1-1

PROBLEM 1-32 b. (cont.)

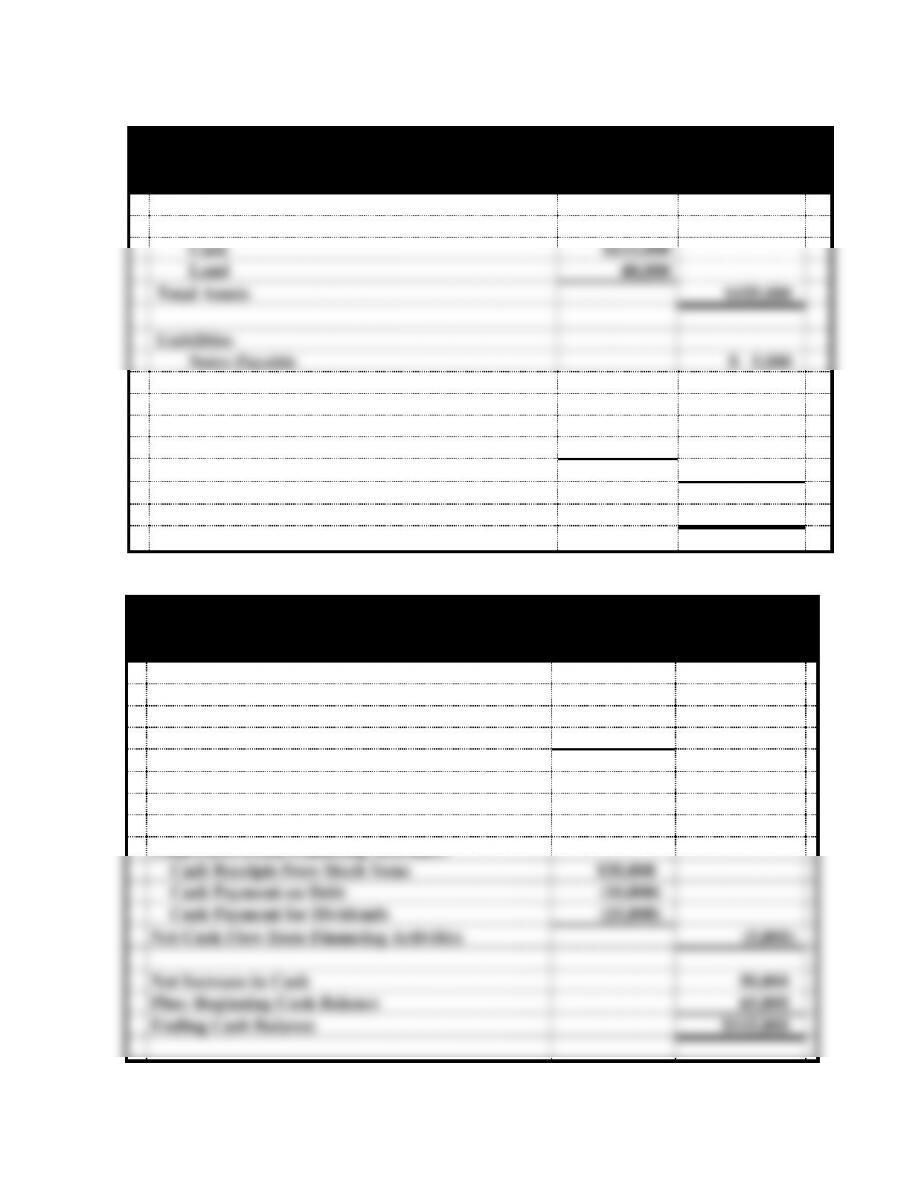

Susan’s Consulting

Balance Sheet

As of December 31, 2015

Assets

Cash

$115,000

Land

40,000

Total Assets

$155,000

Liabilities

Notes Payable

$ 5,000

Stockholders’ Equity

Common Stock

$70,000

Retained Earnings

80,000

Total Stockholders’ Equity

150,000

Total Liabilities and Stockholders’ Equity

$155,000

PROBLEM 1-32 b. (cont.)

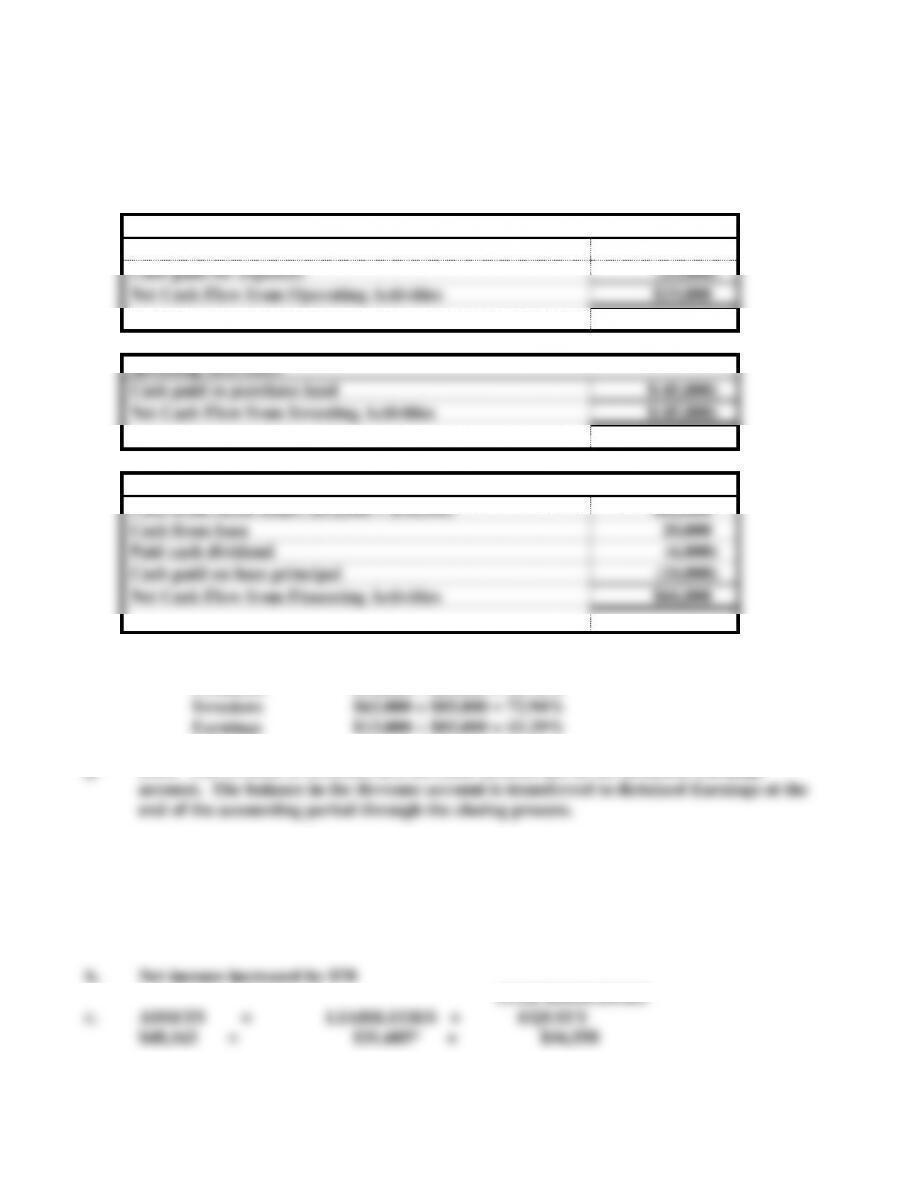

Susan’s Consulting

Statement of Cash Flows

For the Year Ended December 31, 2015

Cash Flows From Operating Activities:

Cash Receipts from Customers

$130,000

Cash Payments for Expenses

(75,000)

Net Cash Flow from Operating Activities

$55,000

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Cash Receipts from Stock Issue

$20,000

Cash Payment on Debt

(10,000)

Cash Payment for Dividends

(15,000)

Net Cash Flow from Financing Activities

(5,000)

Net Increase in Cash

50,000

Plus: Beginning Cash Balance

65,000

Ending Cash Balance

$115,000

1-2

c. Retained earnings does not contain cash.

e. Immediately after Event 2 in 2014 is recorded the balance in the Retained Earnings

The 2014 ending balance in Retained Earnings becomes next year’s beginning balance.

Thus, the balance in the Retained Earnings account on January 1, 2015 is $40,000. This

$40,000.

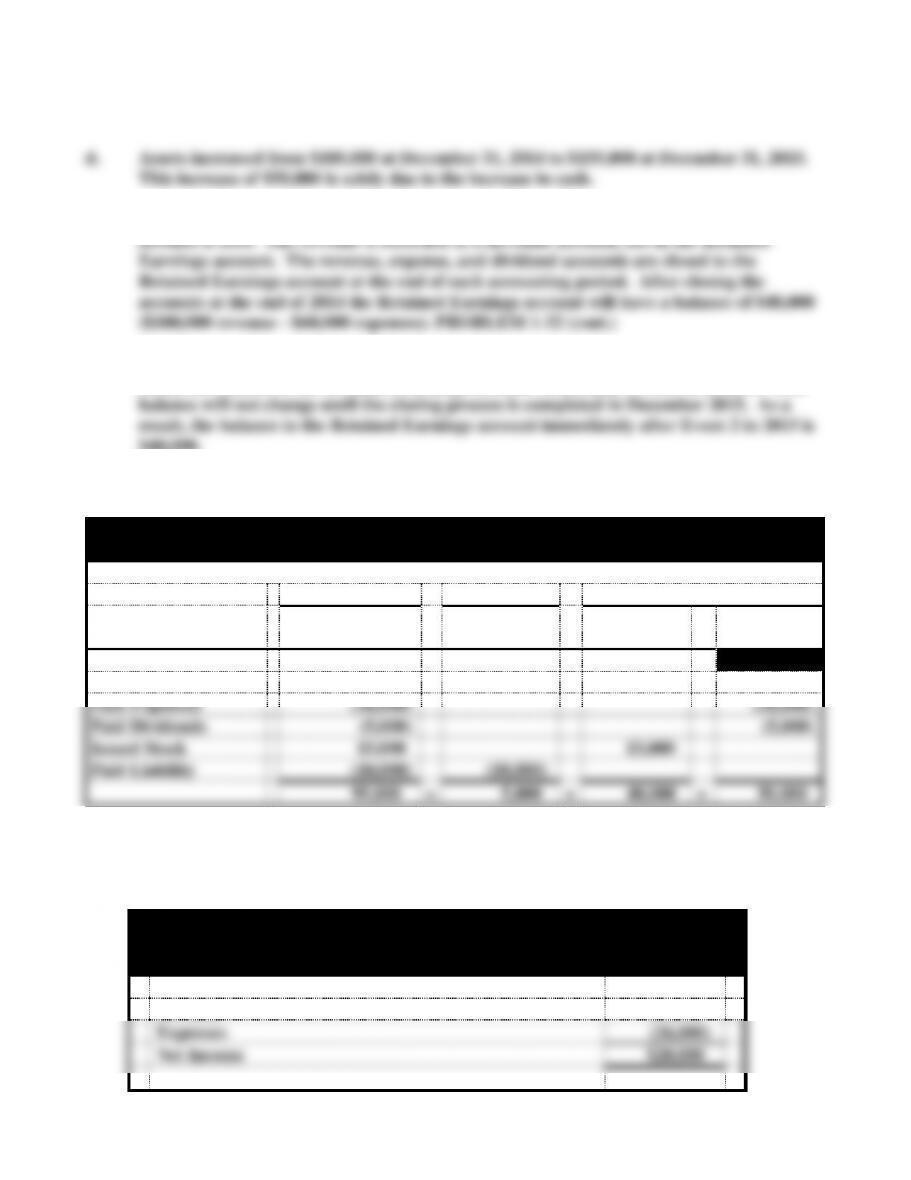

PROBLEM 1-33

Not required:

Crawford Enterprises

Accounting Equation

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

=

Liabilities

+

Common

Stock

+

Retained

Earnings

Beg. Balances

75,000

15,000

25,000

35,000

Earned Revenue

46,000

46,000

Paid Expenses

(26,000)

(26,000)

Paid Dividends

(5,000)

(5,000)

Issued Stock

15,000

15,000

Paid Liability

(10,000)

(10,000)

95,000

=

5,000

+

40,000

+

50,000

a.

Crawford Enterprises

Income Statement

For the Period Ended December 31, 2014

Revenue

$46,000

Expenses

(26,000)

Net Income

$20,000

1-3

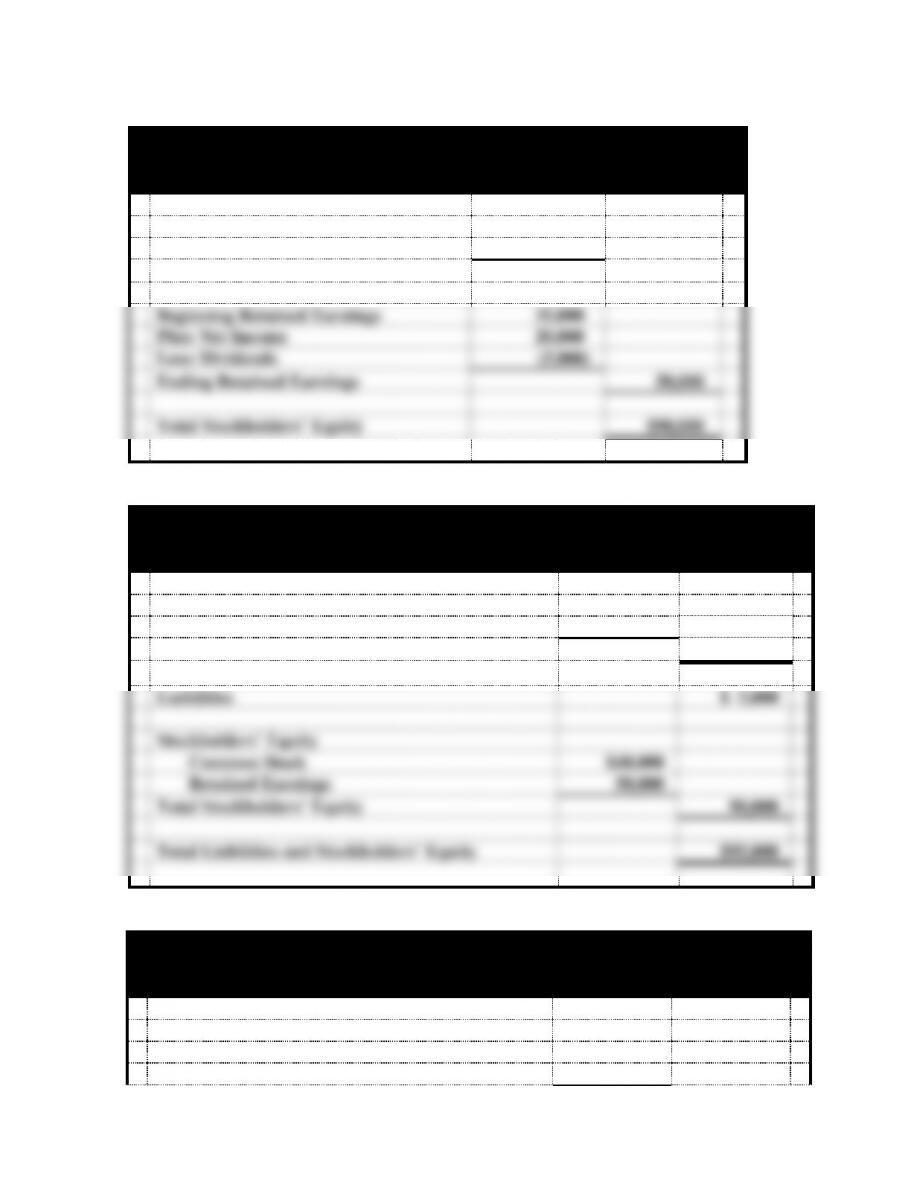

PROBLEM 1-33 a. (cont.)

Crawford Enterprises

Statement of Changes in Stockholders’ Equity

For the Period Ended December 31, 2014

Beginning Common Stock

$25,000

Plus: Common Stock Issued

15,000

Ending Common Stock

$40,000

Beginning Retained Earnings

35,000

Plus: Net Income

20,000

Less: Dividends

(5,000)

Ending Retained Earnings

50,000

Total Stockholders’ Equity

$90,000

Crawford Enterprises

Balance Sheet

As of December 31, 2014

Assets

Cash

$95,000

Total Assets

$95,000

Liabilities

$ 5,000

Stockholders’ Equity

Common Stock

$40,000

Retained Earnings

50,000

Total Stockholders’ Equity

90,000

Total Liabilities and Stockholders’ Equity

$95,000

PROBLEM 1-33 a. (cont.)

Crawford Enterprises

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash Flows From Operating Activities:

Cash Receipts from Customers

$46,000

Cash Payments for Expenses

(26,000)

1-4

Net Cash Flow from Operating Activities

$20,000

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Cash Receipts from Stock Issue

15,000

Cash Payments to Creditors

(10,000)

Cash Dividend to Stockholders

(5,000)

Net Cash Flow from Financing Activities

-0-

Net Increase in Cash

20,000

Plus: Beginning Cash Balance

75,000

Ending Cash Balance

$95,000

b. Percentage of assets provided by:

Creditors $ 5,000 ÷ $95,000 = 5.26%

c. The balance in the temporary accounts, revenue, expenses and dividends will be zero on

1-5

a.

Davidson Company

Horizontal Statements Model for 2014

Balance Sheet

Income Statement

Statement of

Assets

=

Liab.

+

Stockholders’ Equity

Revenue

−

Expense

=

Net Inc.

Cash Flows

Event

No.

Cash

+

Land

=

Notes

Payable

+

Common

Stock

+

Retained

Earnings

1

52,000

NA

NA

52,000

NA

NA

NA

NA

52,000 FA

2

20,000

NA

20,000

NA

NA

NA

NA

NA

20,000 FA

3

42,000

NA

NA

NA

42,000

42,000

NA

42,000

42,000 OA

4

(23,000)

NA

NA

NA

(23,000)

NA

23,000

(23,000)

(23,000) OA

5

(6,000)

NA

NA

NA

(6,000)

NA

NA

NA

(6,000) FA

6

10,000

NA

NA

10,000

NA

NA

NA

NA

10,000 FA

7

(10,000)

NA

(10,000)

NA

NA

NA

NA

NA

(10,000) FA

8

(45,000)

45,000

NA

NA

NA

NA

NA

NA

(45,000) IA

9

NA

NA

NA

NA

NA

NA

NA

NA

NA

Total

40,000

+

45,000

=

10,000

+

62,000

+

13,000

42,000

−

23,000

=

19,000

40,000 NC

b. Total Assets = $40,000 + $45,000 = $85,000

c.

Sources of Assets

Event

1. Issue of stock

$ 52,000

2. Cash from loan

20,000

3. Cash from revenue

42,000

6. Issue of stock

10,000

Total Sources of Assets

$124,000

1-6

PROBLEM 1-34 (cont.)

d. Net income is $19,000 (see part a.) Dividends are not expenses so they do not appear on the

income statement.

e.

Operating Activities:

Cash from customers

$42,000

Cash paid for expenses

(23,000)

Net Cash Flow from Operating Activities

$19,000

Investing Activities:

Cash paid to purchase land

$(45,000)

Net Cash Flow from Investing Activities

$(45,000)

Financing Activities:

Cash from stock issues ($52,000 + $10,000)

$62,000

Cash from loan

20,000

Paid cash dividend

(6,000)

Cash paid on loan principal

(10,000)

Net Cash Flow from Financing Activities

$66,000

f. Percentage of assets provided by:

Creditors $10,000 ÷ $85,000 = 11.76%

g. Zero. The revenue is recorded in a Revenue account not in the Retained Earnings

SOLUTIONS TO ANALYZE, THINK, COMMUNICATE – CHAPTER 1

ATC 1-1 (All dollar amounts are in millions.)

a. $2,999

* Liabilities must be computed by subtracting equity from assets.

1-7

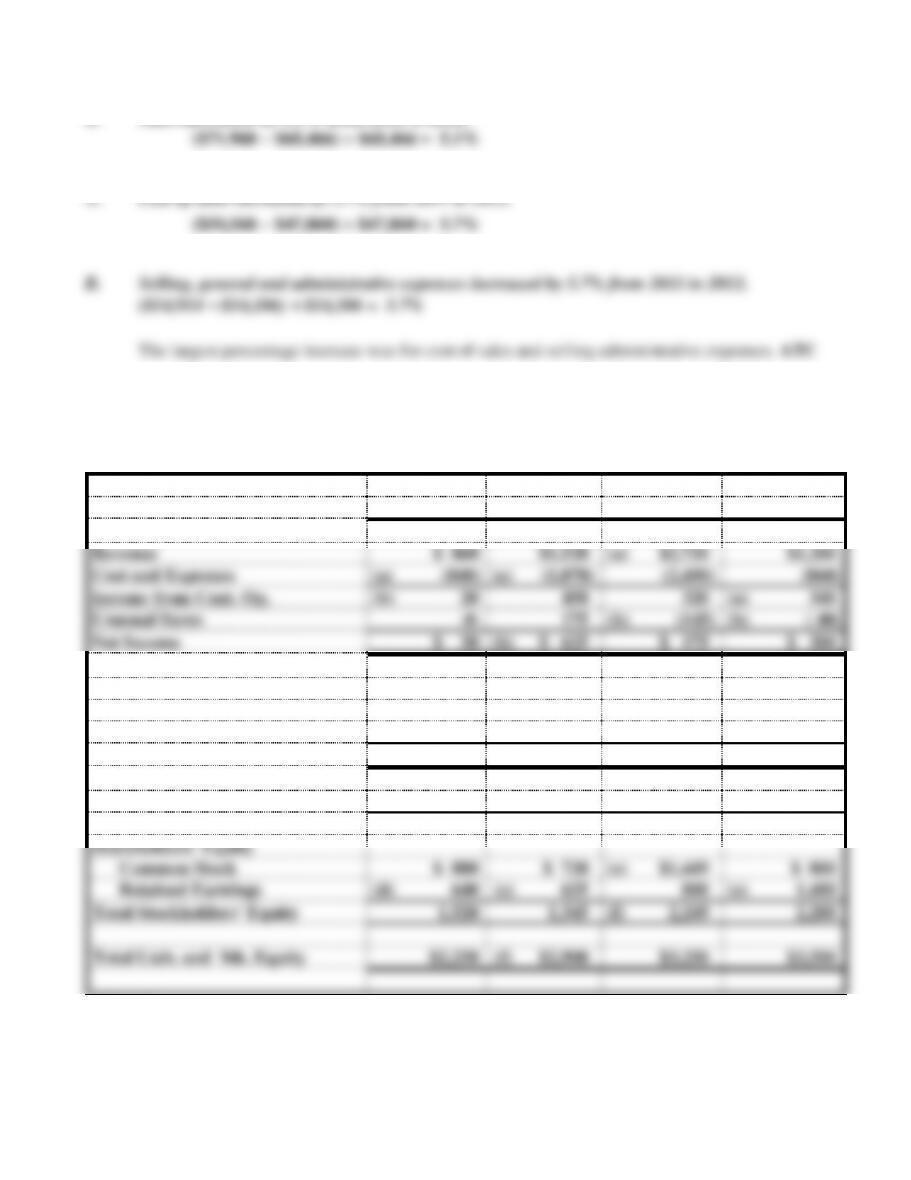

d. Sales increased by 5.1% from 2011 to 2012.

A. Cost of sales increased by 5.7% from 2011 to 2012.

1-2

a.

Income Statements (amounts given are in millions)

2017

2016

2015

2014

Revenue

$ 860

$1,520

(a) $2,720

$1,200

Cost and Expenses

(a) (840)

(a) (1,070)

(2,400)

(860)

Income from Cont. Op.

(b) 20

450

320

(a) 340

Unusual Items

-0-

175

(b) (145)

(b) ( 40)

Net Income

$ 20

(b) $ 625

$ 175

$ 300

Balance Sheets

Cash and Marketable Sec.

$ 350

$1,720

(c) $ 750

$ 940

Other Assets

1,900

(c) 1,180

2,500

(c) 2,560

Total Assets

$2,250

$2,900

(d) $3,250

$3,500

Liabilities

(c) $ 730

(d) $1,555

$1,001

(d) $1,300

Stockholders’ Equity

Common Stock

$ 880

$ 720

(e) $1,449

$ 800

Retained Earnings

(d) 640

(e) 625

800

(e) 1,400

Total Stockholders’ Equity

1,520

1,345

(f) 2,249

2,200

Total Liab. and Stk. Equity

$2,250

(f) $2,900

$3,250

$3,500

ATC 1-3

This solution is based on McDonald’s 2012 financial report.

1-8

a. McDonald’s net income for 2012, 2011, and 2010 were as follows:

b. The company had $35,386.5 million of assets at the end of 2012.

d. For 2012, the company’s:

net cash flow from operating activities were $6,966.1 million

ATC 1-4

This problem is designed to test written communication skills. The memo should describe the

balance sheet and the income statement. It should explain that the balance sheet is a statement

of assets, liabilities, and stockholders’ equity at the date of the financial statement. The income

statement gives the amount of revenues and expenses for the designated period. The memo

should also define each of the following terms:

Assets