Chapter 10 – Management Accounting: A Value-added Discipline

Answers to questions

1. Financial accounting deals with regulated, historical, financial information that

pertains to the whole company and is designed primarily to meet the information

2. The value-added principle means that management accountants are free to engage in

any information gathering and reporting activity so long as the activity adds value in

3. Both financial and managerial accountants need cost information about the

company’s products and services. In managerial accounting, cost information is

useful in product pricing decisions and is an essential part of cost control (comparing

4. A cost that has the future economic potential to increase assets is recorded as an asset

5. The cash paid to production workers is not used to produce revenue but to produce

6. Product costs associated with goods that have not been sold are recorded in the

account called inventory. Inventory cost is shown on the balance sheet as an asset.

7. An indirect product cost is a cost that cannot be easily or economically traced to a

specific product. Product costs that would be considered indirect include costs such

8. Product costs are all costs incurred to obtain a product or provide a service. These

costs are treated as assets, recorded in inventory, and expensed when the associated

products are sold. Period costs are all costs not associated with a product. They are

9. The effects of cost classification on the financial statements can have important

implications for managers with respect to the following:

(1) Availability of financing – Investors and creditors use financial statement data

to predict businesses’ future earnings. Favorable financial statements provide

evidence of favorable future performance whereas unfavorable financial

statements are an indication of possible poor future financial performance. A

and equity, enhances businesses’ ability to obtain financing.

(2) Management motivation – Executive compensation may be affected by

financial statement data. Many managers’ bonuses are based on a percentage

(3) Income tax considerations – With respect to taxes, managers prefer to classify

10. Cost allocation is the process of dividing a total cost into parts and assigning the parts

to relevant cost objects. A production manager is usually in charge of the

11. Some of the more common ethical conflicts encountered by accountants include the

following:

12. A pricing decision must include all costs associated with the product. The

manufacturing product cost as well as all upstream costs (costs that occur before the

13. JIT inventory system is a reengineering principle where inventory is made available

for customer consumption at the time of customer demand. A JIT inventory system

eliminated.

14. The two dimensions of the TQM program are: (1) management should follow a

continuous, systematic problem solving philosophy that engages all employees to eliminate

15. Reengineering is the term used to explain companies’ responses to world-wide

companies by changing production and delivery systems so as to eliminate waste,

16. In recognition of its responsibility to uphold high ethical standards of conduct, the

Institute of Management Accountants issued a Statement of Ethical Professional

17. Activity-based management assesses the value chain of an organization’s business

18. A value chain is the sequence of activities through which an organization provides

19. A value-added activity is any unit of work that contributes to a product’s ability to

satisfy customer needs. Value-added activities include the following:

(1) Input activities – research and development, product design, and hiring and

training.

Nonvalue-added activities are tasks undertaken that do not contribute to a product’s

ability to satisfy customer needs. Examples would include the following:

Exercise 10-1

Managerial Accounting

Financial Accounting

a.

X

b.

X

c.

X

d.

X

e.

X

f.

X

g.

X

h.

X

i.

X

j.

X

Exercise 10-2

Product Cost

General, Selling, and

Administrative Cost

a.

X

b.

X

c.

X

d.

X

e.

X

f.

X

g.

X

h.

X

i.

X

j.

X

Exercise 10-3

Cost Category

Product /

GS&A

Asset /

Expense

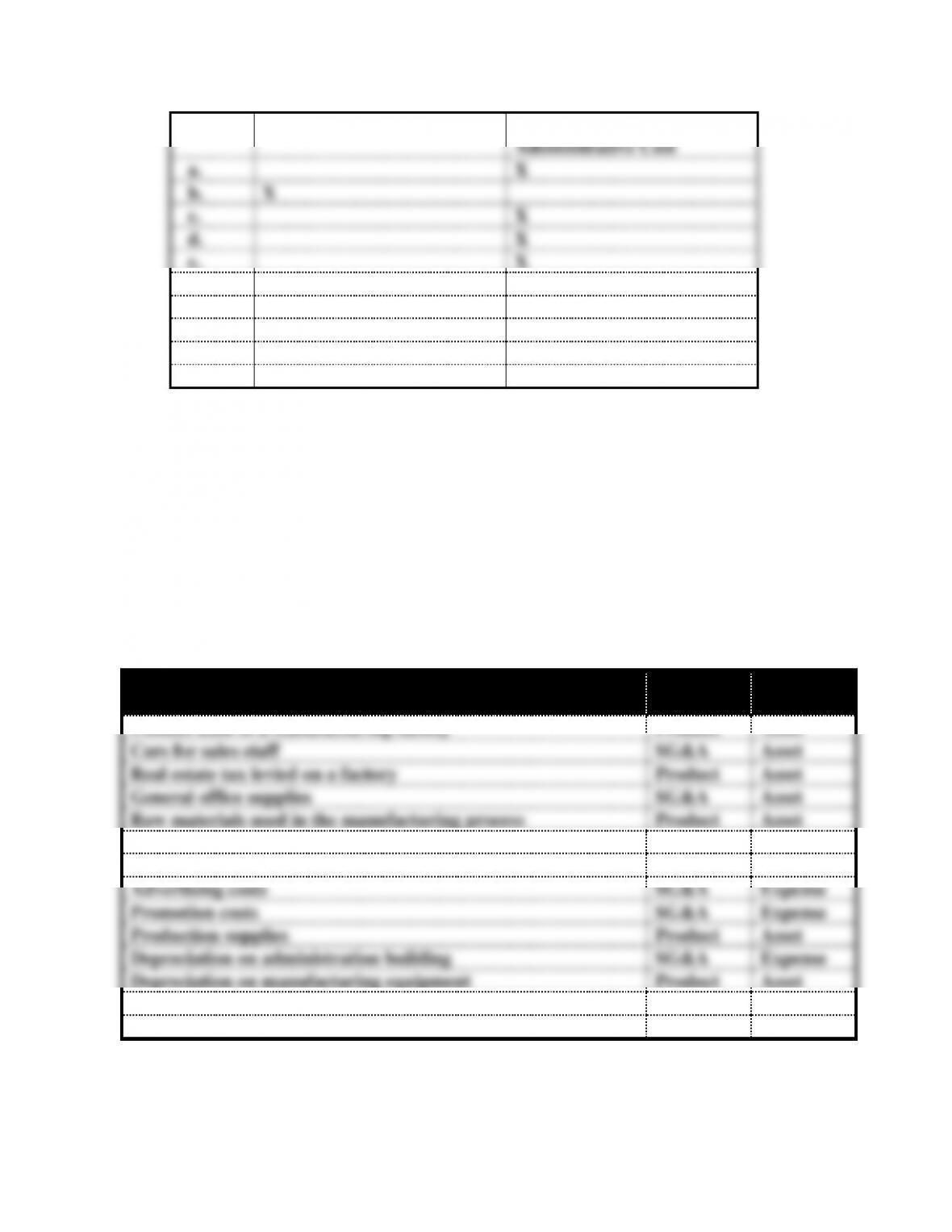

Utilities used in a manufacturing facility

Product

Asset

Cars for sales staff

SG&A

Asset

Real estate tax levied on a factory

Product

Asset

General office supplies

SG&A

Asset

Raw materials used in the manufacturing process

Product

Asset

Costs to rent office equipment

SG&A

Expense

Wages of production workers

Product

Asset

Advertising costs

SG&A

Expense

Promotion costs

SG&A

Expense

Production supplies

Product

Asset

Depreciation on administration building

SG&A

Expense

Depreciation on manufacturing equipment

Product

Asset

Research and development costs

SG&A

Expense

Cost to set up manufacturing equipment

Product

Asset

Exercise 10-4

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

1.

NA

+

–

NA

+

–

NA

2.

+

+

NA

NA

NA

NA

NA

Exercise 10-5

Assets

=

Equity

Event

Manuf.

Office

Com.

Ret.

No.

Cash

+

Inventory

+

Equip.

+

Furn.

=

Stk.

+

Earn.

Rev.

–

Exp.

=

Net Inc.

Cash Flow

1.

NA

NA

NA

D

NA

D

NA

I

D

NA

2.

NA

I

D

NA

NA

NA

NA

NA

NA

NA

Exercise 10-6

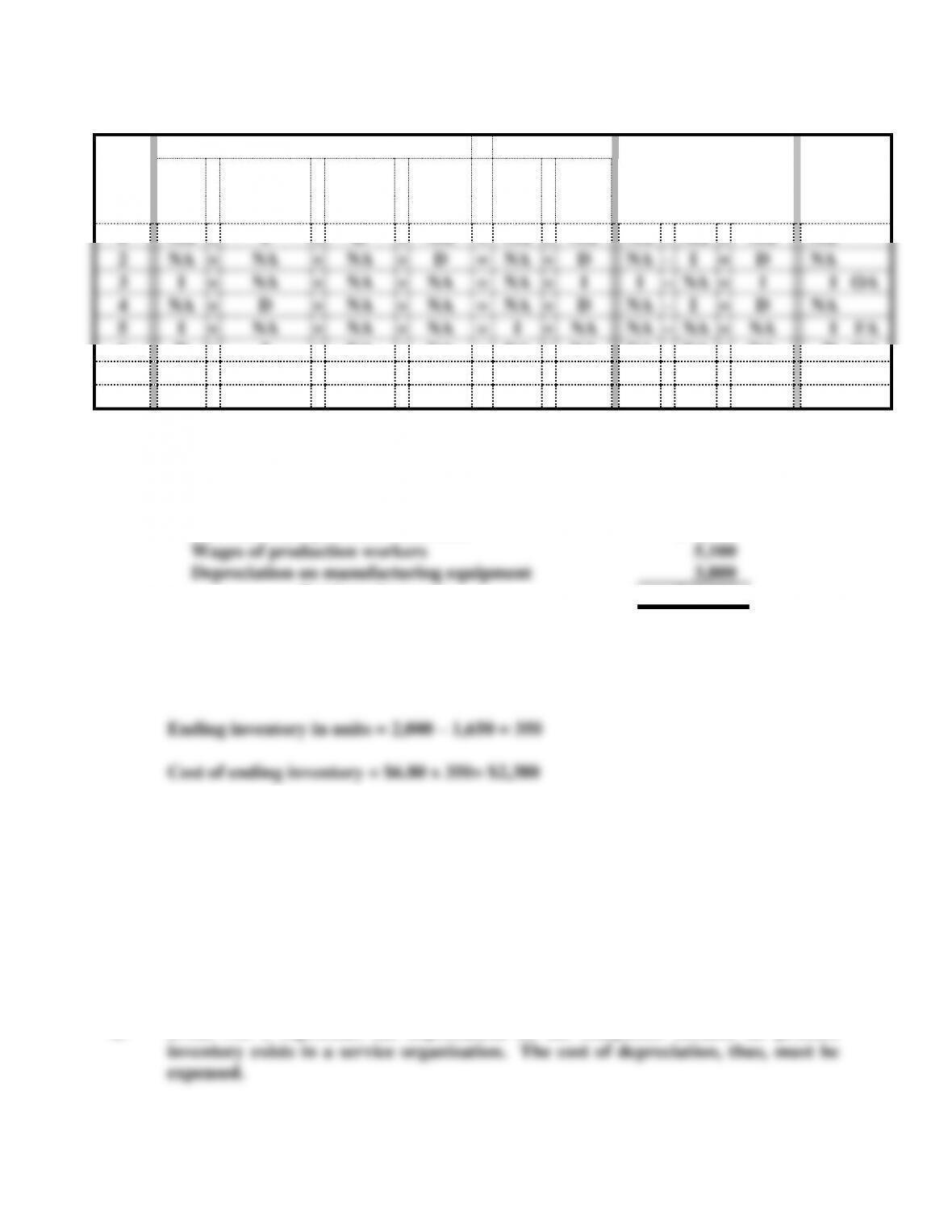

a. The three main components of product cost for a manufacturing entity are direct

materials, direct labor, and manufacturing overhead.

b. The product cost in a merchandising company, such as a retail toy store, is

relatively easy to determine. It includes vendor’s price charged on the invoice,

freight cost, and other necessary costs to make the inventory available for sale.

c. If each product is given a fixed amount of space for display, it is possible to use

the percentage of space occupied by each product to allocate the rental cost.

The salary of the store manager cannot be allocated to individual products easily,

Exercise 10-7

a. Payroll costs that would be classified as selling, general, and administrative

expense include the following:

Salary of the company president

$ 40,000

Salary of the chief financial officer

20,000

Salary of the vice president of marketing

18,000

Salaries of administrative secretaries

60,000

Commissions paid to sales staff

252,000

Total

$390,000

b. Payroll costs that would be classified as product cost include the following:

Salary of the vice president of manufacturing

$ 25,000

Salary of middle managers in manufacturing plant

196,000

Wages of production workers

938,000

Salaries of engineers and maintenance crew

178,000

Total

$1,337,000

Since 3,600 units of 4,000 finished products were sold, 90% (i.e. 3,600 ÷ 4,000) of

the product cost would be classified as cost of goods sold. Therefore, the payroll

cost that would be included in cost of goods sold is determined as follows:

Alternatrive computation for the same result follows :

Exercise 10-8

Assets

=

Equity

Event

Manuf.

Office

Cont.

Ret.

No.

Cash

+

Inventory

+

Equip.

+

Furn.

=

Cap.

+

Ear.

Rev.

–

Exp.

=

Net

Inc.

Cash Flow

1

NA

+

I

+

D

+

NA

=

NA

+

NA

NA

–

NA

=

NA

NA

2

NA

+

NA

+

NA

+

D

=

NA

+

D

NA

–

I

=

D

NA

3

I

+

NA

+

NA

+

NA

=

NA

+

I

I

–

NA

=

I

I OA

4

NA

+

D

+

NA

+

NA

=

NA

+

D

NA

–

I

=

D

NA

5

I

+

NA

+

NA

+

NA

=

I

+

NA

NA

–

NA

=

NA

I FA

6

D

+

I

+

NA

+

NA

=

NA

+

NA

NA

–

NA

=

NA

D OA

7

D

+

I

+

NA

+

NA

=

NA

+

NA

NA

–

NA

=

NA

D OA

8

D

+

NA

+

NA

+

NA

=

NA

+

D

NA

–

I

=

D

D OA

Exercise 10-9

a.

Raw materials purchased and used

$ 4,700

Wages of production workers

5,100

Depreciation on manufacturing equipment

3,800

Total product cost

$13,600

b.

Cost of inventory per unit = $13,600 ÷ 2,000 = $6.80

c.

Cost of goods sold = $6.80 x 1,650 = $11,220

Exercise 10-10

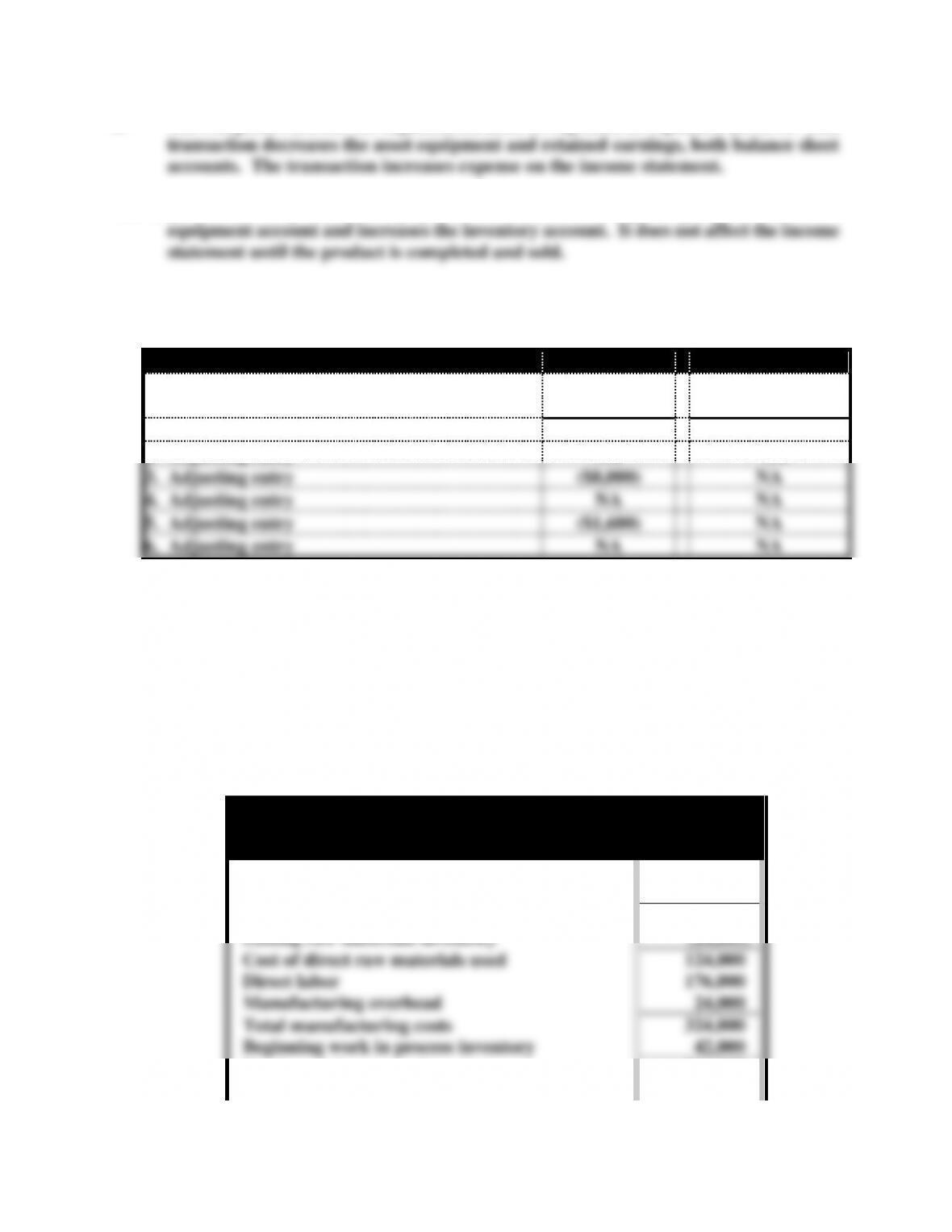

a. Event No. 1 represents the depreciation on the computers because no product

b. The computers in a service organization must be expensed as explained in Part a. This

The depreciation on production equipment in a manufacturing company decreases the

Exercise 10-11

Net Income

Cash Flow

Event No.

Amount of

Change

Amount of Change

1. Adjusting entry

($5,000)

NA

2. Adjusting entry

NA

NA

3. Adjusting entry

($8,000)

NA

4. Adjusting entry

NA

NA

5. Adjusting entry

($1,600)

NA

6. Adjusting entry

NA

NA

Exercise 10-12

Fischer Corporation

Schedule of Cost of Goods Manufactured

For the Year Ended December 31, 2014

Beginning raw materials inventory

$ 28,000

Purchases

120,000

Raw materials available

148,000

Ending raw materials inventory

(24,000)

Cost of direct raw materials used

124,000

Direct labor

176,000

Manufacturing overhead

24,000

Total manufacturing costs

324,000

Beginning work in process inventory

42,000

Total work in process inventory

366,000

Ending work in process inventory

(46,000)

Cost of goods manufactured

$320,000

Exercise 10-13

a.

Flaxman Manufacturing Company

Schedule of Cost of Goods Manufactured and Sold

For March 2015

Beginning raw materials inventory

$100,000

Purchases

120,000

Raw materials available for Use

220,000

Ending raw materials inventory

(60,000)

Direct raw materials used

160,000

Direct labor

100,000

Overhead (actual)

63,000

Total manufacturing costs

323,000

Beginning WIP inventory

120,000

Total WIP inventory

443,000

Ending WIP inventory

(145,000)

Cost of goods manufactured

298,000

Beginning finish. goods inventory

78,000

Cost of goods available for sale

376,000

Less ending finished goods inventory

(80,000)

Cost of goods sold

$296,000

b. Sales revenues $380,000

Exercise 10-14

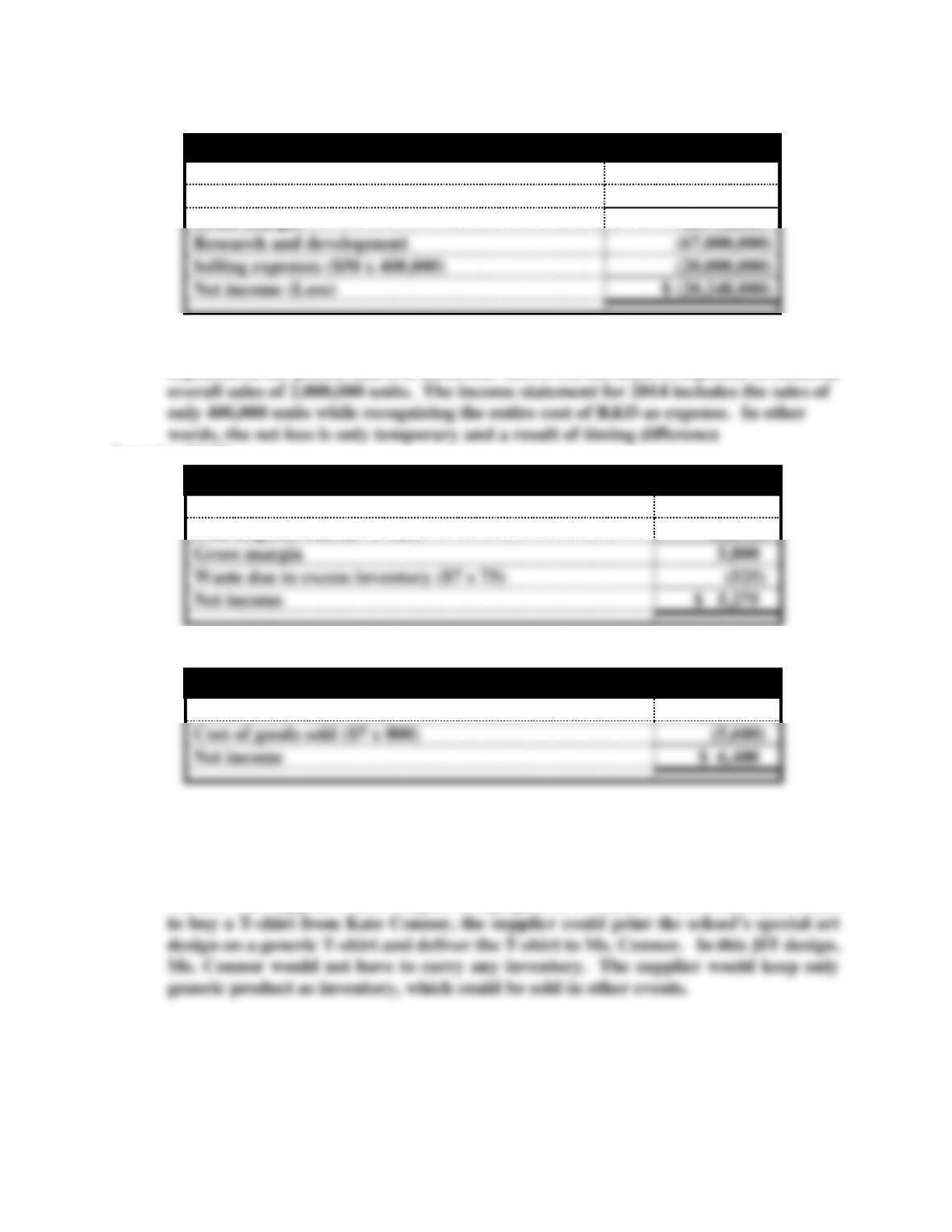

a. The $67,000,000 of research and development cost is an upstream cost while

packaging, shipping, and sales commissions are downstream costs.

b. Cost of goods sold: $250 x 400,000 = $100,000,000

Ending inventory: $250 x 40,000 = $10,000,00

Upstream cost per unit, $67,000,000 ÷ 2,000,000

$ 33.50

Manufacturing cost per unit

250.00

Downstream costs per unit

50.00

Total cost

333.50

Plus: 25% profit margin, $333.50 x 25%

83.38*

Price

$416.88

d.

Income Statement

Sales revenue ($416.88 X 400,000)

$ 166,752,000

Cost of goods sold

(100,000,000)

Gross margin

66,752,000

Research and development

(67,000,000)

Selling expenses ($50 x 400,000)

(20,000,000)

Net income (Loss)

$ (20,248,000)

e. The upstream cost of research and development is required by GAAP to be

expensed in the period that it is incurred. However, the R&D is expected to result in

Exercise 10-15

Income Statement

Sales revenue ($15 x 725)

$ 10,875

Cost of goods sold ($7 x 725)

(5,075)

Gross margin

5,800

Waste due to excess inventory ($7 x 75)

(525)

Net income

$ 5,275

b.

Income Statement

Sales revenue ($15 x 800)

$12,000

Cost of goods sold ($7 x 800)

(5,600)

Net income

$ 6,400

The opportunity cost of lost profit: ($15 – $7) x 25 = $200

c. If Ms. Connor can arrange an effective JIT system, the T-shirts would be delivered

by the supplier just in time for customers to purchase. To give an example of such a

system, assume that the supplier sets up a simple T-shirt printing facility at Meadow

School. The supplier could bring in enough generic T-shirts. When a customer wants