Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 11 Cost Behavior, Operating Leverage, and Profitability Analysis

Answer to questions

1. A fixed cost is a cost that in total remains constant as volume of activity changes but

on a per unit basis varies inversely with changes in volume of activity. A variable cost

2. Most business decisions are based on cost information. The behavior of cost in

relation to volume affects total costs and cost per unit. For example, knowing that

3. Operating leverage is the condition whereby a small percentage change in sales

volume can produce a significantly larger percentage change in profitability. It is the

4. Operating leverage is calculated by dividing the contribution margin by net income.

5. The concept of operating leverage is limited in predicting profitability because, in

6. With increasing volume a company would benefit more from a fixed cost structure

because of operating leverage, where each sales dollar represents pure profit once

7. Fixed costs can provide financial rewards with increases in volume because increases

in volume reduce fixed costs per unit, thereby increasing profits. The risk involved

8. Fixed costs can provide financial rewards with increases in volume since increases in

volume do not cause corresponding increases in fixed costs. This kind of cost behavior

in costs, which can eventually result in losses (increases in cost per unit).

9. The definitions of both fixed and variable costs are based on volume being within the

relevant range (normal range of activity). If volume is outside the relevant range,

fixed cost may increase in total if volume increases require that additional fixed assets

10. A fixed cost structure would have more risk because profits vary more with changes

in volume. Small changes in volume can cause dramatic changes in profits. In

11. The president appears to be in error because fixed costs frequently can be changed.

For example, fixed costs such as advertising expense, training, and product

changed by selling long-term assets.

12. The statement is false for two reasons. More importantly, the statement ignores the

concept of relevant range. The terms fixed cost and variable cost apply over some

13. Verna is confused because the terms apply to total cost rather than to per unit cost.

Total fixed cost remains constant regardless of the level of production. Total variable

14. Break-even is the point where total revenue is equal to total costs. It can be measured

in units or sales dollars.

15. In the contribution margin income statement all variable costs are subtracted from

16. The margin of safety is the decrease in sales that can occur before experiencing a loss.

The margin of safety expressed as a percentage would mean Company A’s actual sales

17. From Hartwell’s perspective, the $2,000 cost of the computer is a fixed cost. The

Exercise 11-1

Requirement

Fixed

Variable

Mixed

a.

x

b.

x

c.

x

d.

x

e.

x

f.

x

Exercise 11-2

Requirement

Fixed

Variable

Mixed

a.

x

b.

x

c.

x

d.

x

e.

x

f.

x

g.

x

h.

x

i.

x

j.

x

Exercise 11-3

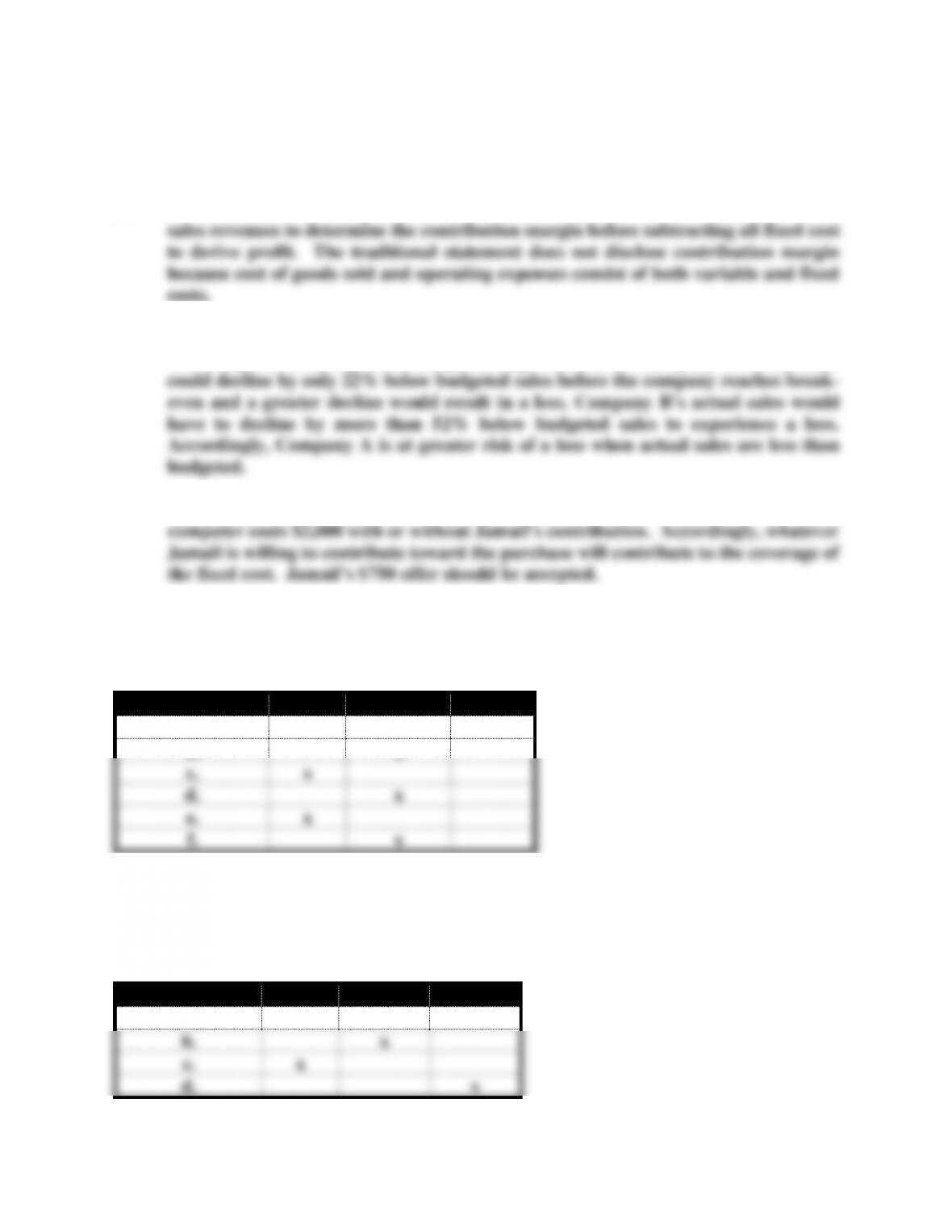

Total Fixed Cost:

Item

Cost

Depreciation

$ 75,000

Officers' salaries

160,000

Long-term lease

38,000

Property taxes

12,000

Total fixed

$285,000

Units Produced (a)

4,000

4,500

5,000

Total fixed cost (b)

$285,000

$285,000

$285,000

Fixed cost per unit (b ÷ a)

$71.25

$63.33

$57.00

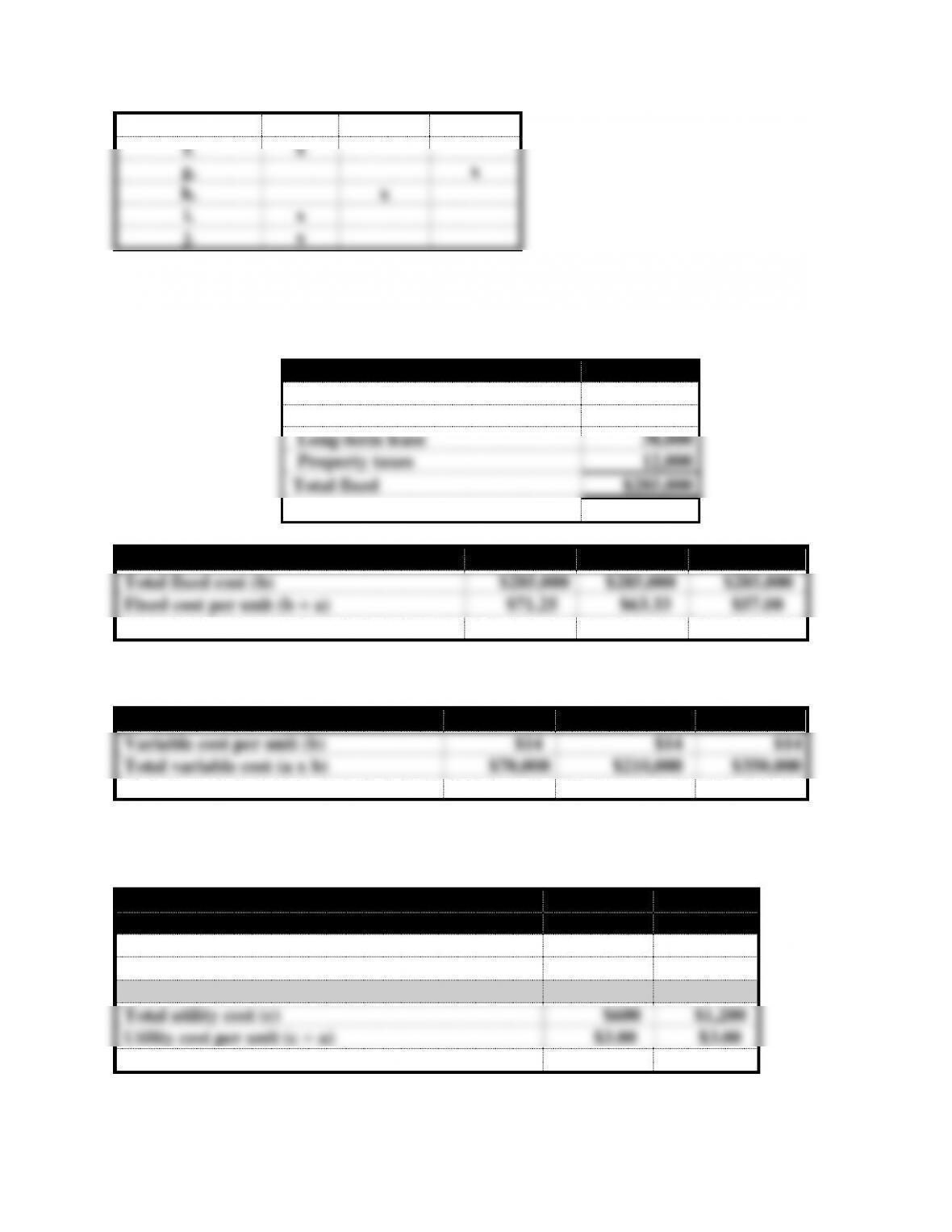

Exercise 11-4

Units Produced (a)

5,000

15,000

25,000

Variable cost per unit (b)

$14

$14

$14

Total variable cost (a x b)

$70,000

$210,000

$350,000

Exercise 11-5

a.

March

April

Units Produced (a)

200

400

Total rent cost (b)

$1,800

$1,800

Rent cost per unit (b ÷ a)

$9.00

$4.50

Total utility cost (c)

$600

$1,200

Utility cost per unit (c ÷ a)

$3.00

$3.00

b.

Since the total rent cost remains unchanged when the number of units produced changes, it

is a fixed cost. Since the total utility cost changes in direct proportion with changes in the

number of units, it is a variable cost.

Exercise 11-6

Number of Units

6,000

8,000

10,000

12,000

Total costs incurred

Fixed

$48,000

$ 48,000

$ 48,000

$ 48,000

Variable

48,000

64,000

80,000

96,000

Total costs

$96,000

$112,000

$128,000

$144,000

Cost per unit

Fixed

$ 8.00

$ 6.00

$ 4.80

$ 4.00

Variable

8.00

8.00

8.00

8.00

Total cost per unit

$16.00

$14.00

$12.80

$12.00

b. The total cost per unit declines as volume increases because the same amount of fixed

cost is spread over an increasingly larger number of units of product.

Exercise 11-7

Exercise 11-8

a.

a.

Total fixed cost

a.

Total variable cost

b.

Fixed cost per unit

Units

Units

$

$

$

$

b.

Variable cost per unit

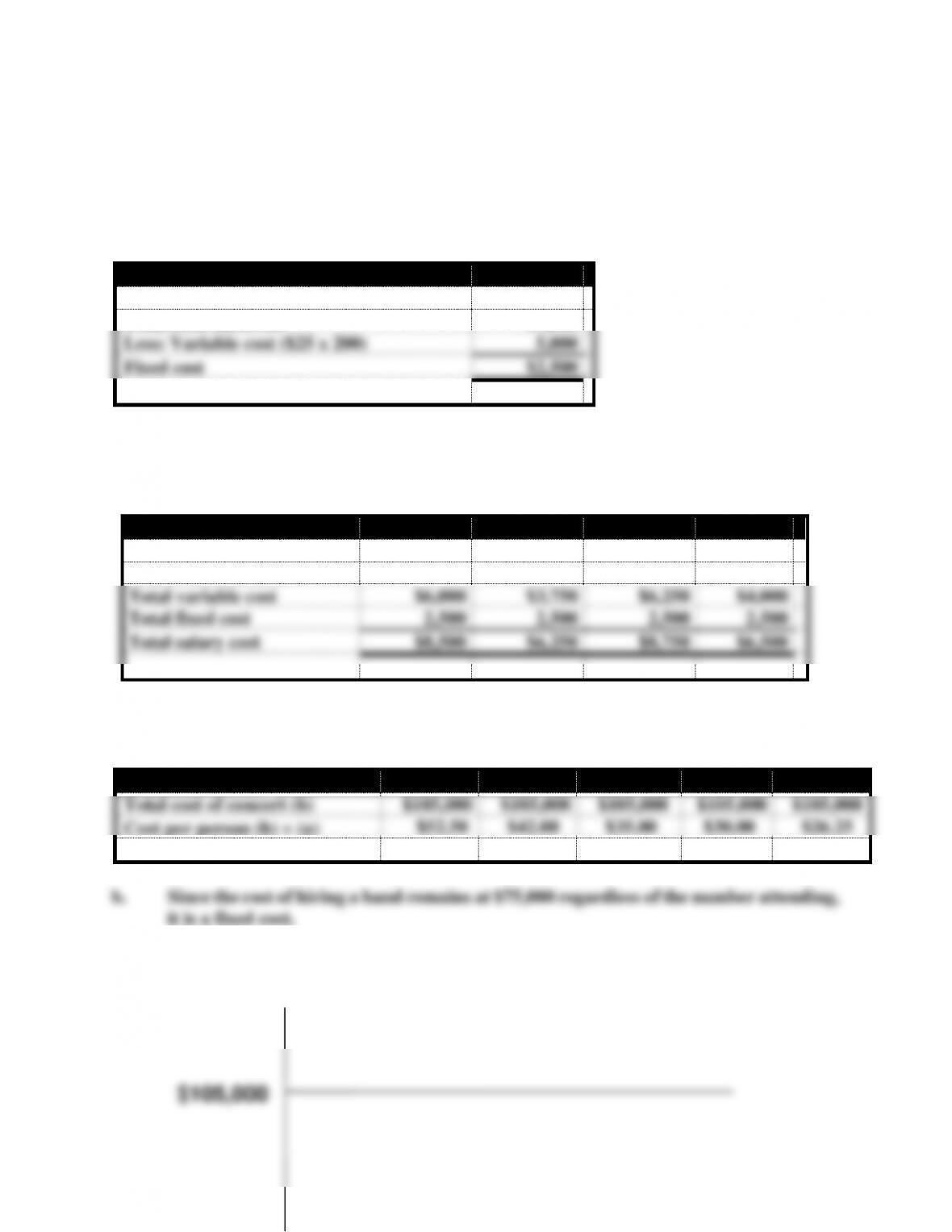

Exercise 11-9

Begin by calculating the fixed cost based on the March sales. Calculate the fixed cost

by subtracting the variable cost from the total cost.

April

Total costs incurred

$7,500

Less: Variable cost ($25 x 200)

5,000

Fixed cost

$2,500

The fixed portion of the mixed cost will remain at $2,500 for any volume of sales within

the relevant range. Accordingly, this cost will be the same for all of the months under

consideration.

Month

April

May

June

July

Number of units

240

150

250

160

Total costs incurred

Total variable cost

$6,000

$3,750

$6,250

$4,000

Total fixed cost

2,500

2,500

2,500

2,500

Total salary cost

$8,500

$6,250

$8,750

$6,500

Exercise 11-10

a.

Number Attending (a)

2,000

2,500

3,000

3,500

4,000

Total cost of concert (b)

$105,000

$105,000

$105,000

$105,000

$105,000

Cost per person (b) (a)

$52.50

$42.00

$35.00

$30.00

$26.25

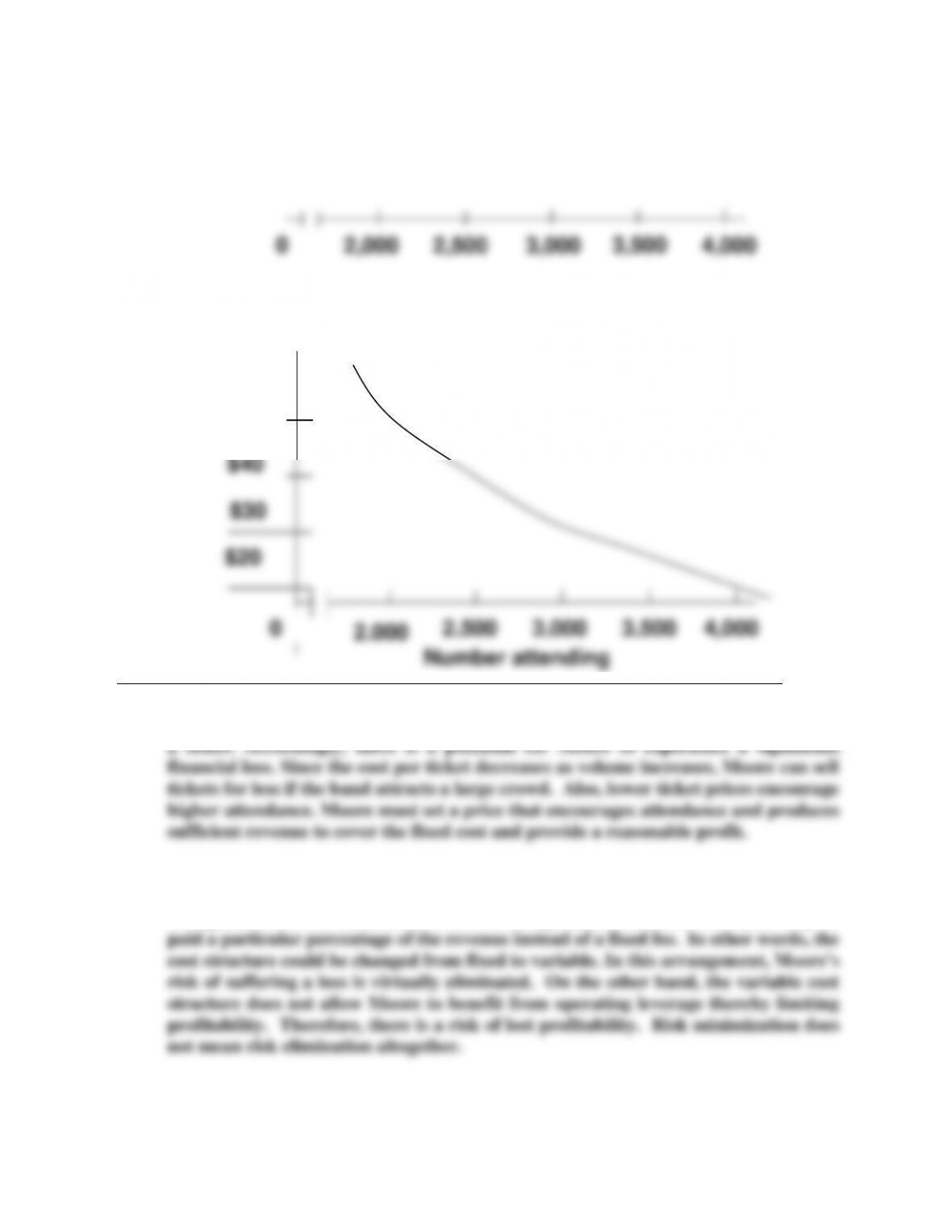

c.

$105,000

Total cost

Exercise 11-10 (continued)

d. Moore’s major business risk is the uncertainty about whether it can generate enough

revenue to cover the fixed cost. Moore must pay the $105,000 cost even if no one buys

To a large extent, Moore’s business risk is the result of its cost structure. To minimize

the risk, Moore could possibly change that structure. For instance, Moore may want

to negotiate with the band to set a flexible compensation scheme. The band may be

Number attending

Cost per unit

$50

Other business risks that may adversely affect Moore’s profit include competition,

unfavorable economy, security, and litigation.

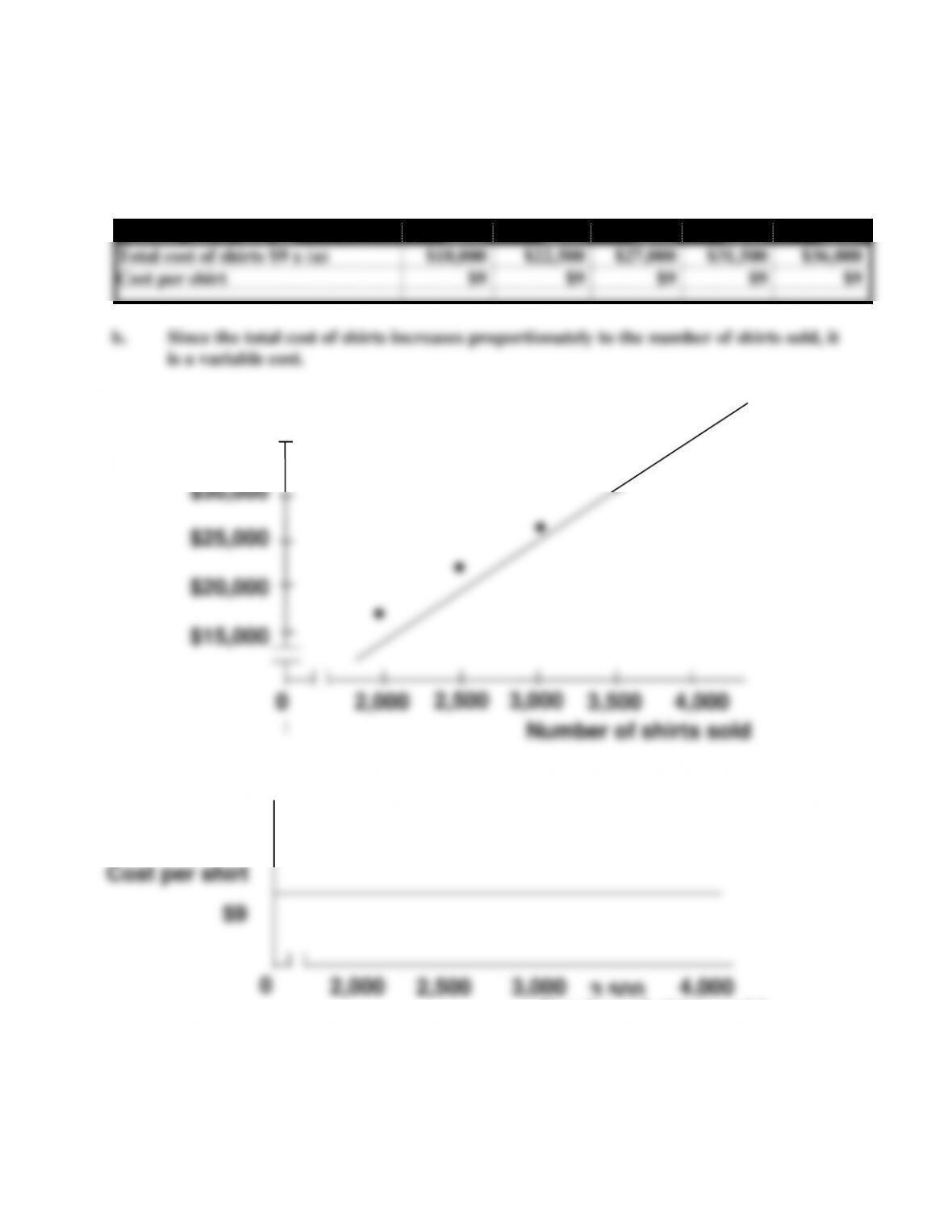

Exercise 11-11

a.

Number shirts sold (a)

2,000

2,500

3,000

3,500

4,000

Total cost of shirts $9 x (a)

$18,000

$22,500

$27,000

$31,500

$36,000

Cost per shirt

$9

$9

$9

$9

$9

c.

Exercise 11-11 (continued)

d. Moore’s major business risk is the uncertainty about whether it can generate a

desirable profit. The cost and the revenue are both variable if Moore can return unsold

Total Cost

$35,000

.

.

0

2,000

2,500

3,000

3,500

4,000

Number of shirts sold

$

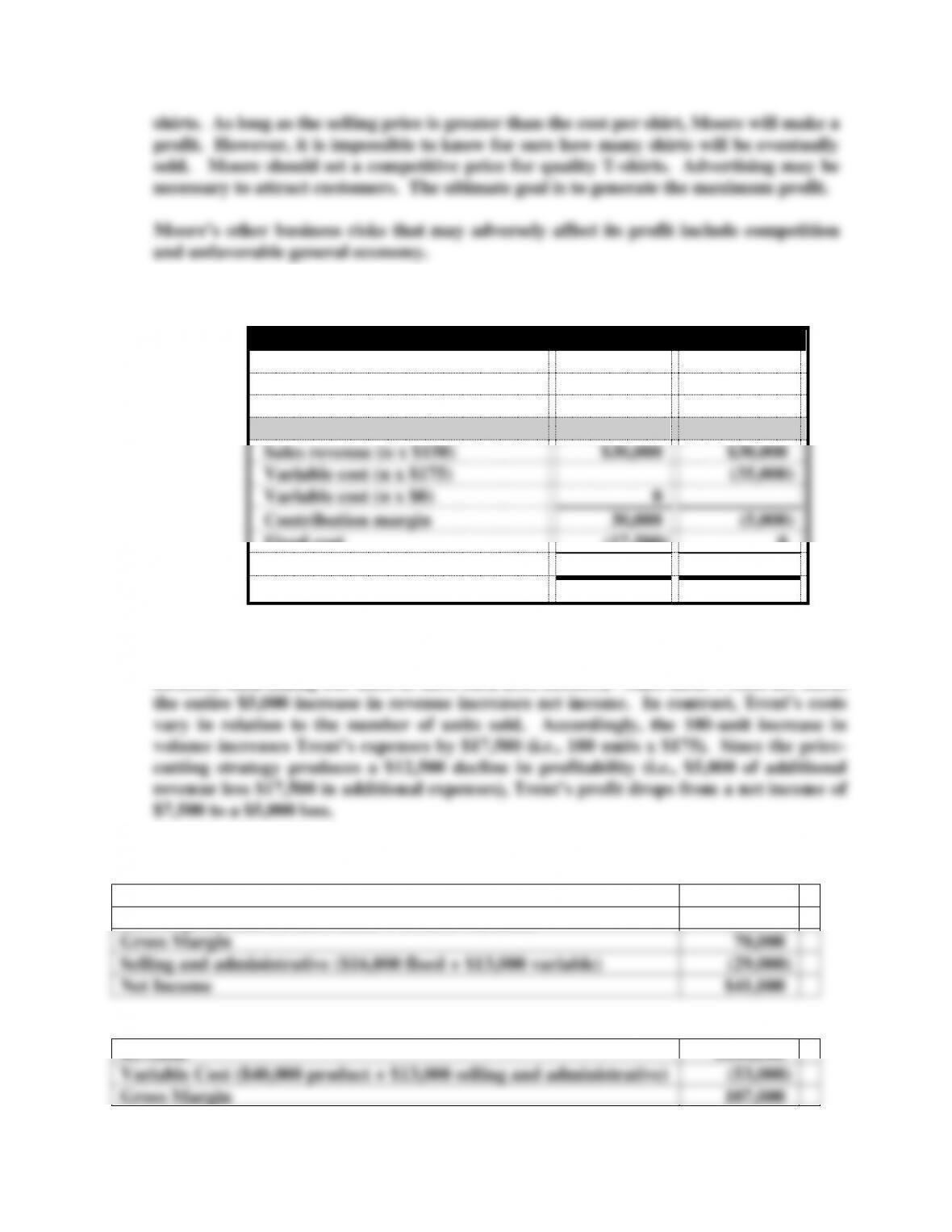

Exercise 11-12

Income Statements

a.

b.

Company Name

Kent

Trent

Number of Customers (n)

200

200

Sales revenue (n x $150)

$30,000

$30,000

Variable cost (n x $175)

(35,000)

Variable cost (n x $0)

0

Contribution margin

30,000

(5,000)

Fixed cost

(17,500)

0

Net income

$12,500

$ (5,000)

c. The strategy of cutting prices increases Kent’s revenue by $5,000 (i.e., $30,000 –

$25,000). In other words, selling 200 units at $150 each produces more revenue (i.e.,

$30,000) than selling 100 units at $250 each (i.e., $25,000). Since Kent’s costs are fixed,

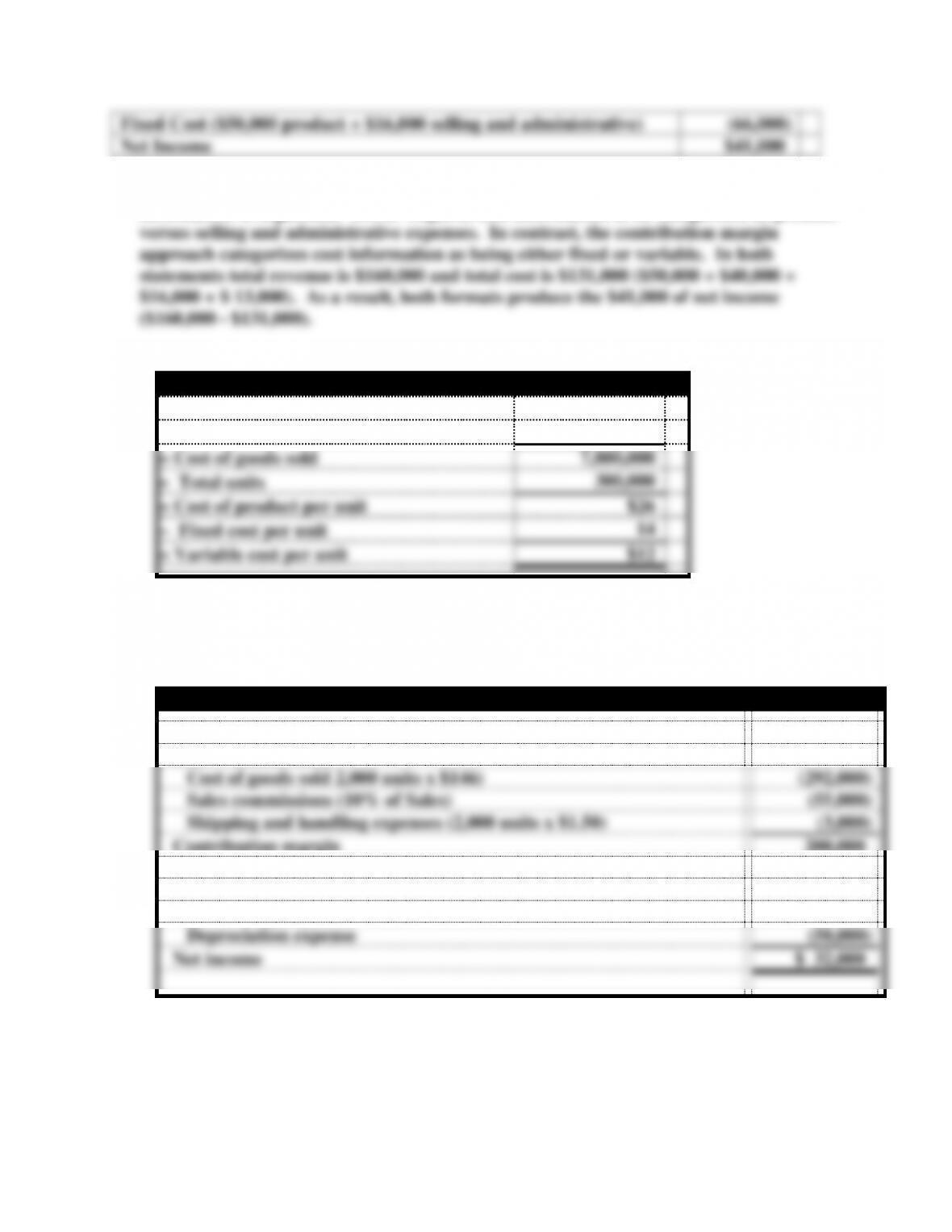

Exercise 11-13

a. GAAP format:

Revenue

$160,000

Cost of goods sold ($50,000 fixed + $40,000 variable)

(90,000)

Gross Margin

70,000

Selling and administrative ($16,000 fixed + $13,000 variable)

(29,000)

Net Income

$41,000

b. Contribution margin format:

Revenue

$160,000

Variable Cost ($40,000 product + $13,000 selling and administrative)

(53,000)

Gross Margin

107,000

a. & b.

Fixed Cost ($50,000 product + $16,000 selling and administrative)

(66,000)

Net Income

$41,000

c. Both statements contain the same information. The difference is in how the

information is organized. GAAP requires cost information to be categorized as product

Exercise 11-14

Income Statement

Sales revenue ($35 x 300,000)

$10,500,000

− Gross margin

2,700,000

= Cost of goods sold

7,800,000

Total units

300,000

= Cost of product per unit

$26

− Fixed cost per unit

14

= Variable cost per unit

$12

Variable cost = $12 x 300,000 = $3,600,000

Total contribution margin = $10,500,000 − $3,600,000 = $6,900,000

Exercise 11-15

Income Statement

Sales Revenue (2,000 units x $275)

$550,000

Less: Variable costs

Cost of goods sold 2,000 units x $146)

(292,000)

Sales commissions (10% of Sales)

(55,000)

Shipping and handling expenses (2,000 units x $1.50)

(3,000)

Contribution margin

200,000

Less: Fixed costs

Administrative salaries

(80,000)

Advertising expense

(38,000)

Depreciation expense

(50,000)

Net income

$ 32,000

b.

Contribution margin

Operating leverage

=

—––——————––—

Net income

a.