General Comments for Chapter 3

Accounting for Merchandising Businesses

Chapter 3 introduces accounting for inventory transactions using the perpetual method. In

today’s high-technology environment, the perpetual system has become the predominant method

of accounting for inventories. Because the periodic method is still used by some companies, it is

included in the chapter appendix, though in less depth.

With the perpetual method, purchases and related transactions (purchase returns and

allowances, purchase discounts, and transportation-in) are recorded in the inventory account.

Likewise, sales returns and allowances and sales discounts are recorded directly in the Sales

account. The balance in the Sales account is therefore the amount of net sales, which is the first

item reported on the income statement. This presentation is consistent with the way sales are

reported in real-world financial statements.

The text explains only the net method of accounting for cash discounts. The net method is

easier to understand and theoretically superior. Indeed, GAAP requires “purchase discounts lost”

to be reported as interest in the financial statements if the amount is material. When the gross

method is used, “purchase discounts lost” is misclassified as a product cost that is first placed in

the inventory account and later recognized as cost of goods sold expense.

This chapter introduces the multistep income statement; earlier chapters used the single step

income statement. Within this context, direct your students’ attention toward the reporting of

interest. As you are aware, interest is classified as a nonoperating item on a multistep income

statement and as an operating activities item on the statement of cash flows. This inconsistency

provides an opportunity to discuss how accounting standards are developed. If you have not yet

talked about the role of the Financial Accounting Standards Board, this is a good time to do so.

Students should learn that accounting standards evolve through a participative process influenced

by changes in society. While we may strive for perfection, we are not likely to attain it. Good

accounting requires the ability to adapt and to exercise judgment. It is not a discipline of hard

facts and natural laws, but a living social science.

Detailed Outline of a Lesson Plan for Chapter 3

I. Define merchandise inventory as goods purchased for resale to customers, then

distinguish product costs from selling and administrative costs. Explain that product

costs are first accumulated in inventory accounts and then expensed when the products

are sold, regardless of when the costs were initially incurred. In contrast, selling and

administrative costs are usually, though not always, expensed in the period in which they

are incurred. The most common exception is the cost of long-term assets. While the cost

of obtaining a long-term asset may be incurred in a single accounting period, expense

recognition occurs over multiple periods. Because selling and administrative costs are

usually matched with the period in which they are incurred, they are frequently called

period costs.

II. Sketch adjacent income statements on the chalkboard to contrast service businesses

and merchandising businesses. Explain that merchandising companies have the same

types of expenses as service companies (salaries, utilities, advertising, depreciation), but

unlike service companies, merchandising companies also have cost of goods sold.

Introduce the multistep income statement by showing the subtotal for gross margin (net

sales minus cost of goods sold) before subtracting period expenses. Initially, avoid more

advanced topics such as accounting for returns, allowances, discounts, and freight.

Introduce these topics after the students understand the basic events illustrated in

Demonstration Problem 3-1.

III. Work Demonstration Problem 3-1. We suggest you write each transaction on the

board one step at a time. Allow students time to record each event in the financial

statements model. Show them the answer before moving on to the next transaction. The

problem, solution, and work papers are available if you desire to duplicate them for your

students.

The requirements call only for preparing an income statement and a balance sheet.

The statement of changes in stockholders’ equity and the statement of cash flows are not

required. Instead of requiring a full set of formal statements each time you or students

work a problem, require only the relevant ones. In this problem the income statement is

required because it appears in a new format (multistep). Likewise, students need to see

the reporting of inventory on the balance sheet. It is meaningful for students to prepare

these two statements in addition to showing financial statement effects in the statements

model.

Use the statements model to demonstrate the cash flow effects. Emphasize that

although the company paid $4,500 cash for inventory, only $3,500 of that cost was

charged to cost of goods sold. The remaining amount of product cost ($1,000) is reported

as inventory on the balance sheet. This illustration demonstrates that product costs are

expensed in the period in which inventory is sold regardless of when cash for it is paid.

IV. Demonstration Problem 3-2 provides a platform for explaining such advanced

topics as returns, allowances, cash discounts, and freight costs. Work the problem in

steps, explaining each topic as it arises in the problem. Event No. 2 introduces cash

discount terms. Explain the meaning of 2/10, n/30. Event No. 3 involves freight costs.

At this point you should explain FOB shipping point and FOB destination. The event

invites you to introduce the general topic of freight costs, going beyond the specific

freight transaction described in the problem. Draw pictures! Put rectangles on the board

representing the merchandising company, a supplier, and a customer. Draw trucks

traveling between the companies. Explain to your students that we are viewing all

inventory transactions from the merchandising company’s point of view. Help students

see that transactions between the merchandising company and its suppliers are purchases,

though from the supplier’s point of view they are sales. In this way your lecture flows

from the problem. Use Event No. 4 to introduce purchase returns and allowances. Using

this approach, you will explain sales and purchase returns and allowances, cash

discounts, and freight costs by the time you have finished Demonstration Problem 3-2.

V. Explain that failure to pay for purchases within the discount period results in

interest costs. Refer to the payment LDS made in Event No. 5 of Demonstration

Problem 3-2. If LDS had paid after the discount period expired, it would have owed the

supplier $50,000 (list price of $54,000 purchase – list price of $4,000 purchase return),

not $49,000. The $1,000 difference represents interest expense and the payment would

have been recorded as follows:

2014

Cash

+

Acct.

Rec.

+

Inv.

=

Acct.

Pay.

+

Com.

Stock

+

Ret. Ear.

(5) Pay Acct. Payable

(50,000)

(49,000)

(1,000)

VI. If you plan to include the appendix material, use Demonstration Problem 3-3 to

introduce the periodic inventory method. This problem uses the same transactions as

Demonstration Problem 3-2, illustrating that either of two different accounting methods

can be used to record the same data. Prepare a schedule of cost of goods sold. Compare

the amount of cost of goods sold in the schedule with the amount of cost of goods sold

determined using the perpetual method. Ask your students to prepare a set of financial

statements using the periodic method. Chances are few of them will realize that the

statements resulting from the periodic method are identical to the statements resulting

from the perpetual method. We usually let them finish the income statement before

stopping them. Preparing at least one comparative statement demonstrates that the two

methods are alternative approaches to the same end.

VII. Discuss accounting for lost, damaged, or stolen merchandise. Illustrate by asking

your students to return to Demonstration Problem 3-2. Suppose a physical count

establishes that only $9,000 of inventory is actually on hand at the end of the accounting

period. Recall that the balance in the inventory account at the end of the period was

$10,800. Have students explain how the $1,800 loss would affect the financial

statements by recording the event in a statements model like shown below. The

“Balances” row displays the amounts in various categories after recording all of the

Demonstration Problem 3-2 transactions. Expenses are shown as one single total

($39,200 + $1,200 + $9,600 = $50,000). These balances agree with the financial

statements solution for Demonstration Problem 3-2. The row labeled “Inv. Loss”

demonstrates the effects of the inventory loss on the financial statements. The “Totals”

row displays the balances after recognizing the inventory loss.

Assets

=

Claims

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

+

Accts.

Rec.

+

Inv.

=

Com.

Stk.

+

Ret. Ear.

Balances

48,700

+

13,860

+

10,800

=

60,000

+

13,360

63,360

–

50,000

=

13,360

48,700 NC

Inv. Loss

-0-

+

-0-

+

(1,800)

=

-0-

+

(1,800)

-0-

–

1,800

=

(1,800)

-0-

Totals

48,700

+

13,860

+

9,000

=

60,000

+

11,560

63,360

–

51,800

=

11,560

48,700 NC

VIII. Time considerations and homework assignments. Allot two to three hours of class

time for Chapter 3. Exercise 3-2 contrasts merchandising companies with service

companies; Exercises 3-3 through 3-5 require students to demonstrate the effect of

inventory transactions on the financial statements. Exercise 3-15 involves preparation of

single step and multistep income statements. Exercise 3-12 shows the interest costs of

failure to pay for purchases within the discount period. Problems 3-25 and 3-26 provide

a comprehensive follow-up of Demonstration Problem 3-2. Problem 3-28 focuses on

preparing financial statements using the periodic method.

IX. Enrichment. By now you are familiar with the types of cases included at the end of each

chapter. You probably have a preference consistent with your personal objectives. We

leave to your judgment the most appropriate form of enrichment. You may choose to use

the study guide, computer tutorials, or other supplements that accompany the text.

Demonstration Problems for Chapter 3

Demonstration Problem 3-1: Inventory Purchase/Sale, Perpetual

Method

The following events pertain to Jefferson Hardware Store. Jefferson uses the perpetual inventory

method.

1. Jefferson Hardware was started on January 1, 2014 when it acquired $5,000 cash by issuing

common stock.

2. The store paid $4,500 cash to purchase inventory.

3. Jefferson sold for $6,000 cash inventory that cost $3,500.

4. During 2014, the store paid $2,000 cash for operating expenses.

Required

Record the events in a financial statements model. Then prepare an income statement and a

balance sheet.

Demonstration Problem 3-2: Perpetual Inventory Transactions

Lisa’s Dress Shop (LDS) experienced the following events in 2014, its first year of operations.

The dress shop uses the perpetual inventory method.

1. LDS was started when it issued common stock for $60,000 cash.

2. LDS purchased on account inventory with a list price of $54,000. Payment terms were 2/10,

n/30. LDS records inventory transactions net of discounts.

3. The freight terms for the merchandise delivered in Event No. 2 were FOB shipping point.

LDS paid the freight cost of $1,000 in cash.

4. An inspection revealed that merchandise with a list price of $4,000 purchased in Event No.

2 was defective. LDS returned this merchandise to the supplier for credit.

5. LDS paid within the discount period for the inventory purchased in Event No. 2.

6. LDS sold inventory on account. LDS offers customers payment terms of 1/15, n/30. The list

price for the sale was $68,000. The net cost of the inventory sold was $42,140.

7. Customers returned some goods LDS had sold in Event No. 6. The goods had been sold for

a net price of $3,960 and had a net cost of $2,940.

8. LDS paid in cash freight cost of $1,200 for goods delivered to customers FOB destination.

9. LDS collected cash from customers who paid off accounts receivable with a list price of

$50,000 within the 15-day discount period.

10. LDS paid $9,600 in cash for other operating expenses.

Required

Record the events under an accounting equation, and prepare an income statement, a balance

sheet, and a statement of cash flows.

Demonstration Problem 3-3: Periodic Inventory Transactions

Assume Lisa’s Dress Shop (LDS) uses the periodic rather than the perpetual inventory method.

LDS determined by physical count there was $10,800 of inventory on hand at the end of 2014.

Required

Determine account balances using information in Demonstration Problem 3-2, but assuming use

of the periodic inventory method. Then prepare a schedule of cost of goods sold, an income

statement, a balance sheet, and a statement of cash flows based on the periodic method.

SOLUTIONS TO

DEMONSTRATION PROBLEMS

Demonstration Problem 3-1: Solution

Assets

=

Liab.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

No.

Cash

+

Inven.

=

Liab.

+

C. Stk.

+

Ret. Ear.

Beg. Bal.

-0-

+

-0-

=

-0-

+

-0-

+

-0-

-0-

–

-0-

=

-0-

-0-

1

5,000

+

-0-

=

-0-

+

5,000

+

-0-

-0-

–

-0-

=

-0-

5,000 FA

2

(4,500)

+

4,500

=

-0-

+

-0-

+

-0-

-0-

–

-0-

=

-0-

(4,500) OA

3(a)

6,000

+

-0-

=

-0-

+

-0-

+

6,000

6,000

–

-0-

=

6,000

6,000 OA

3(b)

-0-

+

(3,500)

=

-0-

+

-0-

+

(3,500)

-0-

–

3,500

=

(3,500)

-0-

4

(2,000)

+

-0-

=

-0-

+

-0-

+

(2,000)

-0-

–

2,000

=

(2,000)

(2,000) OA

Totals

4,500

+

1,000

=

-0-

+

5,000

+

500

6,000

–

5,500

=

500

4,500 NC

Jefferson Hardware Store

Financial Statements

Income Statement

For the Year Ended December 31,

2014

Sales

$6,000

Cost of Goods Sold (Product Cost)

(3,500)

Gross Margin

$2,500

Operating Expenses (Period Cost)

(2,000)

Net Income

$ 500

Balance Sheet as of December 31

Assets

Cash

$4,500

Inventory

1,000

Total Assets

$5,500

Stockholders’ Equity

Common Stock

$5,000

Retained Earnings

500

Total Stockholders’ Equity

$5,500

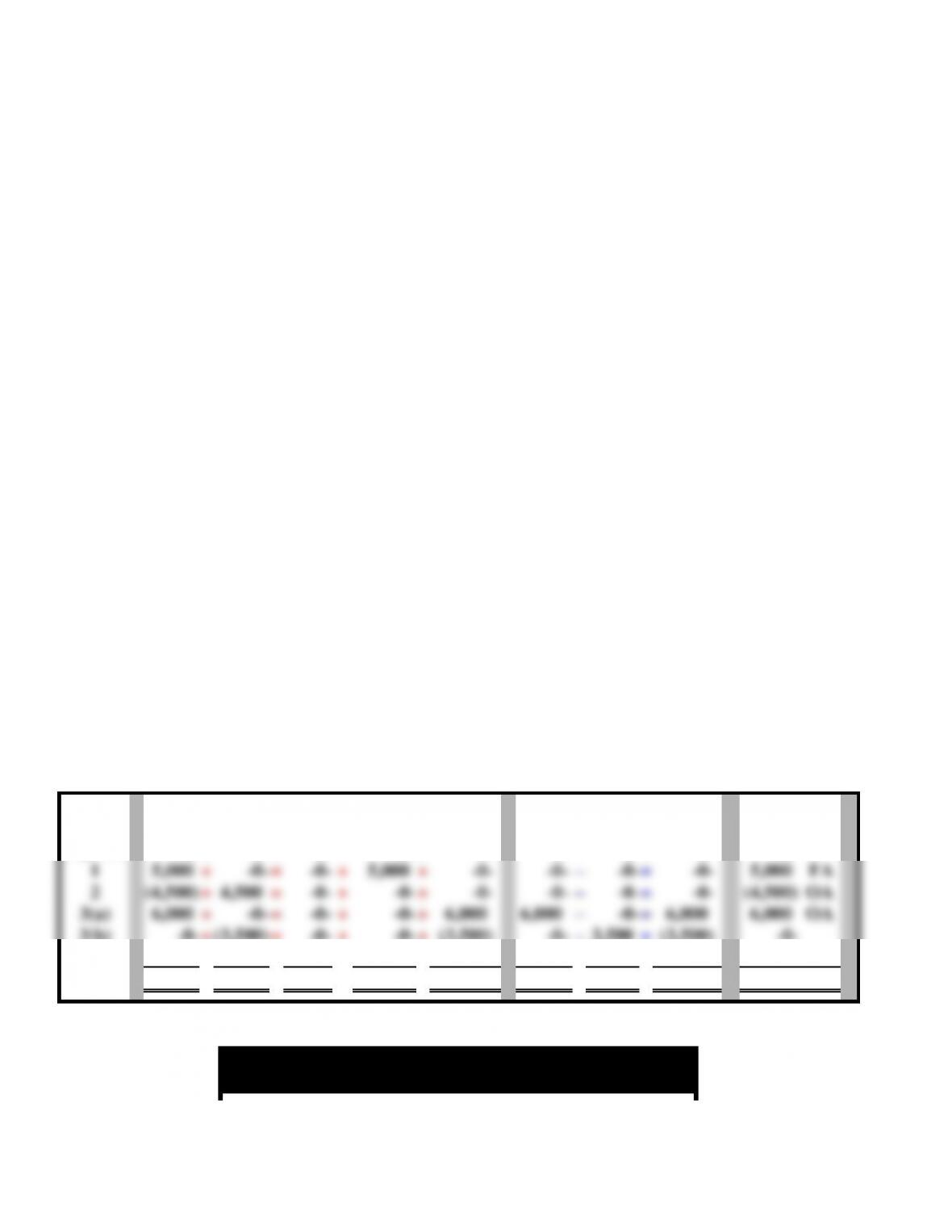

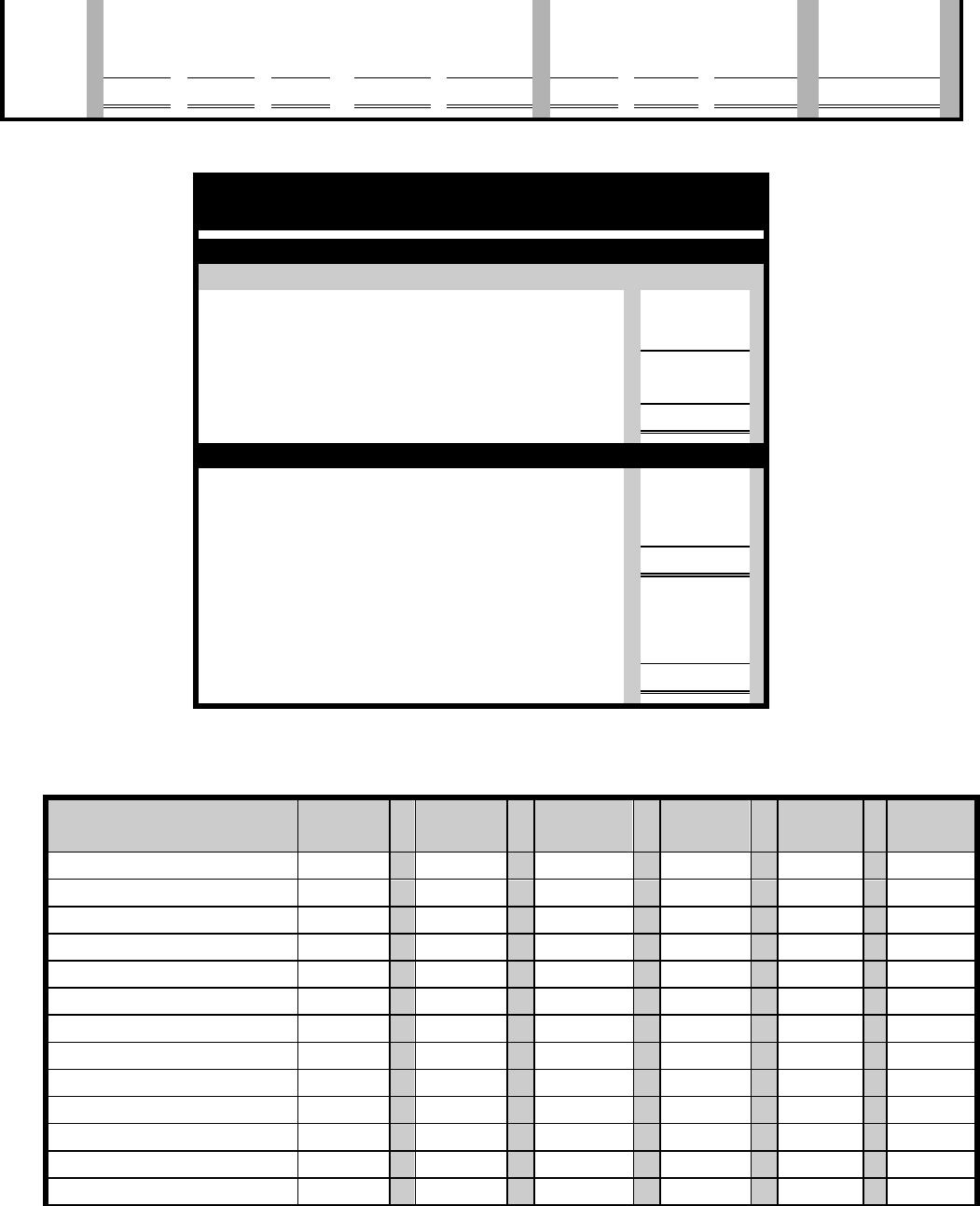

Demonstration Problem 3-2: Solution, Accounting Equation

2014

Cash

+

Acct.

Rec.

+

Inv.

=

Acct.

Pay.

+

Com.

Stock

+

Ret. Ear.

Beginning Balances

$ -0-

$ -0-

$ -0-

$ -0-

$ -0-

$ -0-

(1) Common Stock Issue

60,000

60,000

(2) Inventory Purchase

52,920

52,920

(3) Transportation-in

(1,000)

1,000

(4) Purchase Return

(3,920)

(3,920)

(5) Pay Acct. Payable

(49,000)

(49,000)

(6a) Sale of Inventory

67,320

67,320

(6b) Cost of Goods Sold

(42,140)

(42,140)

(7a) Sales Return

(3,960)

(3,960)

(7b) Cost of Goods Sold

2,940

2,940

(8) Transportation-out

(1,200)

(1,200)

(9) Collect Acct. Rec.

49,500

(49,500)

(10) Other Oper. Exp.

(9,600)

(9,600)

−−−−−

−−−−−

−−−−−

−−−−−

−−−−−

−−−−−

Ending Balances

$48,700

$13,860

$10,800

$ -0-

$60,000

$13,360

════

════

═════

════

═════

═════

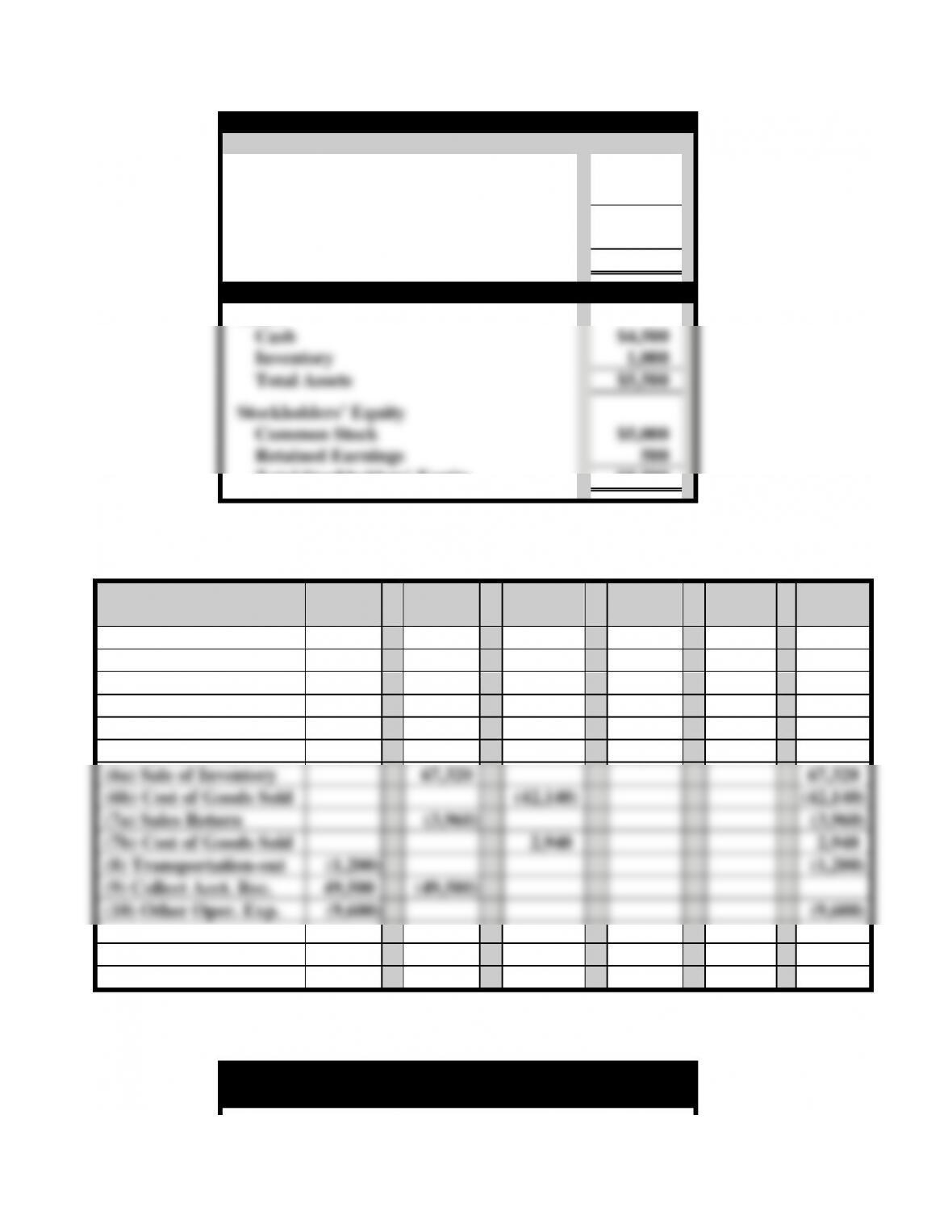

Demonstration Problem 3-2: Solution, Financial Statements

Lisa’s Dress Shop

Financial Statements

Income Statement

For the Year Ended December 31,

2014

Net Sales

$63,360

Cost of Goods Sold (Product Cost)

(39,200)

Gross Margin

$24,160

Transportation-out (Period Cost)

(1,200)

Other Operating Expenses (Period Cost)

(9,600)

Net Income

$13,360

Balance Sheet at December 31

Assets

Cash

$48,700

Accounts Receivable

13,860

Inventory

10,800

Total Assets

$73,360

Stockholders’ Equity

Common Stock

$60,000

Retained Earnings

13,360

Total Stockholders’ Equity

$73,360

Statement of Cash Flows

Net Cash Flow from Operating Activities1

$(11,300)

Net Cash Flow from Investing Activities

-0-

Net Cash Flow from Financing Activities

60,000

Net Change in Cash

$48,700

Beginning Cash Balance

-0-

Ending Cash Balance

$48,700

1Net cash flow from operating activities: $49,500 inflow from revenue less outflows of $1,000

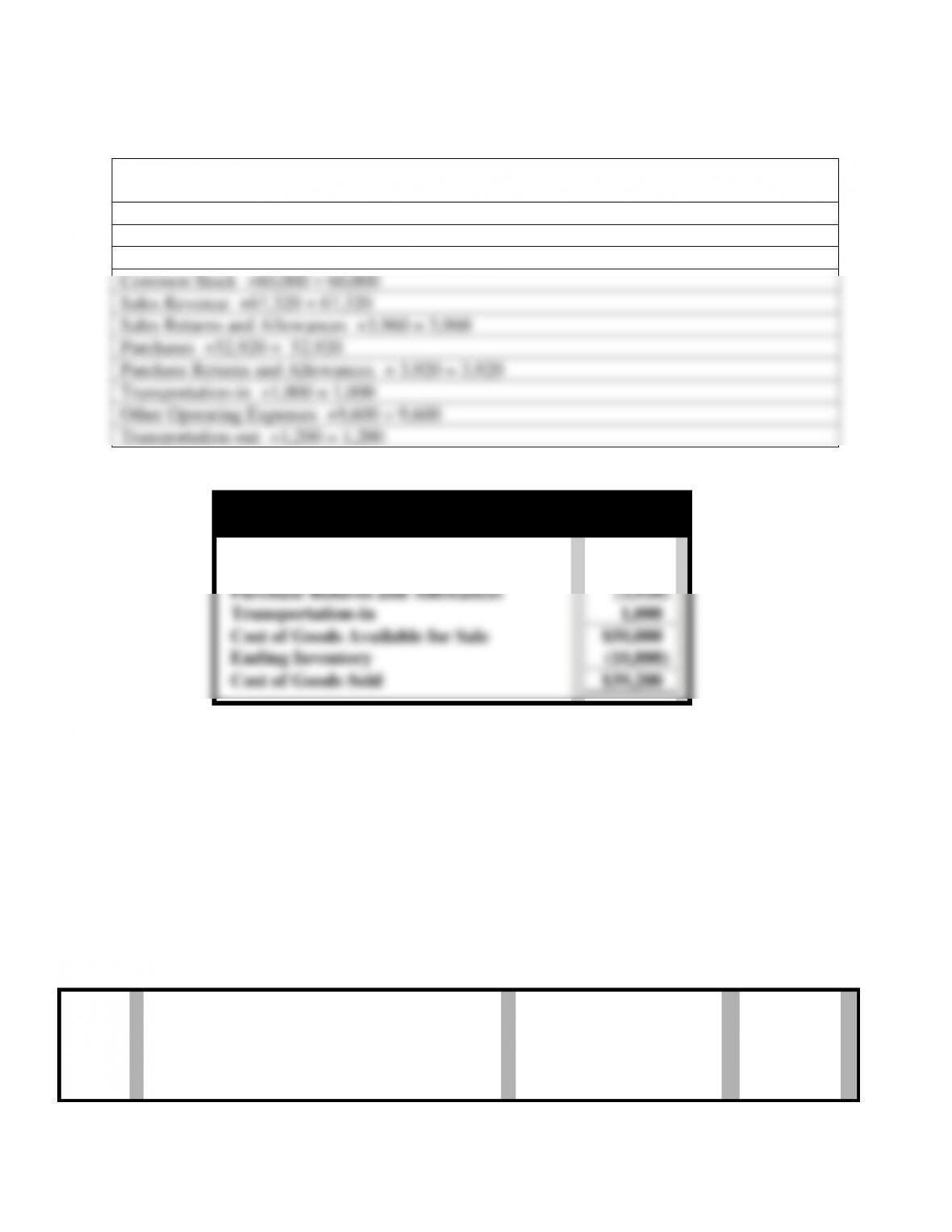

Demonstration Problem 3-3: Solution

Account Balances – Lisa’s Dress Shop – Determine account balances by showing

increases and decreases

Cash +60,000 – 1,000 – 49,000 -1,200 + 49,500 – 9,600 = 48,700

Accounts Receivable +67,320 – 3,960 – 49,500 = 13,860

Accounts Payable +52,920 – 3,920 – 49,000 = 0

Common Stock +60,000 = 60,000

Sales Revenue +67,320 = 67,320

Sales Returns and Allowances +3,960 = 3,960

Purchases +52,920 = 52,920

Purchase Returns and Allowances + 3,920 = 3,920

Transportation-in +1,000 = 1,000

Other Operating Expenses +9,600 = 9,600

Transportation-out +1,200 = 1,200

Lisa’s Dress Shop

Schedule of Cost of Goods Sold

Beginning Inventory

$ -0-

Purchases

52,920

Purchase Returns and Allowances

(3,920)

Transportation-in

1,000

Cost of Goods Available for Sale

$50,000

Ending Inventory

(10,800)

Cost of Goods Sold

$39,200

The financial statements are the same as those prepared for Demonstration Problem 3-2.

The periodic inventory method is an alternative accounting approach that produces the same

end result.

WORK PAPERS FOR

DEMONSTRATION PROBLEMS

Demonstration Problem 3-1: Work Paper

Assets

=

Liab.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

No.

Cash

+

Inven.

=

Liab.

+

C. Stk.

+

Ret. Ear.

Beg. Bal.

-0-

+

-0-

=

-0-

+

-0-

+

-0-

-0-

–

-0-

=

-0-

-0-

1

+

=

+

+

–

=

2

+

=

+

+

–

=

3(a)

+

=

+

+

–

=

3(b)

+

=

+

+

–

=

4

+

=

+

+

–

=

Totals

4,500

+

1,000

=

-0-

+

5,000

+

500

6,000

–

5,500

=

500

4,500 NC

Jefferson Hardware Store

Financial Statements

Income Statement

For the Year Ended December 31,

2014

Sales

Cost of Goods Sold (Product Cost)

Gross Margin

Operating Expenses (Period Cost)

Net Income

$ 500

Balance Sheet as of December 31

Assets

Cash

Inventory

Total Assets

Stockholders’ Equity

Common Stock

$5,000

Retained Earnings

Total Stockholders’ Equity

$5,500

Demonstration Problem 3-2: Work Paper, Accounting Equation

2014

Cash

+

Acct.

Rec.

+

Inv.

=

Acct.

Pay.

+

Com.

Stock

+

Ret. Ear.

Beginning Balances

$ -0-

$ -0-

$ -0-

$ -0-

$ -0-

$ -0-

(1) Common Stock Issue

(2) Inventory Purchase

(3) Transportation-in

(4) Purchase Return

(5) Pay Acct. Payable

(6a) Sale of Inventory

(6b) Cost of Goods Sold

(7a) Sales Return

(7b) Cost of Goods Sold

(8) Transportation-out

(9) Collect Acct. Rec.

(10) Other Oper. Exp.

−−−−−

−−−−−

−−−−−

−−−−−

−−−−−

−−−−−

Ending Balances

$48,700

$13,860

$10,800

$ -0-

$60,000

$13,360

════

════

═════

════

═════

═════

Demonstration Problem 3-2: Work Paper, Financial Statements

Lisa’s Dress Shop

Financial Statements

Income Statement

For the Year Ended December 31,

2014

Net Sales

Cost of Goods Sold (Product Cost)

Gross Margin

$24,160

Transportation-out (Period Cost)

Other Operating Expenses (Period Cost)

Net Income

$13,360

Balance Sheet at December 31

Assets

Cash

Accounts Receivable

Inventory

Total Assets

Stockholders’ Equity

Common Stock

$60,000

Retained Earnings

Total Stockholders’ Equity

$73,360

Statement of Cash Flows

Net Cash Flow from Operating Activities1

Net Cash Flow from Investing Activities

Net Cash Flow from Financing Activities

Net Change in Cash

$48,700

Beginning Cash Balance

Ending Cash Balance

1The net cash flow from operating activities consists of an inflow from revenue less outflows

for transportation-in, payments of accounts payable, transportation-out, and other operating

expenses.

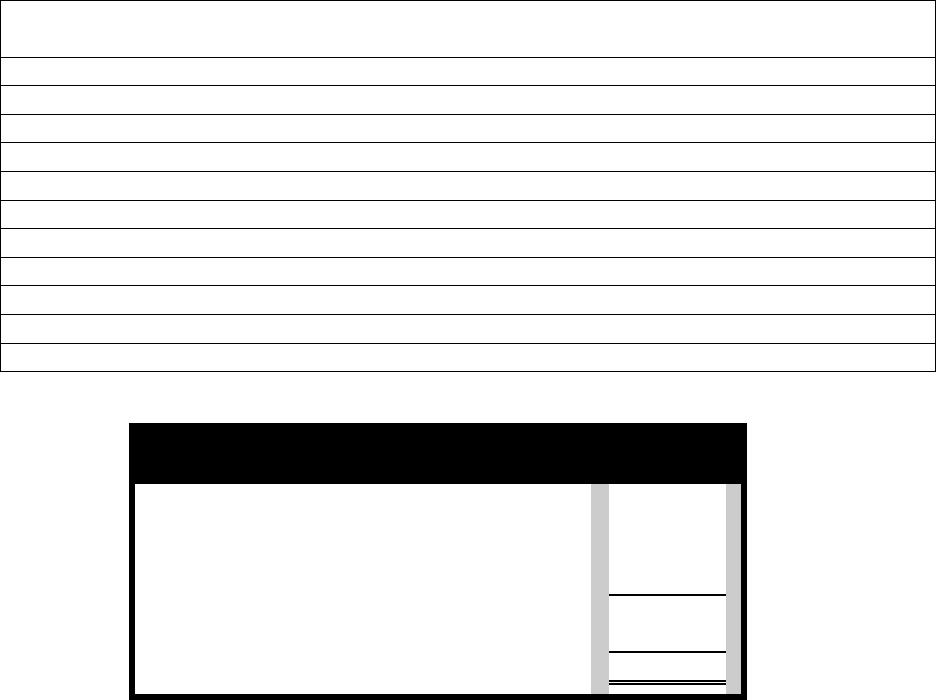

Demonstration Problem 3-3: Work Paper

Account Balances – Lisa’s Dress Shop – Determine account balances by

showing increases and decreases

Cash

Accounts Receivable

Accounts Payable

Common Stock

Sales Revenue

Sales Returns and Allowances

Purchases

Purchase Returns and Allowances

Transportation-in

Other Operating Expenses

Transportation-out

Lisa’s Dress Shop

Schedule of Cost of Goods Sold

Beginning Inventory

$ -0-

Purchases

Purchase Returns and Allowances

Transportation-in

Cost of Goods Available for Sale

Ending Inventory

Cost of Goods Sold

$39,200

The financial statements are the same as those prepared for Demonstration Problem 3-2.

The periodic inventory method is an alternative accounting approach that produces the

same end result as the perpetual inventory method.