10-1

Problem 10-24

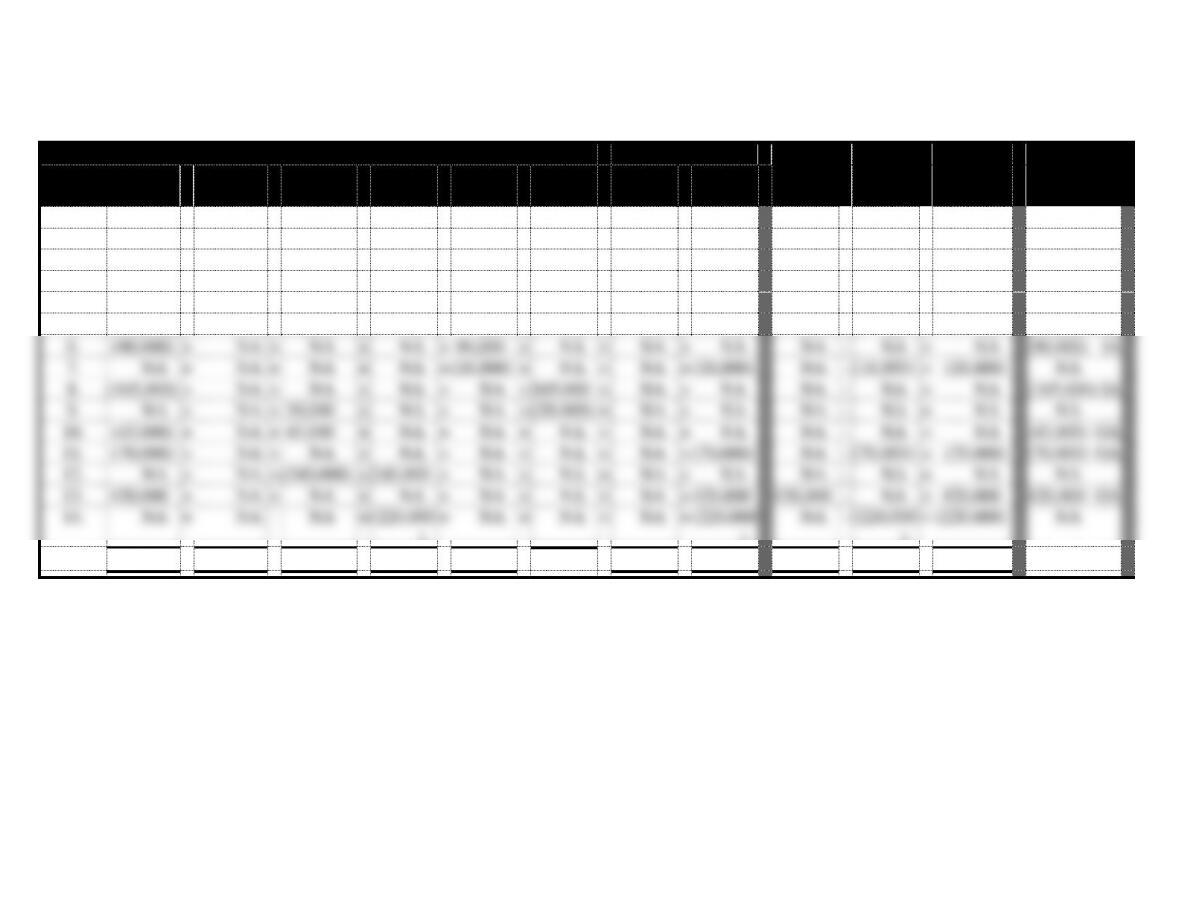

Event

Assets

=

Equity

Rev.

–

Exp.

=

N. Inc.

Cash Flow

No.

Cash

+

Raw M.

+

WIP

+

Finished

Goods

+

Office

Furn.

+

Manuf.

Equip.

=

Com.

Stk.

+

Ret. Ear.

BB

660,000

+

51,000

+

18,000

+

43,000

+

NA

+

NA

=

583,000

+

189,000

NA

–

NA

=

NA

1.

(23,000)

+

NA

+

NA

+

NA

+

NA

+

NA

=

NA

+

(23,000)

NA

–

(23,000)

=

(23,000)

(23,000) OA

2.

(47,000)

+

47,000

+

NA

+

NA

+

NA

+

NA

=

NA

+

NA

NA

–

NA

=

NA

(47,000) OA

3.

NA

+

(83,000)

+

83,000

+

NA

+

NA

+

NA

=

NA

+

NA

NA

–

NA

=

NA

NA

4.

(60,000)

+

NA

+

NA

+

NA

+

NA

+

NA

=

NA

+

(60,000)

NA

–

(60,000)

=

(60,000)

(60,000) OA

5.

(91,000)

+

NA

+

91,000

+

NA

+

NA

+

NA

=

NA

+

NA

NA

–

NA

=

NA

(91,000) OA

6.

(90,000)

+

NA

+

NA

+

NA

+

90,000

+

NA

=

NA

+

NA

NA

–

NA

=

NA

(90,000) IA

7.

NA

+

NA

+

NA

+

NA

+

(16,000)

+

NA

=

NA

+

(16,000)

NA

–

(16,000)

=

(16,000)

NA

8.

(165,000)

+

NA

+

NA

+

NA

+

NA

+

165,000

=

NA

+

NA

NA

–

NA

=

NA

(165,000) IA

9.

NA

+

NA

+

20,000

+

NA

+

NA

+

(20,000)

=

NA

+

NA

NA

–

NA

=

NA

NA

10.

(45,000)

+

NA

+

45,000

+

NA

+

NA

+

NA

=

NA

+

NA

NA

–

NA

=

NA

(45,000) OA

11.

(70,000)

+

NA

+

NA

+

NA

+

NA

+

NA

=

NA

+

(70,000)

NA

–

(70,000)

=

(70,000)

(70,000) OA

12.

NA

+

NA

+

(240,000)

+

240,000

+

NA

+

NA

=

NA

+

NA

NA

–

NA

=

NA

NA

13.

420,000

+

NA

+

NA

+

NA

+

NA

+

NA

=

NA

+

420,000

420,000

–

NA

=

420,000

420,000 OA

14.

NA

+

NA

NA

+

(220,000

)

+

NA

+

NA

=

NA

+

(220,000

)

NA

–

(220,000

)

=

(220,000)

NA

Total

489,000

+

15,000

+

17,000

+

63,000

+

74,000

+

145,000

=

583,000

+

220,000

420,000

–

389,000

=

31,000

(171,000)

10-2

Problem 10-24 (continued)

b.

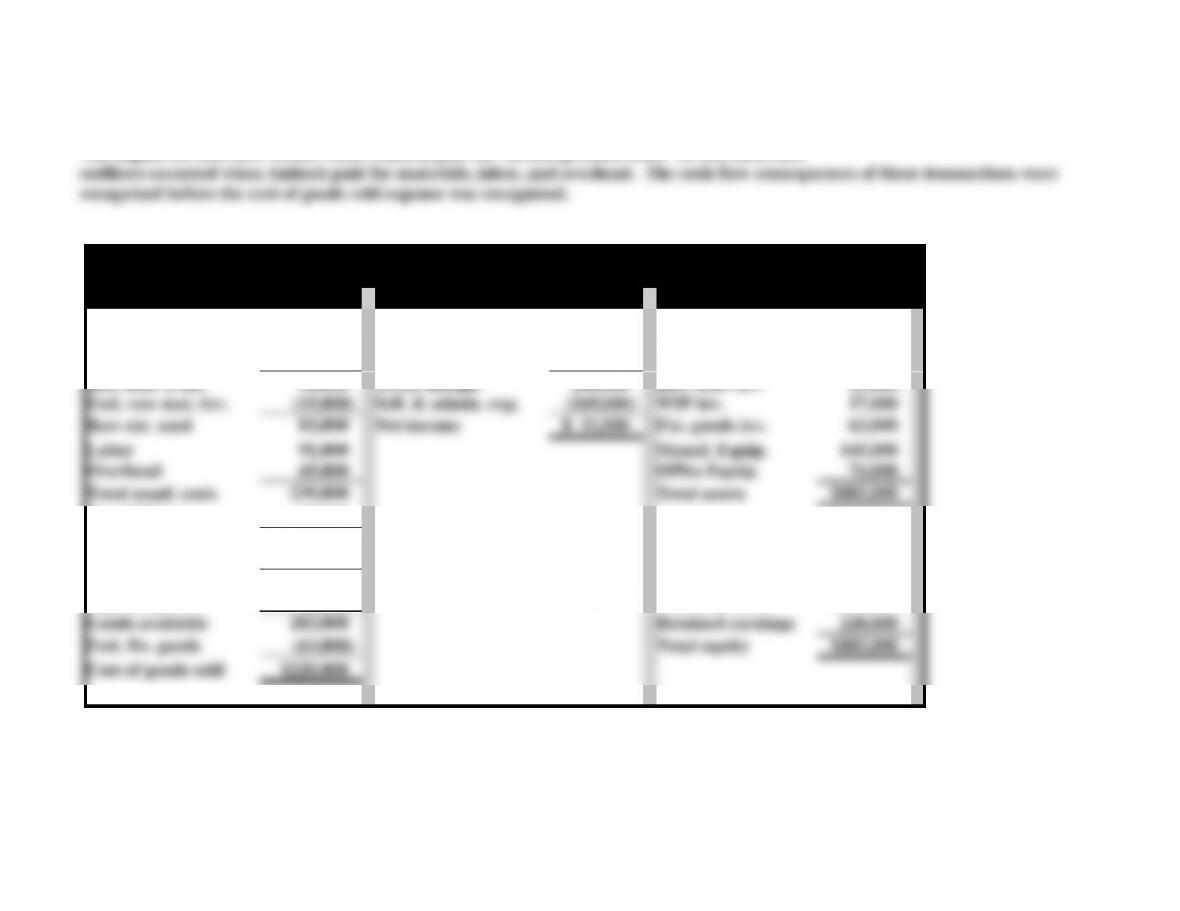

The impact on cash flow occurs when Antioch pays for various product costs. In this case, cash

c.

Antioch Company

Financial Statements for 2014

Cost of Goods Manf. and Sold

Income Statement

Balance Sheet

Beg. raw mat. inv.

$51,000

Sales revenue

$420,000

Assets

Purchases

47,000

Cost of goods sold

(220,000)

Cash

$489,000

Raw mat. avail.

98,000

Gross margin

200,000

Raw mat. inv.

15,000

End. raw mat. inv.

(15,000)

Sell. & admin. exp.

(169,000)

WIP inv.

17,000

Raw rat. used

83,000

Net income

$ 31,000

Fin. goods inv.

63,000

Labor

91,000

Manuf. Equip.

145,000

Overhead

65,000

Office Equip.

74,000

Total manf. costs

239,000

Total assets

$803,000

Beg. WIP inv.

18,000

Total WIP inv.

257,000

End. WIP inv.

(17,000)

Cost of goods man.

240,000

Equity

Beg. fin. goods

43,000

Common stock

$583,000

Goods available

283,000

Retained earnings

220,000

End. fin. goods

(63,000)

Total equity

$803,000

Cost of goods sold

$220,000

10-3

Problem 11-24 (continued)

d.

Inventory product costs for manufacturing companies focus on the costs necessary to make

the product. The cost of research and development (Event 1) occurs before the inventory is

made and is therefore an upstream cost, not an inventory (product) cost. The inventories

holding costs (Event 11) are incurred after the inventory has been made and are, therefore,

as product costs.

e.

Since the merchandise would be available on demand, Antioch could operate a just–in-time

inventory system thereby eliminating the inventory holding expense. Since the additional

10-4

Problem 10-25

a. Annual inventory holding cost:

($2,000,000 x 10%) + ($9,000 x 12) = $308,000

b. A JIT system should enable Torre to receive raw materials just in time for

production. Therefore, it virtually eliminates the need to hold inventory. The

inventory holding cost can be eliminated as well.

Problem 10-26

a. 95 students enroll in the course:

Revenue ($1,500 x 95)

$142,500

Expenses

Cost of textbooks ($80 x 110)

$ 8,800

Cost of teachers

36,000

Other operating expenses

40,000

Total expenses

84,800

Net income

$ 57,700

Cost of unused books: [(110 – 95) x $80] = $1,200.

b. 115 students attempt to register, but only 110 students can be accepted:

Revenue ($1,500 x 110)

$165,000

Expenses

Cost of textbooks ($80 x 110)

$ 8,800

Cost of teachers

36,000

Other operating expenses

40,000

Total expenses

84,800

Net income

$ 80,200

Problem 10-26 (continued)

If all 115 students could be accepted, the income statement would be as follows:

Revenue ($1,500 x 115)

$172,500

Expenses

Cost of textbooks ($80 x 115)

$ 9,200

Cost of teachers

36,000

Other operating expenses

40,000

Total expenses

85,200

10-5

Net income

$ 87,300

The lost profit resulting from rejecting 5 additional students is $7,100 ($87,300 –

$80,200).

c. 95 students enrolled under a JIT system:

Revenue ($1,500 x 95)

$142,500

Expenses

Cost of textbooks ($90 x 95)

$ 8,550

Cost of teachers

36,000

Other operating expenses

40,000

Total expenses

84,550

Net income

$ 57,950

The savings from eliminating the cost of excessive books exceeds the increased

Problem 10-26 (continued)

d. 115 students enrolled under the JIT system

Revenue ($1,500 x 115)

$172,500

Expenses

Cost of textbooks ($90 x 115)

$10,350

Cost of teacher

36,000

Other operating expenses

40,000

Total expenses

86,350

Net income

$ 86,150

The additional revenue from 5 students who would have been turned away

under the condition of requirement b exceeds the additional cost of books

required under the JIT system. Therefore, the JIT system results in a greater

net income than the traditional system.

e. Students who are denied enrollment may develop a negative image of CMA

Review, Inc. The negative image could become widespread when the disgruntled

10-6

students complain to their friends. The JIT system not only improves net

income, but improves customer satisfaction by allowing everyone entry into the

course.

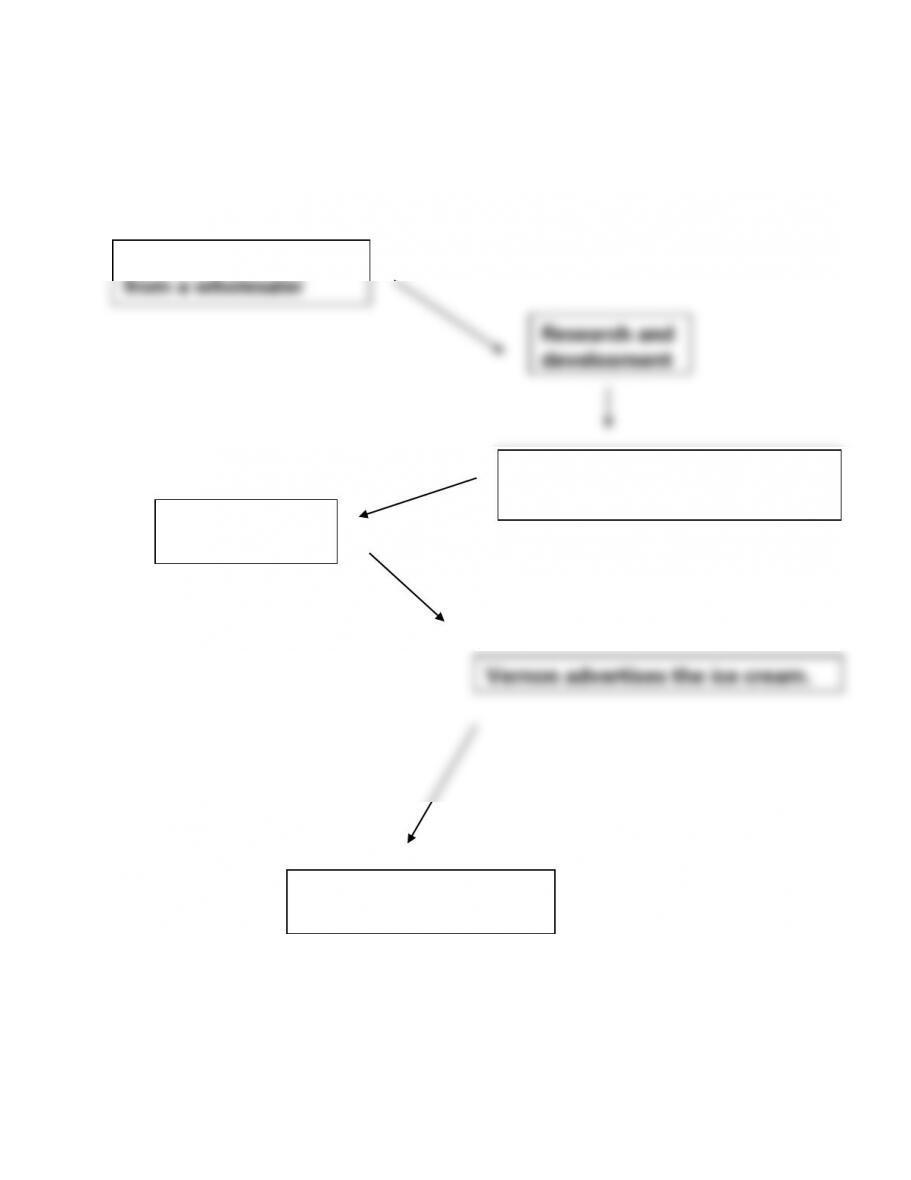

Problem 10-27

Purchases materials

from a wholesaler

supplier.

Vernon processes the materials

to make ice cream.

a. Value Chain

Research and

development

Distributes to

ice cream

shops.

Ice cream shops sell the

product to the public.

Vernon advertises the ice cream.

10-7

Problem 10-27 (continued)

b. Vernon’s competitors engage in activities similar to Jensen’s for materials

acquisition, product manufacturing, product distribution, and advertising. The

value-added activity that Vernon has created is its research and development

effort, which resulted in a new product for consumers.

ATC 10-1

a. The information described in the table is primarily managerial accounting

for managerial accounting purposes.

c. Starbucks’ 2012 fiscal year appears a better than 2011 because in 2012 it had

higher revenues and net earnings.

ATC 10-2

a.

1. Cost of goods sold

Raw materials

$ 720,000

Utilities1

96,000

Labor

880,000

Depreciation on manufacturing equipment2

1,000,000

Setup cost

80,000

Total product cost

$2,776,000

10-8

Cost of goods sold = $40 per unit x 60,000 units = $2,400,000

2. Upstream Costs

Note: The $10,000 of accrued engineer’s salaries is an upstream cost. However, it

would not be used in the computation of net income because it applies to the previous

accounting period.

Utilities1

$ 16,000

Salaries

390,000

Redesign cost

186,000

Insurance expense3

16,000

Total

$608,000

3. Downstream Costs

Advertising

$ 70,000

Utilities1

48,000

Salaries ($658,000 + $16,000)

674,000

Insurance expense3

32,000

Total

$824,000

ATC 10-2 (continued)

1Allocation Rate for Utilities = $160,000 100,000 = $1.60 per square foot.

Research and development

10,000

x

$1.60

=

$ 16,000

Manufacturing

60,000

x

$1.60

=

96,000

Selling and administrative

30,000

x

$1.60

=

48,000

Total

100,000

x

$1.60

=

$160,000

Rate for insurance expense = $48,000 12 = $4,000 per employee.

Research and development

4

x

$4,000

=

$16,000

Selling and administrative

8

x

$4,000

=

32,000

Total

12

x

$4,000

=

$48,000

10-9

b. Income Statement

Revenue (60,000 x $70)

$4,200,000

Cost of goods sold

(2,400,000)

Gross margin

1,800,000

Upstream expense

(608,000)

Downstream expenses

(824,000)

Net income

$ 368,000

ATC 10-3

a. The company’s annual report provides little detail regarding the individual costs

incurred to manufacture its products. This annual report, like those of all public

companies, is designed primarily to meet the needs of external or internal users.

d. The company reports the balances in three separate inventory accounts:

Finished goods, Work in process, and Raw materials.

ATC 10-4

Each letter prepared by the students will be unique. Accordingly, there is no single

solution. However, student letters should include some discussion of at least a few of the

following ideas: (1) global competition, (2) benchmarking, (3) value-added assessment,

(4) reengineering, and (5) just-in-time inventory systems.

b. As discussed in part a, misclassifying the start-up costs would present a more

favorable representation of the company’s financial condition (i.e., assets and net

income are overstated) than actually exists. Accordingly, investors or creditors

10-10

may be lured into making an investment in or loan to the company that they

otherwise would have avoided.

c. The overstatement of income would result in the overpayment of taxes. This

would be detrimental to the owners of the business.

d. Ms. Emerson violated many of the ethical principles some of which included the

failure to (1) perform professional duties in accordance with relevant laws,

regulations, and technical standards, (2) prepare complete and clear reports and