1-7

ANSWERS TO QUESTIONS – CHAPTER 1

1. Stakeholders are the parties that use accounting information.

Stakeholders with a direct interest include owners, managers, creditors, suppliers, and

employees. These individuals are directly affected by what happens to the business.

All students are direct users of accounting information related to tuition and fees,

financial aid, and account balances.

2. Accounting provides information that is useful in making decisions by all participants in

3. The primary mechanism used to allocate resources in the U.S. is competition for

resources in the open market.

5. The market for business resources involves three distinct participants: consumers,

6. Financial Resource: money

Physical Resource: natural resources (i.e. land, forests, mine ore, petroleum, etc.),

7. Investors expect a distribution of the business’s profits as a return on their financial

investment (capital allocation).

8. Financial accounting provides information that is useful to external resource providers.

1-8

9. Not-for-profit or nonprofit entities provide goods or services to consumers for

humanitarian or special reasons rather than to earn a profit for owners. For example,

10. The U.S. rules of accounting information measurement are called generally accepted

accounting principles (GAAP).

11. Careers in public accounting consist of providing services to the general public from a

public accounting firm. These services include auditing, tax and consulting services.

12. Items reported on the financial statements are organized into classes or categories called

elements. The ten elements of financial statements are:

1. Assets

2. Liabilities

13. Assets, the economic resources of a business, are used to produce earnings.

14. The assets of a business belong to that business entity and there may be claims on the

15. Creditors are individuals and/or institutions that have provided goods or services to the

16. The term “liabilities” is used to describe creditors’ claims on the assets of a business.

1-9

Assets are the economic resources used by a business for the production of revenue.

18. The owners ultimately bear the risk and collect the rewards associated with operating a

business.

19. A double-entry bookkeeping system is one in which every transaction affects at least two

20. Capital is acquired from owners by issuing stock to them. When stock is issued, the assets

21. Assets that are acquired by issuing common stock are the result of investments by owners.

22. Revenue increases the asset side of the accounting equation and also increases the

retained earnings account in the stockholders’ equity section of the equation.

24. Retained earnings are a result of a business retaining its earned assets, rather than

25. Distributions to owners, called dividends, decrease the asset side of the accounting

26. Dividends and expenses are similar in that they both decrease assets and affect the

accounting equation in the same way (i.e. reduction of retained earnings). However,

27. (1) Income Statement – measures the difference between the asset increases and the

asset decreases that were associated with operating a business during a particular

accounting period.

(2) Statement of Changes in Stockholders’ Equity – explains the effects of transactions

1-10

(4) Statement of Cash Flows – explains how a company obtained and used cash during

the accounting period.

28. The balance sheet provides information about the enterprise at a particular point in time.

30. (1) Operating activities – explain the cash generated from revenue and the cash paid

for expenses.

31. Asset accounts are arranged on the balance sheet in accordance with their level of

liquidity (those that can be most quickly converted to cash are listed first).

33. Temporary accounts are used to capture information for a single accounting period. The

balances in temporary accounts are transferred out of the accounts at the end of the

34. The historical cost concept requires that most assets be reported at the amount paid for

35. An asset source transaction results in an increase in an asset account and an increase in

one of the claims accounts; i.e., investments by owners (equity), borrowing funds from

creditors (liabilities), or earnings activities (revenue).

A claims exchange transaction will be covered in a later chapter.

1-11

36. While the contents of annual reports vary from company to company, all annual reports

contain:

Auditor’s report

37. U.S. GAAP, generally accepted accounting principles in the United States, are the

measurement rules established by the (FASB) Financial Accounting Standards Board.

SOLUTIONS TO EXERCISES – SERIES A – CHAPTER 1

EXERCISE 1-1

The three types of resources available to conversion agents are:

Note to instructor:

The memo should discuss the fact that the resource owners are those who own resources that are

desired by others, either in the original form or in a converted form. The conversion agents are

It should also include a discussion of the role of the private accountant and the allocation of

resources. For example, private accountants prepare the annual reports that businesses

EXERCISE 1-2

a. The three areas of service provided by public accountants are auditing, tax and

consulting.

1-12

b. The private accountant generally works for a specific company. Some of the functions

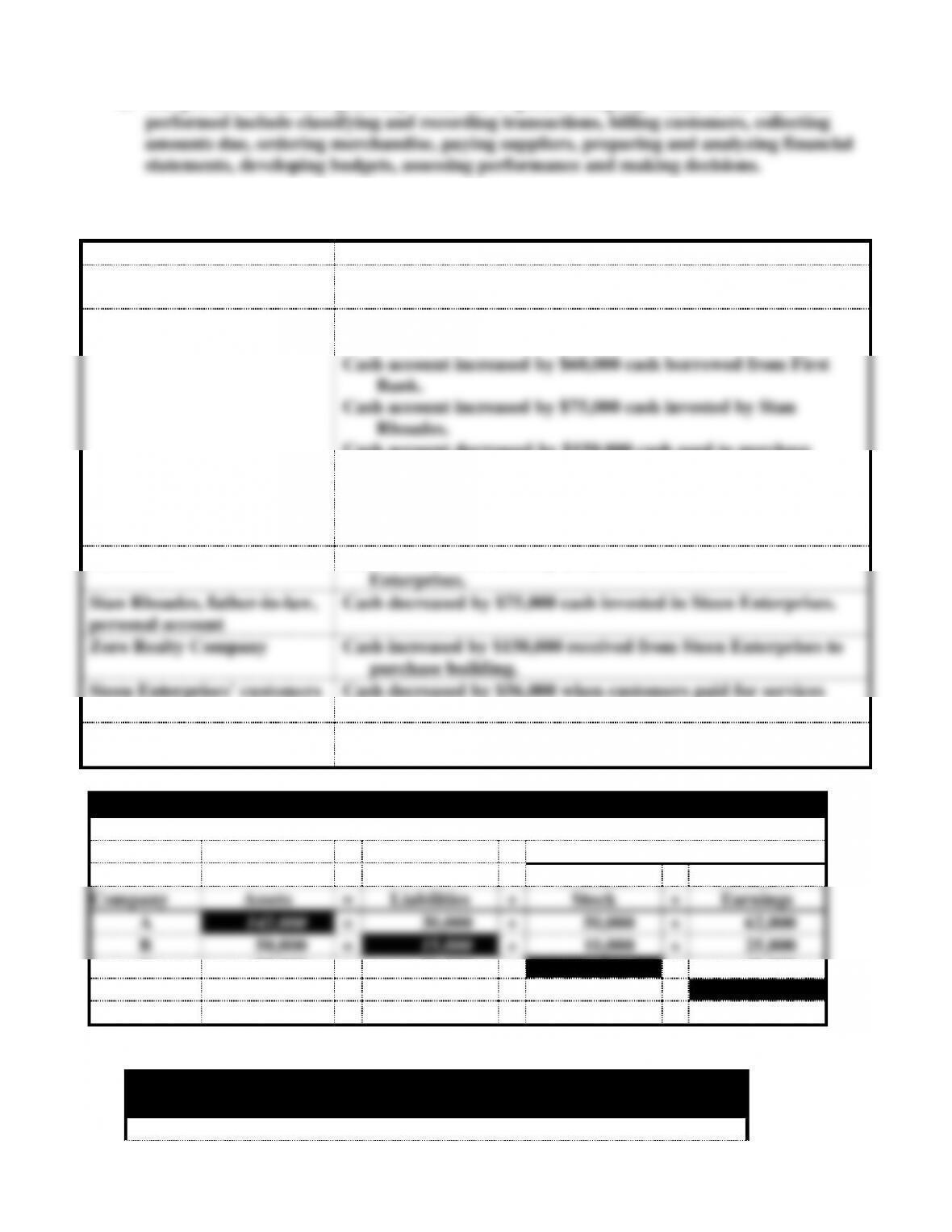

c. EXERCISE 1-3

Entities

Distribution of Cash

Ray Steen (personal account)

Personal account was decreased by the $100,000 cash deposited

in the Steen Enterprises’ business account.

Steen Enterprises

Cash account increased by the $100,000 cash deposited by Mr.

Steen.

Cash account increased by $60,000 cash borrowed from First

Bank.

Cash account increased by $75,000 cash invested by Stan

Rhoades.

Cash account decreased by $150,000 cash used to purchase

building.

Cash account increased by $56,000 cash revenue earned.

Cash account decreased by $31,000 cash payment to employees

for salaries.

First Bank

Cash account decreased by $60,000 cash loaned to Steen

Enterprises.

Stan Rhoades, father-in-law,

personal account

Cash decreased by $75,000 cash invested in Steen Enterprises.

Zoro Realty Company

Cash increased by $150,000 received from Steen Enterprises to

purchase building.

Steen Enterprises’ customers

Cash decreased by $56,000 when customers paid for services

performed.

Steen Enterprises’ employees

Cash increased by $31,000 when employees received payment for

salaries.

EXERCISE 1-4

Accounting Equation

Stockholders’ Equity

Common

Retained

Company

Assets

=

Liabilities

+

Stock

+

Earnings

A

142,000

=

30,000

+

50,000

+

62,000

B

50,000

=

15,000

+

10,000

+

25,000

C

85,000

=

20,000

+

25,000

+

40,000

D

215,000

=

60,000

+

100,000

+

55,000

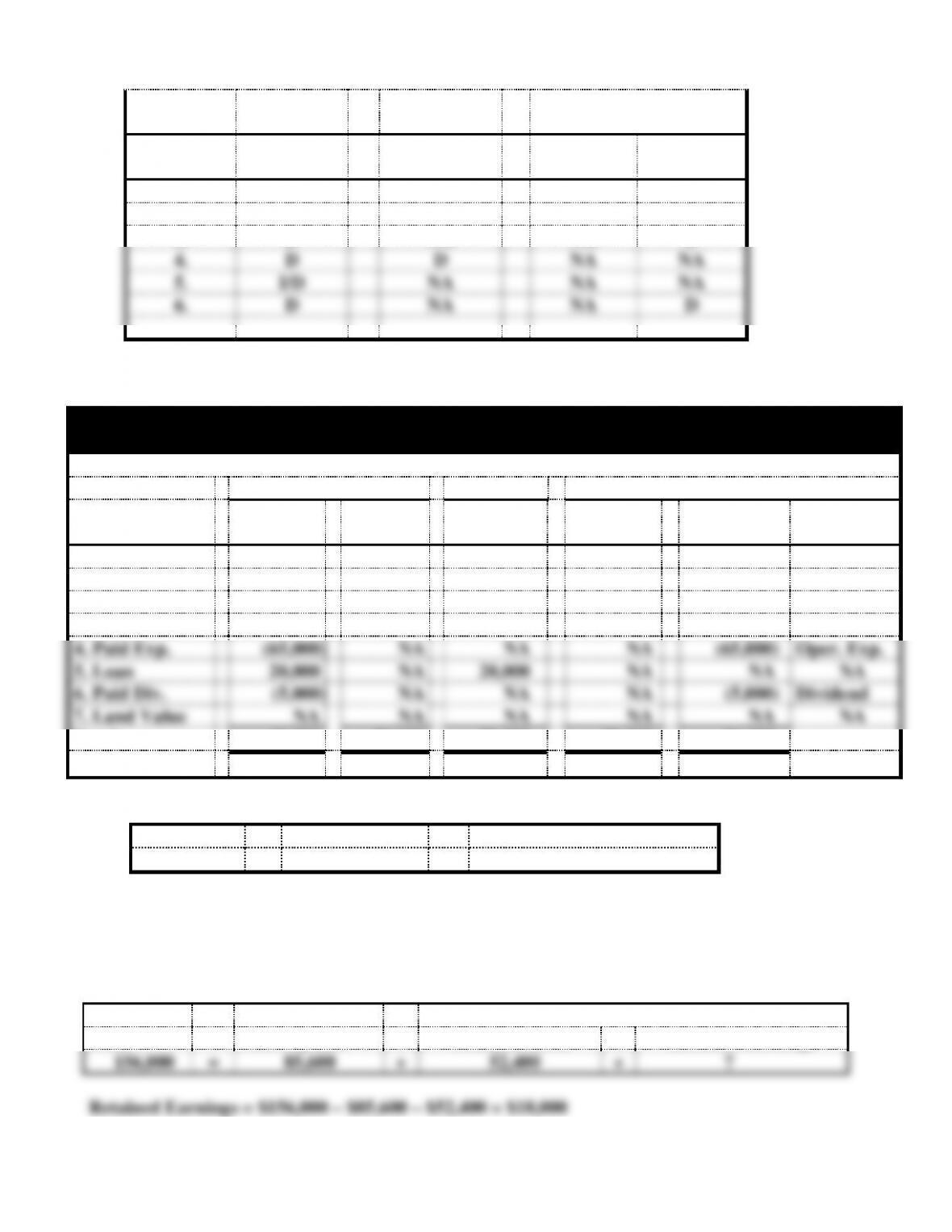

EXERCISE 1-5

1-13

Stockholders’

Equity

Event

Number

Assets

=

Liabilities

+

Common

Stock

Retained

Earnings

1.

I

NA

I

NA

2.

I

NA

NA

I

3.

D

NA

NA

D

4.

D

D

NA

NA

5.

I/D

NA

NA

NA

6.

D

NA

NA

D

EXERCISE 1-6

a.

Foster Corp.

Accounting Equation for 2014

Assets

=

Liabilities

+

Stockholders’ Equity

Event

Cash

+

Land

=

Notes

Payable

+

Com.

Stock

+

Retained

Earnings

Acct.

Title/RE

Bal. 1/1/13

30,000

16,000

10,000

20,000

16,000

1. Pur. Land

(20,000)

20,000

NA

NA

NA

NA

2. Issued stk.

10,000

NA

NA

10,000

NA

NA

3. Provide Svc.

90,000

NA

NA

NA

90,000

Revenue

4. Paid Exp.

(65,000)

NA

NA

NA

(65,000)

Oper. Exp.

5. Loan

20,000

NA

20,000

NA

NA

NA

6. Paid Div.

(5,000)

NA

NA

NA

(5,000)

Dividend

7. Land Value

NA

NA

NA

NA

NA

NA

Totals

60,000

+

36,000

=

30,000

+

30,000

+

36,000

Assets

=

Liabilities

+

Stockholders’ Equity

$96,000

=

$30,000

+

$66,000

d. The balances of total assets, liabilities and stockholders’ equity will be the same on

January 1, 2015 as the balances on December 31, 2014. (See b. above)

e. EXERCISE 1-7

a.

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

=

Note Payable

+

Common Stock

+

Retained Earnings

156,000

=

85,600

+

52,400

+

?

1-14

b. & c.

Post Company

Effect of 2014 Transactions on the Accounting Equation

Assets

=

Liabilities

+

Stockholders’ Equity

Notes

Common

Retained

Event

Cash

=

Payable

+

Stock

+

Earnings

Beginning Balances

156,000

85,600

52,400

18,000

1. Earned Revenue

36,000

NA

NA

36,000

2. Paid expenses

(20,000)

NA

NA

(20,000)

3. Paid dividend

(3,000)

NA

NA

(3,000)

Ending Balance

169,000

=

85,600

+

52,400

+

31,000

d.

Cash

=

Note Payable

+

Common Stock

+

Retained Earnings

169,000

=

85,600

+

52,400

+

31,000

Assets = Liabilities + Stockholders’ Equity

$169,000 = $169,000

f. The beginning and ending balances in the cash account were $156,000 and $169,000

respectively. The beginning balance in the common stock account was $52,400. This

g. EXERCISE 1-8

a.

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Notes Payable

Salaries Expense

Land

Accounts Payable

Common Stock

Office Furniture

Utilities Payable

Service Revenue

Trucks

Interest Expense

Supplies

Utilities Expense

Computers

Operating Expenses

Building

Rent Revenue

Dividends

Supplies Expense

Gasoline Expense

Retained Earnings

Dividends

1-15

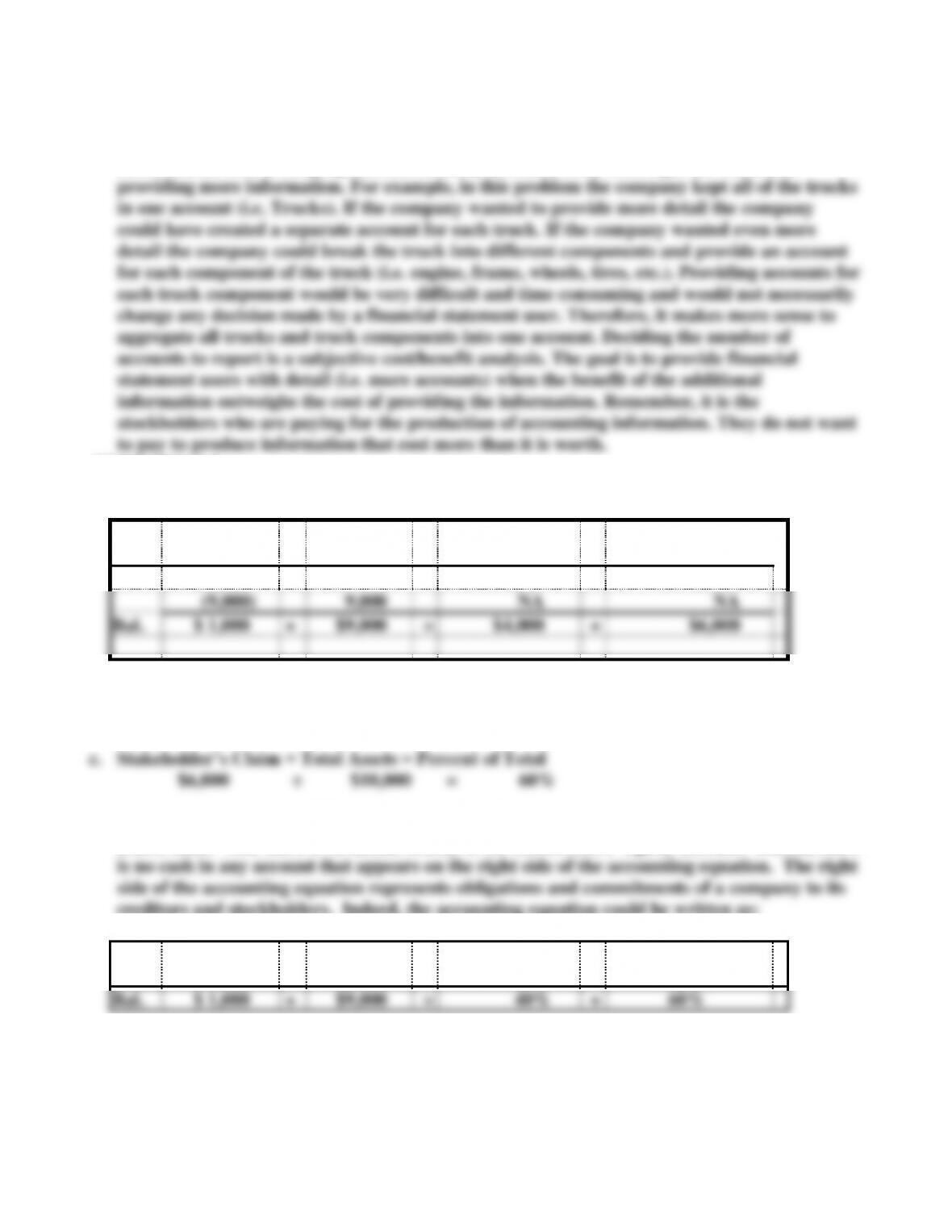

b. No. The number of accounts will vary depending on the level of detail the reporting entity

chooses to provide, as well as the type of company and industry in which it operates. More

accounts provide financial statement users with more information about the reporting entity.

However, the cost of keeping records on many accounts often outweighs the benefit of

EXERCISE 1-9

a.

Cash

+

Land

=

Creditors

+

Stockholders’

Equity

$10,000

$ -0-

$4,000

$6,000

(9,000)

9,000

NA

NA

Bal.

$ 1,000

+

$9,000

=

$4,000

+

$6,000

b. Creditor’s Claim ÷ Total Assets = Percent of Total

$4,000 ÷ $10,000 = 40%

d. The company cannot repay the debt. The company owes the creditors $4,000 but has only

$1,000 cash. Note there is no actual money in the stockholders’ equity account. Indeed, there

creditors and stockholders. Indeed, the accounting equation could be written as:

Cash

+

Land

=

Creditors

+

Stockholders’

Equity

Bal.

$ 1,000

+

$9,000

=

40%

+

60%

All assets including any cash balances are shown on the left side of the equation.

EXERCISE 1-10

1-16

a. Dividends are paid to investors. The investor has an ownership interest in the business

b. There is no cash in the Retained Earnings account. Retained Earnings represents the

c. The amount of dividends that can be paid are limited to retained earnings. In addition, a

d. If the total amount of the liability of $7,000 is due, GreyCo. will not be able to satisfy the

e. If the land becomes worthless, the only asset remaining is the cash of $800. Since

f. EXERCISE 1-11

a. Creditors receive their $400 interest payment, leaving $500 ($900 – $400) to be paid as

dividends to the investors.

b. Creditors receive their $400 interest payment, leaving $100 ($500 – $400) to be paid as

c. Creditors receive their $400 interest payment. No dividend is paid to investors. In this case

the recognition of the interest expense will cause the company to have an after interest

Note that these answers are based on the customary characteristics of interest and dividends. In