Answers to Questions

1. Information that is relevant for decision making differs between the alternatives

and is future oriented.

2. A variable cost may or may not be relevant. The fact that a cost is variable has

no bearing on its relevance. For instance, the cost of direct labor is usually

3. Costs can be classified into the following levels:

(1) Unit-level costs – Costs that are incurred each time a company makes a product

or performs a service. These costs can be avoided by eliminating the

production of a single unit of product or service.

(3) Product-level costs – Costs that are incurred to support specific kinds of

products or services. Product-level costs are eliminated when the product

line is discontinued.

4. Information does not have to be entirely accurate to be relevant for decision

making. Knowing that a future cost can be avoided makes the cost relevant even

5. The conclusion is invalid because it fails to consider the importance of qualitative

6. The president appears to be overlooking the concept of a sunk cost. His company

has already incurred a $50,000 loss. The fact that it has not recognized the loss

borrowing the funds.

7. An opportunity cost is the sacrifice of some benefit (revenues, cost savings) that is

given up by not choosing an alternative. Opportunity costs are relevant in

8. The checking account is not truly free. There is an opportunity cost associated

9. The original costs of the two machines represent sunk costs and should not be

10. Some fixed costs are avoidable. For example advertising costs may be fixed

to the decision under consideration.

11. Numerous qualitative characteristics could apply to special order decisions. Two

specific considerations are: (1) the effects on regular customers who may learn

12. The allocated depreciation, warehousing costs, and property taxes will be the

13. The two factors that should be considered in allocating shelf space are per unit

contribution margin and turnover.

14. The relevant costs are the additional costs that will be incurred as a result of

necessary to fill the special order batch.

15. It may be possible for a company to purchase a product or service at a price below

16. If the fixed costs that Ms. Meyers is referring to are avoidable fixed costs,

17. Qualitative factors that should be considered include: (1) the availability of

reliable suppliers that can comply with quality standards and delivery schedules,

(2) the possibility of low-ball pricing where the supplier accepts a low price for the

18. While it may appear from the segment’s reports that it is operating at a loss, this

is not necessarily the case. When a segment is eliminated, some of the costs

assigned to that segment may still continue. Some of the facility-level costs that

19. Replacing the old machine could result in lower operating income in the first year

of the replacement if the old machine is sold at a loss. The loss would affect

Exercise 13-1

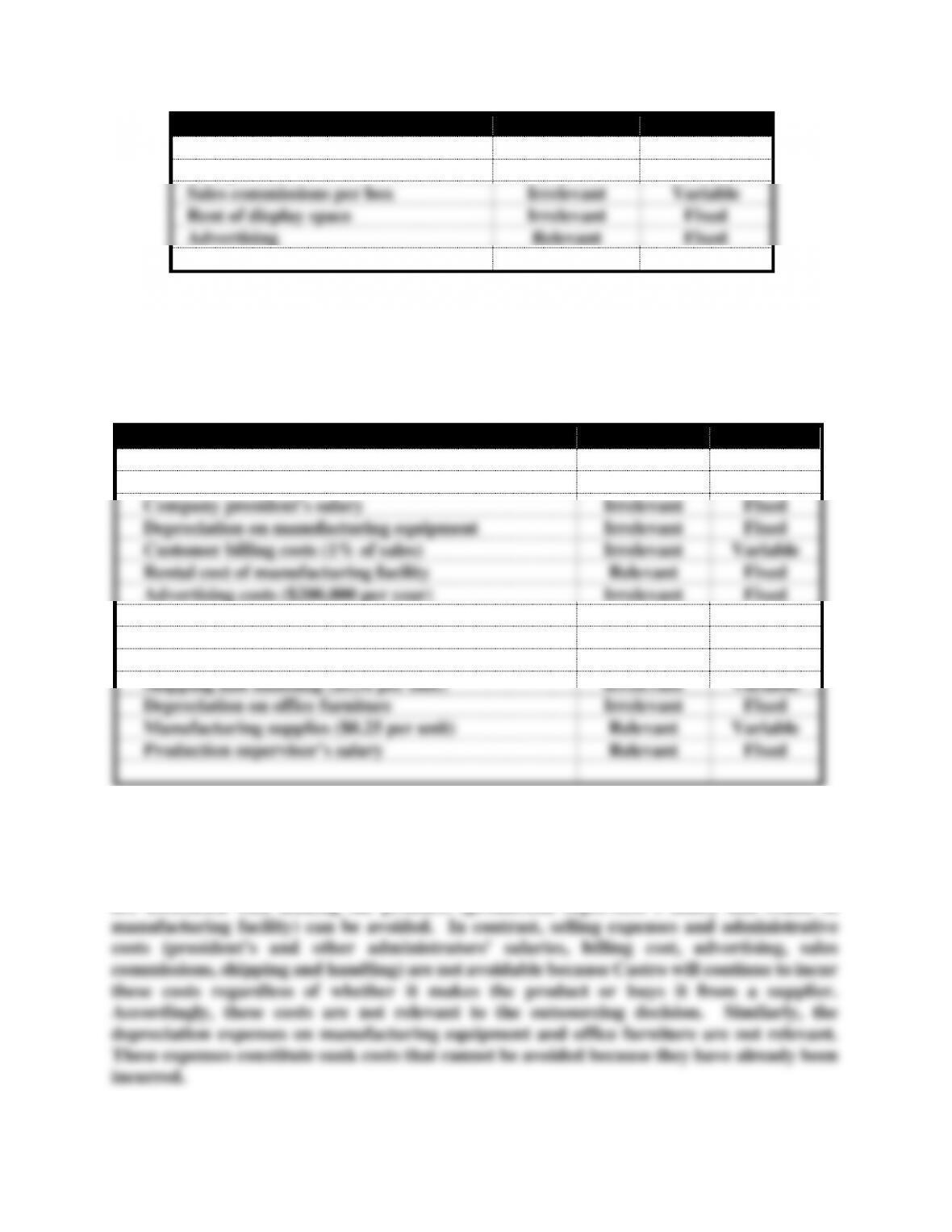

Cost Item

Relevance

Behavior

Cost per box

Relevant

Variable

Sales commissions per box

Irrelevant

Variable

Rent of display space

Irrelevant

Fixed

Advertising

Relevant

Fixed

Since sales commissions per box and the rental cost do not differ between the

alternatives, they cannot be avoided regardless of which alternative is chosen.

Accordingly, these costs are not relevant.

Exercise 13-2

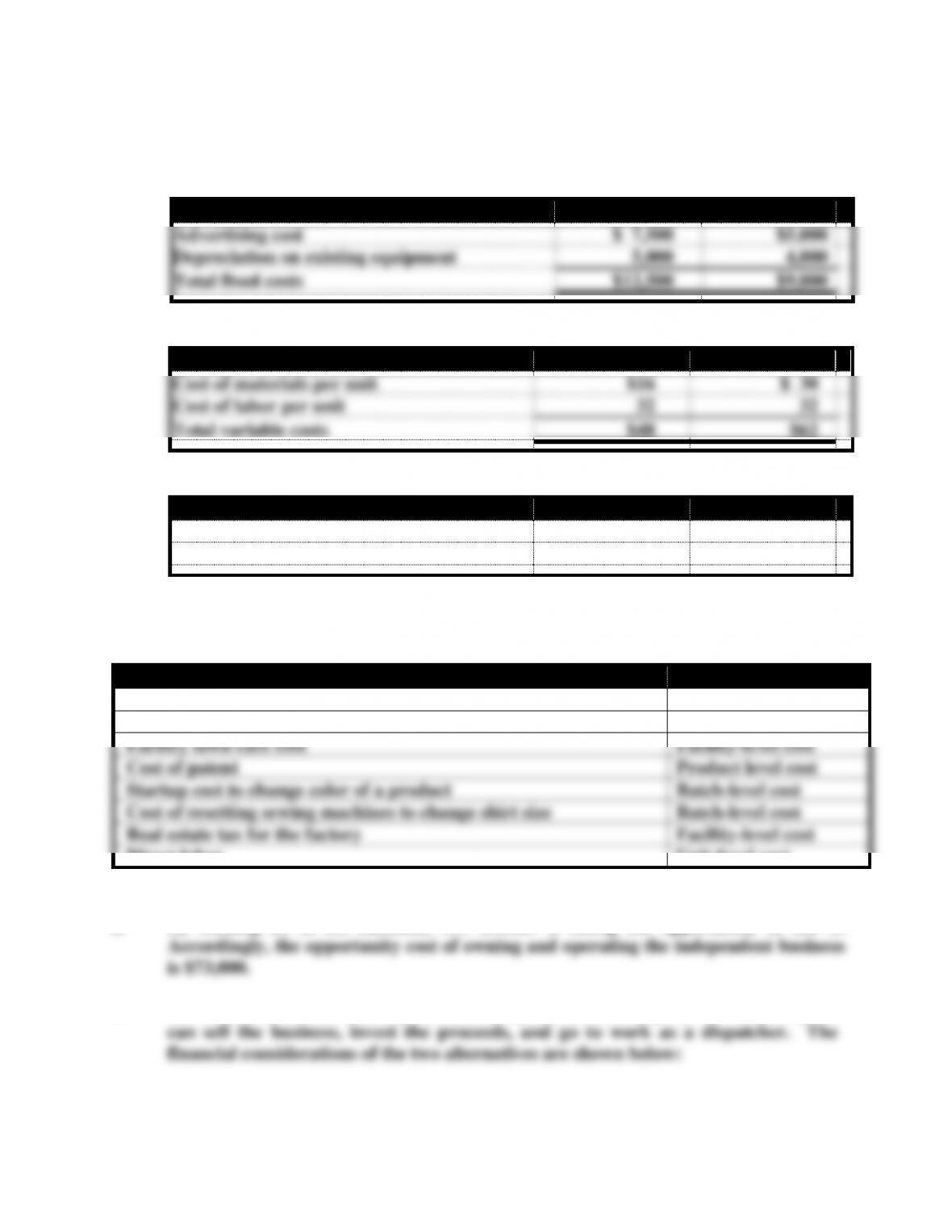

Cost Items

Relevance

Behavior

Materials cost ($9 per unit)

Relevant

Variable

Company president’s salary

Irrelevant

Fixed

Depreciation on manufacturing equipment

Irrelevant

Fixed

Customer billing costs (1% of sales)

Irrelevant

Variable

Rental cost of manufacturing facility

Relevant

Fixed

Advertising costs ($200,000 per year)

Irrelevant

Fixed

Labor cost ($8 per unit)

Relevant

Variable

Sales commissions (1.50% of sales)

Irrelevant

Variable

Salaries of administrative personnel

Irrelevant

Fixed

Shipping and handling ($0.50 per unit)

Irrelevant

Variable

Depreciation on office furniture

Irrelevant

Fixed

Manufacturing supplies ($0.25 per unit)

Relevant

Variable

Production supervisor’s salary

Relevant

Fixed

All unit-level manufacturing costs (materials, labor, manufacturing supplies) are relevant

because they could be avoided if the products were purchased instead of manufactured.

Similarly, it is highly probable that the product-sustaining and facility-sustaining costs that

are associated with making the products (production supervisor’s salary and rental of

Exercise 13-3

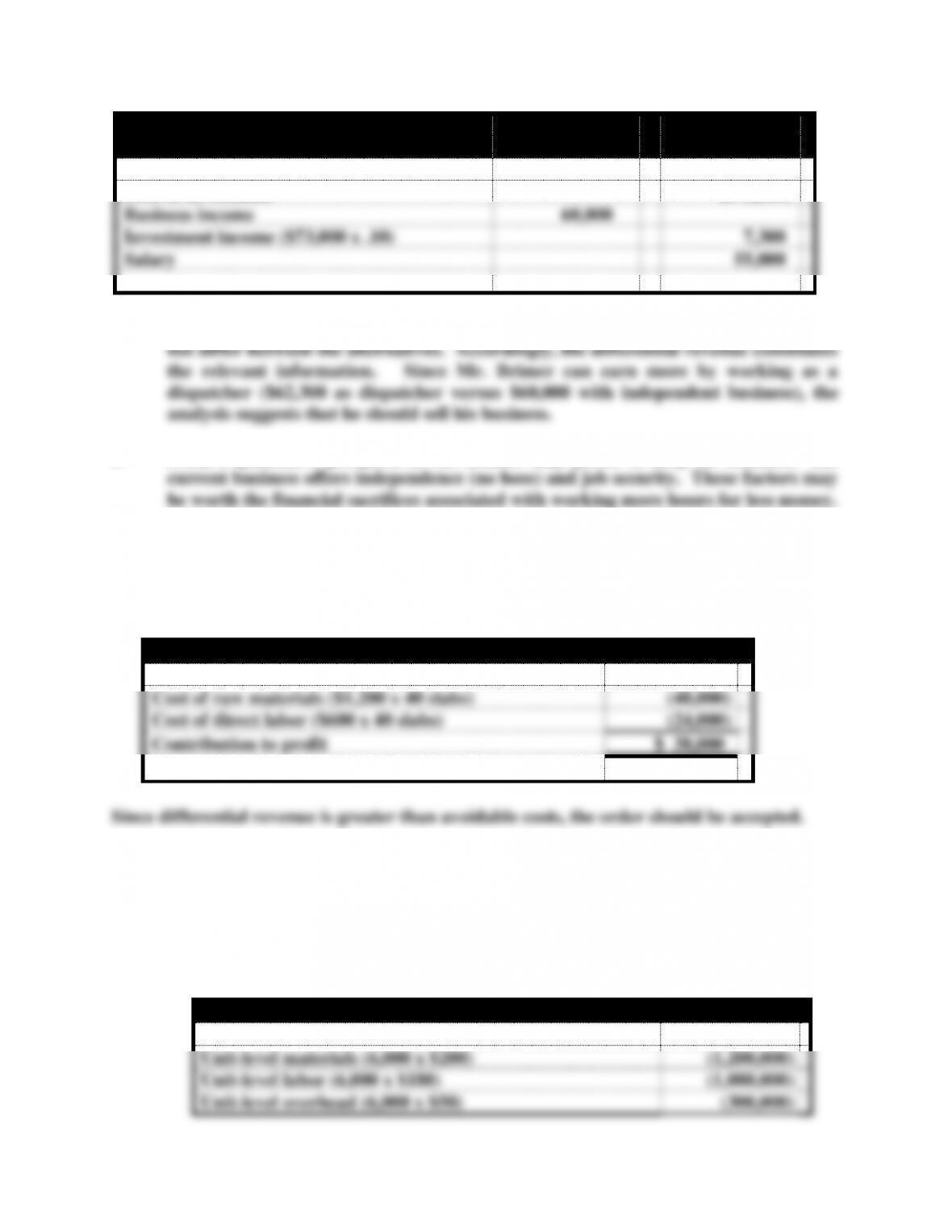

a.

Fixed Costs

Bracelet A

Bracelet B

Advertising cost

$ 7,500

$5,000

Depreciation on existing equipment

5,000

4,000

Total fixed costs

$12,500

$9,000

b.

Variable Costs

Bracelet A

Bracelet B

Cost of materials per unit

$16

$ 30

Cost of labor per unit

32

32

Total variable costs

$48

$62

c.

Avoidable Costs

Bracelet A

Bracelet B

Cost of materials per unit

$ 16

$ 30

Advertising cost

7,500

5,000

Exercise 13-4

Cost Description

Cost Classification

Salary of company president

Facility-level cost

Research and development cost

Product-level cost

Factory lawn care cost

Facility-level cost

Cost of patent

Product level cost

Startup cost to change color of a product

Batch-level cost

Cost of resetting sewing machines to change shirt size

Batch-level cost

Real estate tax for the factory

Facility-level cost

Direct labor

Unit-level cost

Exercise 13-5

a. By holding on to his business, Mr. Brimer is losing the opportunity to sell it.

b. Mr. Brimer can continue to operate his independent taxi company. Alternatively, he

Decision

Independent

Business

Work As

Dispatcher

Opportunity cost

$(73,000)

Cost of investment

$(73,000)

Business income

60,000

Investment income ($73,000 x .10)

7,300

Salary

55,000

The opportunity cost and the cost of the investment are not relevant because they do

c. From a qualitative perspective, Mr. Brimer may prefer to keep his business. His

Exercise 13-6

The facility-sustaining overhead is not relevant because it will be incurred regardless of

whether the special order is accepted or rejected. The differential revenue and avoidable

costs are shown below:

Relevant Revenue and Costs

Sales revenue ($2,750 x 40 slabs)

$110,000

Cost of raw materials ($1,200 x 40 slabs)

(48,000)

Cost of direct labor ($600 x 40 slabs)

(24,000)

Contribution to profit

$ 38,000

Exercise 13-7

Since the product- and facility-sustaining costs do not differ between the alternatives, they

are not avoidable. The differential revenue and relevant (avoidable) costs are shown below:

Relevant Revenue and Costs

Additional revenue (6,000 x $450)

$2,700,000

Unit-level materials (6,000 x $200)

(1,200,000)

Unit-level labor (6,000 x $180)

(1,080,000)

Unit-level overhead (6,000 x $50)

(300,000)

Contribution to profit

$ 120,000

Exercise 13-8

Miko must consider the impact on the company’s existing customers. The special order

customer should be outside Miko’s normal selling territory so as to avoid demands by

existing customers for lower prices. Also, if the special order customer serves the same

Exercise 13-9

a. The unit-level costs increase and decrease in direct proportion with changes in the

number of units sold and produced. Accordingly, these costs are variable costs. The

variable cost per unit is computed by dividing the total unit-level costs by the number

b.

Incremental revenue ($10 x 8,000 units)

$80,000

Variable costs ($7.60 x 8,000 units)

60,800

Contribution to profit

$19,200

Exercise 13-10

The allocated facility-sustaining costs are not avoidable because they will be incurred

regardless of whether the handlebars are made or outsourced. The relevant (avoidable) costs

are shown below:

Item

Per Unit

Total

Cost of materials

$15

$150,000

Cost of labor

10

100,000

Overhead

2

20,000

Total cost

$27

$270,000

Exercise 13-11

a. The maximum amount that Rimes would be willing to pay is the amount of

production costs that could be avoided if production were stopped. In other words,

the cost of buying the engines must be equal to or less than the avoidable cost of

making them. Accordingly, the question can be answered by calculating the per unit

avoidable cost of production. The cost of the depreciation on equipment cannot be

avoided because it is a sunk cost that has already been incurred. Corporate-level

facility-sustaining cost will be incurred regardless of whether engines are purchased

or manufactured. Accordingly, the allocated portion of corporate-level facility-

sustaining costs does not differ between the alternatives and is not avoidable. The

relevant (avoidable) costs are as follows:

Avoidable Costs for Lawn Mower Engines

Cost of materials (20,000 units x $24)

$ 480,000

Labor (20,000 units x $26)

520,000

Production supervisor’s salary

85,000

Rental cost of equipment used to make engines

23,000

Total cost to make 15,000 engines

$1,108,000

Cost per unit ($1,108,000 ÷ 20,000 units)

$55.40

Exercise 13-11 (continued)

The maximum amount that Rimes would be willing to pay to purchase engines would

be $55.40 per unit.

b. The avoidable cost per unit would decrease because the fixed costs (supervisor’s salary

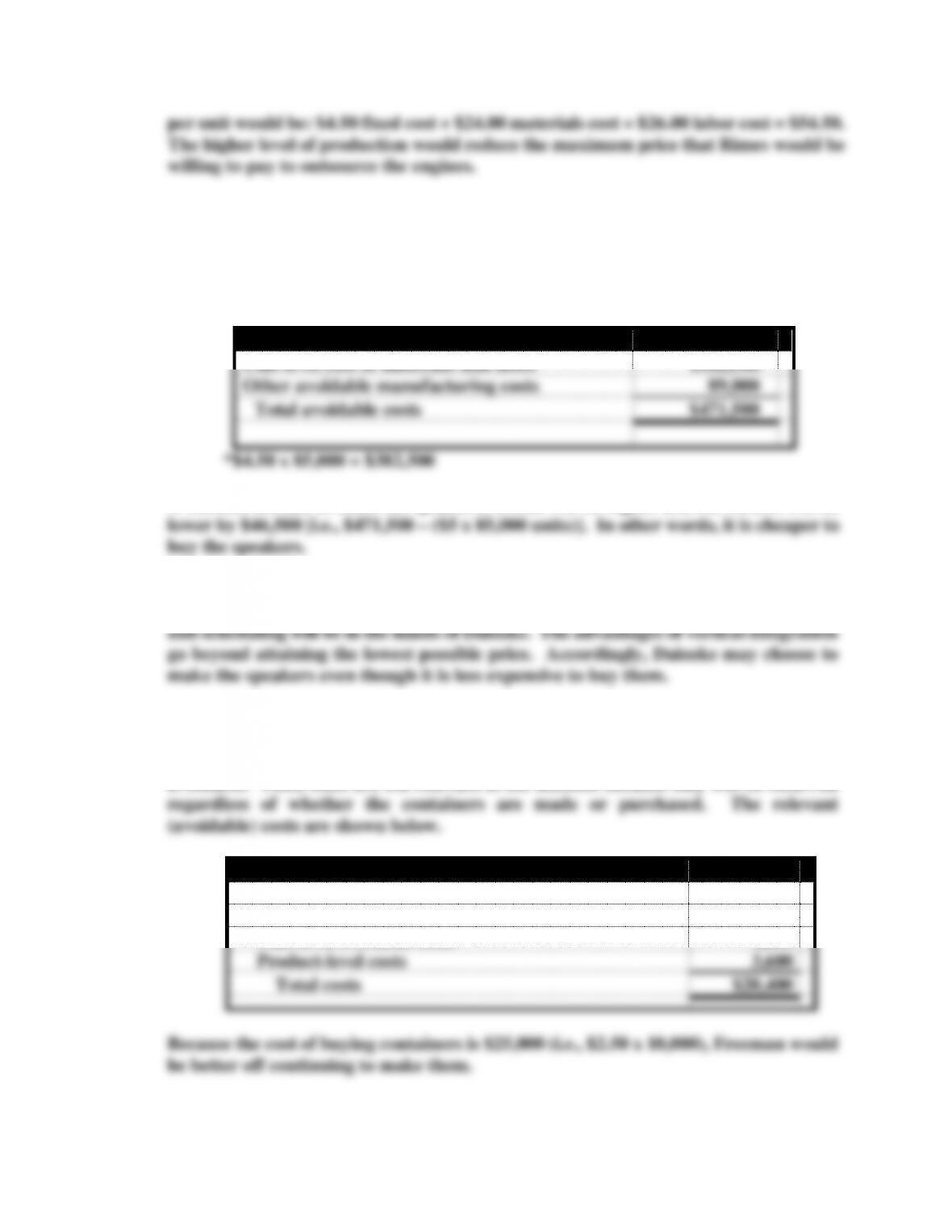

Exercise 13-12

a. The facility-sustaining costs are not avoidable because they will be incurred

regardless of whether the speakers are produced internally or are outsourced. The

relevant (avoidable) costs are shown below:

Decision

Make

Unit-level cost of materials and labor

$382,500*

Other avoidable manufacturing costs

89,000

Total avoidable costs

$471,500

If Daisuke decides to make the speakers, its cost will be higher and net income will be

b. Daisuke should consider the following qualitative factors. If Daisuke makes the

speakers, the company will gain control of the production process. Quality control

Exercise 13-13

a. Two-thirds of the product-level and all of the facility-sustaining costs are not

avoidable. These costs are not relevant to the decision because they will be incurred

Avoidable Costs

Unit-level materials

$ 6,000

Unit-level labor

6,600

Unit-level overhead costs

4,200

Product-level costs

3,600

Total costs

$20,400

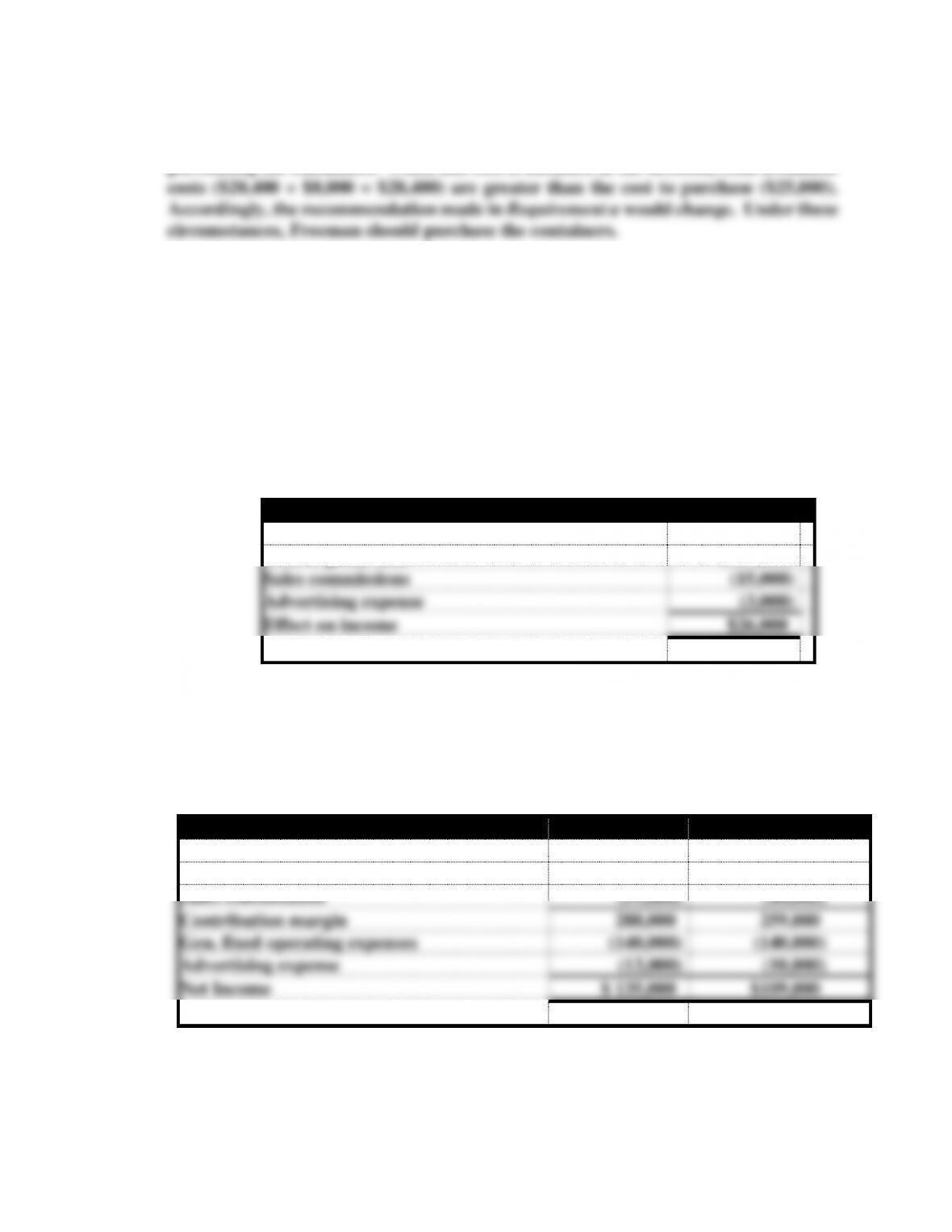

Because the cost of buying containers is $25,000 (i.e., $2.50 x 10,000), Freeman would

be better off continuing to make them.

b. Freeman is giving up the opportunity to obtain $8,000 of lease income by continuing

to make the containers. This is an opportunity cost that could be avoided by

purchasing the containers. When this cost is included in the decision, total avoidable

Exercise 13-14

a. First, identify all of the revenues and costs associated with the operation of Segment

A. These items are listed in the problem under the column labeled Segment A.

Remember the two alternatives are to either keep Segment A or to eliminate the

segment. Eliminate the items that do not differ between these alternatives and the

sunk costs. The $44,000 of general fixed costs will continue regardless of whether the

segment is eliminated. Consequently, this cost is not avoidable. Similarly, the

depreciation charge should be removed because it is a sunk cost. The relevant cost

and revenue items are shown below:

Relevant Rev. and Cost items for Segment A

Sales

$165,000

Cost of goods sold

(121,000)

Sales commissions

(15,000)

Advertising expense

(3,000)

Effect on income

$26,000

The above analysis suggests the segment is contributing $26,000 to the profitability of

the company as a whole. This analysis can be verified by creating comparative

company income statements under the two alternatives. The appropriate

computations are shown below:

b.

Decision

Keep Seg. A

Eliminate Seg. A

Sales

$655,000

$490,000

Cost of goods sold

(308,000)

(187,000)

Sales commissions

(59,000)

(44,000)

Contribution margin

288,000

259,000

Gen. fixed operating expenses

(140,000)

(140,000)

Advertising expense

(13,000)

(10,000)

Net Income

$ 135,000

$109,000

Since Segment A contributes $26,000 to profitability it should not be eliminated.

Exercise 13-15

a. The companywide facility-sustaining costs are not avoidable and therefore not

relevant to the elimination decision. The relevant revenue and cost data are

summarized below:

Income Statement

Revenue

$250,000

Salaries for drivers

(175,000)

Fuel expenses

(25,000)

Insurance

(35,000)

Division level facility-sustaining costs

(20,000)

Contribution to profit

$ (5,000)

Since incremental revenue is less than avoidable costs, the segment should be

eliminated, thereby increasing companywide income by $5,000.

b. Since total avoidable costs amount to $255,000, increasing segment revenue to

c. To justify its existence, segment revenue must be at least equal to avoidable costs.