7-1

(3)

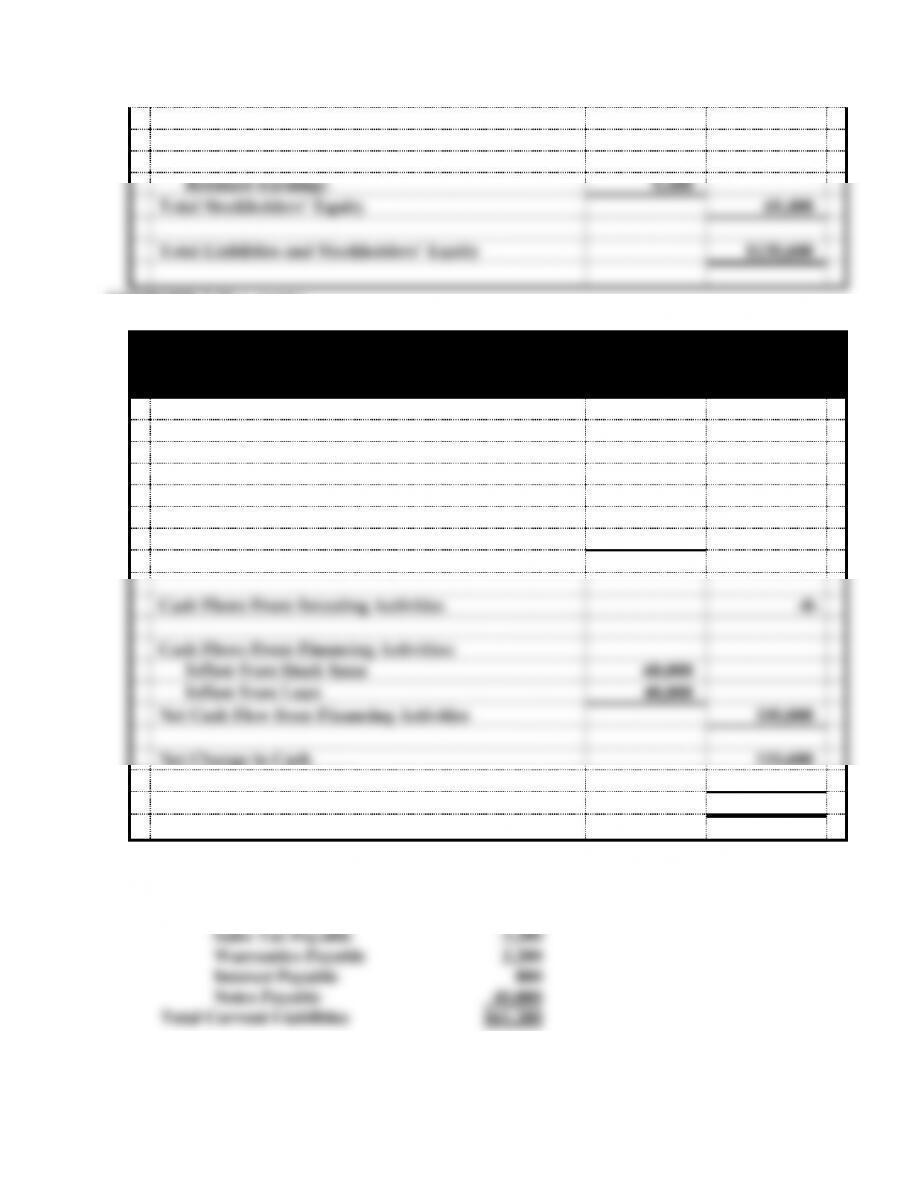

Cash Flows From Financing Activities:

Inflow from Issue of Note

$50,000

Outflow to Repay Note

(8,959)

Net Cash Flow from Financing Activities

$41,041

d. Principal 1/1/15: $41,041 (see schedule in book)

Interest Expense: $41,041 x 5% = $2,052.05 or $2,052 rounded to nearest

dollar.EXERCISE 7-12

Sims Co.

Effect of Transactions on Financial Statements

Balance Sheet

Income Statement

Statement of

Date

Assets

=

Liab.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

1/1

+

+

NA

NA

NA

NA

+ FA

1/31

−

NA

−

NA

+

−

− OA

2/1

+

+

NA

NA

NA

NA

+ FA

2/28

−

NA

−

NA

+

−

− OA

3/1

−

−

NA

NA

NA

NA

− FA

3/31

−

NA

−

NA

+

−

− OA

4/30

−

NA

−

NA

+

−

− OA

5/31

−

NA

−

NA

+

−

− OA

6/30

−

NA

−

NA

+

−

− OA

7/31

−

NA

−

NA

+

−

− OA

8/31

−

NA

−

NA

+

−

− OA

9/30

−

NA

−

NA

+

−

− OA

10/31

−

NA

−

NA

+

−

− OA

11/1

−

−

NA

NA

NA

NA

− FA

11/30

−

NA

−

NA

+

−

− OA

12/1

−

−

NA

NA

NA

NA

− FA

12/31

−

NA

−

NA

+

−

− OA

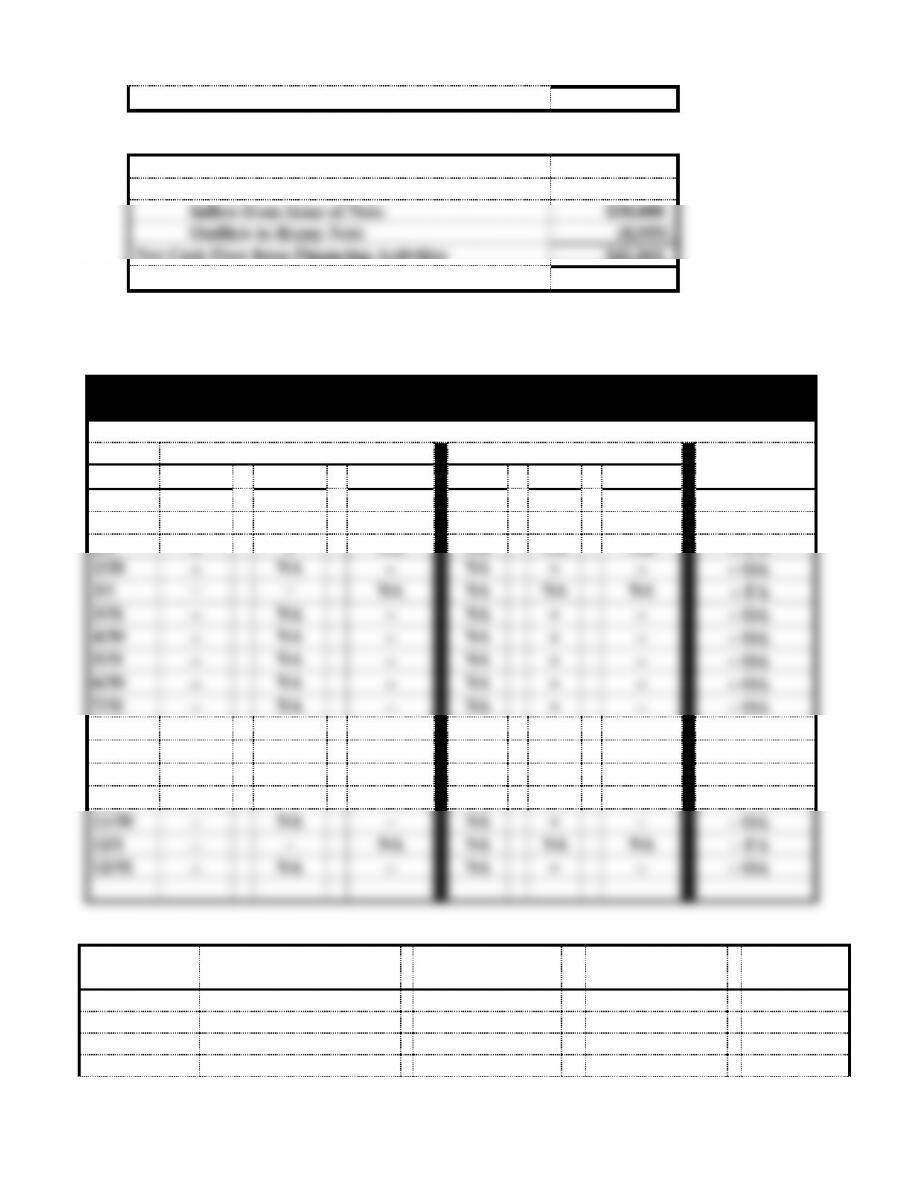

Computation of Interest Expense

Month

Amount

Borrowed (Repaid)

End of Month

Balance

x

Interest Rate per

Month

=

Interest

Expense

January

$60,000

$ 60,000

.06/12

$ 300

February

40,000

100,000

.06/12

500

March

(30,000)

70,000

.07/12

408

7-2

April

-0-

70,000

.07/12

408

May

-0-

70,000

.07/12

408

June

-0-

70,000

.07/12

408

July

-0-

70,000

.07/12

408

August

-0-

70,000

.07/12

408

September

-0-

70,000

.07/12

408

October

-0-

70,000

.07/12

408

November

(20,000)

50,000

.07/12

292

December

(10,000)

40,000

.06/12

200

Total

$4,556

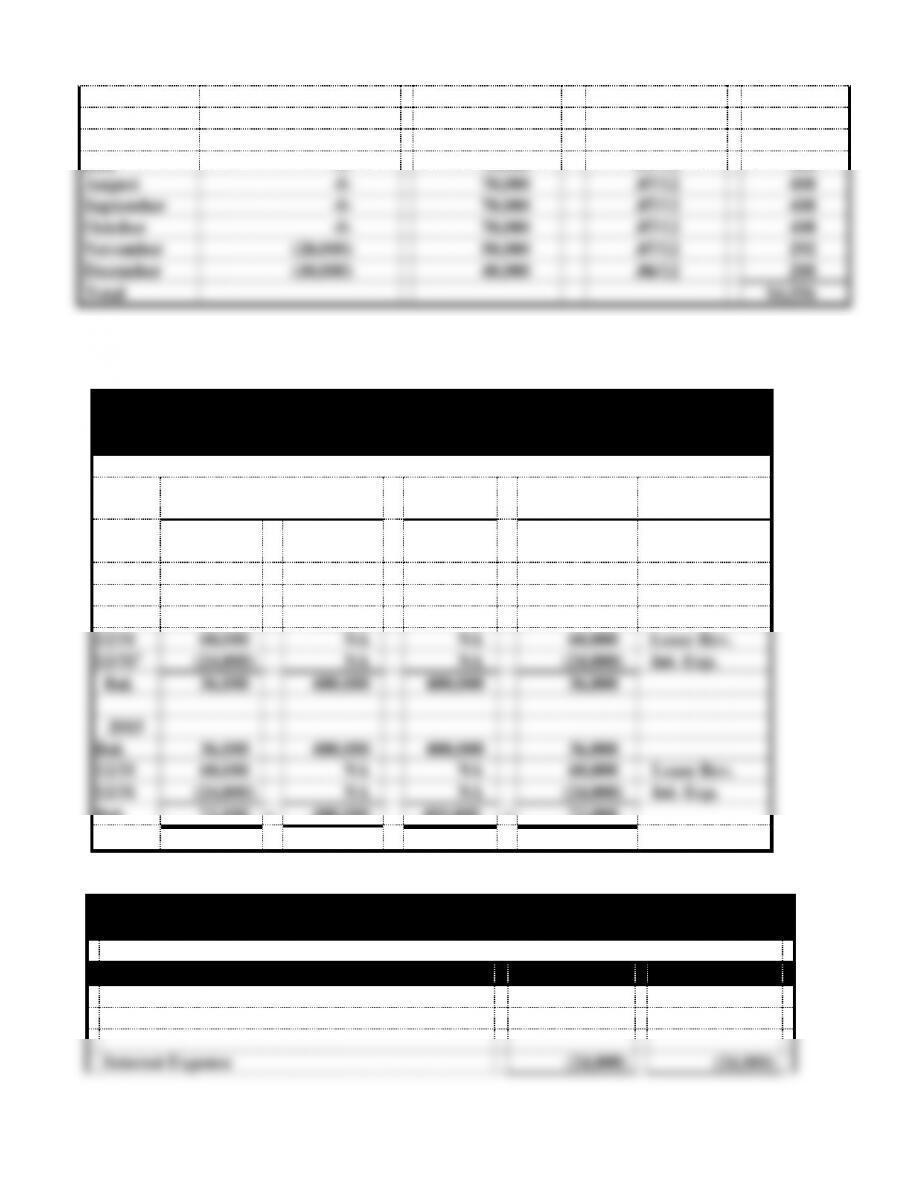

EXERCISE 7-13

a.

Chapman Co.

Effect of Events on the General Ledger

2014 and 2015

Assets

=

Liabilities

+

Stkholders’

Equity

Event

Cash

+

Land

=

Bonds

Pay.

+

Retained

Earnings

Acct. Title/RE

2014

1/1

400,000

NA

400,000

NA

1/1

(400,000)

400,000

NA

NA

12/31

60,000

NA

NA

60,000

Lease Rev.

12/311

(24,000)

NA

NA

(24,000)

Int. Exp.

Bal.

36,000

400,000

400,000

36,000

2015

Bal.

36,000

400,000

400,000

36,000

12/31

60,000

NA

NA

60,000

Lease Rev.

12/31

(24,000)

NA

NA

(24,000)

Int. Exp.

Bal.

72,000

+

400,000

400,000

+

72,000

1$400,000 x 6% = $24,000

EXERCISE 7-13 (cont.) b.

Chapman Company Financial Statements

For the Year Ended December 31

Income Statements

2014

2015

Lease Revenue

$60,000

$60,000

Interest Expense

(24,000)

(24,000)

7-3

Net Income

$36,000

$36,000

Balance Sheets

Assets

Cash

$ 36,000

$ 72,000

Land

400,000

400,000

Total Assets

$436,000

$472,000

Liabilities

Bonds Payable

$400,000

$400,000

Stockholders’ Equity

Common Stock

-0-

-0-

Retained Earnings

36,000

72,000

Total Stockholders’ Equity

36,000

72,000

Total Liab. and Stockholders’ Equity

$436,000

$472,000

Statements of Cash Flows

Cash Flows From Operating Activities:

Inflow from Revenue

$ 60,000

$ 60,000

Outflow for Interest

(24,000)

(24,000)

Net Cash Flow from Operating Act.

36,000

36,000

Cash Flows From Investing Activities:

Outflow to Purchase Land

(400,000)

-0-

Cash Flows From Financing Activities:

Inflow from Bond Issue

400,000

-0-

Net Change in Cash

36,000

36,000

Plus: Beginning Cash Balance

-0-

36,000

Ending Cash Balance

$ 36,000

$ 72,000

EXERCISE 7-14

a. $150,000 x 6% = $9,000

7-4

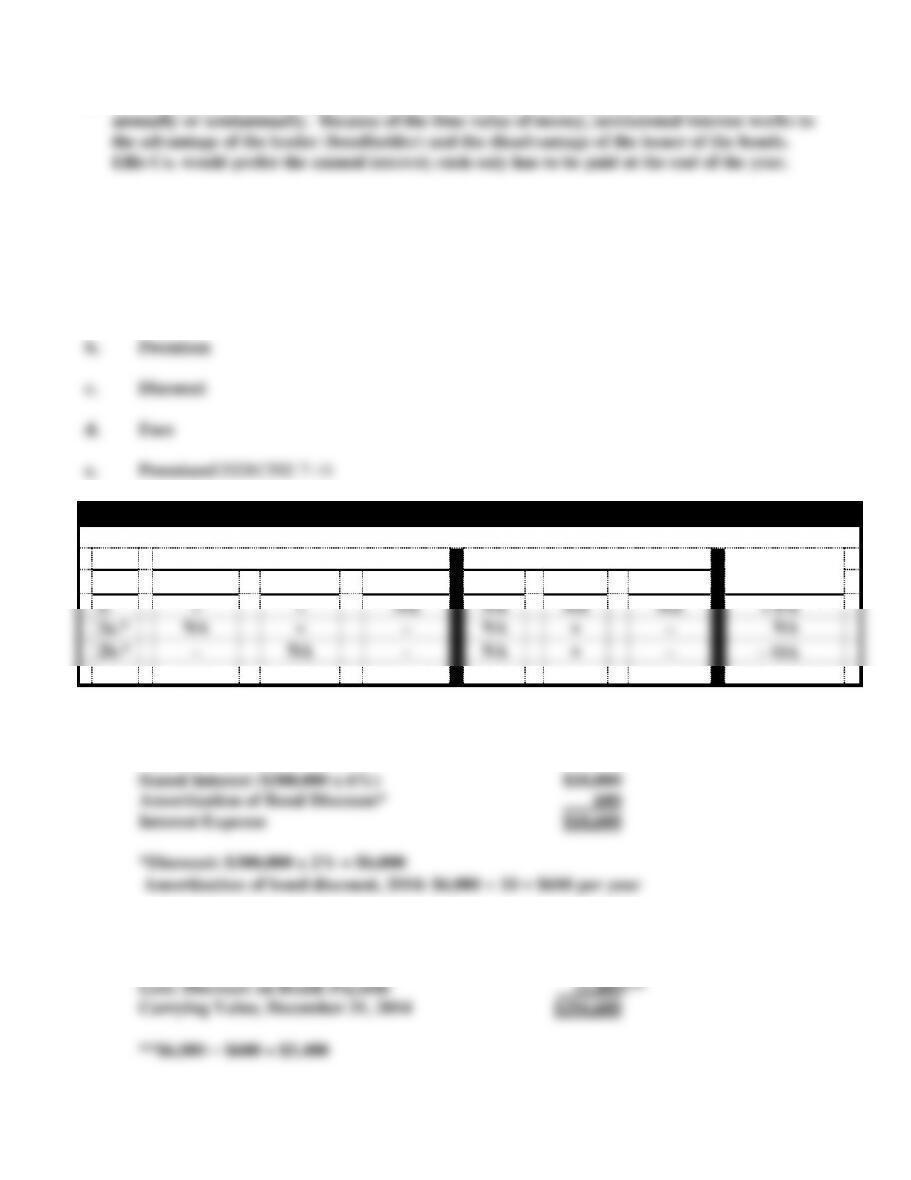

c. The total amount of interest paid each year will be the same regardless of whether it is paid

EXERCISE 7-15

a. Discount

a.

Effect of Transactions on Financial Statements

Balance Sheet

Income Statement

Statement of

No.

Assets

=

Liab.

+

S. Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

1.

+

+

NA

NA

NA

NA

+ FA

2a.*

NA

+

−

NA

+

−

NA

2b.*

−

NA

−

NA

+

−

− OA

*2a is amortization of discount; 2b is payment of interest.

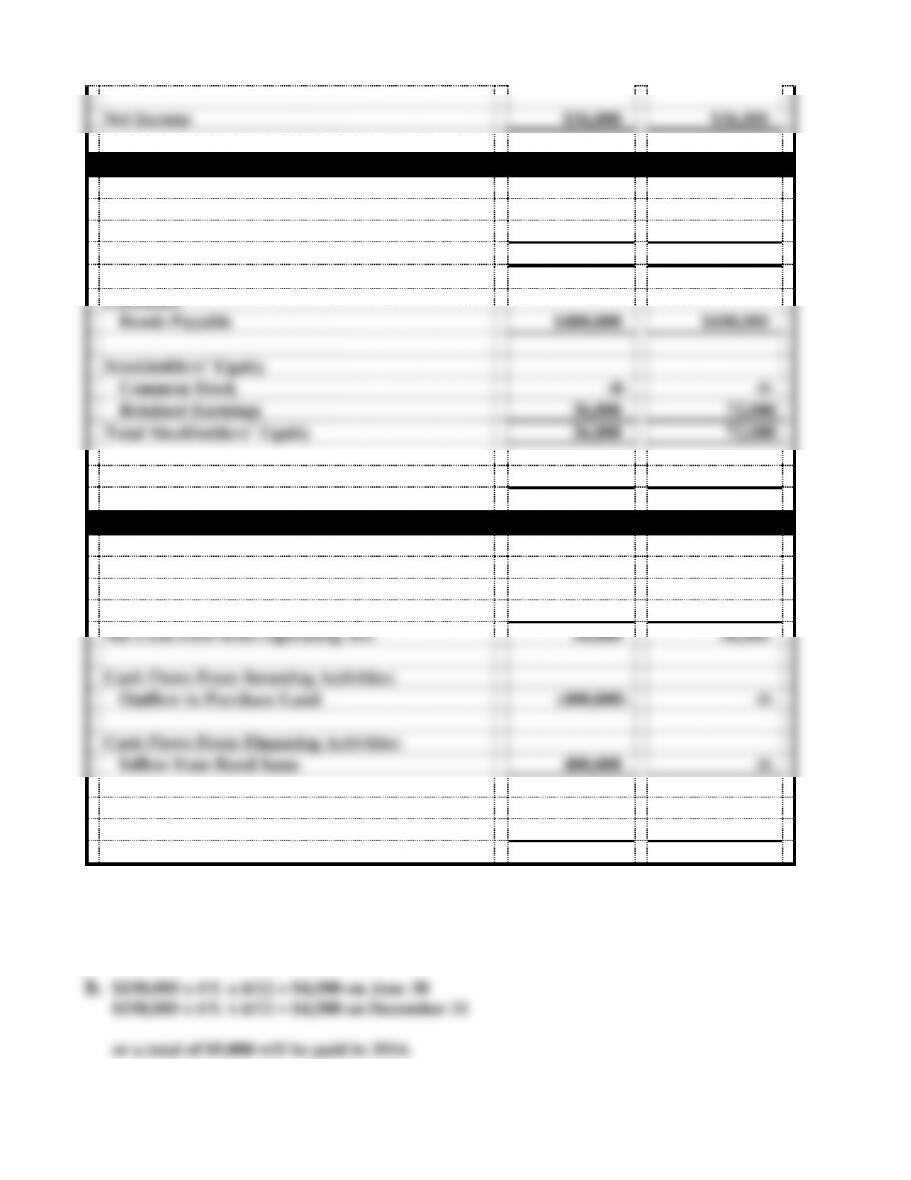

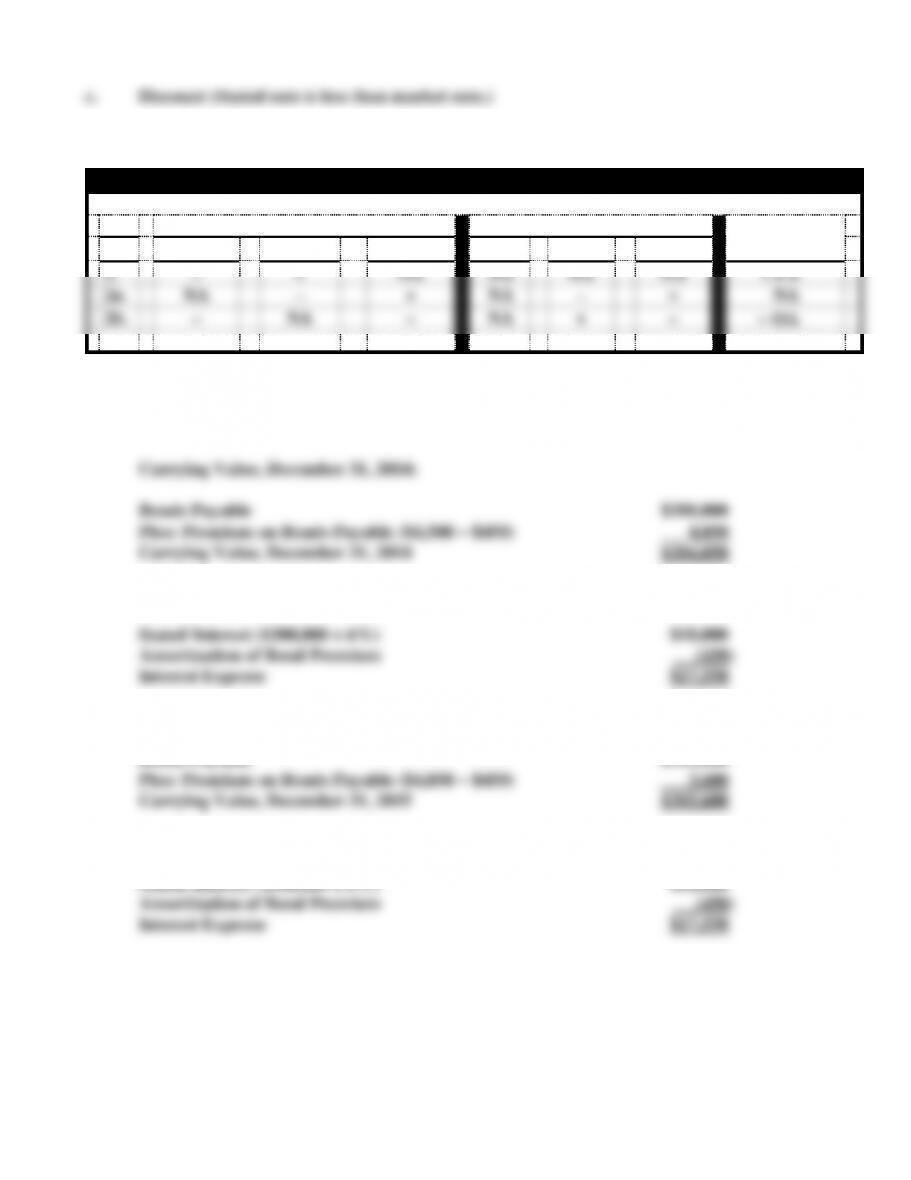

b. Interest Expense, 2014:

c. Carrying Value, December 31, 2014:

Bonds Payable $300,000

7-5

d. Interest Expense, 2015:

Stated Interest ($300,000 x 6%) $18,000

e. Carrying Value, December 31, 2015:

Bonds Payable $300,000

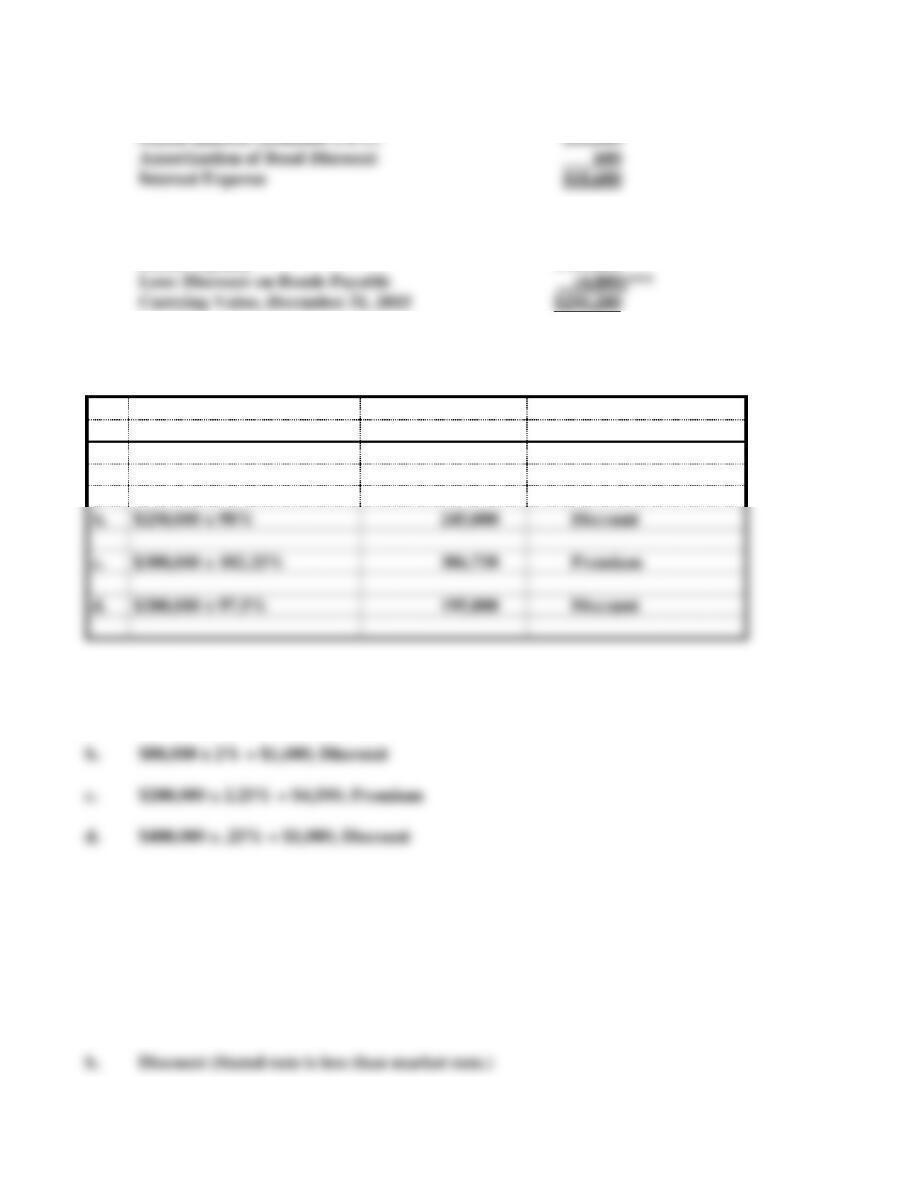

***$6,000 − $1,200 = $4,800EXERCISE 7-17

Face x Selling Price

Cash Proceeds

Discount or Premium

a.

$400,000 x 101%

$404,000

Premium

b.

$250,000 x 98%

245,000

Discount

c.

$300,000 x 102.25%

306,750

Premium

d.

$200,000 x 97.5%

195,000

Discount

EXERCISE 7-18

a. $120,000 x 1% = $1,200; Premium

EXERCISE 7-19

a. Premium (Stated rate is greater than market rate.)

7-6

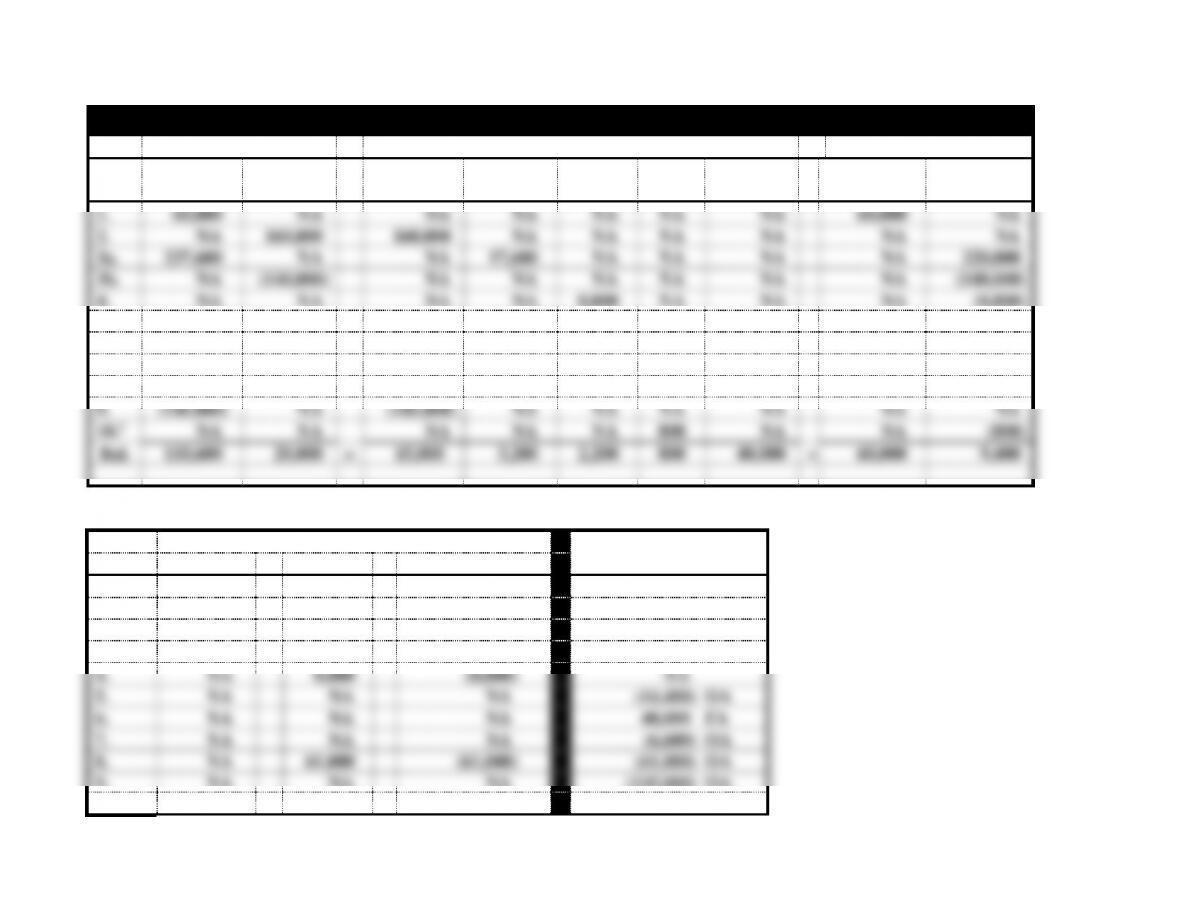

EXERCISE 7-20

a.

Effect of Transactions on Financial Statements

Balance Sheet

Income Statement

Stmt. of

No.

Assets

=

Liab.

+

S. Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

1.

+

+

NA

NA

NA

NA

+ FA

2a.

NA

−

+

NA

−

+

NA

2b.

−

NA

−

NA

+

−

− OA

b. Bond Premium: $300,000 x 1.5% = $4,500

Amortization of bond premium: $4,500 10 = $450 per year

c. Interest Expense, 2014:

d. Carrying Value, December 31, 2015:

Bonds Payable $300,000

e. Interest Expense, 2015:

Stated Interest ($300,000 x 6%) $18,000

7-7

EXERCISE 7-21 a.

Midsouth Equipment Sales Corp. Statements Model

Assets

=

Liabilities

+

Equity

No.

Cash

Inv.

=

Accts. Pay.

Sales Tax

Pay.

Warr.

Pay.

Int. Pay

Notes Pay.

+

Comm.

Stock

Ret. Earn.

1.

60,000

NA

NA

NA

NA

NA

NA

60,000

NA

2.

NA

160,000

160,000

NA

NA

NA

NA

NA

NA

3a.

237,600

NA

NA

17,600

NA

NA

NA

NA

220,000

3b.

NA

(140,000)

NA

NA

NA

NA

NA

NA

(140,000)

4.

NA

NA

NA

NA

8,800

NA

NA

NA

(8,800)

5.

(14,400)

NA

NA

(14,400)

NA

NA

NA

NA

NA

6.

40,000

NA

NA

NA

NA

NA

40,000

NA

NA

7.

(6,600)

NA

NA

NA

(6,600)

NA

NA

NA

NA

8.

(61,000)

NA

NA

NA

NA

NA

NA

NA

(61,000)

9.

(145,000)

NA

(145,000)

NA

NA

NA

NA

NA

NA

10.1

NA

NA

NA

NA

NA

800

NA

NA

(800)

Bal.

110,600

20,000

=

15,000

3,200

2,200

800

40,000

+

60,000

9,400

1$40,000 x 6% x 4/12 = $800.

Income Statement

Statement of

Event

Rev.

–

Exp.

=

Net Inc.

Cash Flows

1.

NA

NA

NA

60,000 FA

2.

NA

NA

NA

NA

3a.

220,000

NA

220,000

237,600 OA

3b.

NA

140,000

(140,000)

NA

4.

NA

8,800

(8,800)

NA

5.

NA

NA

NA

(14,400) OA

6.

NA

NA

NA

40,000 FA

7.

NA

NA

NA

(6,600) OA

8.

NA

61,000

(61,000)

(61,000) OA

9.

NA

NA

NA

(145,000) OA

10

NA

800

(800)

NA

7-8

EXERCISE 7-21 (cont.)

b.

Midsouth Equipment Sales Corp.

Income Statement

For the Year Ended December 31, 2014

Sales Revenue

$220,000

Cost of Goods Sold

(140,000)

Gross Margin

80,000

Expenses

Operating Expenses

$61,000

Warranty Expense

8,800

Total Operating Expenses

(69,800)

Operating Income

10,200

Interest Expense

(800)

Net Income

$ 9,400

EXERCISE 7-21 b. (cont.)

Midsouth Equipment Sales Corp.

Balance Sheet

As of December 31, 2014

Assets

Cash

$110,600

Merchandise Inventory

20,000

Total Assets

$130,600

Liabilities

Accounts Payable

$ 15,000

Sales Tax Payable

3,200

Warranties Payable

2,200

Interest Payable

800

Notes Payable

40,000

Total Liabilities

61,200

7-9

Stockholders’ Equity

Common Stock

$60,000

Retained Earnings

9,400

Total Stockholders’ Equity

69,400

Total Liabilities and Stockholders’ Equity

$130,600

EXERCISE 7-21 c. (cont.)

Midsouth Equipment Sales Corp.

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash Flows From Operating Activities:

Inflow from Customers

$220,000

Inflow from Sales Tax

17,600

Outflow for Inventory

(145,000)

Outflow for Expenses1

(67,600)

Outflow for Sales Tax

(14,400)

Net Cash Flow from Operating Activities

$10,600

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Inflow from Stock Issue

60,000

Inflow from Loan

40,000

Net Cash Flow from Financing Activities

100,000

Net Change in Cash

110,600

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$110,600

1. $61,000 + $6,600 = $67,600

c. Current Liabilities:

Accounts Payable $15,000

7-10

EXERCISE 7-22

Blackmon Co.

Classified Balance Sheet

As of December 31, 2014

Assets

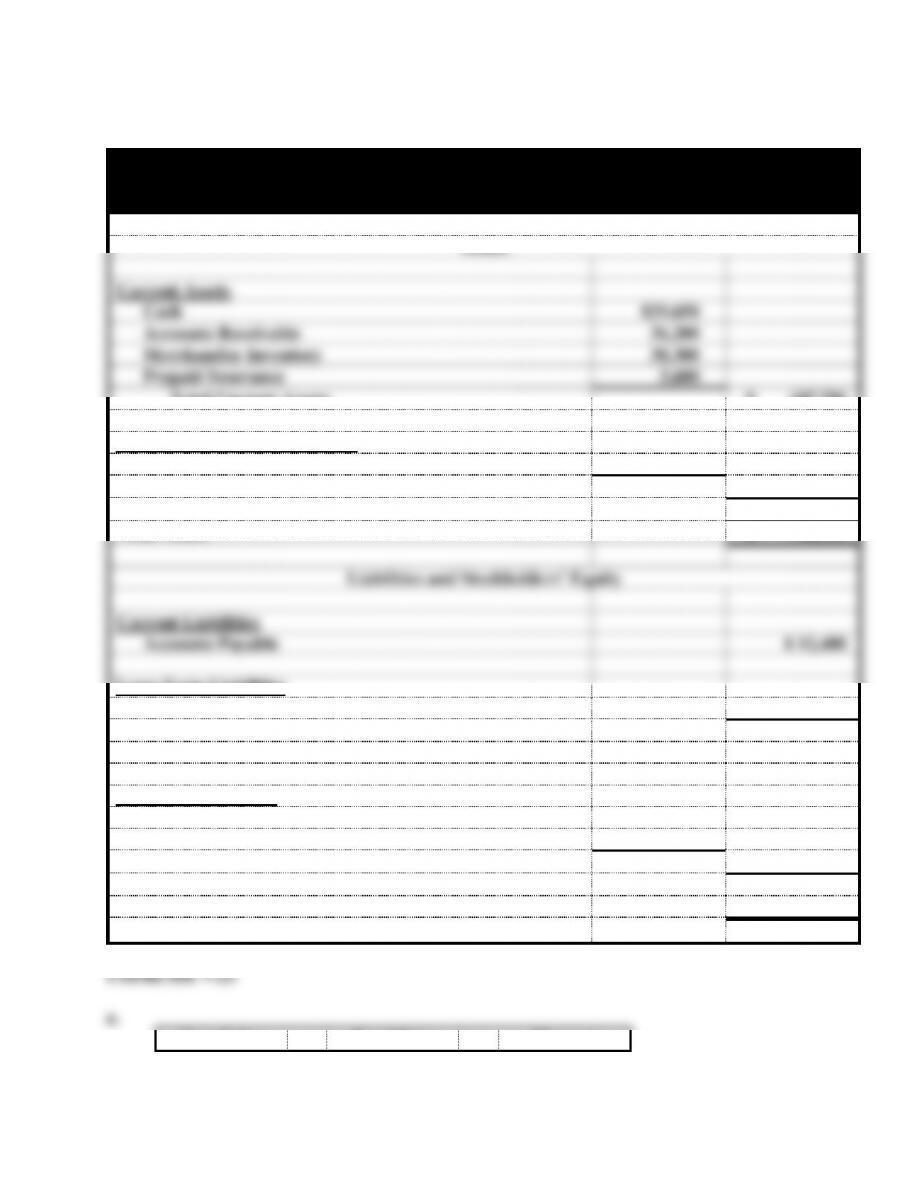

Current Assets

Cash

$29,650

Accounts Receivable

36,200

Merchandise Inventory

38,300

Prepaid Insurance

3,600

Total Current Assets

$ 107,750

Property, Plant and Equipment

Office Equipment

36,400

Total Property, Plant and Equipment

36,400

Total Assets

$ 144,150

Liabilities and Stockholders’ Equity

Current Liabilities

Accounts Payable

$ 12,400

Long-Term Liabilities

Long-Term Notes Payable

45,500

Total Liabilities

57,900

Stockholders’ Equity

Common Stock

$50,000

Retained Earnings

36,250

Total Stockholders’ Equity

86,250

Total Liabilities and Stockholders’ Equity

$144,150

Face Value

−

Bond Price

=

Discount

7-11

$250,000

−

$219,277

=

$30,723

b.

Carrying Value

x

Effective Rate

=

Interest Expense

$219,277

x

.10

=

$21,928

c. Compute the Ending Balance in the Discount Account

Face Value

x

Stated Rate

=

Cash Payment

$250,000

x

.08

=

$20,000

Interest Expense

−

Cash Payment

=

Amortization