Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

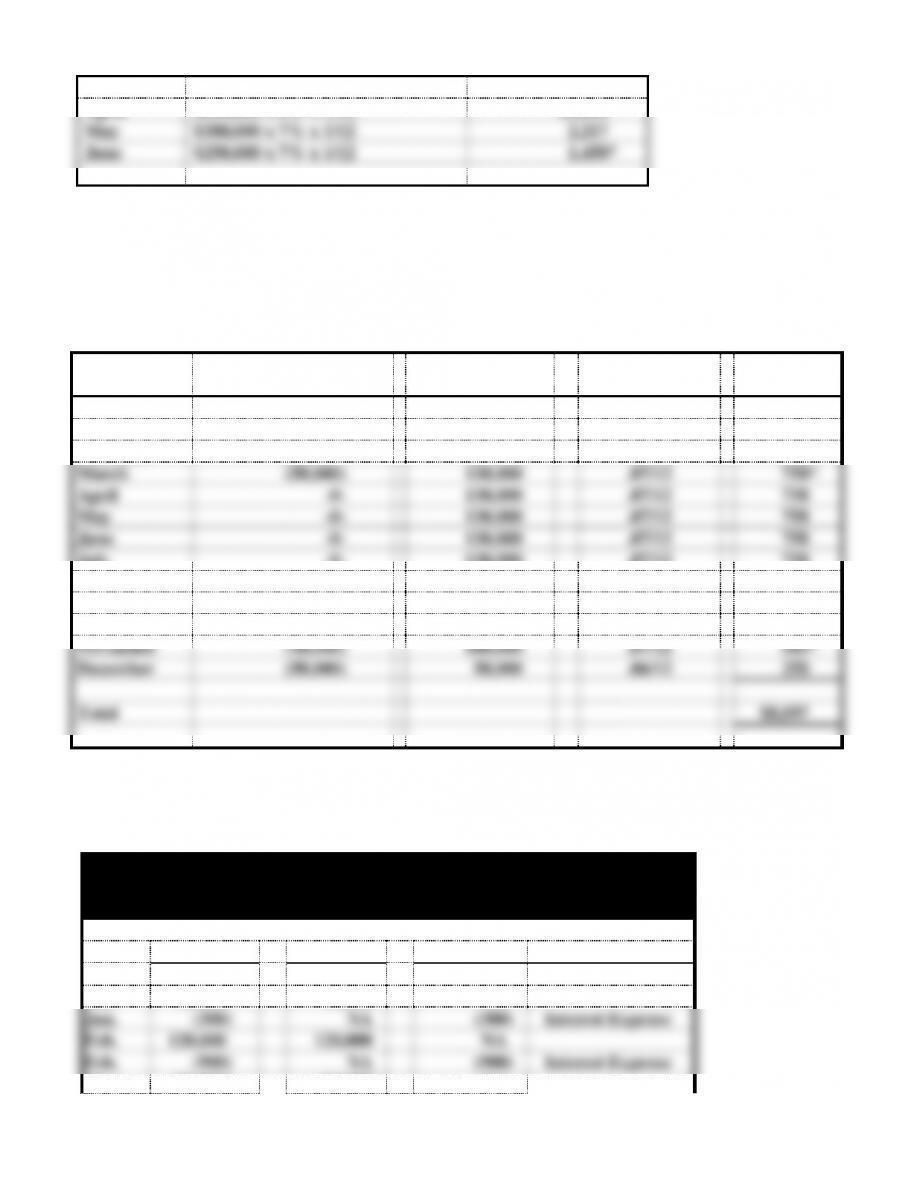

7-1

April

$210,000 x 6% x 1/12

$1,050

May

$380,000 x 7% x 1/12

2,217

June

$250,000 x 7% x 1/12

1,458*

*rounded

b. The amount of cash paid for interest is the same as interest expense. Interest is paid on the

last day of each month.

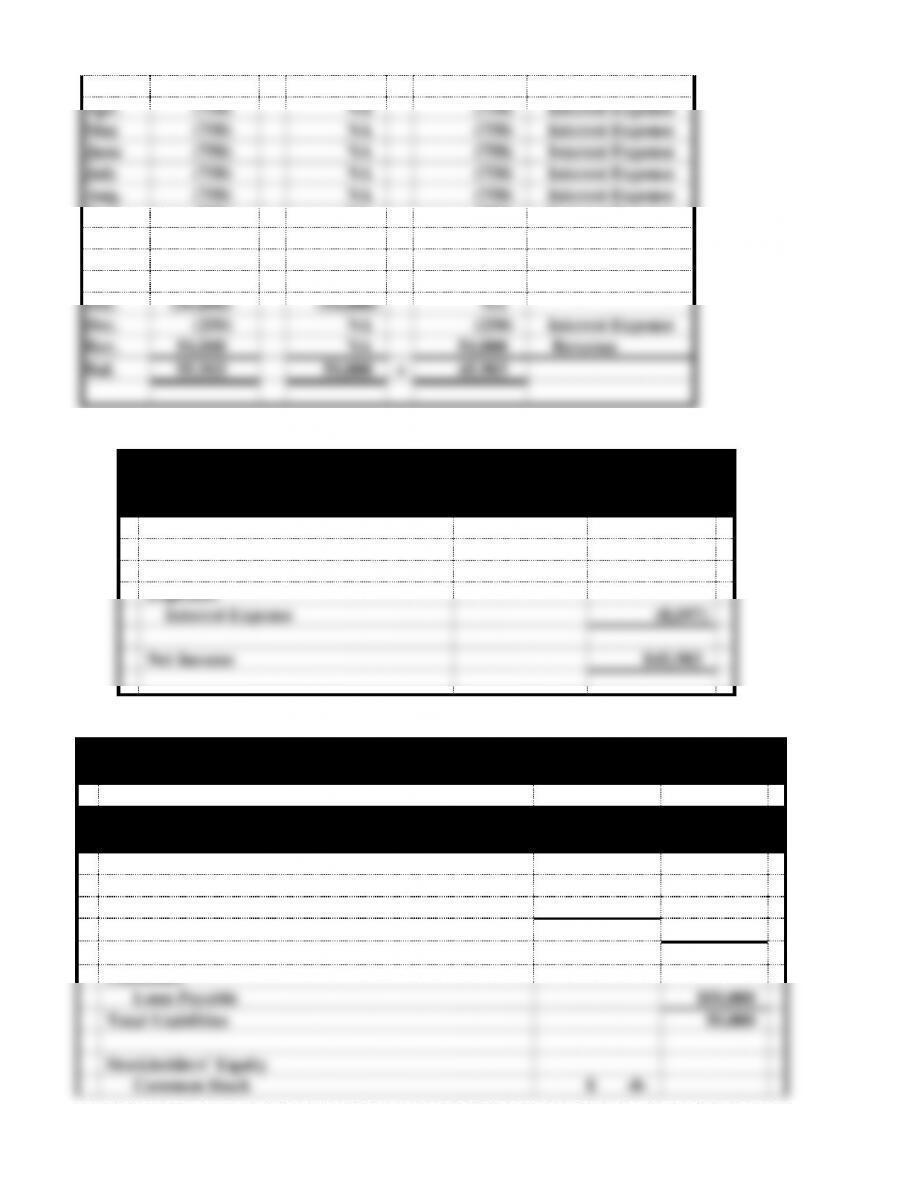

PROBLEM 7-33

Computation of Interest Expense

Month

Amount

Borrowed (Repaid)

End of Month

Balance

x

Interest Rate per

Month

=

Interest

Expense

January

$60,000

$ 60,000

.06/12

$ 300

February

120,000

180,000

.06/12

900

March

(50,000)

130,000

.07/12

758*

April

-0-

130,000

.07/12

758

May

-0-

130,000

.07/12

758

June

-0-

130,000

.07/12

758

July

-0-

130,000

.07/12

758

August

-0-

130,000

.07/12

758

September

-0-

130,000

.07/12

758

October

-0-

130,000

.07/12

758

November

(30,000)

100,000

.07/12

583*

December

(50,000)

50,000

.06/12

250

Total

$8,097

*rounded

PROBLEM 7-33

a.

Melvin Company

Effect of Events on the General Ledger

2014

Assets

=

Liabilities

+

Stk. Equity

Event

Cash

=

Note Pay.

+

Ret. Earn.

Acct. Title/RE

Jan.

60,000

60,000

NA

Jan.

(300)

NA

(300)

Interest Expense

Feb.

120,000

120,000

NA

Feb.

(900)

NA

(900)

Interest Expense

Mar.

(50,000)

(50,000)

NA

7-2

Mar.

(758)

NA

(758)

Interest Expense

Apr.

(758)

NA

(758)

Interest Expense

May

(758)

NA

(758)

Interest Expense

June

(758)

NA

(758)

Interest Expense

July

(758)

NA

(758)

Interest Expense

Aug.

(758)

NA

(758)

Interest Expense

Sept.

(758)

NA

(758)

Interest Expense

Oct.

(758)

NA

(758)

Interest Expense

Nov.

(30,000)

(30,000)

NA

Nov.

(583)

NA

(583)

Interest Expense

Dec.

(50,000)

(50,000)

NA

Dec.

(250)

NA

(250)

Interest Expense

Rev.

54,000

NA

54,000

Revenue

Bal.

95,903

50,000

+

45,903

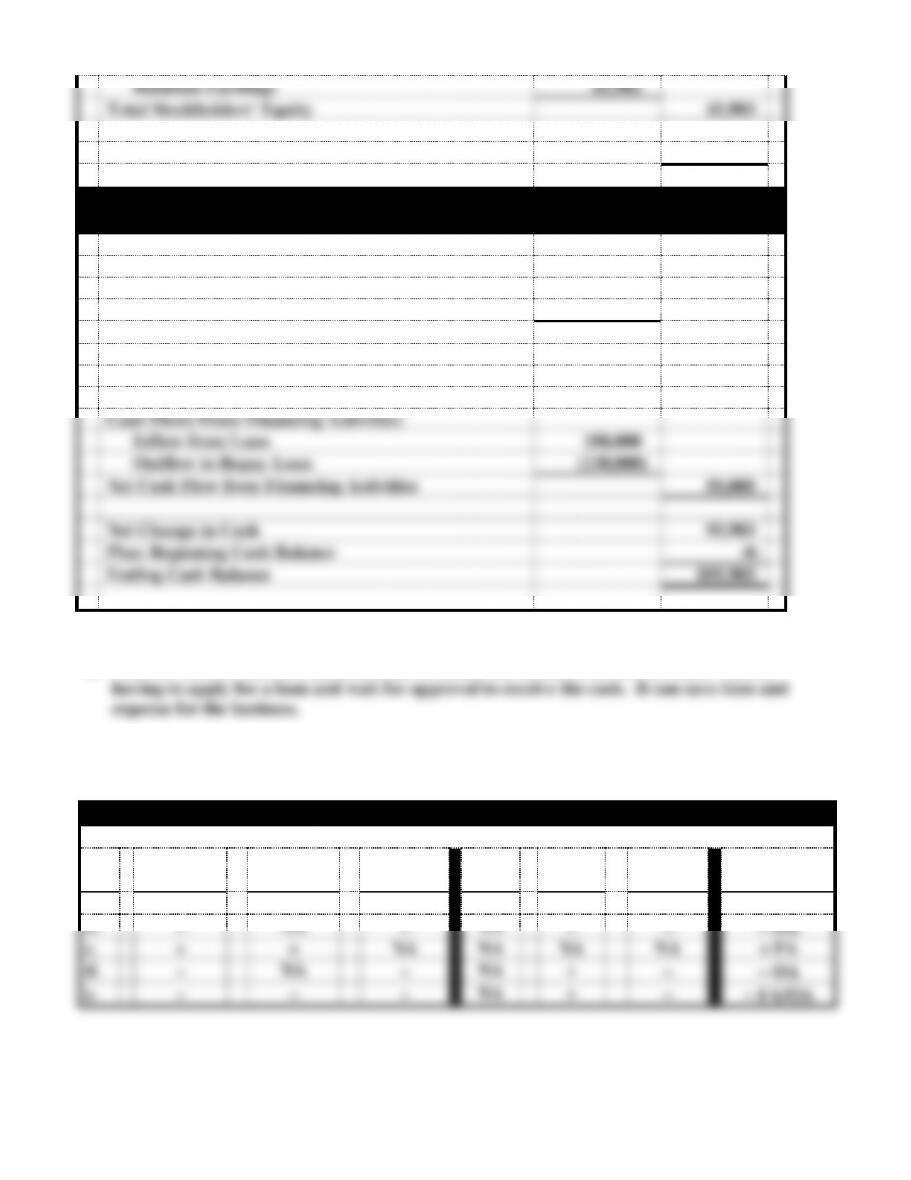

b.

Melvin Company

Income Statement

For the Year Ended December 31, 2014

Service Revenue

$54,000

Expenses

Interest Expense

(8,097)

Net Income

$45,903

PROBLEM 7-33 b. (cont.)

Melvin Company

Financial Statements

Balance Sheet

As of December 31, 2014

Assets

Cash ($50,000 + $45,903)

$95,903

Total Assets

$95,903

Liabilities

Loan Payable

$50,000

Total Liabilities

50,000

Stockholders’ Equity

Common Stock

$ -0-

7-3

Retained Earnings

45,903

Total Stockholders’ Equity

45,903

Total Liabilities and Stockholders’ Equity

$95,903

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash Flows From Operating Activities:

Inflow from Revenue

$54,000

Outflow for Interest

(8,097)

Net Cash Flow from Operating Activities

$45,903

Cash Flows From Investing Activities:

-0-

Cash Flows From Financing Activities:

Inflow from Loan

180,000

Outflow to Repay Loan

(130,000)

Net Cash Flow from Financing Activities

50,000

Net Change in Cash

95,903

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$95,903

PROBLEM 7-33 (cont.)

b. When a business has an established line of credit, the business can access funds without

PROBLEM 7-34

Effect of Transactions on Financial Statements

No.

Assets

=

Liab.

+

Equity

Rev./

Gain

−

Exp./

Loss

=

Net Inc.

Cash Flows

a.

+

+

NA

NA

NA

NA

+ FA

b.

−

NA

−

NA

+

−

− OA

c.

+

+

NA

NA

NA

NA

+ FA

d.

−

NA

−

NA

+

−

− OA

e.

−

−

−

NA

+

−

− FA/OA

7-4

PROBLEM 7-35

Brown Co.

Event

No.

Type of

Event

Assets

=

Liabilities

+

Common Stock

+

Retained

Earnings

Net Income

Cash Flow

1.

AS

+

NA

+

NA

NA

+ FA

2.

AS

+

+

NA

NA

NA

+ FA

3.

AE

+−

NA

NA

NA

NA

− IA

4.

AS

+

NA

NA

+

+

+ OA

5.

AU/CE

−

+

NA

−

−

− OA

6.

AS

+

NA

NA

+

+

+ OA

7.

AU/CE

−

+

NA

−

−

− OA

8.

AS/AE

+

NA

NA

+

+

+ IA

9.

AU

−

−

NA

NA

NA

− FA

7-5

PROBLEM 7-36

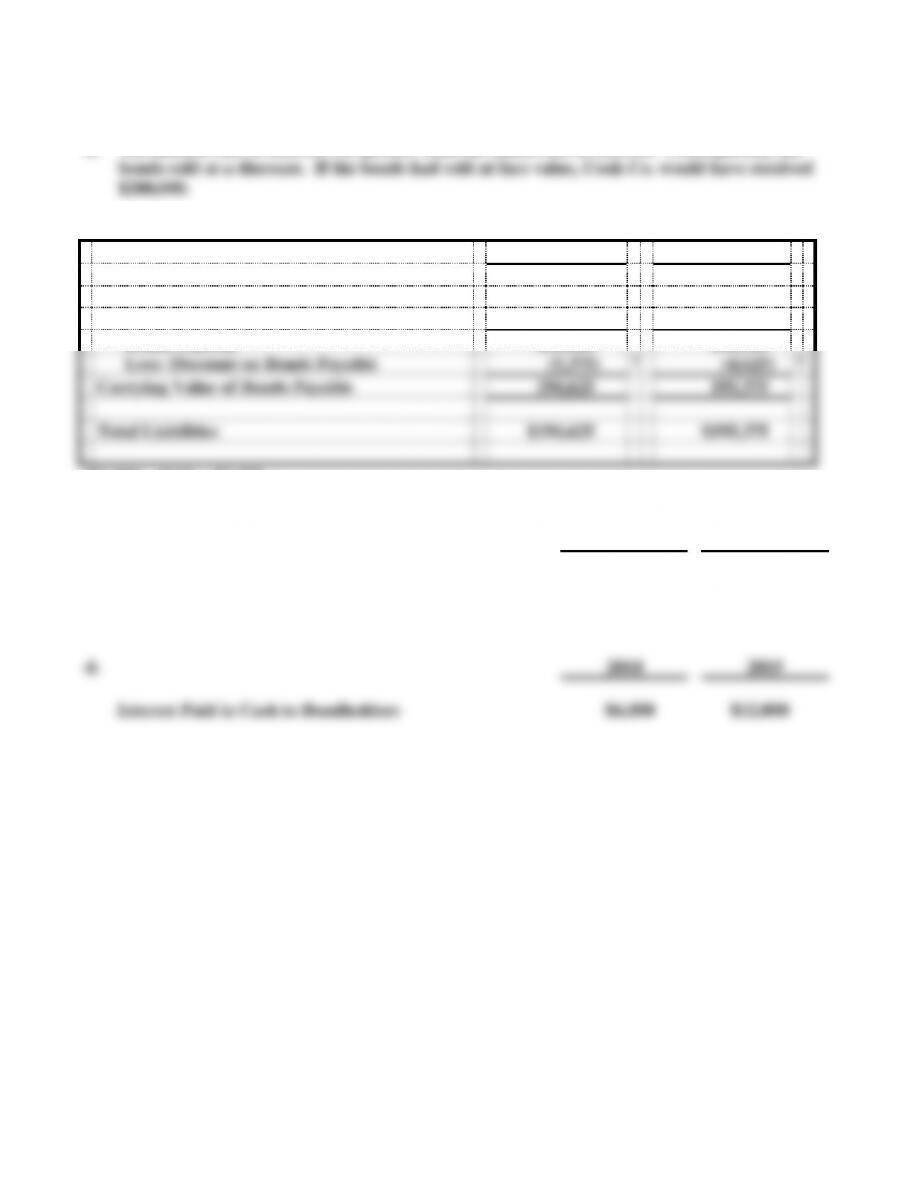

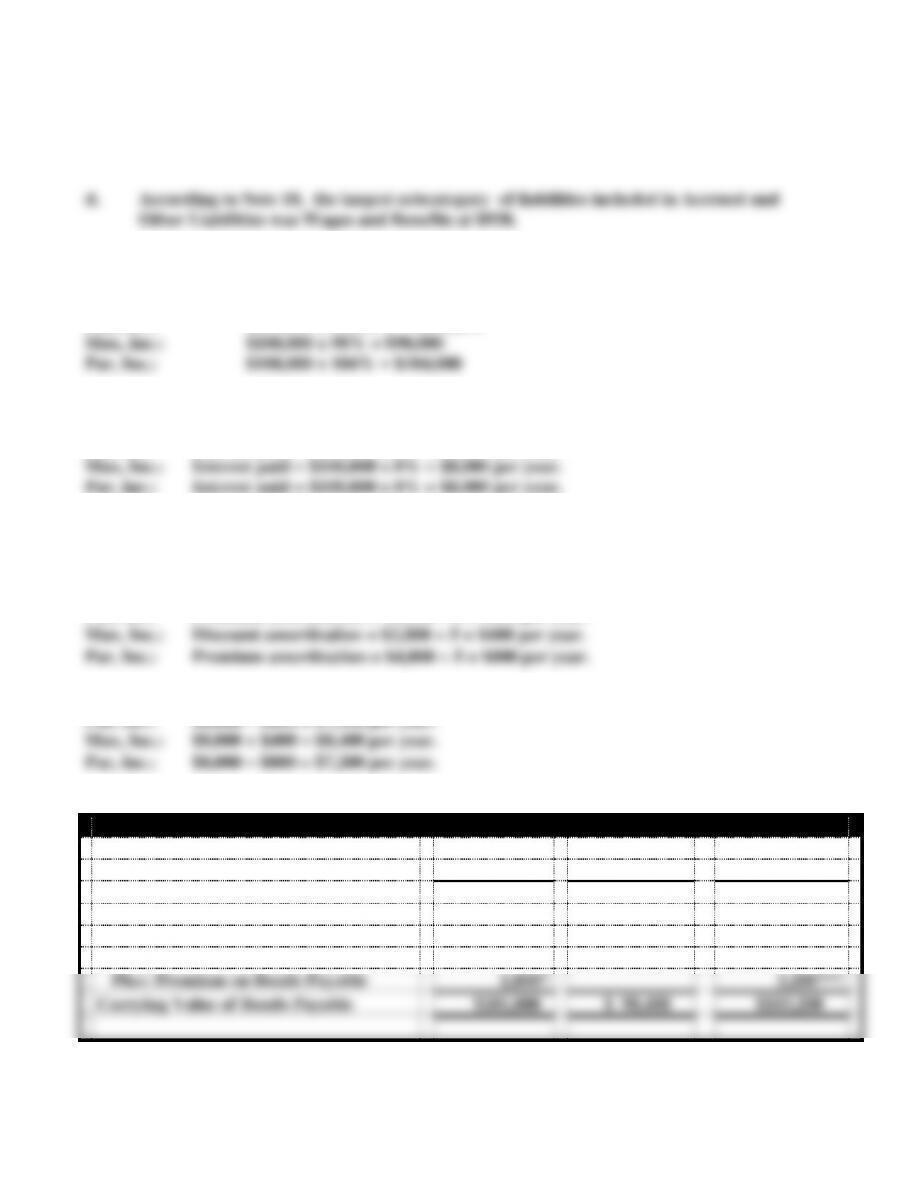

a. The market rate of interest was greater than the stated rate of interest. Consequently, the

b.

2014

2015

Liabilities

Interest Payable

$ 4,000

$ 4,000

Bonds Payable

200,000

200,000

Less: Discount on Bonds Payable

(5,375)

1

(4,625)

2

Carrying Value of Bonds Payable

194,625

195,375

Total Liabilities

$194,625

$195,375

1$6,000 − $625 = $5,375

2$5,375 − $750 = $4,625

c.

2014

2015

Interest Expense Reported on Income Statement

$10,625

$12,750

d.

2014

2015

Interest Paid in Cash to Bondholders

$6,000

$12,000

7-6

PROBLEM 7-37

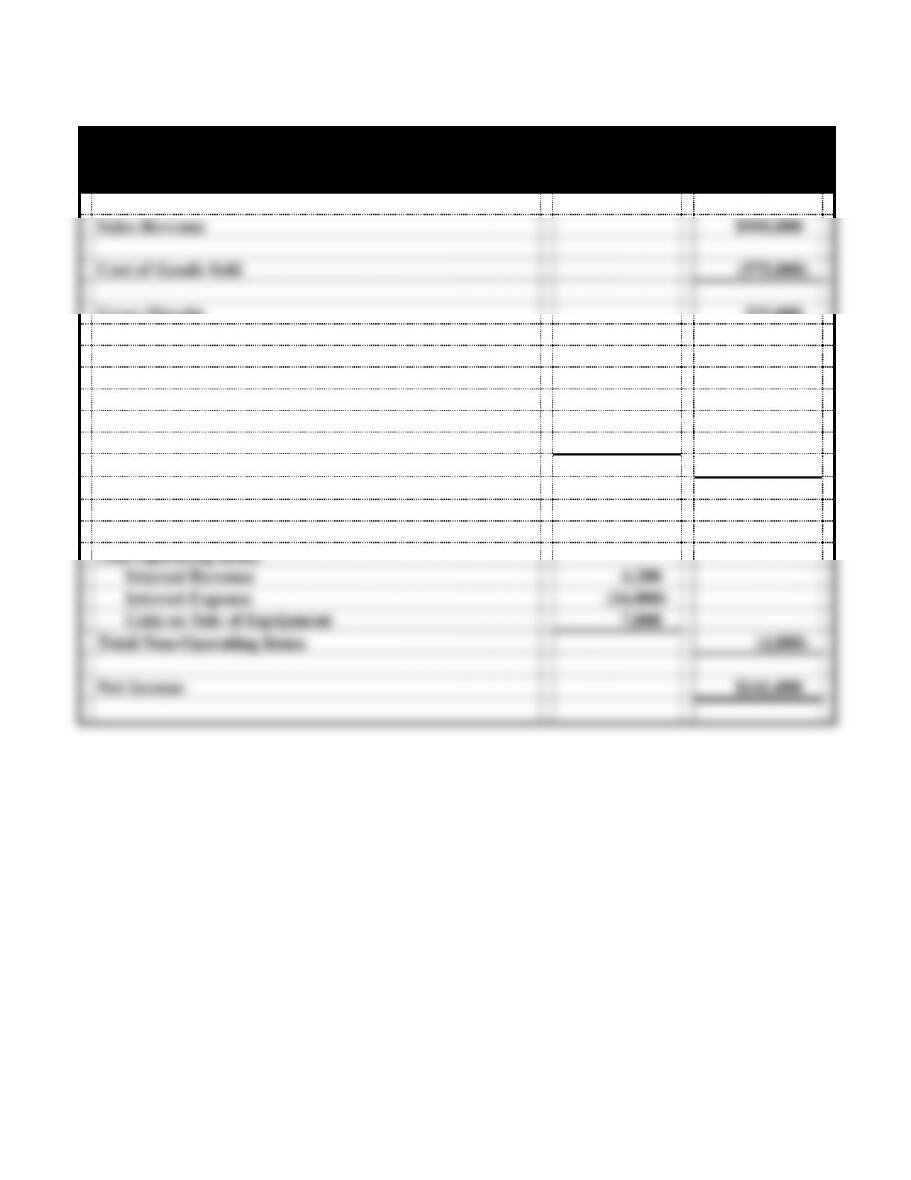

Vernon Company

Income Statement

For the Year Ended December 31, 2014

Sales Revenue

$900,000

Cost of Goods Sold

(575,000)

Gross Margin

325,000

Operating Expenses

Salaries Expense

$102,000

Operating Expenses

45,000

Warranty Expense

7,200

Uncollectible Accounts Expense

25,000

Total Operating Expenses

(179,200)

Operating Income

145,800

Non-Operating Items

Interest Revenue

4,200

Interest Expense

(16,000)

Gain on Sale of Equipment

7,000

Total Non-Operating Items

(4,800)

Net Income

$141,000

7-7

PROBLEM 7-37 (cont.)

Vernon Company

Balance Sheet

As of December 31, 2014

Assets

Current Assets

Cash

$ 46,000

Accounts Receivable

$88,000

Less: Allow. for Doubtful Accounts

(14,000)

74,000

Inventory

126,000

Interest Receivable

1,600

Prepaid Rent

18,000

Supplies

4,500

Notes Receivable

12,500

Total Current Assets

$282,600

Property, Plant and Equipment

Buildings and Equipment

206,000

Less: Accumulated Depreciation

(46,000)

160,000

Land

75,000

Total Property, Plant and Equipment

235,000

Total Assets

$517,600

Liabilities and Stockholders’ Equity

Current Liabilities

Accounts Payable

$ 35,000

Unearned Revenue

27,000

Warranties Payable

4,500

Interest Payable

6,000

Salaries Payable

48,000

Total Current Liabilities

$120,500

Long-Term Liabilities

Notes Payable

140,000

Total Long-Term Liabilities

140,000

Total Liabilities

260,500

Stockholders’ Equity

Common Stock

90,000

Retained Earnings*

167,100

Total Stockholders’ Equity

257,100

7-8

PROBLEM 7-38

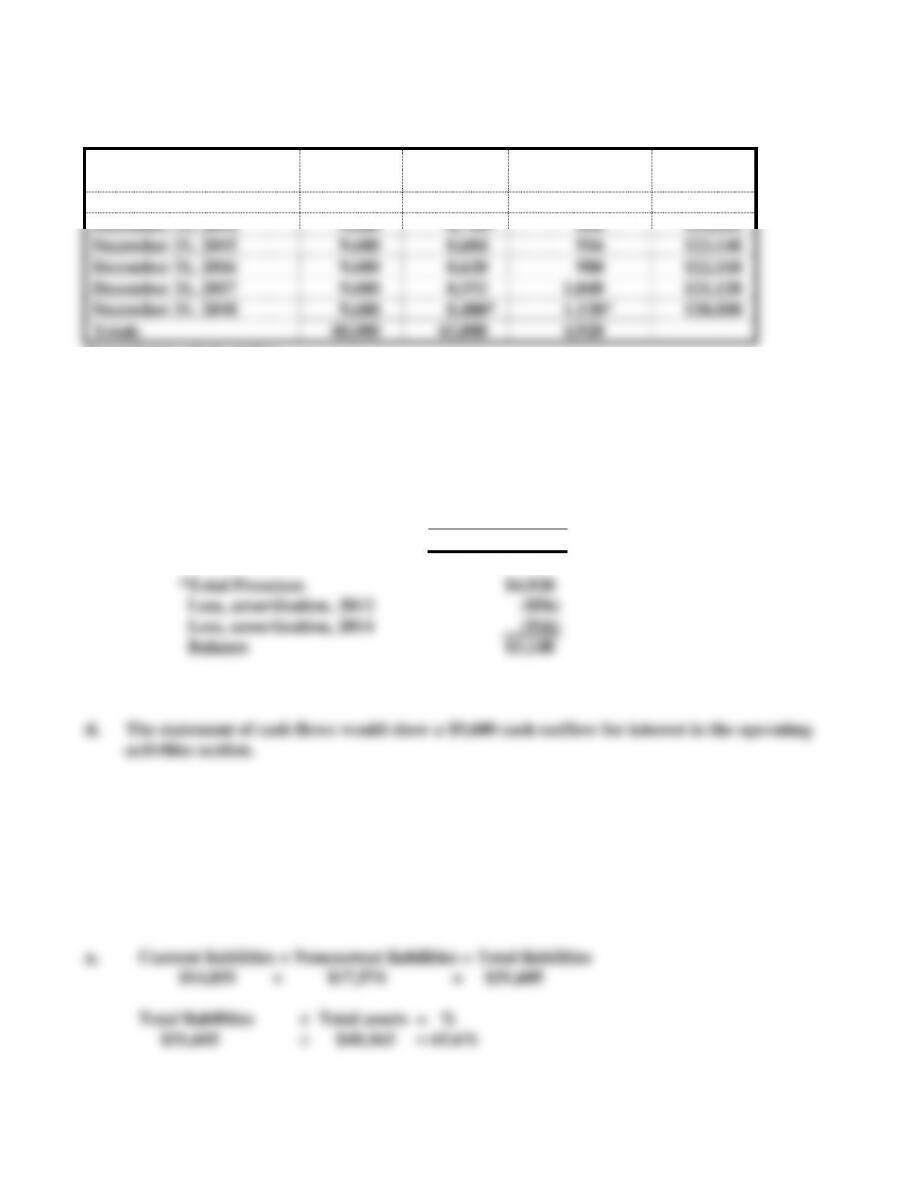

a.

Date

Cash

Payment

Interest

Expense

Premium

Amortization

Carrying

Value

January 1, 2014

124,920

December 31, 2014

9,600

8,744*

856

124,064

December 31, 2015

9,600

8,684

916

123,148

December 31, 2016

9,600

8,620

980

122,168

December 31, 2017

9,600

8,552

1,048

121,120

December 31, 2018

9,600

8,480*

1,120*

120,000

Totals

48,000

43,080

4,920

*rounded to whole dollar

b. The balance sheet would show the carrying value of the bond liability. The carrying value

could be shown net of the premium, $123,148, with further disclosure in the notes to the

financial statements. Alternatively, the face value plus the premium could be shown as

follows:

Bond liability

$120,000

Plus: Bond premium

3,148*

Carrying value

$123,148

c. The income statement would show $8,620 of interest expense.

SOLUTIONS TO ANALYZE, THINK, COMMUNICATE

ATC 7-1

All dollar amounts are in millions.

b. According to Note 17, bank overdrafts are included in Accounts Payable, and Target had

7-9

$588 as of February 2, 2013.

c. According to Note 19, Target’s average interest rate was 4.7% on long term debt and

0.16% on commercial paper, which is short term debt.

ATC 7-2

a.

(1)(a) Cash Proceeds

Lot, Inc.: $100,000 x 102.25% = $102,250

(1)(b)

Interest Paid:

Lot, Inc.: Interest paid = $100,000 x 8% = $8,000 per year.

(1)(c)

Interest Expense = Interest paid +/− amortized discount/premium.

Amortization of premium or discount:

Lot, Inc.: Premium amortization = $2,250 5 = $450 per year.

Interest Expense:

Lot, Inc.: $8,000 − $450 = $7,550 per year.

(2)

December 31, 2014

Lot

Max

Par

Liabilities

Bonds Payable

$100,000

$100,000

$100,000

Less: Discount on Bonds Payable

(1,600)**

Plus: Premium on Bonds Payable

1,800*

3,200***

Carrying Value of Bonds Payable

$101,800

$ 98,400

$103,200

*Lot, Inc. $2,250 − $450 = $1,800 ***Par, Inc. $4,000 − $800 = $3,200

7-10

**Max, Inc. $2,000 − $400 = $1,60ATC 7-2 (cont.)

c. The amount of interest expense is different for each of the three companies because the issue

d. The amount of interest paid is the same for each of the companies because the face value of

the bond and the interest rate is the same for all three.

ATC 7-3

Theses answers are based on Dominion Resources December 30, 2012 and Lowe’s February 1,

2013 Form 10-Ks. All dollar amounts are in millions.

a. Lowe’s financed 57.6% of its assets with liabilities as of February 1, 2013.

b. A company in the business of generating and supplying electric and gas power is less

likely to be adversely affected by a weak economy. People use electricity even if they are

c. According to Note 6 – Short-term Borrowings and Lines of Credit, Lowe’s has several

ACT 7-4

b. The amount of debt seems excessive in view of the fact that the amount of interest on the

c. Since YUM will have a net loss after interest, it will not pay any income taxes.

7-11

d. An explanation of how YUM could meet its debt payments would be that there is

sufficient cash flow to pay debt. With a large amount of depreciation (a noncash

ATC 7-5

a. David’s scheme made Global’s financial statements appear much better than what they

actually were. If the liabilities are not reported in the balance sheet, it will result in

b. David’s most glaring violation of the Code of Professional Conduct is that of Article II,

The Public Interest. His scheme served to mislead the general public and all unaware

c. The three elements of the fraud triangle are opportunity, pressure and rationalization.

Since David’s scheme required the cooperation of another party and the collusion of

upper management, the opportunity to commit fraud was less. However, upper