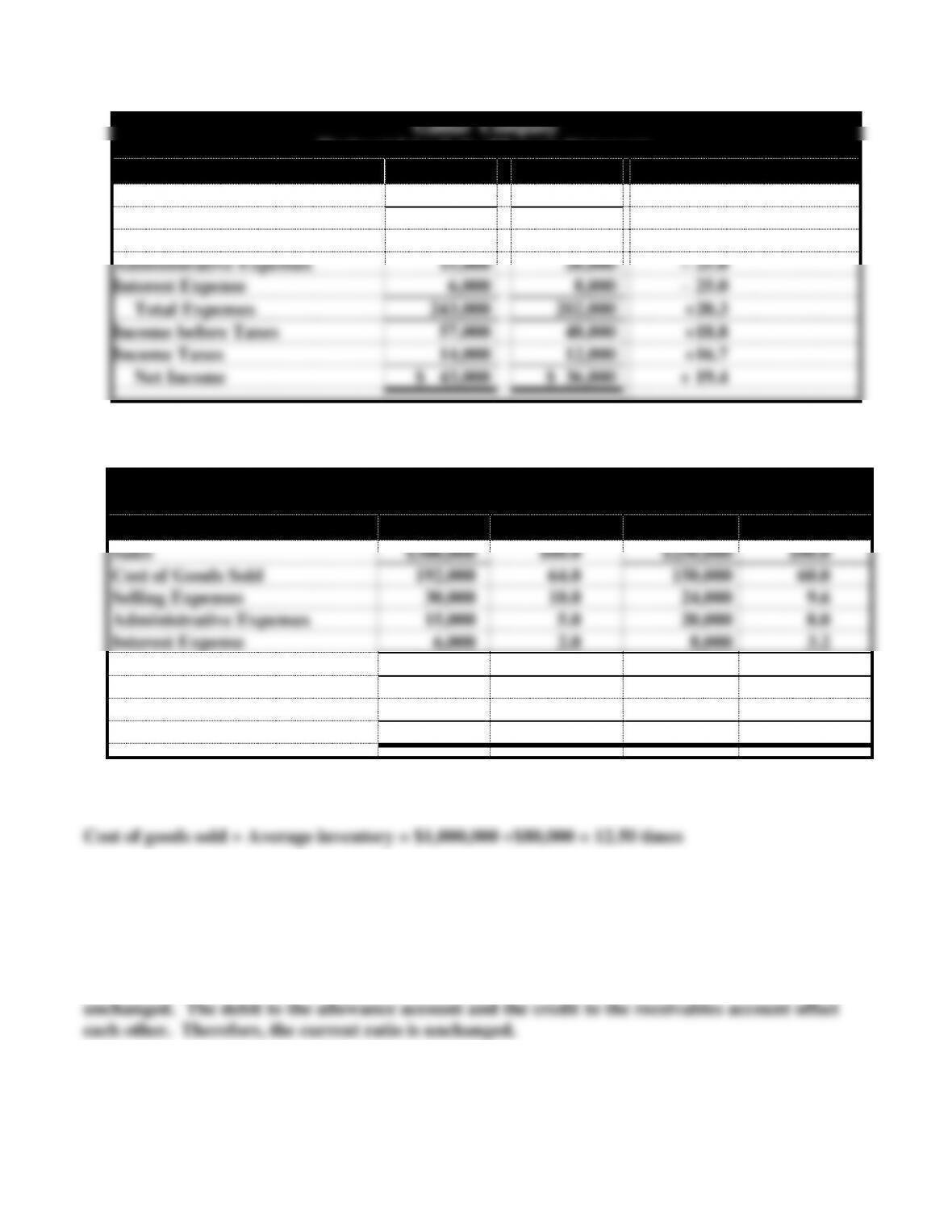

Gaidar Company

Horizontal Analysis of Income Statements

2015

2014

% Change over 2014

Sales

$300,000

$250,000

+20.0

Cost of Goods Sold

192,000

150,000

+28.0

Selling Expenses

30,000

24,000

+25.0

Administrative Expenses

15,000

20,000

– 25.0

Interest Expense

6,000

8,000

– 25.0

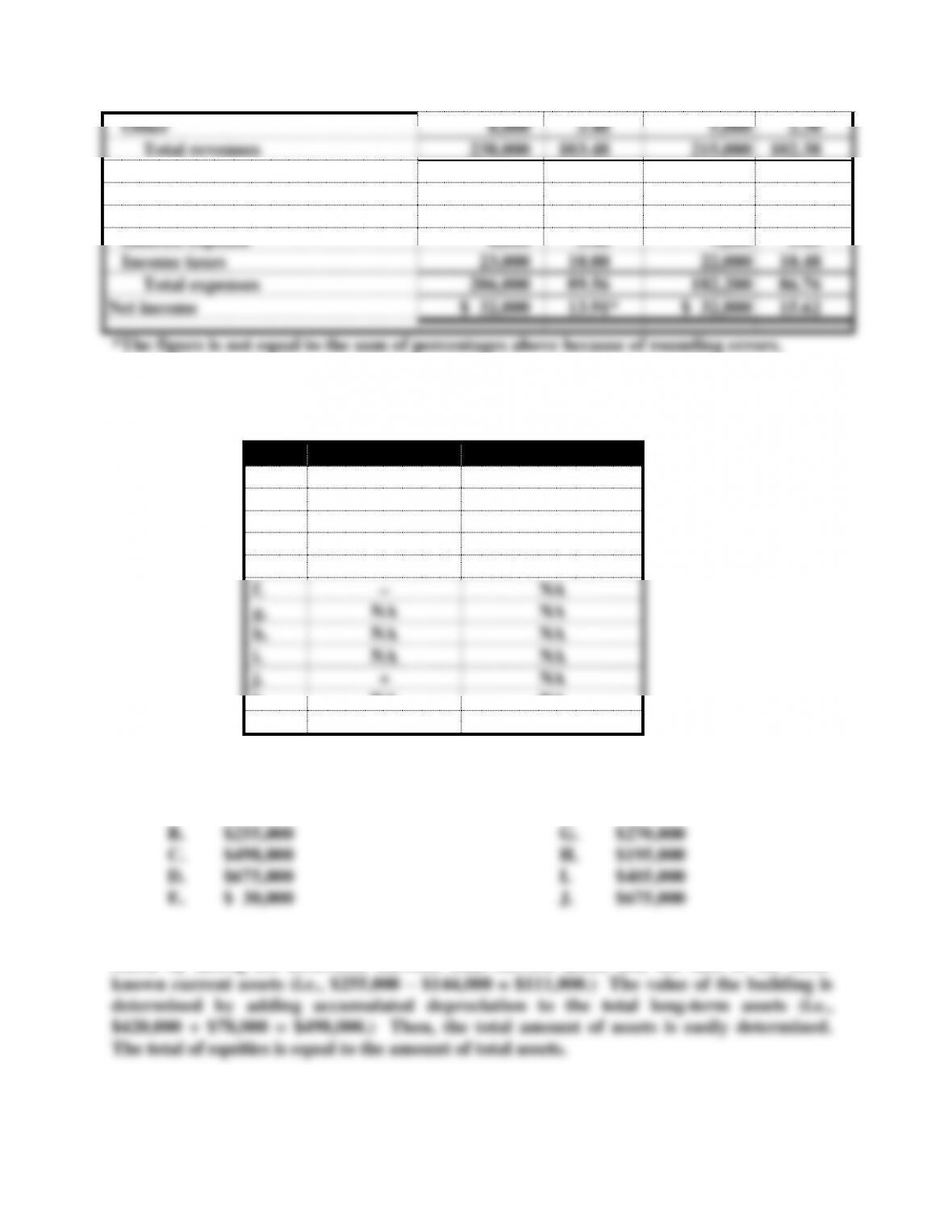

Total Expenses

243,000

202,000

+20.3

Income before Taxes

57,000

48,000

+18.8

Income Taxes

14,000

12,000

+16.7

Net Income

$ 43,000

$ 36,000

+ 19.4

b. Vertical Analysis

Gaidar Company

Vertical Analysis of Income Statements

2015

% of Sales

2014

% of Sales

Sales

$300,000

100.0

$250,000

100.0

Cost of Goods Sold

192,000

64.0

150,000

60.0

Selling Expenses

30,000

10.0

24,000

9.6

Administrative Expenses

15,000

5.0

20,000

8.0

Interest Expense

6,000

2.0

8,000

3.2

Total Expenses

243,000

81.0

202,000

80.8

Income before Taxes

57,000

19.0

48,000

19.2

Income Taxes

14,000

4.7

12,000

4.8

Net Income

$ 43,000

14.3

$ 36,000

14.4

Exercise 9-4

Exercise 9-5

When an account is written off, the net realizable value of accounts receivable remains

Exercise 9-6

a. Working capital before the transaction:

Current assets – Current liabilities

= $800,000 – $400,000 = $400,000

b. Current ratio before the transaction:

Current assets Current liabilities = $800,000 $400,000 = 2:1

Exercise 9-7

a. Working capital before the transaction:

$800,000 – $400,000 = $400,000

b. Current ratio before the transaction: $800,000 $400,000 = 2:1

Exercise 9-8

Working capital = Current assets – Current liabilities

= $300,000 – $200,000 = $100,000

Debt to assets ratio = Total liabilities ÷ Total assets

= $800,000 ÷ $1,250,000 = 64.0%

9-6

Exercise 9-9

a. Current assets = $432,000 – $294,000 = $138,000

$92,000 – $25,000 = $67,000.

b. Solved by simultaneous equations based on known information.

Liabilities: L Stockholders’ Equity: SE Common Stock: CS

L + SE = $432,000

c. Inventory: I Sales: S Cost of goods sold: COGS

Gross margin rate: GMR Gross margin: GM

I = COGS ÷ 10.5 = $735,000 ÷ 10.5 = $70,000

Exercise 9-10

Income before interest and taxes:

$42,000 + $12,000 + $6,000 = $60,000.

Exercise 9-11

a. Net credit sales Average net receivables =

$2,000,000 $457,000 = 4.38 Times

9-7

Exercise 9-12

a. Earnings per share:

= ($3,890,000 – $90,000) ÷ 400,000 = $9.50

b. Book Value per Share of common stock:

= ($20,000,000 – $1,000,000) ÷ 400,000 = $47.50

c. Price-Earnings ratio:

Common stock price ÷ Earnings per share

= $52.00 ÷ $9.50 = 5.47 times earnings

Exercise 9-13

a. Current ratio: $77,000 ÷ $15,000 = 5.13:1

b. Earnings per share: $20,000 ÷ 880 = $22.73 per share

Exercise 9-14

1. c 7. d

Exercise 9-15

Current

Ratio

Working

Capital

Stockholders’

Equity

Book

Value

Retained

Earnings

a.

NC

NC

NC

NC

NC

b.

NC

NC

NC

NC

NC

c.

+

+

NC

NC

NC

d.

–

NC

NC

NC

NC

e.

–

–

–

–

–

f.

+

+

+*

+

+

9-8

g.

NC

NC

NC

–

–

h.

+

NC

NC

NC

NC

i.

+

+

–**

–

–

+: Increase NC: No change

–: Decrease X: Depends on situation

* The eventual effect will be income on the sale which will increase retained

earnings, thus stockholders’ equity.

** The proceeds will increase cash; the loss will reduce earnings. Total assets will

decrease.

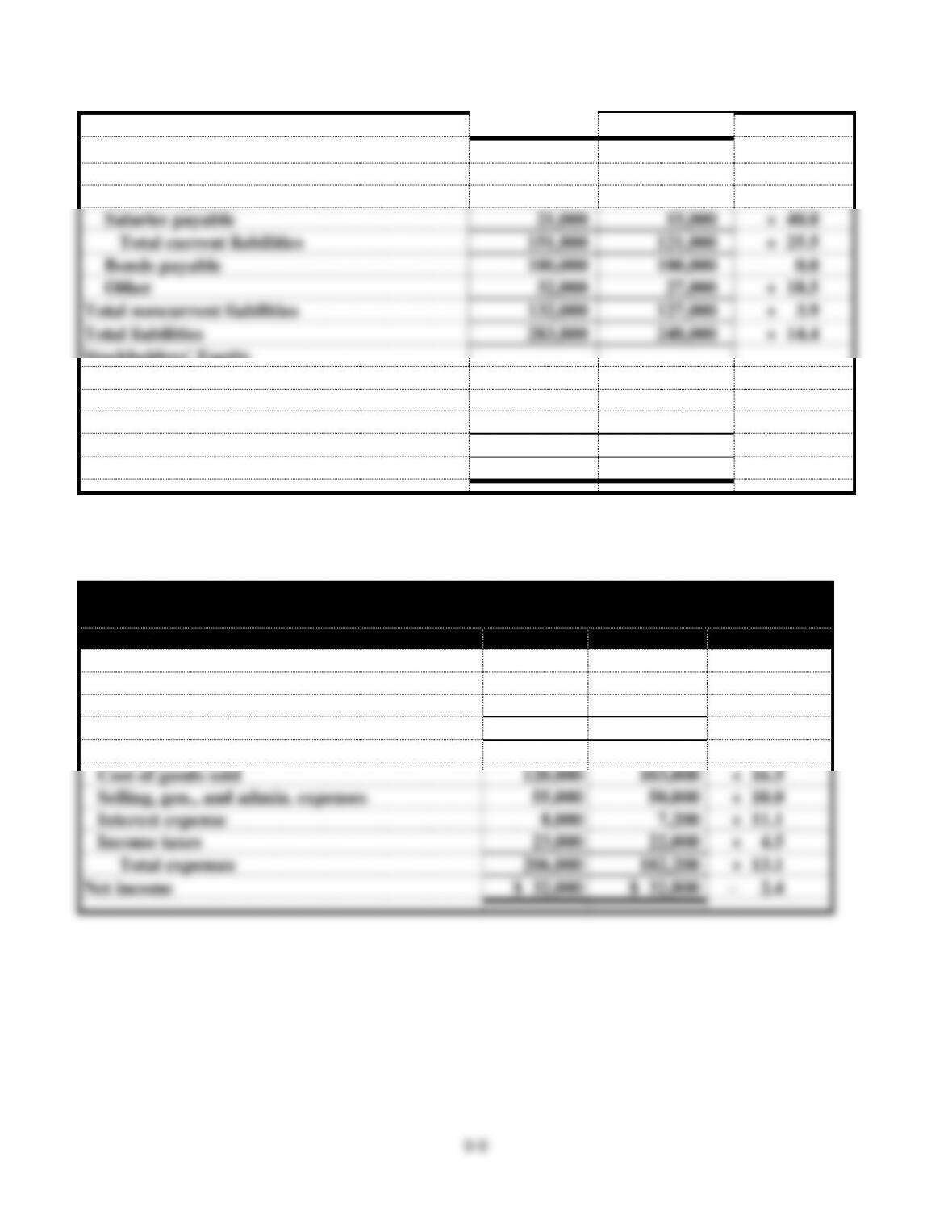

Problem 9-16

Safin Company

Income Statements

2015

2014

Sales

$480,000

$400,000

Cost of Goods Sold

292,800

256,000

Gross Margin

187,200

144,000

Selling and Administrative Expenses

127,200

82,000

Interest Expense

12,000

8,000

Total Expenses

139,200

90,000

Income before Taxes

48,000

54,000

Income Taxes

26,400

28,000

Net Income

$ 21,600

$ 26,000

Problem 9-17

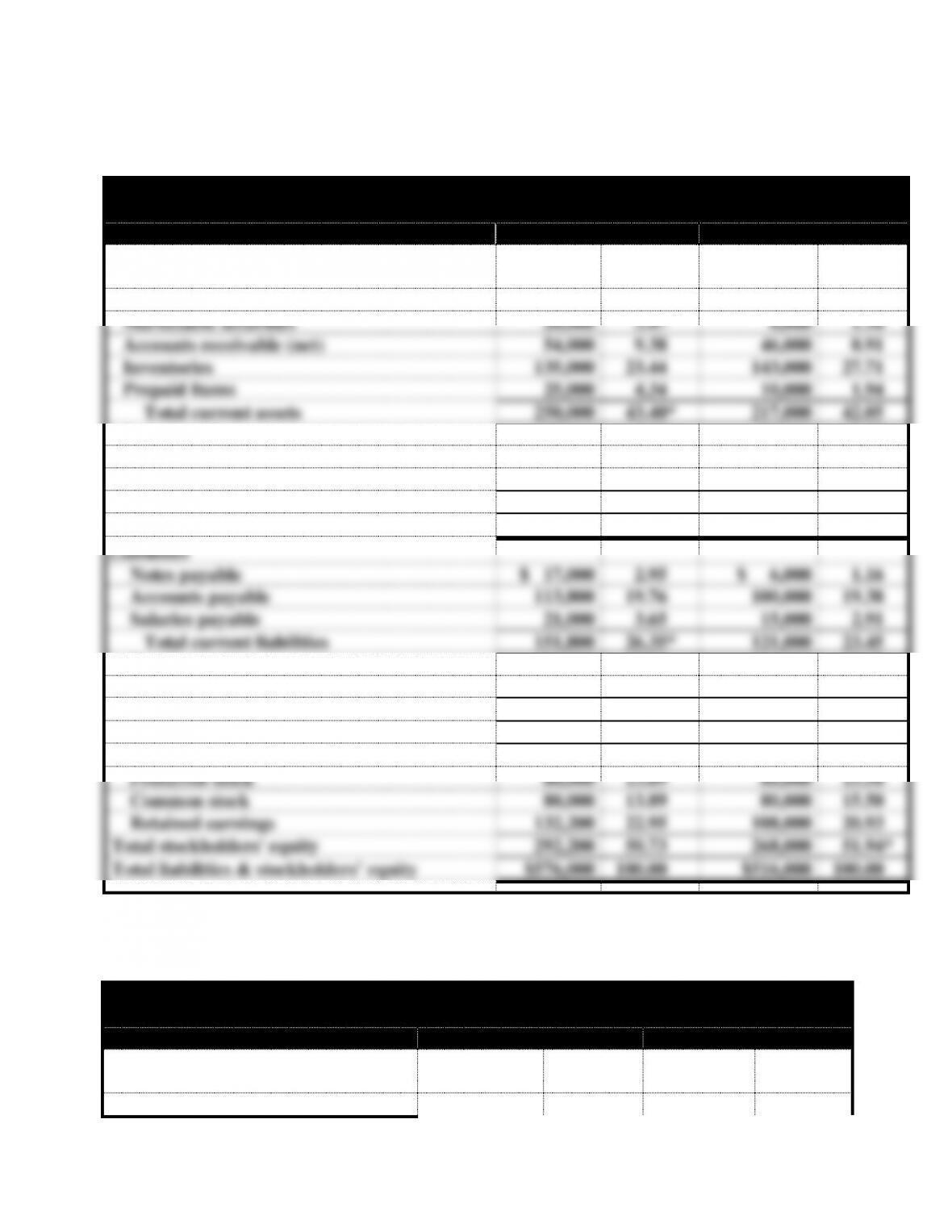

Revnik Company

Horizontal Analysis of Balance Sheets

2015

2014

% Change

Assets

Cash

$ 16,000

$ 12,000

+ 33.3%

Marketable securities

20,000

6,000

+233.3

Accounts receivable (net)

54,000

46,000

+ 17.4

Inventories

135,000

143,000

– 5.6

Prepaid items

25,000

10,000

+150.0

Total current assets

250,000

217,000

+ 15.2

Investments

27,000

20,000

+ 35.0

Plant (net)

270,000

255,000

+ 5.9

Land

29,000

24,000

+ 20.8

Total long-term assets

326,000

299,000

+ 9.0

Total assets

$576,000

$516,000

+ 11.6

Liabilities

Notes payable

$ 17,000

$ 6,000

+183.3

Accounts payable

113,800

100,000

+ 13.8

Salaries payable

21,000

15,000

+ 40.0

Total current liabilities

151,800

121,000

+ 25.5

Bonds payable

100,000

100,000

0.0

Other

32,000

27,000

+ 18.5

Total noncurrent liabilities

132,000

127,000

+ 3.9

Total liabilities

283,800

248,000

+ 14.4

Stockholders’ Equity

Preferred stock

80,000

80,000

0.0

Common stock

80,000

80,000

0.0

Retained earnings

132,200

108,000

+ 22.4

Total stockholders’ equity

292,200

268,000

+ 9.0

Total liabilities & stockholders’ equity

$576,000

$516,000

+ 11.6

Problem 9-17 (continued)

Revnik Company

Horizontal Analysis of Income Statements

2015

2014

% Change

Revenues

Sales (net)

$230,000

$210,000

+ 9.5%

Other

8,000

5,000

+ 60.0

Total revenues

238,000

215,000

+ 10.7

Expenses

Cost of goods sold

120,000

103,000

+ 16.5

Selling, gen., and admin. expenses

55,000

50,000

+ 10.0

Interest expense

8,000

7,200

+ 11.1

Income taxes

23,000

22,000

+ 4.5

Total expenses

206,000

182,200

+ 13.1

Net income

$ 32,000

$ 32,800

– 2.4

9-10

Problem 9-18

Revnik Company

Vertical Analysis of Balance Sheets

2015

2014

Assets

Amount

% of Total

Amount

% of

Total

Cash

$ 16,000

2.78%

$ 12,000

2.33%

Marketable securities

20,000

3.47

6,000

1.16

Accounts receivable (net)

54,000

9.38

46,000

8.91

Inventories

135,000

23.44

143,000

27.71

Prepaid Items

25,000

4.34

10,000

1.94

Total current assets

250,000

43.40*

217,000

42.05

Investments

27,000

4.69

20,000

3.88

Plant (net)

270,000

46.88

255,000

49.42

Land

29,000

5.03

24,000

4.65

Total Long-term assets

326,000

56.60

299,000

57.95

Total Assets

$576,000

100.00

$516,000

100.00

Liabilities

Notes payable

$ 17,000

2.95

$ 6,000

1.16

Accounts payable

113,800

19.76

100,000

19.38

Salaries payable

21,000

3.65

15,000

2.91

Total current liabilities

151,800

26.35*

121,000

23.45

Bonds payable

100,000

17.36

100,000

19.38

Other

32,000

5.56

27,000

5.23

Total noncurrent liabilities

132,000

22.92

127,000

24.61

Total liabilities

283,800

49.27

248,000

48.06

Stockholders’ Equity

Preferred stock

80,000

13.89

80,000

15.50

Common stock

80,000

13.89

80,000

15.50

Retained earnings

132,200

22.95

108,000

20.93

Total stockholders’ equity

292,200

50.73

268,000

51.94*

Total liabilities & stockholders’ equity

$576,000

100.00

$516,000

100.00

*The figure is not equal to the sum of percentages above because of rounding errors.

Problem 9-18 (continued)

Revnik Company

Vertical Analysis of Income Statements

2015

2014

Revenues

Amount

% of Total

Amount

% of Total

Sales (net)

$230,000

100.00%

$210,000

100.00%

9-11

Other

8,000

3.48

5,000

2.38

Total revenues

238,000

103.48

215,000

102.38

Expenses

Cost of goods sold

120,000

52.17

103,000

49.05

Selling, gen., and admin. exp.

55,000

23.91

50,000

23.81

Interest expense

8,000

3.48

7,200

3.43

Income taxes

23,000

10.00

22,000

10.48

Total expenses

206,000

89.56

182,200

86.76

Net income

$ 32,000

13.91*

$ 32,800

15.62

*The figure is not equal to the sum of percentages above because of rounding errors.

Problem 9-19

Current Ratio

Working Capital

a.

–

–

b.

NA

NA

c.

+

+

d.

+

+

e.

–

–

f.

–

NA

g.

NA

NA

h.

NA

NA

i.

NA

NA

j.

+

NA

k.

NA

NA

l.

NA

NA

Problem 9-20

A. $111,000 F. $195,000

If working capital is $180,000, current assets must be $255,000. From this, inventory is

found by taking the difference between total current assets and the sum of the other