3-1

ANSWERS TO QUESTIONS – CHAPTER 3

1. Merchandise inventory is finished goods that are held for sale to customers. Costs that are

2. Product costs are costs associated with goods for resale, usually inventory costs. Selling and

3. Cost of goods available for sale is the total of inventory on hand at the beginning of the period plus

inventory purchased during the period.

4. The cost of the items that have not been sold are allocated to merchandise inventory (asset) and are

goods sold (expense) and are shown on the income statement.

5. Period costs are expensed in the period they are incurred or used. Product costs are expensed in

the period in which the inventory is sold.

6. Net Sales $600,000

Ending Merchandise Inventory $ 75,000 (shown in balance sheet)

7. Under a perpetual inventory system, the balance in the inventory account is increased each time

goods are purchased and decreased each time goods are sold. The major advantage of the

8. a. Assets increase, stockholders’ equity increases – The balance sheet, statement of cash flows,

and statement of changes in stockholders’ equity are affected.

b. Assets increase, stockholders’ equity increases – This is similar to an acquisition of cash

affected.

3-2

d. Assets both increase and decrease (cash increases, inventory decreases) and stockholders’

statement of cash flows are affected.

9. Assets would both increase and decrease (cash increases by $20,000 and inventory decreases by

10. If goods are shipped FOB shipping point, the buyer is responsible for the shipping costs.

12. The $80 transportation-in is a product cost and is added to the Merchandise Inventory account.

The $135 transportation-out is a period cost and is added to the expense account Transportation-out.

13. When allowances are granted it is usually because the customer received inferior or damaged

14. 2/10 n/30 means that a 2% discount may be taken off of the selling price if payment is made

30 days.

15. If the $5,000 is for the purchase of inventory, this is an asset exchange in that inventory is

16. Cash discounts are offered to customers to encourage prompt payment.

18. The net amount of $4,000 will be added to the inventory account. If the invoice is paid within the

19. Purchase returns refer to the situation where the buyer of the goods returns them. Sales returns

refer to the situation where goods sold by the seller are returned to the seller. A sales return on the

3-3

20. Gross margin is net sales less cost of goods sold and relates the sales of primary products. Gain

21. The multistep income statement provides more information on the results of various business

22. Common size income statements covering several accounting periods help management identify

have been rising disproportionately with sales and take corrective action.

23. When using the periodic method of accounting for inventory, the schedule of cost of goods sold is

24. When using the periodic inventory system, a temporary account, Purchases, is used to accumulate

the purchases transactions for the year. Inventory is not adjusted until the end of the accounting

The periodic inventory system is easy to use in that when goods are sold, the cost of goods sold

One of the primary disadvantages of the periodic system is that the business owner has no account

of the amount of lost, stolen or damaged goods. Also, it is difficult to determine the amount of

25. The periodic inventory system does not separate the cost of lost, damaged, or stolen merchandise

3-4

SOLUTIONS TO EXERCISES – CHAPTER 3

EXERCISE 3-1

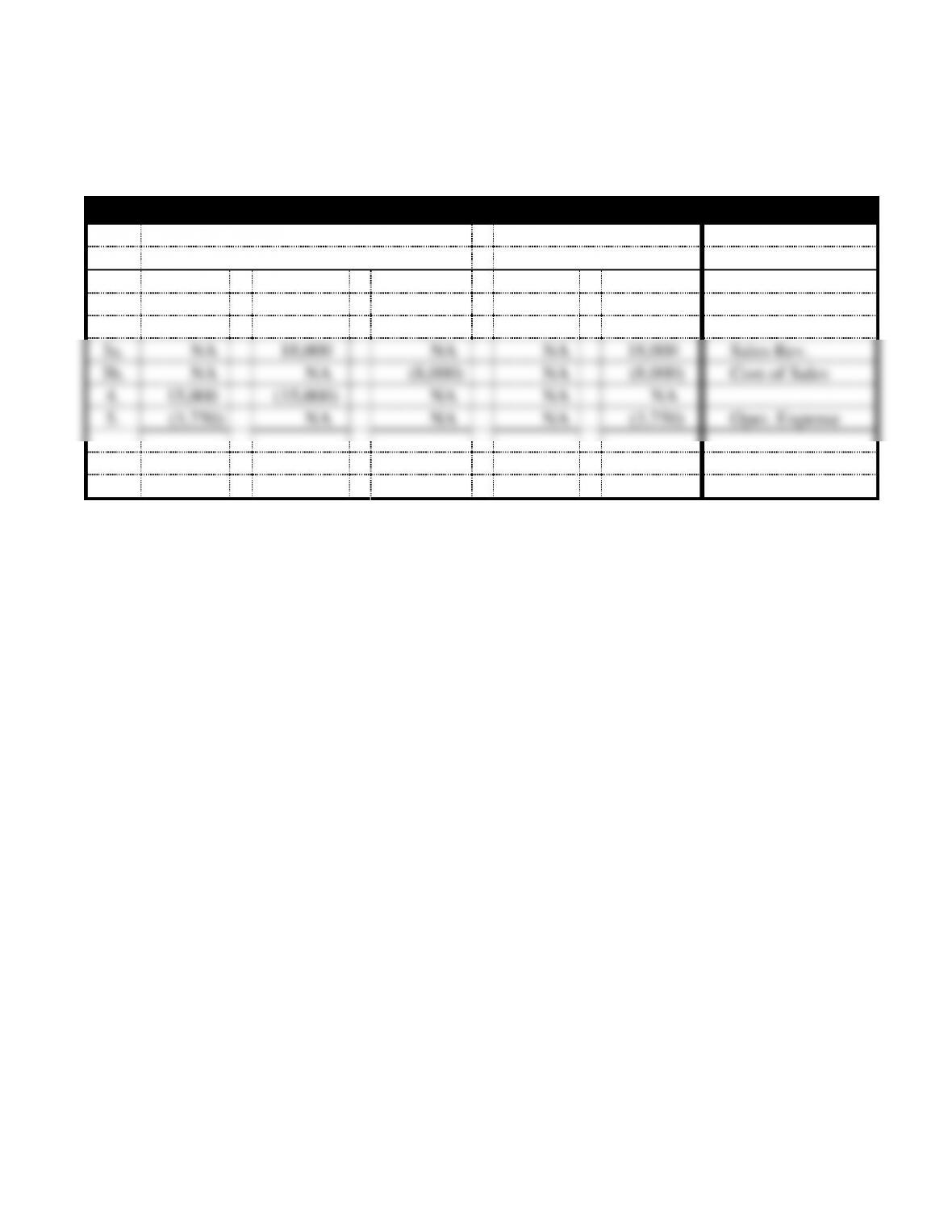

a.

Laura’s Flowers Effect of Events on the Accounting Equation

Assets

=

Equity

Acct. Title for RE

No.

Cash

+

A. Rec.

+

Inv.

=

C. Stock

+

Ret. Earn.

1.

20,000

NA

NA

20,000

NA

2.

(14,000)

NA

14,000

NA

NA

3a.

NA

18,000

NA

NA

18,000

Sales Rev.

3b.

NA

NA

(8,000)

NA

(8,000)

Cost of Sales

4.

15,000

(15,000)

NA

NA

NA

5.

(3,750)

NA

NA

NA

(3,750)

Oper. Expense

Tot.

17,250

+

3,000

+

6,000

=

20,000

+

6,250

3-5

EXERCISE 3-1 (cont.)

b.

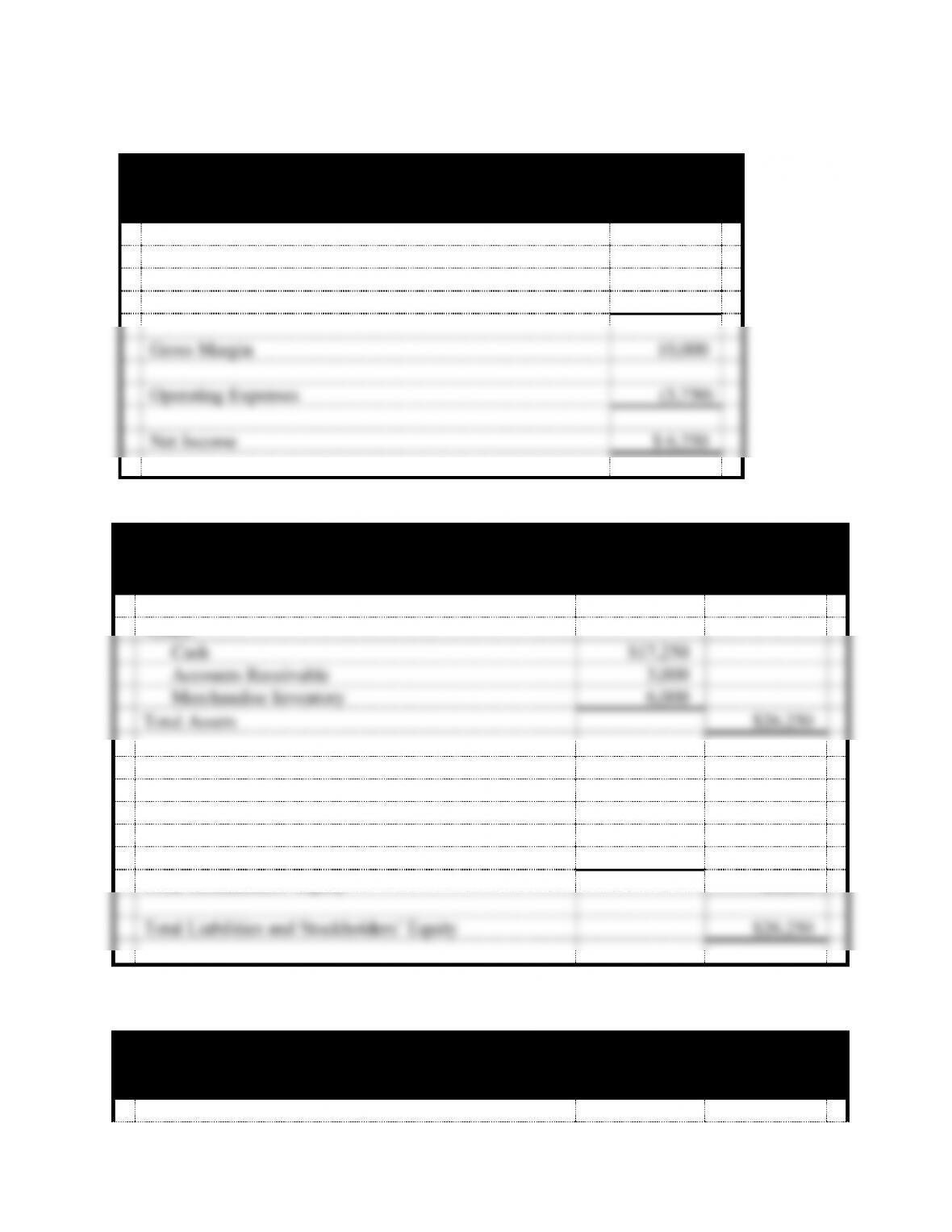

Laura’s Flowers

Income Statement

For the Year Ended December 31, 2014

Net Sales

$18,000

Cost of Goods Sold

(8,000)

Gross Margin

10,000

Operating Expenses

(3,750)

Net Income

$ 6,250

Laura’s Flowers

Balance Sheet

As of December 31, 2014

Assets

Cash

$17,250

Accounts Receivable

3,000

Merchandise Inventory

6,000

Total Assets

$26,250

Liabilities

$ -0-

Stockholders’ Equity

Common Stock

$20,000

Retained Earnings

6,250

Total Stockholders’ Equity

26,250

Total Liabilities and Stockholders’ Equity

$26,250

EXERCISE 3-1 b. (cont.)

Laura’s Flowers

Statement of Cash Flows

For the Year Ending December 31, 2014

3-6

Cash Flows From Operating Activities:

Inflow from Customers

$15,000

Outflow for Inventory

(14,000)

Outflow for Expenses

(3,750)

Net Cash Flow from Operating Activities

$(2,750)

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Cash Inflow from Stock Issue

20,000

Net Change in Cash

17,250

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$17,250

c. Yes, Laura could recover more than half of her investment in the common stock ($20,000). She

collected $15,000 of the sales on account and paid $3,750 in operating expenses. Her ending cash

EXERCISE 3-2

a.

Lewis CPAs

Income Statement

For the Year Ended December 31, 2014

Revenue

Service Revenue

$60,000

Expenses

Salaries Expense

(40,000)

Net Income

$20,000

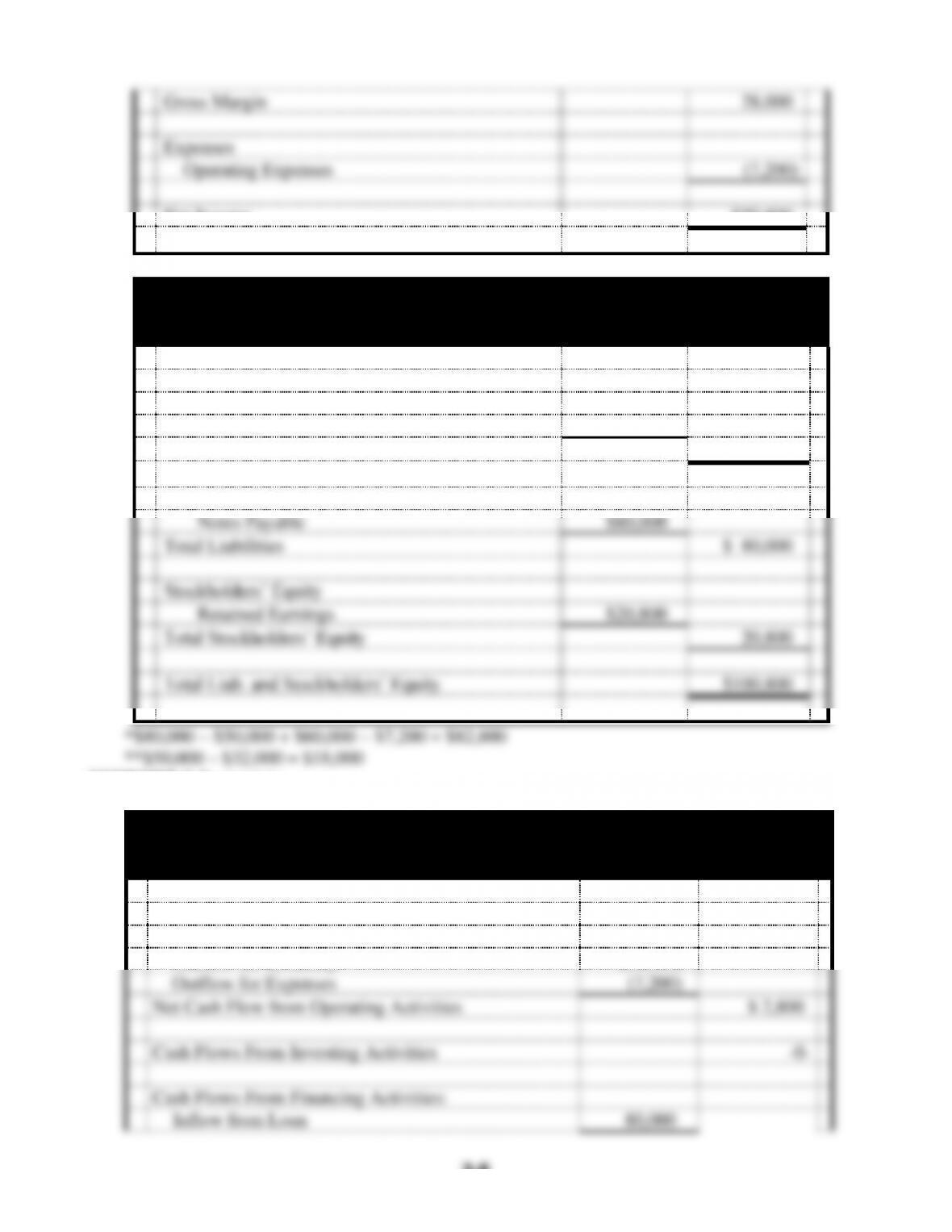

Lewis CPAs

Balance Sheet

As of December 31, 2014

Assets

Cash*

$100,000

3-7

Total Assets

$100,000

Liabilities

Notes Payable

$80,000

Total Liabilities

$80,000

Stockholders’ Equity

Retained Earnings

$20,000

Total Stockholders’ Equity

20,000

Total Liab. and Stockholders’ Equity

$100,000

*$80,000 + $60,000 − $40,000 = $100,000

EXERCISE 3-2 a. (cont.)

Lewis CPAs

Statement of Cash Flows

For Year Ended December 31, 2014

Cash Flows From Operating Activities:

Inflow from Clients

$60,000

Outflow for Salaries

(40,000)

Net Cash Flow from Operating Activ.

$20,000

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Inflow from Loan

$80,000

Net Cash Flow from Financing Activ.

80,000

Net Increase in Cash

100,000

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$100,000

EXERCISE 3-2 a. (cont.)

Casual Clothing

Income Statement

For the Year Ended December 31, 2014

Net Sales Revenue

$60,000

Cost of Goods Sold

(32,000)

3-8

Gross Margin

28,000

Expenses

Operating Expenses

(7,200)

Net Income

$20,800

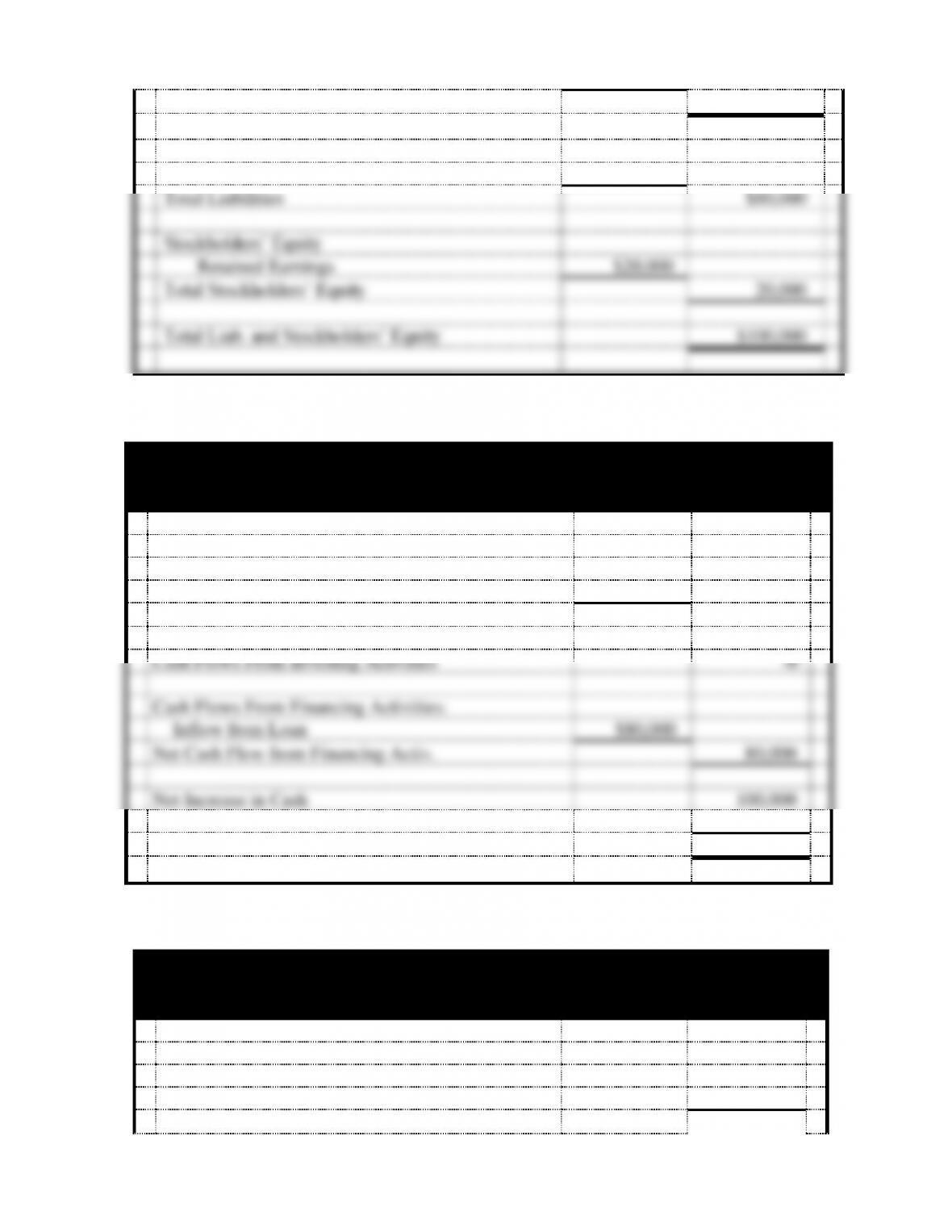

Casual Clothing

Balance Sheet

As of December 31, 2014

Assets

Cash*

$82,800

Merchandise Inventory**

18,000

Total Assets

$100,800

Liabilities

Notes Payable

$80,000

Total Liabilities

$ 80,000

Stockholders’ Equity

Retained Earnings

$20,800

Total Stockholders’ Equity

20,800

Total Liab. and Stockholders’ Equity

$100,800

EXERCISE 3-2a. (cont.)

Casual Clothing

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash Flows From Operating Activities:

Inflow from Customers

$60,000

Outflow for Inventory

(50,000)

Outflow for Expenses

(7,200)

Net Cash Flow from Operating Activities

$ 2,800

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Inflow from Loan

80,000

3-9

Net Cash Flow from Financing Activities

80,000

Net Increase in Cash

82,800

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$82,800

b. Casual Clothing is a merchandising business and has inventory and cost of goods sold — product

costs. Lewis is a service business and does not have product costs.

d. The asset in common is cash. The only asset that Lewis has is cash. Casual Clothing has cash but

3-10

EXERCISE 3-3

a.

Justin Swords Merchandising Effect of Events on Fianancial Statements

Assets

=

Equity

Rev.

−

Exp.

=

Net. Inc.

Cash Flow

No.

Cash

+

Inv.

=

C. Stock

+

Ret. Earn.

1.

70,000

NA

70,000

NA

NA

NA

NA

70,000 FA

2.

(60,000)

60,000

NA

NA

NA

NA

NA

(60,000) OA

3a.

82,000

NA

NA

82,000

82,000

NA

82,000

82,000 OA

3b.

NA

(48,000)

NA

(48,000)

NA

48,000

(48,000)

NA

Tot.

92,000

+

12,000

=

70,000

+

34,000

82,000

−

48,000

=

34,000

92,000 NC