Indicate whether each of the following statements is true or false.

1) Deposits in transit appear on the bank statement as credit memos

2) Service fees charged by a bank appear on bank statements as debit memos

3) Credit memos in a bank statement describe transactions that act to increase the bank’s

liabilities

4) Outstanding checks do not appear on the bank statement

5) Debit memos in a bank statement describe transactions that act to increase the

depositor’s assets

A dollar to be received in the future is subject to the effects of risk and inflation.

Asset use transactions always involve the payment of cash.

Indicate whether each of the following statements about cash receipts is true or false.

1) A record of all cash collections should be made immediately upon receipt

2) Cash that a business collects late in the day should be deposited with the next day’s

cash receipts

3) The amount of cash on hand, including petty cash, should be counted periodically

4) Giving a written receipt to customers who pay cash is part of a business’s internal

controls over cash

5) A business should minimize the amount of cash that it keeps on hand

Under the terms of the Sarbanes-Oxley Act, a company and its external auditor are

required to report on the effectiveness of the company’s system of internal controls.

In a market, consumers are resource providers.

Where should a company undergoing reorganization report the gains and losses

resulting from the reorganization?

A.on the statement of retained earnings.

B.on the income statement, combined with the gains and losses from operations.

C.on the statement of stockholders’ equity.

D.on the income statement, separate from other gains and losses.

E.on the statement of cash flows.

Hacienda Company issued common stock for $250,000 cash. As a result of this event,

A.assets increased.

B.retained earnings increased.

C.equity increased.

D.assets increased and equity increased.

Using the form below, record each of the following 2013 transactions for Morris

Corporation:

a) Nov. 1 Received cash from clients for services to be performed over the next six

months, $6,000.

b) Nov. 1 Paid $600 for a 12-month insurance policy.

c) Dec. 31 Recorded expiration of two months of the insurance.

d) Dec. 31 Earned $2,000 of the amount received from clients in November.

A customary assumption in capital budgeting analysis is that:

A.the desired rate of return includes the effects of compounding.

B.the cash inflows generated by the investment are not reinvestment.

C.annual cash flows occur at the beginning of each period.

D. the time value of money is ignored.

Burton Company sold land for $25,000 cash. The original cost of the land was $25,000.

Select the answer that indicates how this event affects the company’s financial

statements.

A.

B.

C.

D.

During 2013, Saranac Company earned $12,000 of cash revenue and paid $8,200 of

cash expenses and $600 in dividends to the company’s owners. Enter each of these three

events into the horizontal financial statements model, below. Indicate dollar amounts of

increases and decreases. For cash flows, show whether they are operating activities

(OA), investing activities (IA), or financing activities (FA).

Kenyon Company uses accrual accounting. Indicate whether each of the following

statements regarding Kenyon’s accounting system is true or false.

_____ a) The recognition of accounting events and the realization of cash consequences

may occur in different accounting periods.

_____ b) The cash consequence of a transaction always precedes its accounting

recognition.

_____ c) Expenses may either be matched to revenues they produce or to periods in

which they are incurred.

_____ d) Kenyon may record accrual transactions, but may not record deferral

transactions.

_____ e) Kenyon is not permitted to make cash sales.

Liabilities are shown on the

A.income statement.

B.balance sheet.

C.statement of cash flows.

D.statement of changes in stockholders’ equity.

Randall Company manufactures chocolate bars. The following were among Randall’s

2013 manufacturing costs:

Randall’s 2013 direct labor costs amounted to:

A.$400,000

B.$300,000

C.$175,000

D.$375,000

The Poole Company reported the following income for 2014:

What is the company’s net margin?

A.73%

B.40%

C.18%

D.27%

The advantages of the partnership form of business organization, compared to

corporations, include

A.single taxation.

B.ease of raising capital.

C.mutual agency.

D.limited liability.

E.difficulty of formation.

Assuming all of the following expenses have priority, in what order are they prioritized?

A.Administrative expenses, employee claims for wages, unpaid taxes, claims for the

return of customer deposits.

B.Employee claims for wages, unpaid taxes, administrative expenses, claims for the

return of customer deposits.

C.Unpaid taxes, administrative expenses, employee claims for wages, return of

customer deposits.

D.Administrative expenses, employee claims for wages, claims for the return of

customer deposits, unpaid taxes.

E.Unpaid taxes, return of customer deposits, employee claims for wages, administrative

expenses.

The length of time required to recover the initial investment in a capital asset is known

as the:

A.the rate of return.

B.investment period.

C.present value period.

D. payback period.

The Jefferson Company is a manufacturer of antique reproduction furniture. Which

term best describes Jefferson’s role in society?

A.Consumer

B.Regulatory Agency

C.Conversion Agent

D.Resource Owner

On January 1, 2013, Lamb and Mona LLP admitted Noris to a 20% interest in net assets

for an investment of $50,000 cash. Prior to the admission of Noris, Lamb and Mona had

net assets of $100,000 and an income-sharing ratio of 25% to Lamb and 75% to Mona.

After the admission of Noris, the partnership contract included the following

provisions:

– Salary of $40,000 a year to Noris.

– Remaining net income in ratio Lamb 20%, Mona 60%, Noris 20%.

– During the fiscal year ended December 31, 2013, the partnership had income of

$90,000 prior to recognition of salary to Noris.

Record the journal entry to record the remainder of net income to the capital accounts.

A company acquired a new piece of equipment on January 1, 2011 at a cost of

$200,000. The equipment is expected to have a useful life of 10 years, a residual value

of $20,000 and is depreciated on a straight-line basis. On January 1, 2013, the

equipment was appraised and determined to have a fair value of $190,000 and a

residual value of $25,000 and a remaining useful life of 10 years.

At what amount should the equipment be reported on the December 31, 2013 balance

sheet under U.S. GAAP?

A.$160,000

B.$150,000

C.$146,000

D.$140,000

E.$116,000

The present value index indicates:

A.the time it will take to recover the initial cash outflow of an investment.

B.the additional cash inflows from operating activities.

C.the rate of return per dollar invested in a capital project.

D.the ratio of the net present value of an investment to the initial investment.

Which of the following items is an example of revenue?

A.Cash received from a bank loan

B.Cash received from customers at the time services were provided

C.Cash investments made by owners

D.All of these

Which of the following statements is true?

A.Balance sheet accounts are referred to as nominal accounts.

B.Balance sheet accounts are referred to as permanent accounts.

C.Dividends are permanent accounts.

D.All of these statements are true.

Why is the SEC’s Rule 14c-3 important to the accounting profession?

Norr and Caylor established a partnership on January 1, 2012. Norr invested cash of

$100,000 and Caylor invested $30,000 in cash and equipment with a book value of

$40,000 and fair value of $50,000. For both partners, the beginning capital balance was

to equal the initial investment. Norr and Caylor agreed to the following procedure for

sharing profits and losses:

– 12% interest on the yearly beginning capital balance

– $10 per hour of work that can be billed to the partnership’s clients

– the remainder divided in a 3:2 ratio

The Articles of Partnership specified that each partner should withdraw no more than

$1,000 per month.

For 2012, the partnership’s income was $70,000. Norr had 1,000 billable hours, and

Caylor worked 1,400 billable hours. In 2013, the partnership’s income was $24,000, and

Norr and Caylor worked 800 and 1,200 billable hours respectively. Each partner

withdrew $1,000 per month throughout 2012 and 2013.

Determine the amount of net income allocated to each partner for 2012.

Principal Company is a U.S.-based company that prepares its consolidated financial

statements in accordance with U.S. GAAP. Principal reported net income of $2,600,000

in 2013 and stockholders’ equity of $12,000,000 at December 31, 2013. Principal wants

to determine the reporting impact of switching to IFRS. The following three items

would create differences in financial reporting:

1) At December 31, 2013, inventory had a historical cost of $850,000, a replacement

cost of $700,000, and a net realizable value of $800,000. The normal profit margin was

10%.

2) Principal acquired a building at the beginning of 2011 at a cost of $5,000,000. The

building has an estimated useful life of 20 years, an estimated residual value of

$1,000,000, and is being depreciated on a straight-line basis. On January 1, 2013, the

building has a fair value of $5,500,000. There is no change in the estimated useful life

or residual value. In a switch to IFRS, Principal would use the revaluation model in IAS

16 to determine the carrying value of property, plant, and equipment subsequent to

acquisition.

3) In 2013, Principal incurred $800,000 of research and development for a new product,

of which 35% relates to development activities subsequent to the point at which criteria

indicating the creation of an intangible asset had been met. As of the end of 2013,

development of the new product had not been completed.

Required:

1) Prepare a schedule reconciling net income under U.S. GAAP to net income under

IFRS for the year ended December 31, 2013.

2) Prepare a schedule reconciling stockholders’ equity under U.S. GAAP to

stockholders’ equity under IFRS at December 31, 2013.

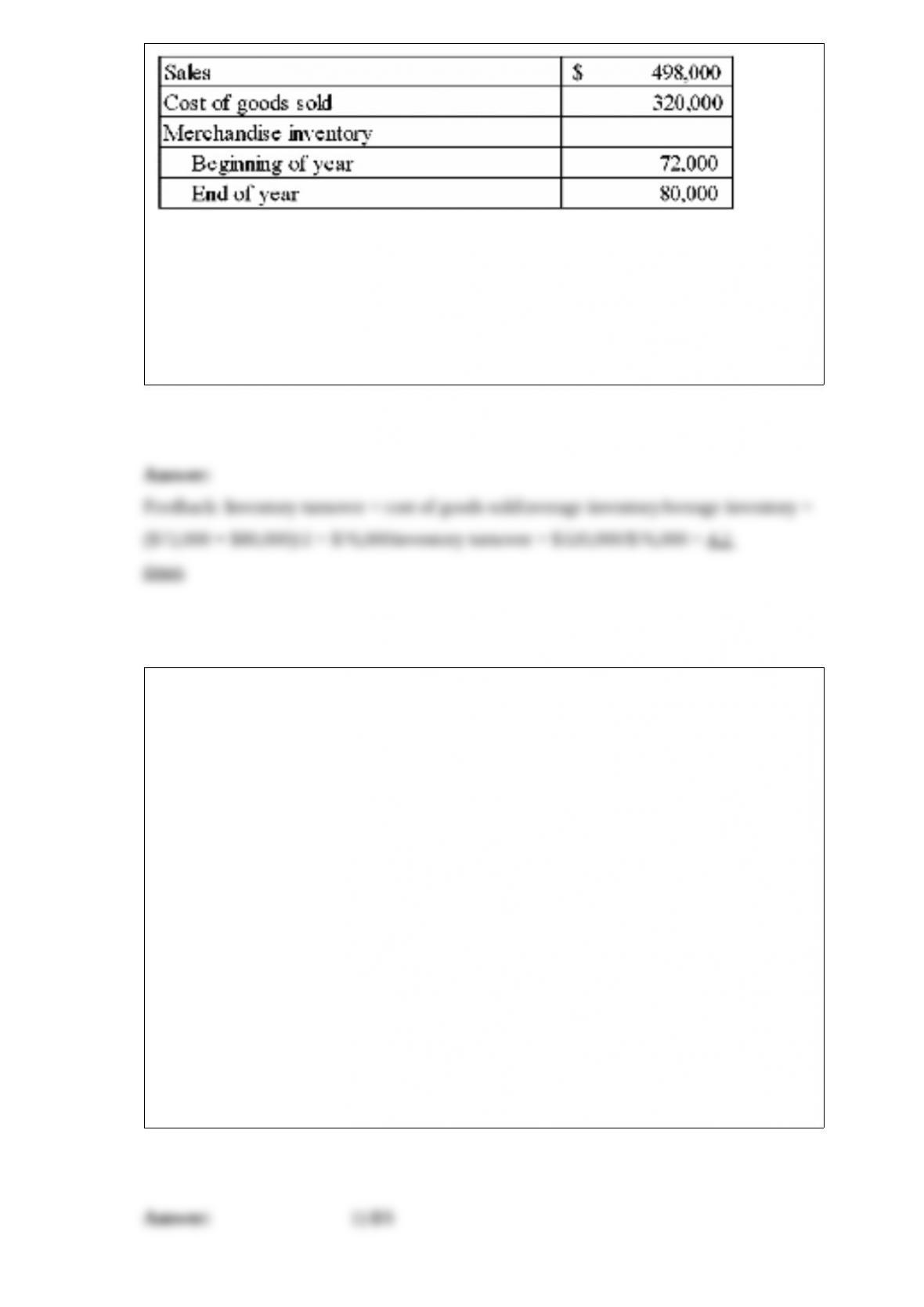

Selected financial information for Martin Company for 2014 follows:

Required:

How many times did Martin’s merchandise inventory turnover during 2014? Round

your answer to one decimal place.

Indicate for each of the following items if the item would be reported on the income

statement (IS), statement of changes in equity (CE), balance sheet (BS), or statement of

cash flows (CF). Some items may appear on more than one statement, if so, identify all

applicable statements.

1) Prepaid insurance

2) Dividends paid to stockholders

3) Interest revenue

4) Accounts payable

5) Salaries expense

6) Retained earnings

7) Unearned subscription revenue

8) Cash flows from operating activities

9) Beginning common stock

10) Issued stock to investors for cash

11) Salaries payable

12) Accounts receivable

For each of the following transactions, indicate the type by entering “AS” for asset

source transaction, “AU” for asset use transaction, “AE” for asset exchange transaction,

and “CE” for claims exchange transaction.

1) ____ The company paid $10,000 for a plot of land.

2) ____ Recorded the accrual of $1,000 in salaries to be paid later.

3) ____ The company issued common stock for $20,000 in cash.

4) ____ The business incurred operating expense on account.

5) ____ The business paid off its accounts payable.

6) ____ The business earned revenue to be collected next year.

7) ____ The company paid $2,000 in dividends to its stockholders.

8) ____ The business received cash from customers in #6 above.

9) ____ Paid the salaries accrued in #2 above.

10) ___ Borrowed money from a local bank.

Which two EU directives have helped harmonize accounting standards?

What is the meaning of the phrase debtor in possession?

What is meant by a “partially secured liability”?

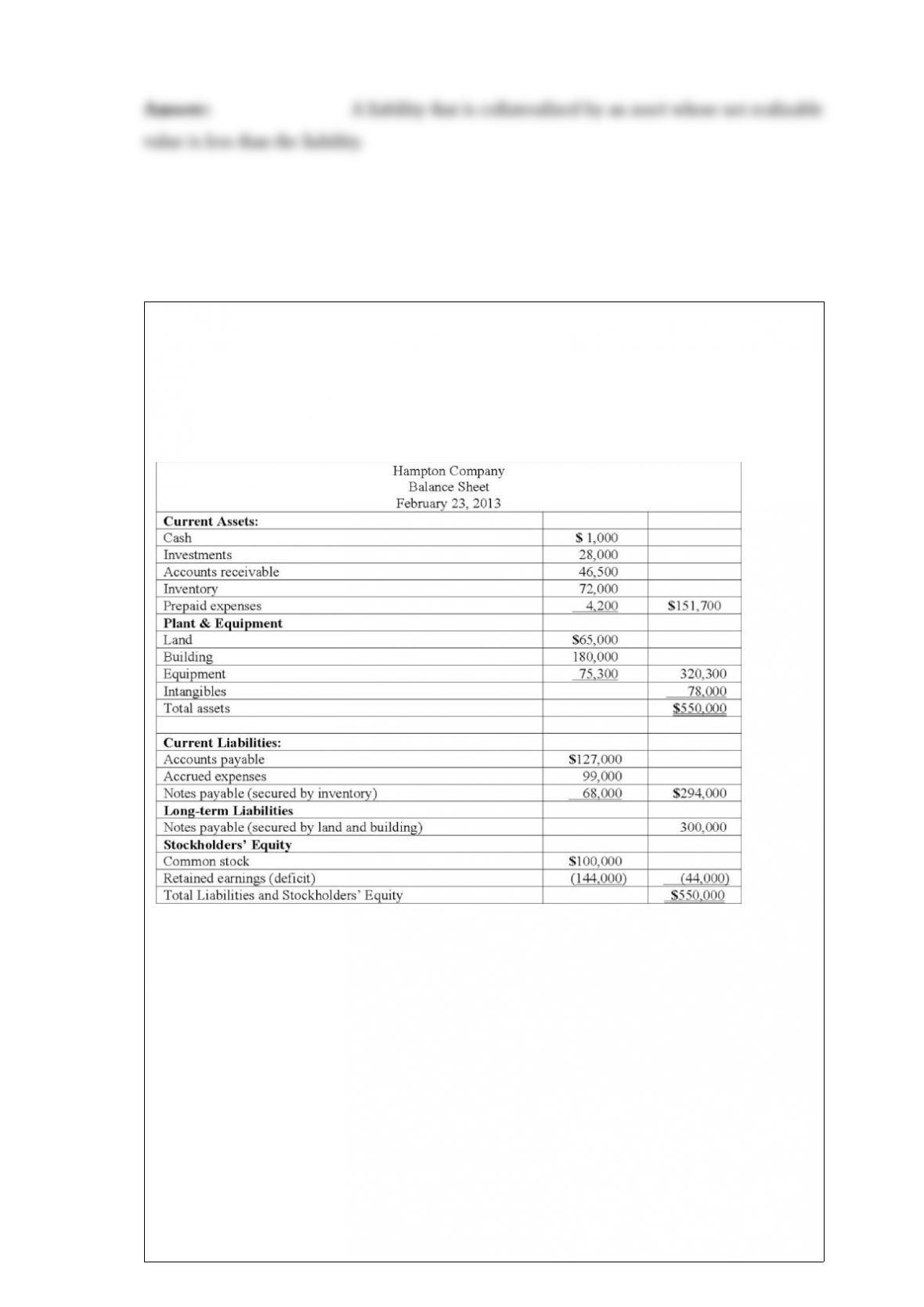

Hampton Company is trying to decide whether to seek liquidation or reorganization.

Hampton has provided the following balance sheet:

Additional information is as follows:

– The investments are currently worth $13,000.

– It is estimated that $32,000 of the accounts receivable are collectible.

– The inventory can be sold for $74,000.

– The prepaid expenses and the intangible assets have no net realizable value.

– The land and building are currently valued at $250,000.

– The equipment can be sold for $60,000.

– Administrative expenses (not yet recorded) are estimated to be $12,500.

– Accrued expenses include $17,000 of salaries payable ($11,000 to one employee and

$3,000 each to two other employees).

– Accrued expenses include $7,000 of unpaid payroll taxes.

How much will Hampton’s creditor of an unsecured accounts payable of $4,000

receive?