Chapter 13 Financial Statement Analysis

9-1

The remaining figures can only be found by using the debt to assets ratio of 40% times total

assets to determine total liabilities (0.40 x $675,000 = $270,000.) From this the remaining

figures fall into place.

Problem 9-21

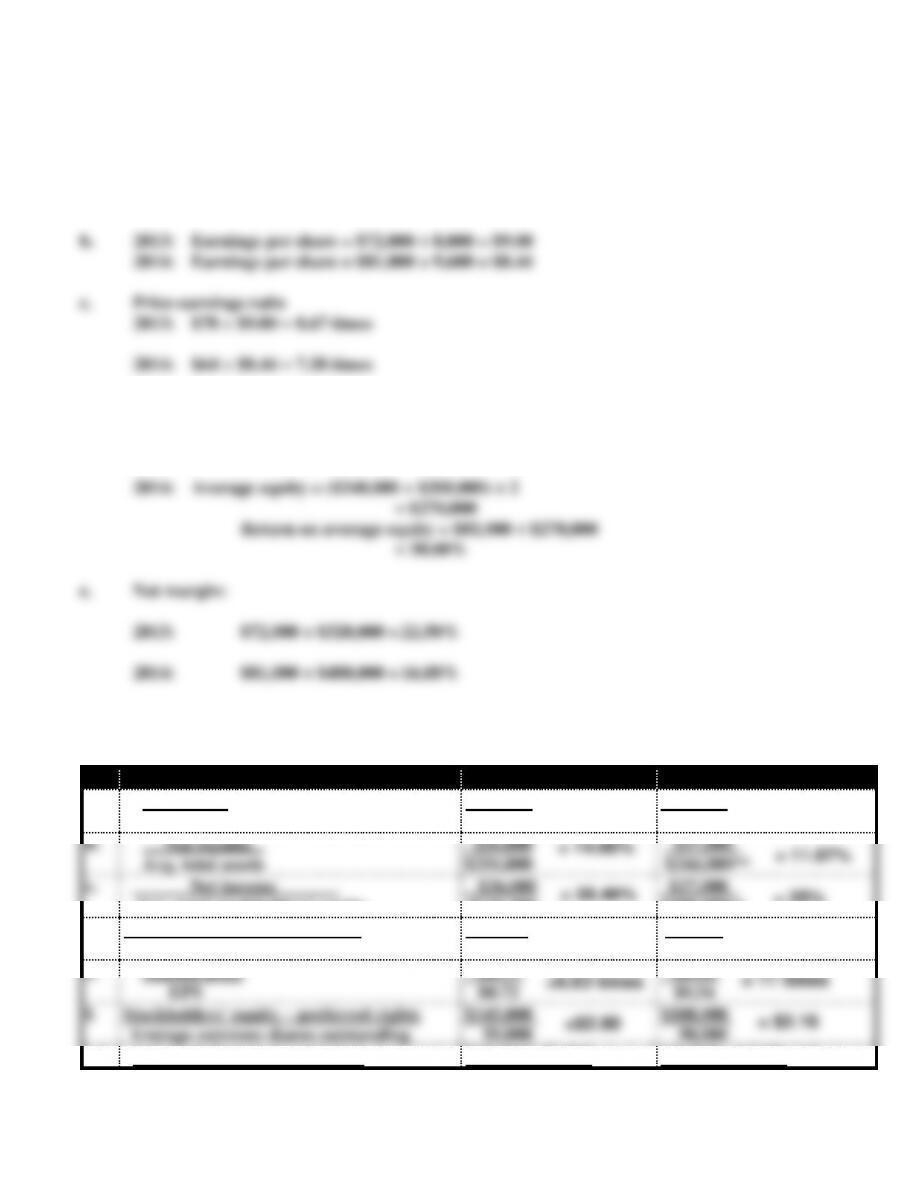

a. Earnings per share:

$195,600 – $22,800*

———————————— = $4 per share

43,200**

b. From this information only, investors should be cautious about buying Putin’s stock.

These three ratios provide mixed results in comparison with other companies in the

2

9-2

Problem 9-22

a. Times interest earned

2013: $98,000 ÷ $8,000 = 12.25 times

2014: $120,000 ÷ $9,000 = 13.33 times

d. 2013: Average equity = ($200,000+$240,000)÷2 =$220,000

Return on average equity = $72,000 ÷ $220,000

= 32.73%

Problem 9-23

2015

2014

a.

Net income

Net sales

$36,000

$210,000

$27,000

$175,000

b.

Net income

Avg. total assets

$36,000

$256,000

$27,000

$244,000**

c.

Net income

Avg. total stockholders’ equity

$36,000

$126,500

$27,000

$108,000**

d.

Net income

Avg. common shares outstanding

$36,000

50,000

$27,000

50,000

e.

Market price

EPS

$4.77

$0.72

$5.94

$0.54

f.

Stockholders’ equity – preferred rights

Average common shares outstanding

$145,000

50,000

$108,000

50,000

g.*

Income before taxes + Interest

$53,000*+$3,000

$45,000 + $3,000

= 17.14%

= 15.43%

= 28.46%

= 11.07%

= 14.06%

= 25%

= $0.72

= $0.54

=6.63 times

= 11 times

=$2.90

= $2.16

= 18.67

times

= 16

times

3

9-3

Interest

$3,000

$ 3,000

h.

Current assets – Current liabilities

$143,000 – $57,000

= $86,000

$139,000 – $69,000

= $70,000

i.

Current assets

Current liabilities

$143,000

$57,000

$139,000

$69,000

j.

Quick assets

Current liabilities

$40,000

$57,000

$41,000

$69,000

k.

Net sales

Average accounts receivable

$210,000

$33,500

$175,000

$32,000**

l.

Cost of goods sold

Average inventory

$126,000

$98,000

$103,000

$96,000**

m.

Total liabilities

Total stockholders’ equity

$123,000

$145,000

$136,000

$108,000

n.

Total liabilities

Total assets

$123,000

$268,000

$136,000

$244,000

* Note that the computation omits extraordinary items. This practice is logical because, by

definition, extraordinary items cannot be expected to recur and, therefore, will not be

available to satisfy future interest payments.

**Averages cannot be computed from the data provided in the problem.

= 2.51:1

= 2.01 : 1

= 0.70:1

=0.59 : 1

= 6.27

times

=5.47

times

= 1.29

times

=1.07

times

= 0.85:1

=1.26:1

=46%

= 56%

4

9-4

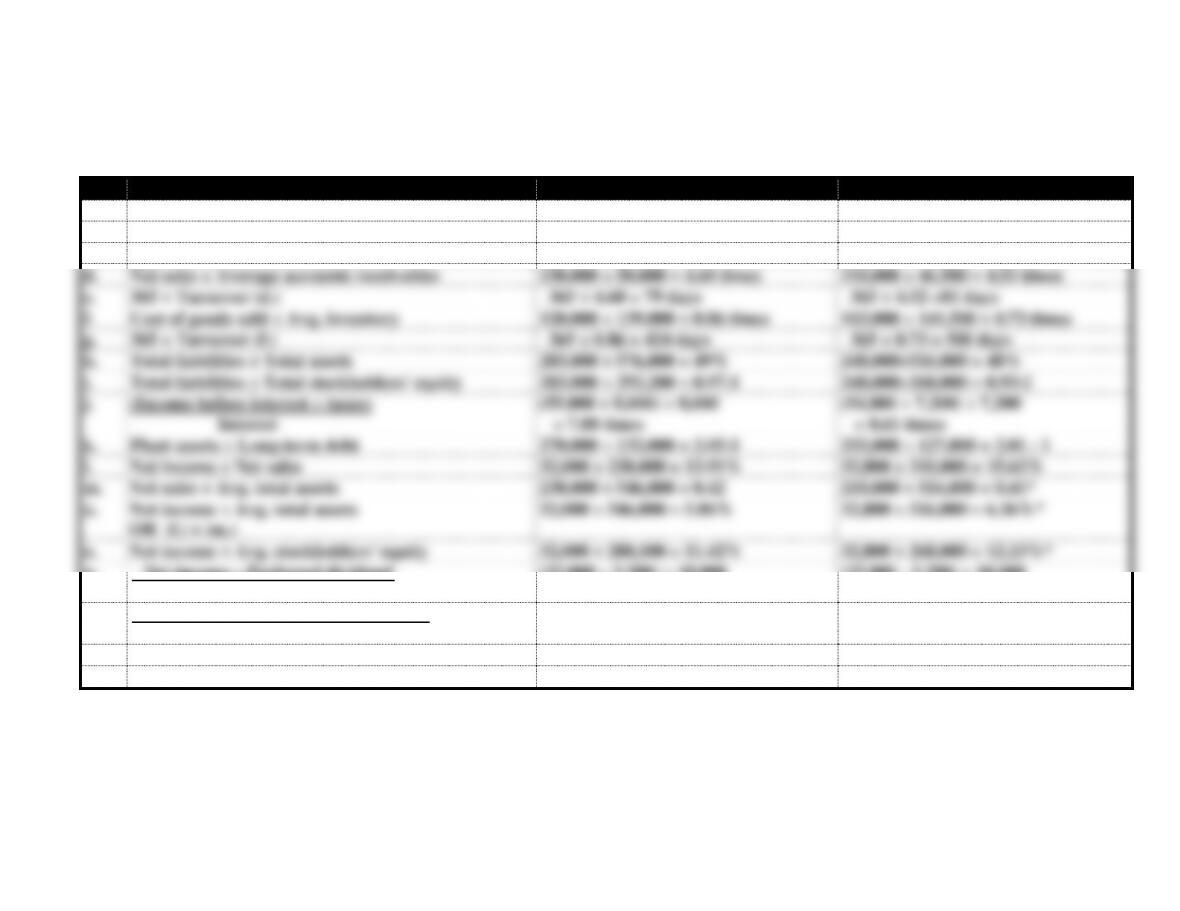

Problem 9-24

Because of space limitation, $ signs are omitted in these computations.

2015

2014

a.

Current assets – Current liabilities

250,000 – 151,800 = 98,200

217,000 – 121,000 = 96,000

b.

Current assets ÷ Current liabilities

250,000 ÷ 151,800 = 1.65 : 1

217,000 ÷ 121,000 = 1.79 : 1

c.

Quick assets ÷ Current liabilities

90,000 ÷ 151,800 = 0.59 : 1

64,000 ÷ 121,000 = 0.53 : 1

d.

Net sales ÷ Average accounts receivables

230,000 ÷ 50,000 = 4.60 times

210,000 ÷ 46,500 = 4.52 times

e.

365 ÷ Turnover (d.)

365 ÷ 4.60 = 79 days

365 ÷ 4.52 =81 days

f.

Cost of goods sold ÷ Avg. inventory

120,000 ÷ 139,000 = 0.86 times

103,000 ÷ 141,500 = 0.73 times

g.

365 ÷ Turnover (f.)

365 ÷ 0.86 = 424 days

365 ÷ 0.73 = 500 days

h.

Total liabilities ÷ Total assets

283,800 ÷ 576,000 = 49%

248,000÷516,000 = 48%

i.

Total liabilities ÷ Total stockholders’ equity

283,800 ÷ 292,200 = 0.97:1

248,000÷268,000 = 0.93:1

j.

(Income before interest + taxes)

Interest

(55,000 + 8,000) ÷ 8,000

= 7.88 times

(54,800 + 7,200) ÷ 7,200

= 8.61 times

k.

Plant assets ÷ Long-term debt

270,000 ÷ 132,000 = 2.05:1

255,000 ÷ 127,000 = 2.01 : 1

l.

Net income ÷ Net sales

32,000 ÷ 230,000 = 13.91%

32,800 ÷ 210,000 = 15.62%

m.

Net sales ÷ Avg. total assets

230,000 ÷ 546,000 = 0.42

210,000 ÷ 516,000 = 0.41*

n.

Net income ÷ Avg. total assets

OR (l.) x (m.)

32,000 ÷ 546,000 = 5.86%

32,800 ÷ 516,000 = 6.36%*

o.

Net income ÷ Avg. stockholders’ equity

32,000 ÷ 280,100 = 11.42%

32,800 ÷ 268,000 = 12.23%*

p.

Net income – Preferred dividend

Avg. common shares outstanding

(32,000 – 3,200) ÷ 10,000

= $2.88 per share

(32,800 – 3,200) ÷ 10,000

= $2.96 per Share

q.

Stockholders’ equity – Preferred rights

Avg. common shares outstanding

(292,200 – 80,000) ÷ 10,000

= $21.22 per Share

(268,000 – 80,000) ÷ 10,000

= $18.80 per Share

r.

Market price ÷ EPS

12.50 ÷ 2.88 = 4.34

11.75 ÷ 2.96 = 3.97

s.

Dividends per share ÷ Market price

0.46 ÷ 12.50 = 3.68 %

0.46 ÷11.75 = 3.91%

*Averages cannot be computed from the data provided in the problem.

5

9-5

ATC 9-1

a. Compute the following ratios for 2012 for the companies’ fiscal years:

1. Current ratio

2. Average days to sell inventory (Use average inventory.)

1st, compute average inventory:

Costco: ($ 7,096+ $ 6,638) ÷ 2 = $ 6,867

Wal-Mart: ($40,714+ $36,318) ÷ 2 = $38,516

3. Debt to assets ratio

Costco: $ 14,622 ÷ $ 27,140 = 54%

4. Return on investment (Use average assets and use “earnings from continuing

operations – before taxes” rather than “net earnings.”)

1st, compute average assets: (Also used for ratio 6.)

Costco: ($ 27,140 + $ 26,761) ÷ 2 = $ 26,951

Wal-Mart: ($193,406 + $180,663) ÷ 2 = $187,035

6

9-6

ATC 9-1 (continued)

6. Asset turnover (Use average assets.)

7. Return on sales (Use “earnings from continuing operations–before taxes” rather than

“net earnings.”)

8. Plant assets to long-term debt ratio

Costco: $ 12,961 ÷ $ 2,362 = 5.5 to 1

Wal-Mart: $112,324 ÷ $55,345 = 2.0 to 1

b. The ratios above that are most relevant to determining profitability are:

Return on investment (Wal-Mart is better.)

Return on sales (Wal-Mart is better.)

d. The ratio above that are most relevant to determining which company is charging the

most for its goods is the gross margin percentage. Wal-Mart’s is significantly higher than

e. The ratios above that are most relevant to determining how efficiently assets are being

used are:

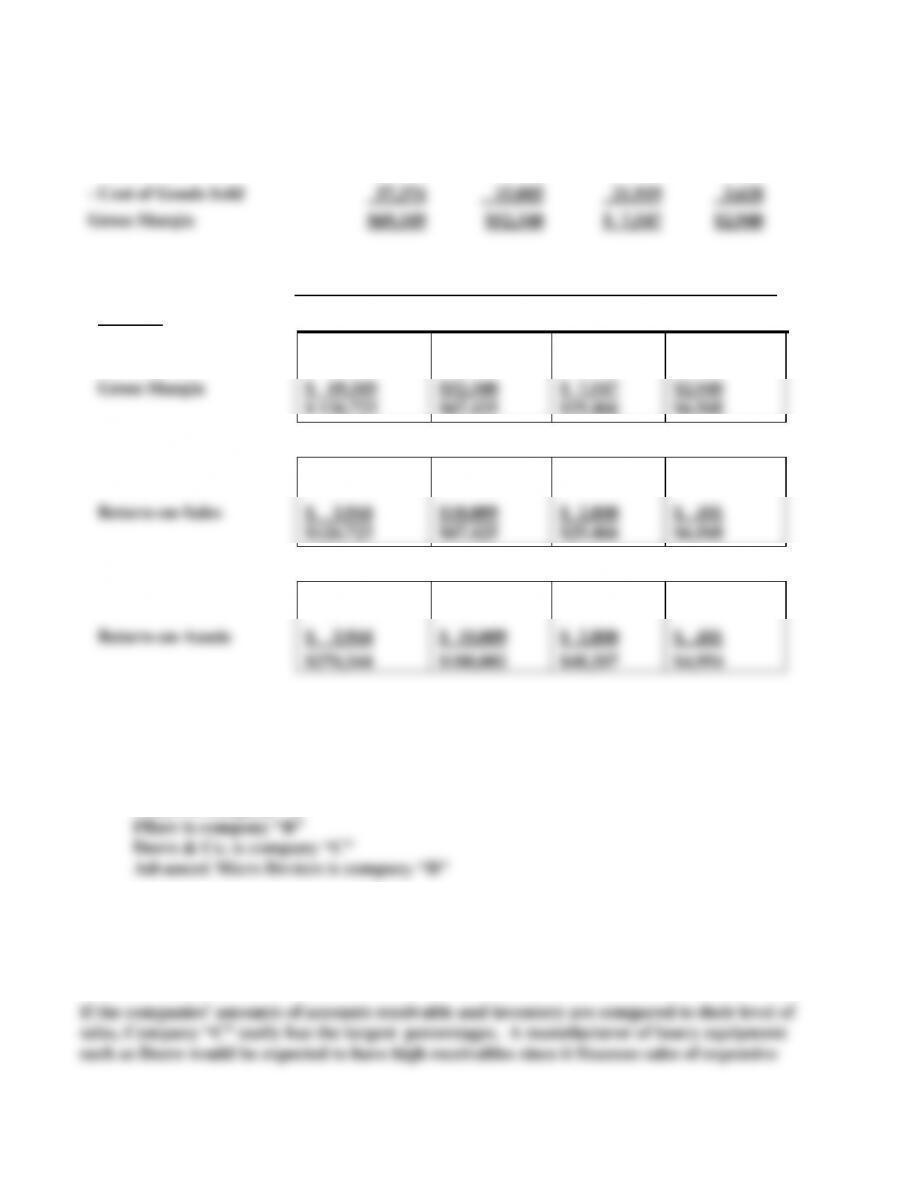

ATC 9-2

The correct matching of the four companies with their related financial data can be achieved

7

9-7

A

B

C

D

Sales

$126,723

$67,425

$29,466

$6,568

– Cost of Goods Sold

57,374

15,085

21,919

3,628

Gross Margin

$69,349

$52,340

$ 7,547

$2,940

Company

RATIO:

A

B

C

D

54.7% =

77.6% =

25.6% =

44.8% =

Gross Margin

$ 69,349

$52,340

$ 7,547

$2,940

$ 126,723

$67,425

$29,466

$6,568

3.1% =

14.8% =

9.5% =

7.5% =

Return-on-Sales

$ 3,944

$10,009

$ 2,800

$ 491

$126,723

$67,425

$29,466

$6,568

1.5% =

5.3% =

5.8% =

9.9% =

Return-on-Assets

$ 3,944

$ 10,009

$ 2,800

$ 491

$270,344

$188,002

$48,207

$4,954

ATC 9-2 (continued)

The four companies relate to the financial information as follows:

AT&T is company “A”

Rationale for matching companies with financial information:

Only company “A” reports -0- inventory. Of the four choices, a telecommunications company is

the most likely to carry little or no inventory. Therefore, AT&T is company “A.”

8

9-8

equipment, as well as lots of inventory compared to sales since heavy equipment does not sell as

quickly as drugs or microchips.

devices. It is a bit interesting that while Pfizer has higher gross margin and return on sales

percentages, Advanced Micro Devices has the better return on assets percentage.

ATC 9-3

a.

2011

2007

Sales

$39,046

$14,430

– Cost of goods sold

16,634

5,936

Gross margin

22,412

8,494

÷ Sales

39,046

14,430

= Gross margin

57.4%

58.9%

2011

2007

Net earnings

$ 7,959

$ 3,048

÷ Sales

39,046

14,430

= Net margin

20.4%

21.1%

2011

2007

Net earnings

$ 7,959

$ 3,048

÷ Assets

112,427

28,699

= Return on investment

7.1%

10.6%

2011

2007

Net earnings

$ 7,959

$ 3,048

÷ Total stockholders’ equity

41,044

14,910

= Return on equity

19.4%

20.4%

9

9-9

ATC 9-3 (continued)

2011

2007

Current assets

$12,323

$5,539

÷ Current liabilities

19,644

6,685

= Current ratio

0.63

0.83

2011

2007

Compute total liabilities:

Total liabilities &

stockholders’ equity

$112,427

$28,699

– Total stockholders’ equity

41,044

14,910

= Total liabilities

$71,383

$13,789

Total liabilities

$ 71,383

$13,789

÷ Total assets

112,427

28,699

= Debt to assets ratio

0.63

0.48

b. All of the ratios were worse in 2011 than they were in 2007, although they were still very

c. InBev’s performance has obviously declined during the three years since it merged with

ATC 9-4

The companies and the set of ratios to which each relates are as follows:

Caterpillar Company 4

Students can probably identify Denny’s as being either Company 1 or Company 2 based on the

relatively short time it takes these companies to sell their inventory. Obviously a restaurant would

not want its inventory sitting around very long. The fact that Company 2 takes the shortest time

to sell its inventory, coupled with the fact that it takes less time to collect its accounts receivables

10

9-10

1 and 3, including, “average days to sell inventory,” “sales per employee,” “current assets as a

percentage of total assets, and “asset turnover” ratios. Most students should be able to deduce that

a brewery would have more of its assets tied up in long-term assets and less in current assets than

a service company such as W-W. This should lead them to identify Company 3 as M-C, leaving

Company 1 as W-W.

that the delivery truck drivers are employees of the distributor, not the brewer.

ATC 9-5

a. Writing off the trucks would make the asset base smaller and thereby cause the return on

assets ratio to be higher.

growth in assets and income to be higher.

c. Ms. Talbot may not be a member of the Institute of Management Accountants and

therefore may not be bound by the organization’s ethical standards. However, her action

is unethical whether or not she is a member of the Institute. If she is bound by those ethical

d. Ms. Talbot and Mr. Winston have the pressure of showing their stockholders good

financial results of Kolla Waste Disposal Corporation. Because this year’s performance is

already very bad, Ms. Talbot is thinking about charging more of future expenses to the

9-11