5-1

EXERCISE 5-11

Balance Sheet

Income Statement

Statement of

Date

Assets

=

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Cash

+

Note Rec.

+

Int. Rec.

=

Ret. Ear.

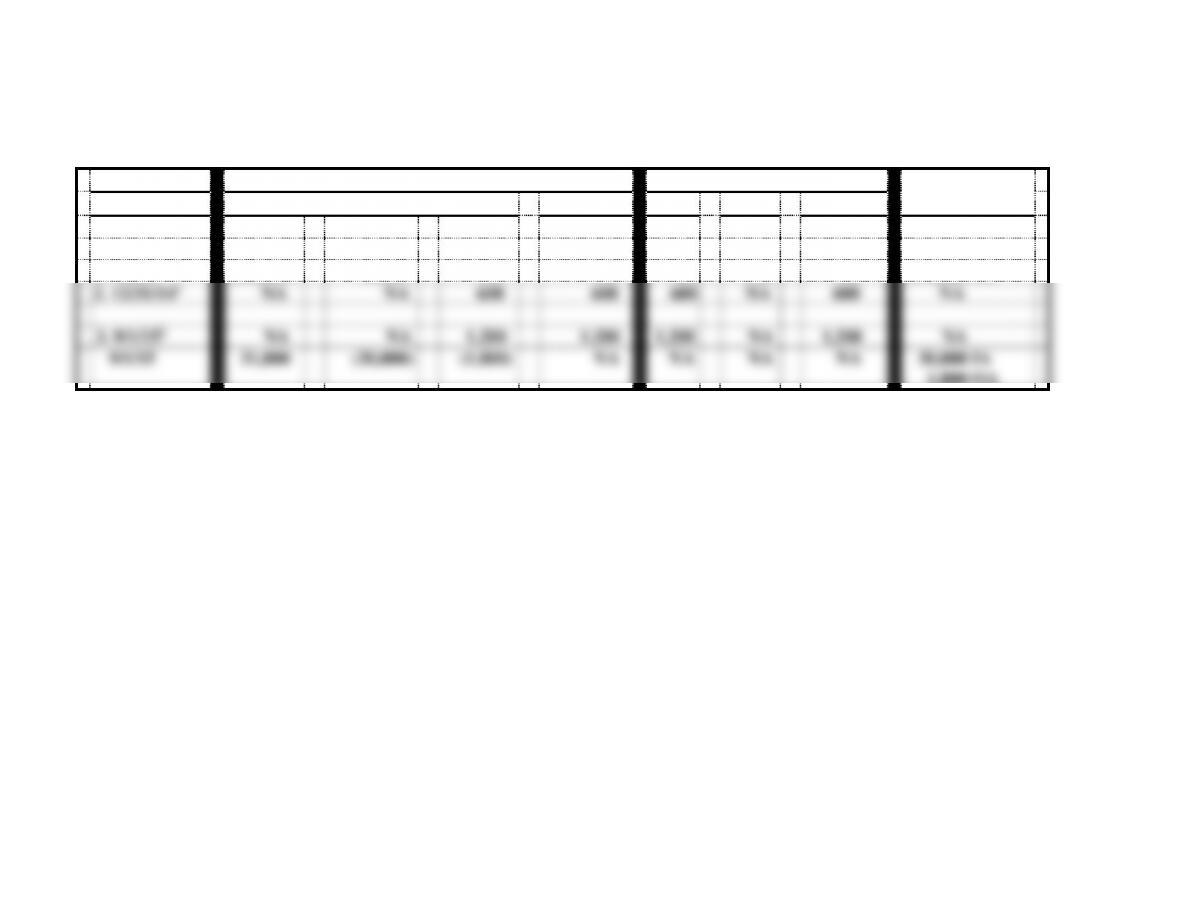

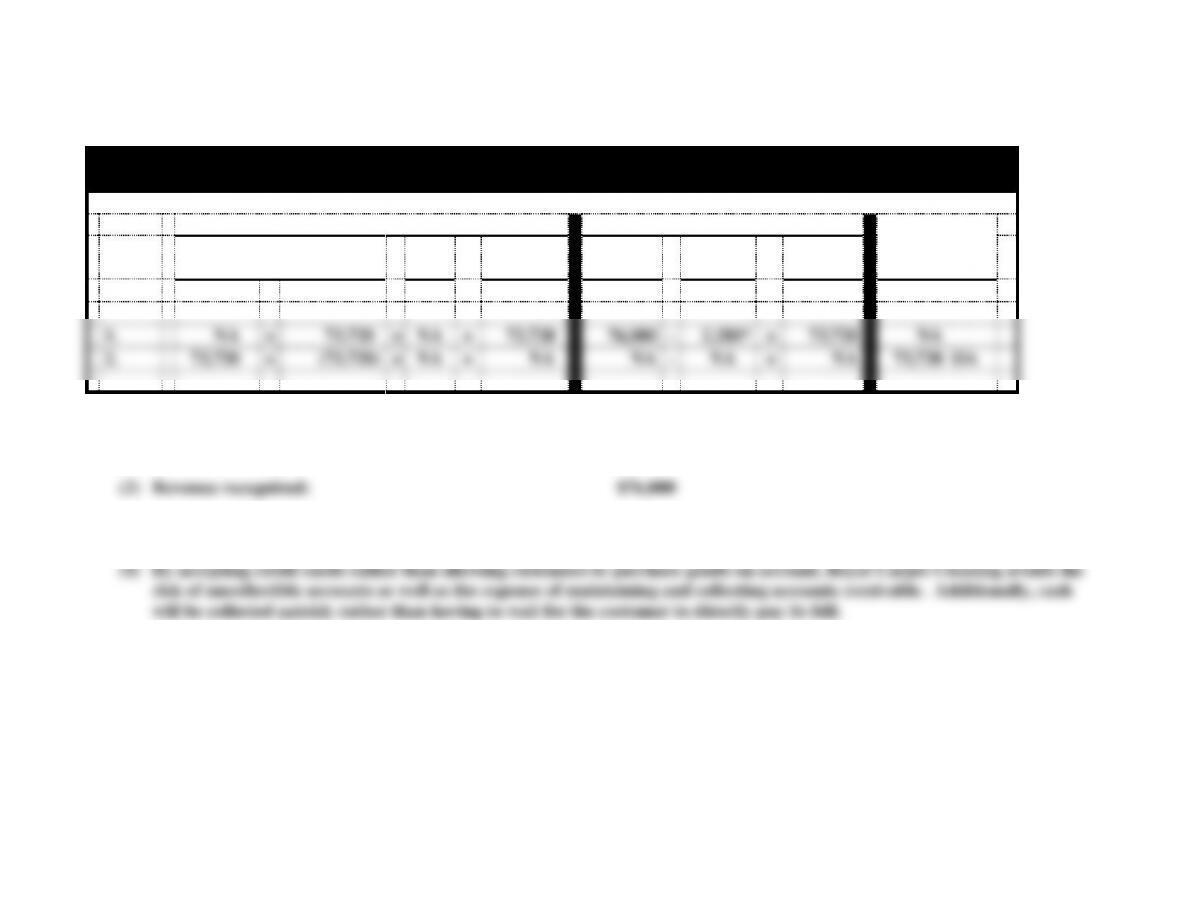

1. 9/1/14

(30,000)

30,000

NA

NA

NA

NA

NA

(30,000) IA

2. 12/31/141

NA

NA

600

600

600

NA

600

NA

3. 9/1/152

NA

NA

1,200

1,200

1,200

NA

1,200

NA

9/1/15

31,800

(30,000)

(1,800)

NA

NA

NA

NA

30,000 IA

1,800 OA

1$30,000 x 6% x 4/12 = $600

2$30,000 x 6% x 8/12 = $1,200

5-2

EXERCISE 5-12

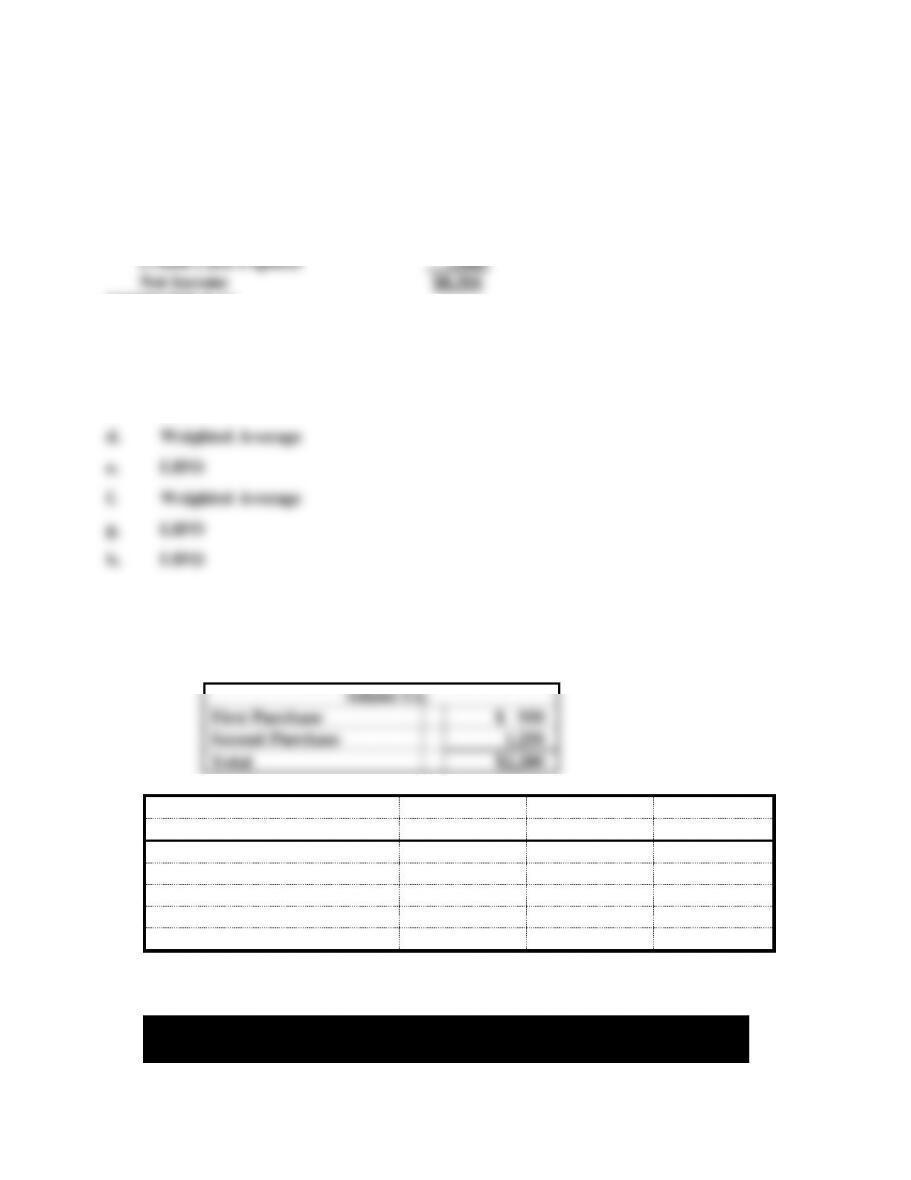

a. $18,000 x 5% x 10/12 = $750

b. Total Receivables at December 31, 2014:

Notes Receivable $18,000

Interest Receivable 750

Total Receivables $18,750

e. Total Cash to be collected:

5-3

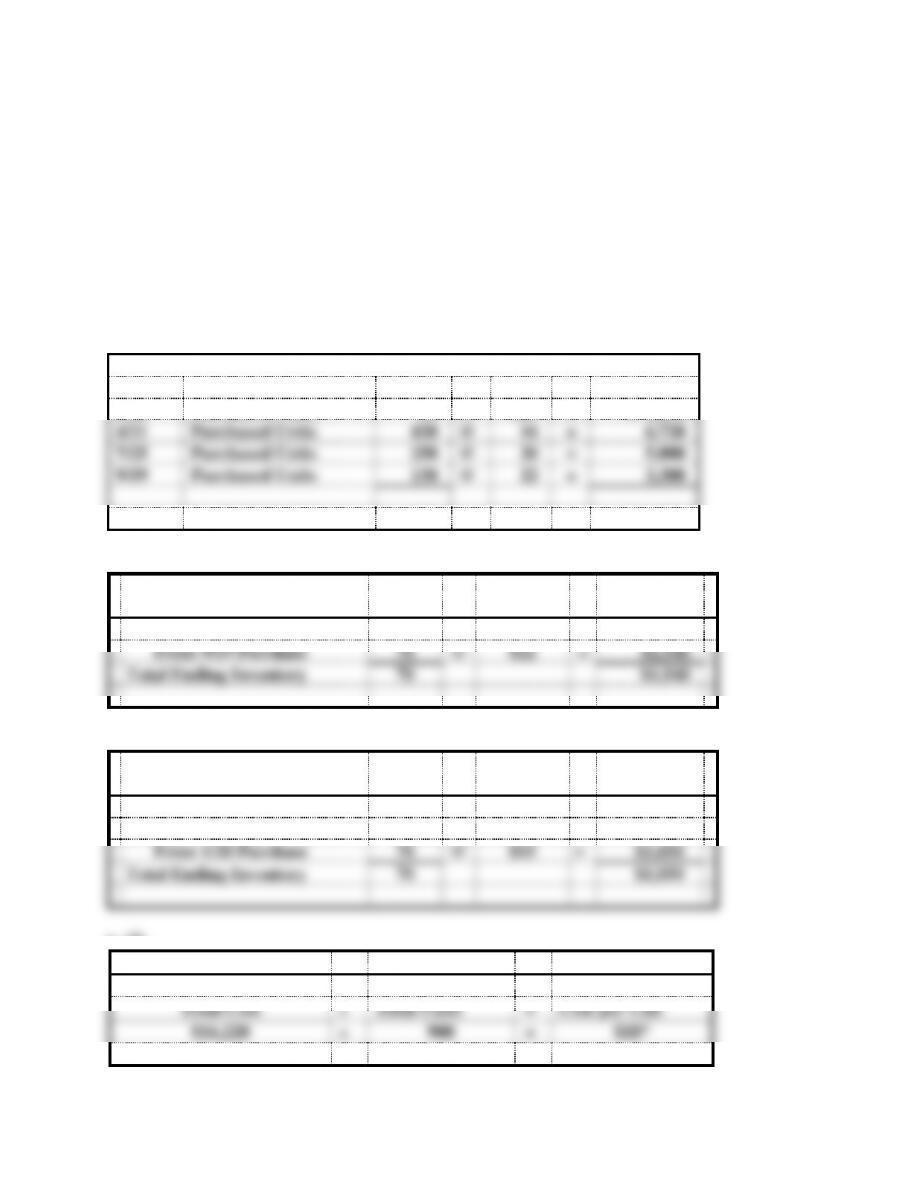

EXERCISE 5-13

a.

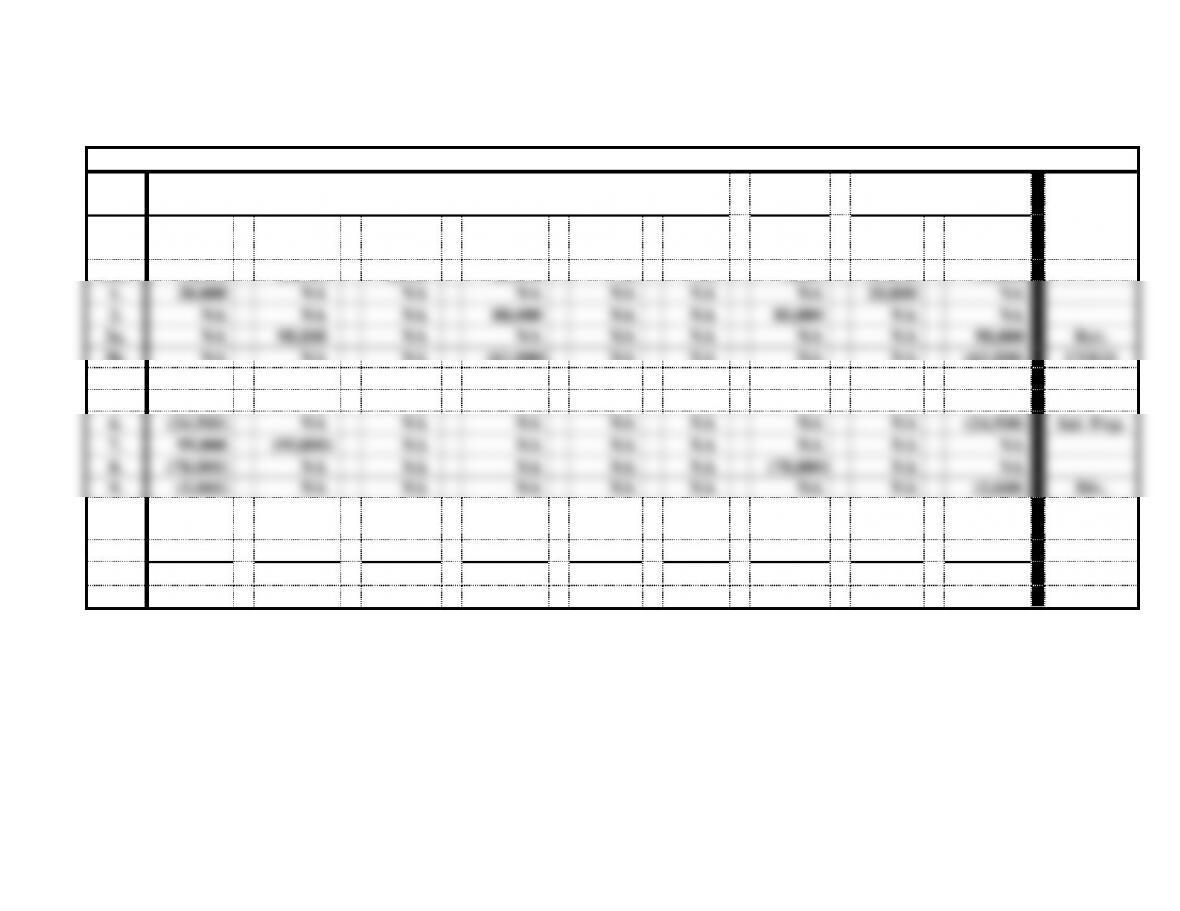

Hardwood Timber Company – Accounting Equation

Assets

=

Liab.

+

Equity

Acct.

Title/Re

Event

Cash

+

A. Rec.

−

Allow.

+

Mdse Inv.

+

Notes

Rec.

+

Int.

Rec.

=

Accts.

Pay.

+

Com.

Stock

=

Ret.

Earn.

Bal.

16,000

18,000

2,000

25,000

NA

NA

9,200

30,000

17,800

1.

20,000

NA

NA

NA

NA

NA

NA

20,000

NA

2.

NA

NA

NA

80,000

NA

NA

80,000

NA

NA

3a.

NA

98,000

NA

NA

NA

NA

NA

NA

98,000

Rev.

3b.

NA

NA

NA

(61,000)

NA

NA

NA

NA

(61,000)

COGS

4.

NA

(1,500)

(1,500)

NA

NA

NA

NA

NA

NA

5.

(10,000)

NA

NA

NA

10,000

NA

NA

NA

NA

6.

(24,500)

NA

NA

NA

NA

NA

NA

NA

(24,500)

Sal. Exp.

7.

99,000

(99,000)

NA

NA

NA

NA

NA

NA

NA

8.

(78,000)

NA

NA

NA

NA

NA

(78,000)

NA

NA

9.

(5,000)

NA

NA

NA

NA

NA

NA

NA

(5,000)

Div.

10.1

NA

NA

980

NA

NA

NA

NA

NA

(980)

Uncoll.

Exp

11.2

NA

NA

NA

NA

NA

200

NA

NA

200

Int. Rev.

Bal.

17,500

+

15,500

−

1,480

+

44,000

+

10,000

+

200

=

11,200

+

50,000

+

24,520

1$98,000 x 1% = $980

2$10,000 x 6% x 4/12 = $200

Assets

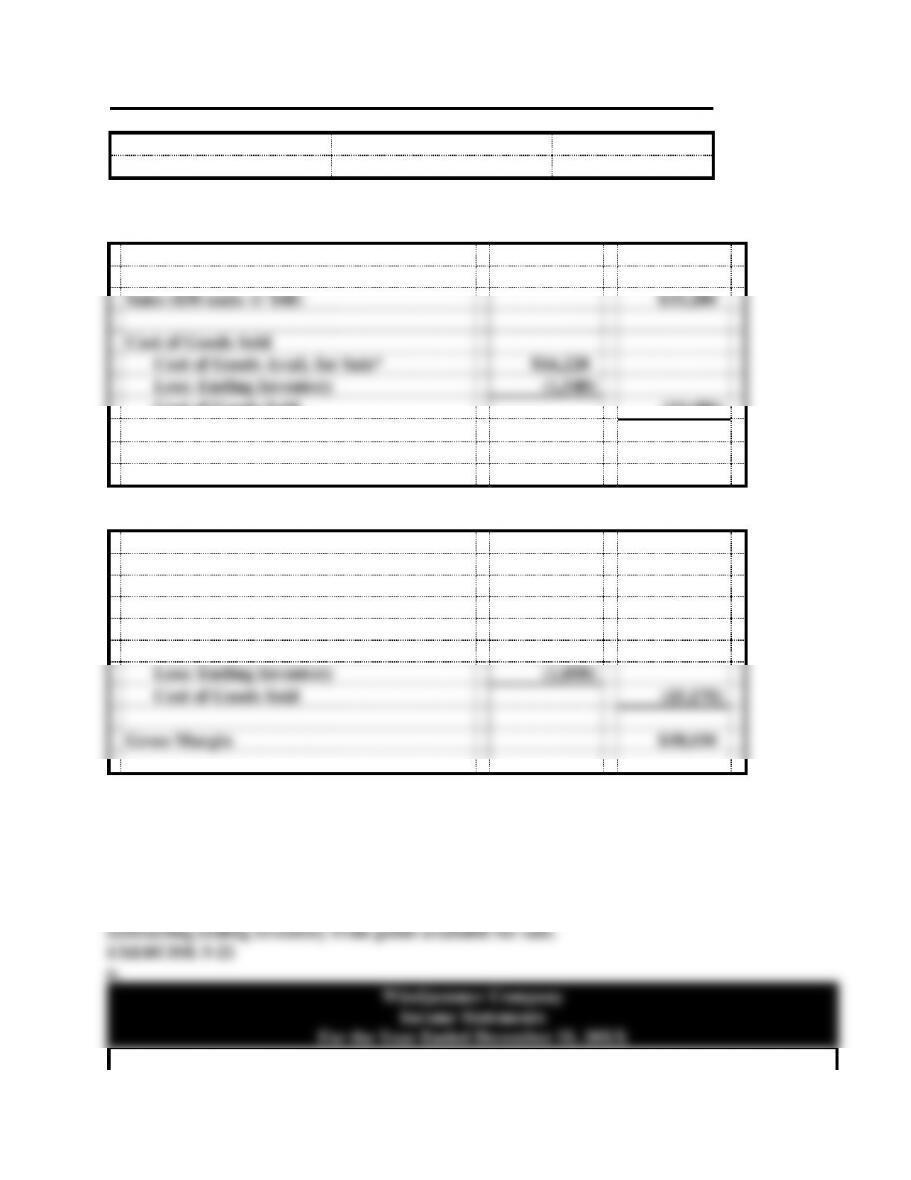

EXERCISE 5-13

b.

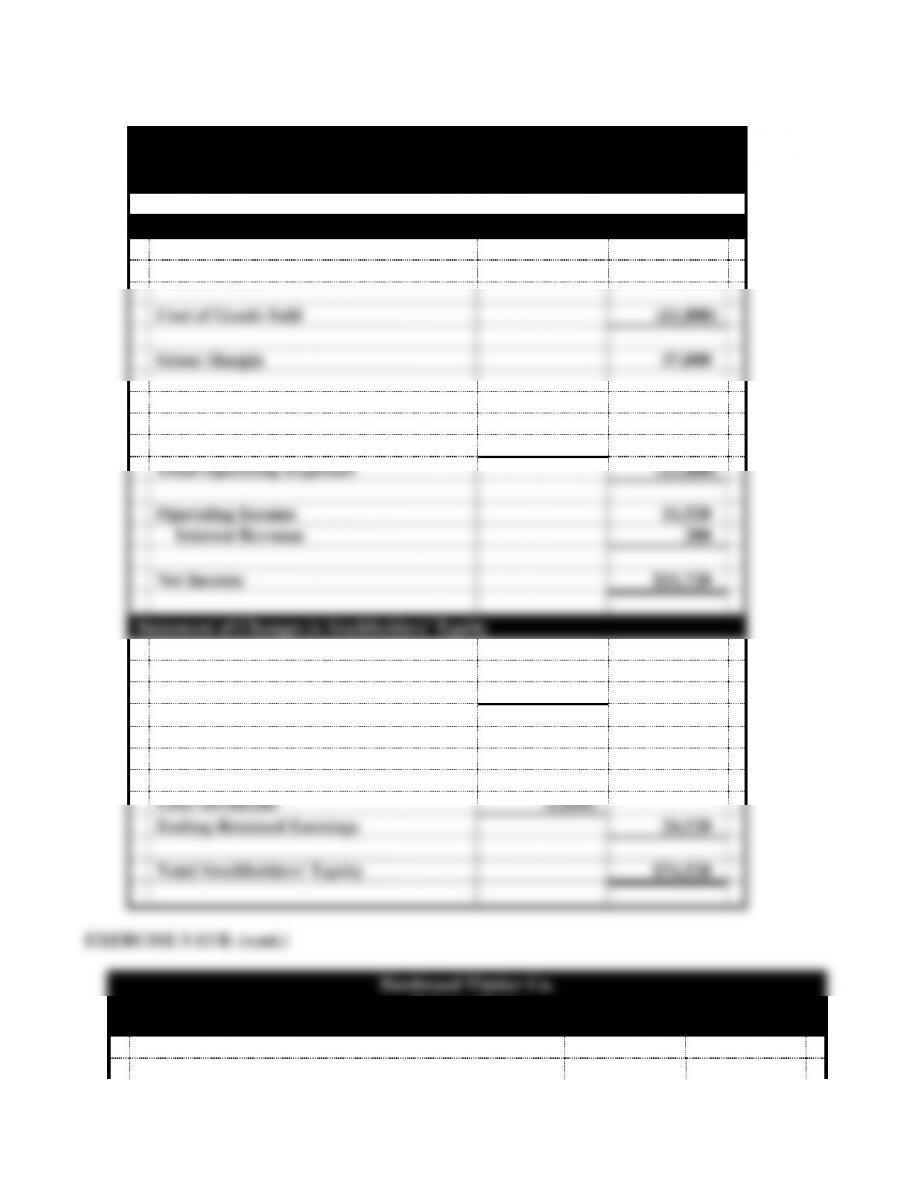

Hardwood Timber Co.

Financial Statements

For the Year Ended December 31, 2014

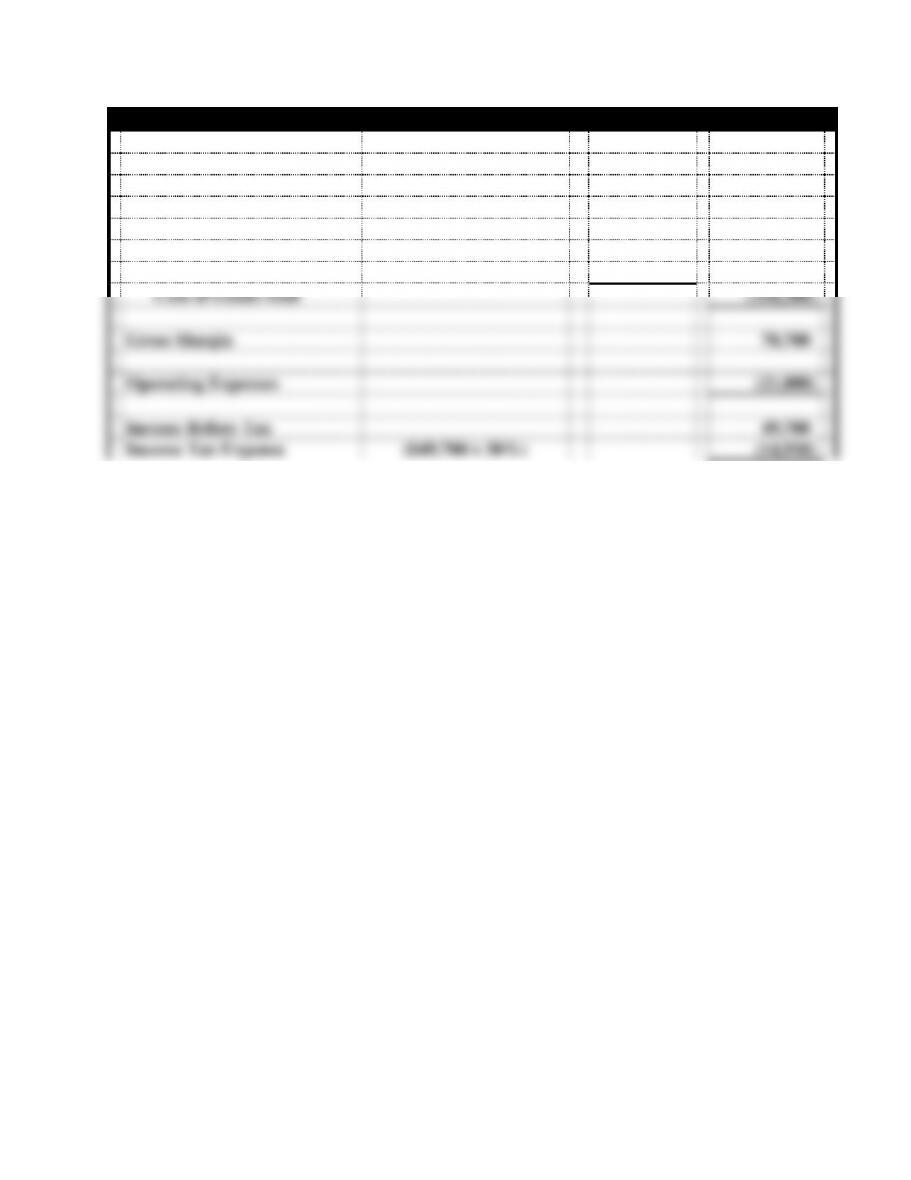

Income Statement

Sales Revenue

$98,000

Cost of Goods Sold

(61,000)

Gross Margin

37,000

Operating Expenses

Salaries Expense

$24,500

Uncollectible Accounts Exp.

980

Total Operating Expenses

(25,480)

Operating Income

11,520

Interest Revenue

200

Net Income

$11,720

Statement of Changes in Stockholders’ Equity

Beginning Common Stock

$30,000

Plus: Stock Issued

20,000

Ending Common Stock

$50,000

Beginning Retained Earnings

$17,800

Plus: Net Income

11,720

Less: Dividends

(5,000)

Ending Retained Earnings

24,520

Total Stockholders’ Equity

$74,520

5-5

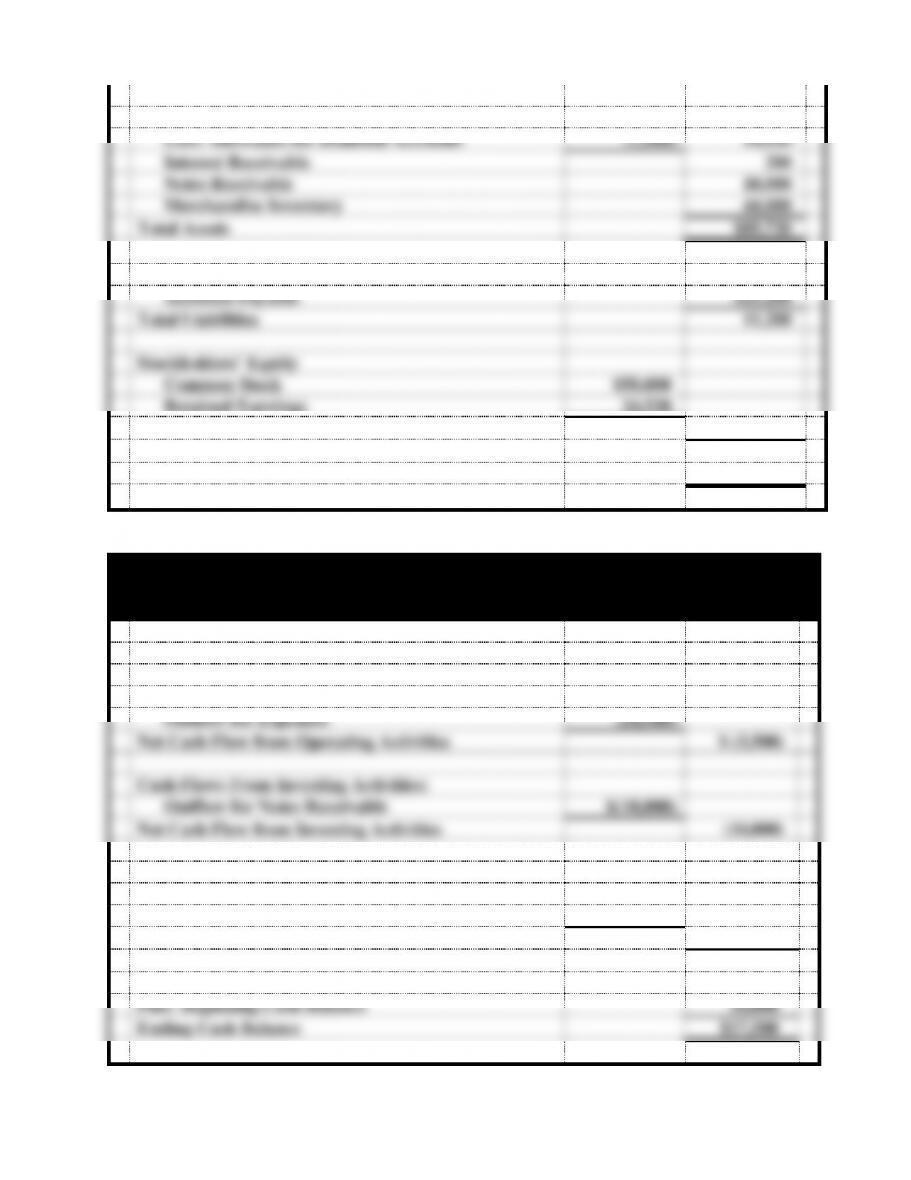

Cash

$17,500

Accounts Receivable

$15,500

Less: Allowance for Doubtful Accounts

(1,480)

14,020

Interest Receivable

200

Notes Receivable

10,000

Merchandise Inventory

44,000

Total Assets

$85,720

Liabilities

Accounts Payable

$11,200

Total Liabilities

11,200

Stockholders’ Equity

Common Stock

$50,000

Retained Earnings

24,520

Total Stockholders’ Equity

74,520

Total Liabilities and Stockholders’ Equity

$85,720

EXERCISE 5-13 B. (cont.)

Hardwood Timber Co.

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash Flows From Operating Activities:

Inflow from Customers

$99,000

Outflow for Inventory

(78,000)

Outflow for Expenses

(24,500)

Net Cash Flow from Operating Activities

$ (3,500)

Cash Flows From Investing Activities:

Outflow for Notes Receivable

$(10,000)

Net Cash Flow from Investing Activities

(10,000)

Cash Flows From Financing Activities:

Inflow from Stock Issue

$20,000

Outflow for Dividend

(5,000)

Net Cash Flow from Financing Activities

15,000

Net Change in Cash

1,500

Plus: Beginning Cash Balance

16,000

Ending Cash Balance

$17,500

5-6

EXERCISE 5-14

a.

Superior Carpet Cleaning

Horizontal Statements Model

Balance Sheet

Income Statement

Statement of

Assets

=

Liab

.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Event

Cash

+

Acc. Rec.

=

+

Ret. Ear

1.

NA

+

73,720

=

NA

+

73,720

76,000

−

2,280*

=

73,720

NA

2.

73,720

+

(73,720)

=

NA

+

NA

NA

−

NA

=

NA

73,720 OA

*$76,000 x 3% = $2,280

b. (1) Total assets: Cash $73,720

(3) Cash Flow from Operating Activities: $73,720

5-7

EXERCISE 5-15

Credit card expense: Sales $8,650 x 4% = $346

Net Income:

Service Revenue $8,650

EXERCISE 5-16

a. FIFO

b. FIFO

c. FIFO

EXERCISE 5-17

Adams Co.

First Purchase

$ 950

Second Purchase

1,250

Total

$2,200

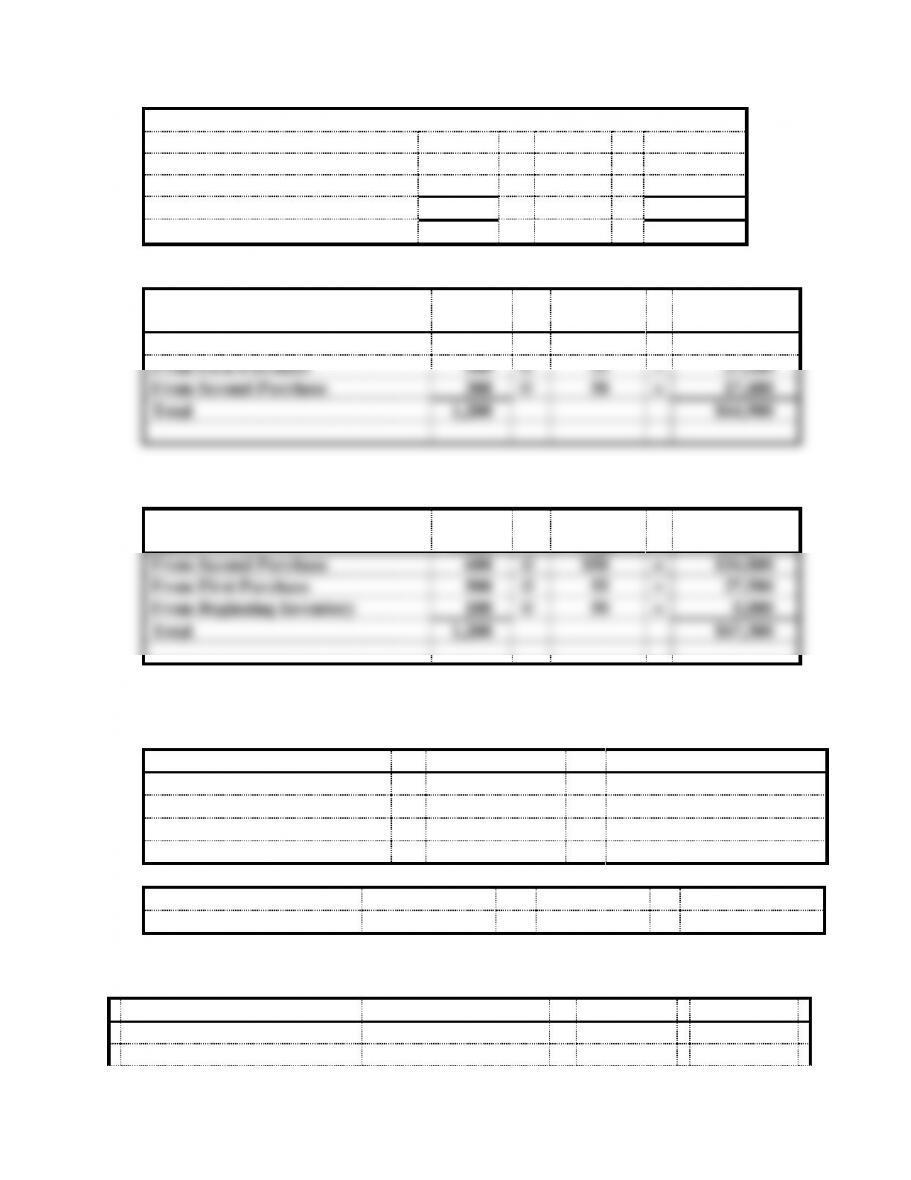

(a)

(b)

(c)

FIFO

LIFO

W. AVG.

Cost of Goods Sold

$ 950

$1,250

$1,100*

Ending Inventory

1,250

950

1,100*

*Average Cost per Unit: $2,200 2 = $1,100EXERCISE 5-18

Suggs Company

Inventory Purchases

5-8

Beginning Inventory

400

@

$50

=

$20,000

First Purchase

500

@

55

=

27,500

Second Purchase

600

@

58

=

34,800

Goods Available for Sale

1,500

$82,300

a. Cost of Goods Sold:

FIFO

Units

Cost per

Unit

Cost of Goods

Sold

From Beginning Inventory

400

@

$50

=

$20,000

From First Purchase

500

@

55

=

27,500

From Second Purchase

300

@

58

=

17,400

Total

1,200

$64,900

Ending Inventory: 300 units from Second Purchase @ $58 = $17,400

b. Cost of Goods Sold:

LIFO

Units

Cost per

Unit

Cost of Goods

Sold

From Second Purchase

600

@

$58

=

$34,800

From First Purchase

500

@

55

=

27,500

From Beginning Inventory

100

@

50

=

5,000

Total

1,200

$67,300

Ending Inventory: 300 units from Beginning Inventory @ $50 = $15,000

c.

Weighted Average:

Total Cost

Total Units

=

Cost per Unit

$82,300

1,500

=

$54.8667

Cost of Goods Sold

1,200 units

@

$54.8667

=

$65,840

Ending Inventory

300 units

@

$54.8667

=

$16,460

EXERCISE 5-19

a. (1) Baxter Company

FIFO

Sales (370 @ $30)

$11,100

5-9

Cost of Goods Sold:

From Beginning Inv.

90 units @ $15

=

$ 1,350

From Purchases

280 units @ $19

=

5,320

(6,670)

Gross Margin

$4,430

a. (2)

LIFO

Sales (370 @ $30)

$11,100

Cost of Goods Sold:

From Purchases

320 units @ $19

=

$6,080

From Beg. Inv.

50 units @ $15

=

750

(6,830)

Gross Margin

$4,270

a. (3)

Weighted Average

Sales (370 @ $30)

$11,100

Cost of Goods Sold:

Average Cost per Unit

370 @ $18.122*

=

$6,705

(6,705)

Gross Margin

$4,395

b. $160 ($4,430 − $4,270). The difference in net income would be the same as the

difference in gross margin, assuming there are no income tax

considerations.EXERCISE 5-19 (cont.)

c.

FIFO

LIFO

W. Avg.

Cash Flows From Operating Activities:

Cash Inflow from Customers

$11,100

$11,100

$11,100

Cash Outflow for Inventory

(6,080)

(6,080)

(6,080)

Net Cash Flow from Operating Act.

$5,020

$5,020

$5,020

5-10

Net cash flow from operating activities will be the same for all three methods because the

amount of cash from sales and the amount of cash paid for inventory is the same regardless

of the method of cost flow assumed. If the company were subject to income tax, the

amount of cash paid for tax expense would be different because the amount of taxable

income would be different.

EXERCISE 5-20

a.

Dugan Sales

Summary of Purchase Transactions

1/20

Purchased Units

80

@

$15

=

$ 1,200

4/21

Purchased Units

420

@

16

=

6,720

7/25

Purchased Units

250

@

20

=

5,000

9/19

Purchased Units

150

@

22

=

3,300

Available for Sale

900

$16,220

a. (1)

FIFO

Units

Cost

per Unit

Ending Inventory

From 9/19 Purchase

70

@

$22

=

$1,540

Total Ending Inventory

70

$1,540

a. (2)

LIFO

Units

Cost

per Unit

Ending Inventory

From 1/20 Purchase

70

@

$15

=

$1,050

Total Ending Inventory

70

$1,050

a. (3)

Weighted Average

Total Cost

Total Units

=

Cost per Unit

$16,220

900

=

$18*

Ending Inventory

70 units @ $18 =

$1,260

*roundedEXERCISE 5-20 (cont.)

B.

FIFO

Sales (830 units @ $40)

$33,200

Cost of Goods Sold

Cost of Goods Avail. for Sale*

$16,220

Less: Ending Inventory

(1,540)

Cost of Goods Sold

(14,680)

Gross Margin

$18,520

LIFO

Sales (830 units @ $40)

$33,200

Cost of Goods Sold

Cost of Goods Avail. for Sale*

$16,220

Less: Ending Inventory

(1,050)

Cost of Goods Sold

(15,170)

Gross Margin

$18,030

*This amount is computed in the Summary of Purchase Transactions at the beginning of the

problem.

Difference in Gross Margin: $18,520 − $18,030 = $490

Note to Instructor: Cost of goods sold can be computed on a units-sold basis rather than

5-12

FIFO

Sales (3,500 @ $50)

$175,000

Cost of Goods Sold:

From Beginning Inv.

300 units @ $25

=

$ 7,500

From 4/1 Purchase

2,800 units @ $30

=

84,000

From 10/1 Purchase

400 units @ $32

=

12,800

Cost of Goods Sold

(104,300)

Gross Margin

70,700

Operating Expenses

(21,000)

Income Before Tax

49,700

Income Tax Expense

($49,700 x 30%)

(14,910)