Chapter 16 – Planning for Capital Investments

16-1

Teaching Notes for Chapter 16

Before this chapter, many students have not studied the time value of money concept.

Although students have some intuitive sense of the concept (they want their money now

rather than later), they frequently have trouble with applications such as computing

interest, analyzing cash flows, and reading interest tables. This chapter introduces the

time value of money concept. It is more important to teach the basic concept than it is to

cover all of the details. To this end, we focus only on determining present values. We

leave discussion of future values to advanced courses. Likewise, we limit discussion to

ordinary annuities, leaving treatment of annuities due to future courses. Still, many

students will find this chapter challenging. We caution you to move your class at a pace

that promotes understanding rather than memorization.

Detailed Outline of a Lesson Plan for Chapter 16

I. Open the class using an entertaining example with which most students can

identify. Ask the class if they have been finalists in a Publisher’s Clearing

House $10,000,000 Sweepstakes. Point out that a winner (if there is one) does

not receive a check for $10,000,000. Instead, the winner would receive $500,000

per year for 20 years. Ask students to imagine that they win this annuity. Ask

them if they would be willing to accept $9,000,000 today rather than $500,000 per

year for the next 20 years. Most of them are likely to accept the $9 million

option. Now point out that the present value of one dollar to be collected in the

future is less than one dollar. In other words, students are willing to give up

$10,000,000 future dollars to get $9,000,000 present dollars. Next, ask students

how much less than $10,000,000 they would be willing to accept. Ask how many

students would take $8, $7, $6, $5, $4, $3, $2, or $1 million instead of the

$500,000 annuity. Students will likely choose different amounts. As students

notice the variety of drop out points their peers choose, they will be motivated to

learn a formal method for calculating the present value of an annuity.

II. Show students how to use the present value tables.

A. An interest rate or desired rate of return is used to convert future dollars to

their present values. Given a specified interest rate, you can use simple

algebra to make the conversion. For example, suppose a manager estimates

that a particular investment will yield a $33,000 cash inflow one year from

today. The business desires to earn a 10% rate of return. How much should

the manager be willing to pay for the investment today? In other words, what

is the present value of $33,000 to be received one year into the future? The

answer can be determined as follows:

Investment + (.10 x Investment) = Future Cash Inflow

16-2

1.10 x Investment = $33,000

Investment = $33,000 1.10

Investment = $30,000

At a 10% required rate of return, the present value of $33,000 to be

received in one year is $30,000.

B. Point out that using algebra can be cumbersome when an investment is

expected to produce many cash inflows over a prolonged period of time.

Inform students they can use interest tables to simplify the computations and

show them they can obtain the same result as above using the present value

interest tables provided in the Appendix to Chapter 16. The present value

interest rate factor for one year at 10% is 0.909091 (Appendix Table 1).

Multiplying the expected future cash inflow by this factor produces the

following present value:

$33,000 x 0.909091 = $30,000

C. Explain that students can use Table 2 to estimate the present value of an

annuity like that described in the Publisher’s Clearing House example. Have

students help you choose a reasonable interest rate. Ask them what rate they

could currently earn on a certificate of deposit or in the stock market. Assume

your class picks 8% as a reasonable return. The present value interest rate

factor for a 20-year annuity at 8% is 9.818147 (See Appendix Table 2).

Multiplying the expected annual cash inflow of $500,000 by this factor

produces the following present value:

$500,000 x 9.818147 = $4,909,073.50

Therefore, given an 8% desired rate of return, the present value of receiving

$500,000 per year for the next twenty years is $4,909,073.50. Explain that the

winner would be indifferent between receiving $4,909,073.50 immediately or

an annuity of $500,000 per year for 20 years, assuming that 8% is a

reasonable rate of return and ignoring the effect of income taxes. Then do the

same example using a higher (or lower) required rate of return.

III. Introduce the cost of capital concept. A business determines its desired rate of

return by estimating its cost of capital. You need not provide a detailed

explanation of how to determine the cost of capital. That topic will be addressed

in a future finance course. However, students can easily understand the basic

concept. A company must earn a rate at least equal to the rate it must pay to

stockholders and creditors. Therefore, the cost of capital is the company’s

minimum desired rate of return. Also, advise students that many different terms

are used in business practice to describe the desired rate of return. These terms

include the minimum rate of return, the cutoff rate, the discount rate, and the

hurdle rate.

Chapter 16 – Planning for Capital Investments

16-3

IV. Introduce the net present value concept.

A. Students should now have the necessary background for Demonstration

Problem 16-1. Distribute the problem and have students complete

requirement a. Let students attempt this requirement on their own before

showing them the solution. Circulate around the room, helping as needed. If

the class as a whole is having difficulty, step in and provide appropriate

instruction.

B. Once students have determined the present value of the future cash savings

(they have completed requirement a), show them how to determine the net

present value by subtracting the present value of the cash outflow from the

present value of the cash savings (complete requirement b). Explain how to

interpret the net present value figure. If the net present value is positive,

management expects the investment to earn more than the desired rate of

return; if it is negative, management expects the investment to earn less than

the desired rate of return. Then ask your students what rate of return will give

a net present value of $0.

C. Have students complete requirement c to give them more practice

determining the net present value of an investment opportunity.

D. Use requirement d to teach students how to use the present value index.

E. Use Exercises 16-5, 16-6, and 16-7 for in-class reinforcement or as

homework.

V. Introduce the internal rate of return concept. Computing the internal rate of

return can be cumbersome unless you use spreadsheets or some other form of

computer software. Unless you use such software, limit your examples to those

that will produce even results, avoiding the need for extrapolation. Use Exercise

16-9 as a demonstration problem and Exercise 16-10 as homework. Use

Problem 16-16 if you introduce Excel software applications.

VI. Use requirements a through d of Demonstration Problem 16-2 to introduce

the payback method of evaluating investment opportunities. Use Exercise

16-12 as in-class reinforcement or as homework.

VII. Use requirement e of Demonstration Problem 16-2 to introduce the

unadjusted rate of return method for the evaluation of investment

opportunities. Use Problem 16-20 as a comprehensive homework assignment

covering both payback and unadjusted rate of return.

Chapter 16 – Planning for Capital Investments

16-4

Summary Outline of a Lesson Plan for Chapter 16

I. Start the class using an example that illustrates present value, such as the

Publisher’s Clearing House $10,000,000 Sweepstakes or the prize in a state

lottery. Explain that the present value of a 20-year payout is less than the future

value of the prize sum (the announced amount of the prize).

II. Show students how to use present value tables.

A. First use simple algebra to compute a present value. What is the present value

of $33,000 to be received one year into the future at a 10% rate of return?

Investment + (.10 x Investment) = Future Cash Inflow

1.10 Investment = $33,000

Investment = $33,000 1.10

Investment = $30,000

B. Illustrate using interest tables like those in Appendix Table 1 to compute

present values, as follows:

$33,000 x 0.909091 = $30,000.

C. Illustrate using Table 2 to estimate the present value of an annuity like the

Publisher’s Clearing House winnings. For example, the present value at 8%

of a 20-year annuity of $500,000 per year is:

$500,000 x 9.818147 = $4,909,073.50.

III. Introduce cost of capital. A company must earn a rate at least equal to the rate it

must pay. Therefore the cost of capital is the minimum desired rate of return.

The desired rate of return may be called the minimum rate of return, the cutoff

rate, the discount rate, and the hurdle rate.

IV. Introduce net present value.

A. Have students complete requirement a of Demonstration Problem 16-1.

B. Once students have completed requirement a, show them how to determine

the net present value by completing requirement b.

C. Have students complete requirement c to give them practice.

D. Use requirement d to teach students how to use the present value index.

E. Use Exercises 16-5, 16-6, and 16-7 for in-class reinforcement or as

homework.

Chapter 16 – Planning for Capital Investments

16-5

V. Introduce internal rate of return. Use Exercise 16-9 as a demonstration

problem and Exercise 16-10 as homework. Use Problem 16-16 if you plan to

introduce Excel software applications.

VI. Use requirements a through d of Demonstration Problem 16-2 to introduce

the payback method. Use Exercise 16-12 as in-class reinforcement or as

homework.

VII. Use requirement e of Demonstration Problem 16-2 to introduce unadjusted

rate of return. Use Problem 16-20 as a comprehensive homework assignment

covering both payback and unadjusted rate of return.

Quiz Questions for Chapter 16

1. Which following statement is true?

a. The present value of a future dollar is less than one dollar.

b. The present value of a future dollar is more than one dollar.

c. The present value of a future dollar is equal to one dollar.

d. The future value of a present dollar equals one dollar.

2. ABC Company has an opportunity to invest in a depreciable asset that will yield a net cash inflow

of $30,000 per year for four years. ABC’s desired rate of return is 10%. Based on this

information, what is the present value of the investment opportunity (round to the nearest whole

dollar)?

a. $97,192

b. $20,490

c. $95,096

d. $61,069

3. Western Company can purchase an asset that costs $1,166,900. The asset is expected to produce

net cash inflows of $300,000 per year for five years. Based on this information alone, the

investment is expected to yield an internal rate of return closest to

a. 6%.

b. 9%.

c. 10%.

d. 12%.

4. The rate that is used to calculate the present value of cash inflows and outflows is called the

a. minimum rate of return.

b. cost of capital.

c. desired rate of return.

d. all of the above.

Use the following information to answer the next two questions: Kramer Company paid $60,000 to

purchase a depreciable asset. The asset is expected to produce annual cash inflows of $12,000 per year for

ten years. Kramer’s desired rate of return is 12%.

5. Which of the following is the present value of the cash inflows expected for this asset? Round to

the nearest whole dollar.

a. $67,803

b. $73,735

c. ($60,000)

Chapter 16 – Planning for Capital Investments

16-6

d. $56,522

6. The internal rate of return for this investment is

a. equal to the desired rate of return.

b. greater than the desired rate of return.

c. less than the desired rate of return.

d. the answer cannot be determined from the information provided.

7. Which of the following is the approximate internal rate of return for an investment that costs

$33,900 and provides a $6,000 annuity for 10 years?

a. 6%

b. 10%

c. 8%

d. 12%

8. North State, Inc. (NSI) is trying to determine its cash inflows from an investment in new computer

equipment. Which of the following would be treated as a cash inflow in determining the present

value of the investment opportunity?

a. Cash revenues from existing operations.

b. Cash savings from reductions in labor costs resulting from using the equipment.

c. Cash collections from alternative investment opportunities.

d. All of the above are considered cash inflows.

Use the following information to answer the next two questions:

Harrison, Inc. is considering two investment opportunities. Each investment costs $7,000 and will provide

the same total future cash inflows. The schedule of estimated cash receipts for each investment follows

(assume cash is received at year-end)

Investment I Investment II

Year 1 $3,000 $1,000

Year 2 2,500 2,000

Year 3 2,000 3,000

Year 4 1,500 3,000

Total $9,000 $9,000

9. Which investment should Harrison choose assuming all other features for the two investments are

the same?

a. Harrison should be indifferent between the two investments because they provide the same

total cash inflows.

b. Harrison should choose Investment I because of the time value of money.

c. Harrison should be indifferent between the two investments because the initial cash outflow is

the same.

d. Harrison should choose Investment II because it generates larger cash inflows at the end of

the investment’s useful life.

10. Assuming an 8% minimum rate of return, what is the net present value of Investment II (round to

the nearest whole dollar)?

a. $7,227

b. $227

c. ($7,000)

d. $926

11. KLM Company has the opportunity to purchase an asset that costs $50,000. The asset is expected

to increase net income by $20,000 per year. The asset has a 5-year useful life. Depreciation

expense used in computing net income amounted to $10,000 per year. Based on this information

the payback period is

a. 3.5 years.

b. 5 years.

c. 1.67 years.

d. 2.5 years.

Chapter 16 – Planning for Capital Investments

16-7

12. Which of the following statements concerning payback analysis is true?

a. If all other variables are the same, an investment with a shorter payback period is preferable to

an investment with a longer payback period.

b. The payback method ignores the time value of money concept.

c. The payback method and the unadjusted rate of return are different approaches that

consistently lead to the same conclusion.

d. a and b.

13. XYZ Company has an opportunity to purchase an asset that will cost the company $60,000. The

asset is expected to add $12,000 per year to the company’s net income. Assuming the asset has a 5–

year useful life and a zero salvage value, the unadjusted rate of return based on the average

investment will be

a. 40%.

b. 20%.

c. 60%.

d. 50%.

14. Marfa Company is evaluating two different investment alternatives, which are to be evaluated

using the present value index.

Alternative 1

Alternative 2

Initial investment

$100,000

$150,000

Present value of cash inflows

$108,000

$160,000

Estimated useful life

5 years

5 years

Which of the following statements is true?

a. Based on present value index, Alternative 2 is preferred.

b. The present value index for Alternative 2 is 1.60.

c. The present value index for Alternative 1 is 1.08.

d. None of the above

Solutions to Quiz Questions

Question

Answer

1

A

2

C

3

B

4

D

5

A

6

B

7

D

8

B

9

B

10

B

11

C

12

D

13

B

14

C

Chapter 16 – Planning for Capital Investments

16-8

Demonstration Problems for Chapter 16

Demonstration Problem 16-1

Net Present Value/Present Value Index

The management team at Savage Corporation is evaluating two alternative capital

investment opportunities. The first alternative, modernizing the company’s current

machinery, costs $45,000. Management estimates the modernization project will reduce

annual net cash outflows by $12,500 per year for the next five years. The second

alternative, purchasing a new machine, costs $56,500. The new machine is expected to

have a five-year useful life and a $4,000 salvage value. Management estimates the new

machine will generate cash inflows of $15,000 per year. Savage’s cost of capital is 10%.

Required

a. Determine the present value of the cash flow savings expected from the

modernization program.

b. Determine the net present value of the modernization project.

c. Determine the net present value of investing in the new machine.

d. Use a present value index to determine which investment alternative will yield the

higher rate of return.

Demonstration Problem 16-2

Payback/Unadjusted Rate of Return

EZ Rentals can purchase a van that costs $24,000. The van has an expected useful life of

5 years and no salvage value. EZ expects cash revenue from leasing the van to be

$12,000 per year. Alternatively, EZ can purchase a car that costs $16,000. EZ expects

cash revenue from leasing the car to be $10,000 per year over a 3-year useful life. Ignore

income taxes.

Required

a. Determine the payback period for the van.

b. Determine the payback period for the car.

c. Indicate which vehicle is the better alternative if payback is used as the sole

investment criteria.

d. Describe the possible shortcomings of using payback as the investment criteria.

e. Determine the unadjusted rate of return for both alternatives.

Demonstration Problem 16-1 Solution

Chapter 16 – Planning for Capital Investments

16-9

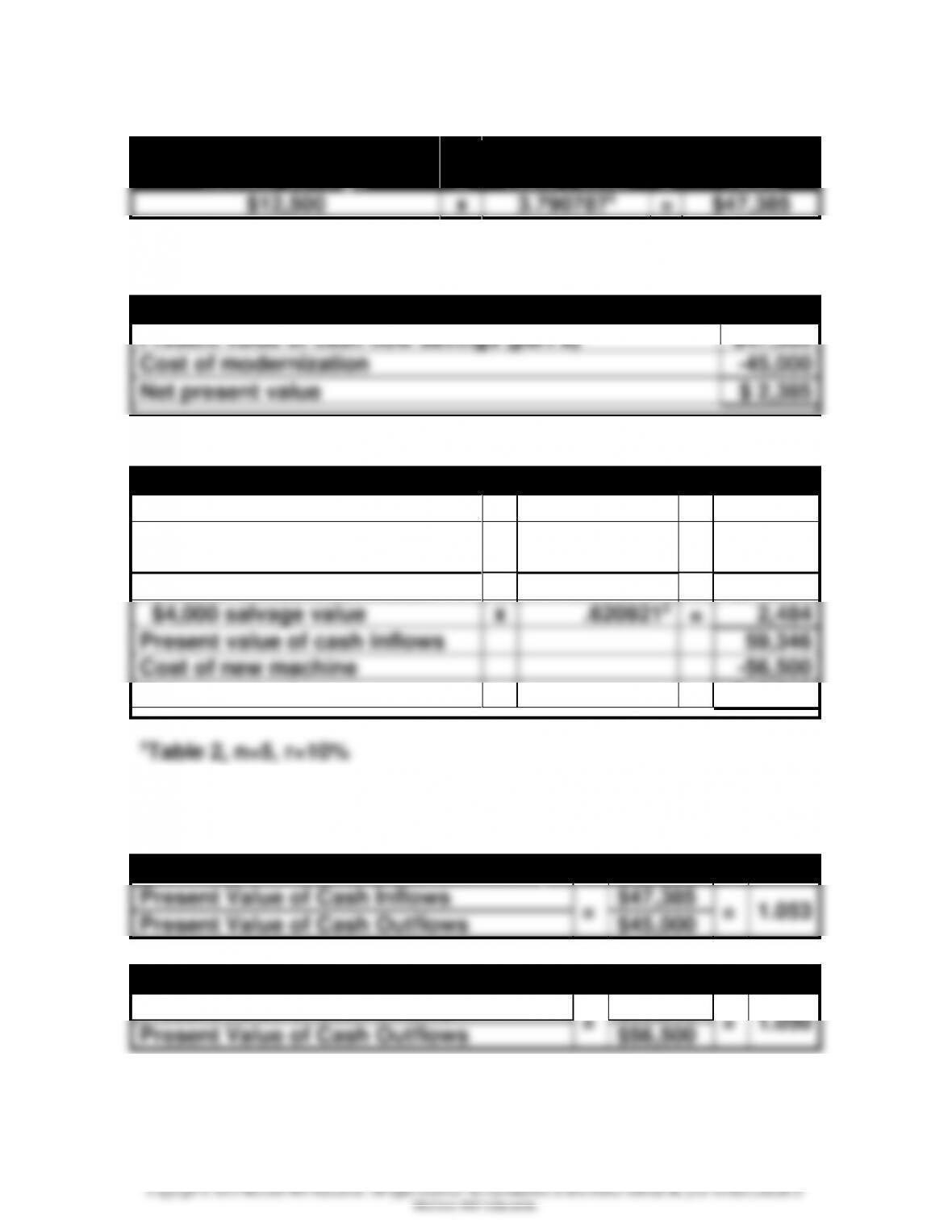

a. Present value of cash flow savings

Annual Savings

x

Present Value

Table Factor

=

Present

Value

$12,500

x

3.7907871

=

$47,385

1Table 2, n=5, r=10%

b.

Net present value of modernization project

Present value of cash flow savings (part a)

$47,385

Cost of modernization

-45,000

Net present value

$ 2,385

c.

Net present value of investing in new machine

Present Value of Cash Inflows

Future Value

x

Present Value

Table Factor

=

Present

Value

$15,000 annual cash inflow

x

3.7907871

=

$56,862

$4,000 salvage value

x

.6209212

=

2,484

Present value of cash inflows

59,346

Cost of new machine

-56,500

Net present value

$ 2,846

2Table 1, n=5, r=10%Demonstration Problem 16-1 Solution

d.

Present value index for modernization project

Present Value of Cash Inflows

=

$47,385

=

1.053

Present Value of Cash Outflows

$45,000

Present value index for investing in new machine

Present Value of Cash Inflows

=

$59,346

=

1.050

Present Value of Cash Outflows

$56,500

Chapter 16 – Planning for Capital Investments

16–10

The higher present value index for the modernization project

Demonstration Problem 16-2 Solution

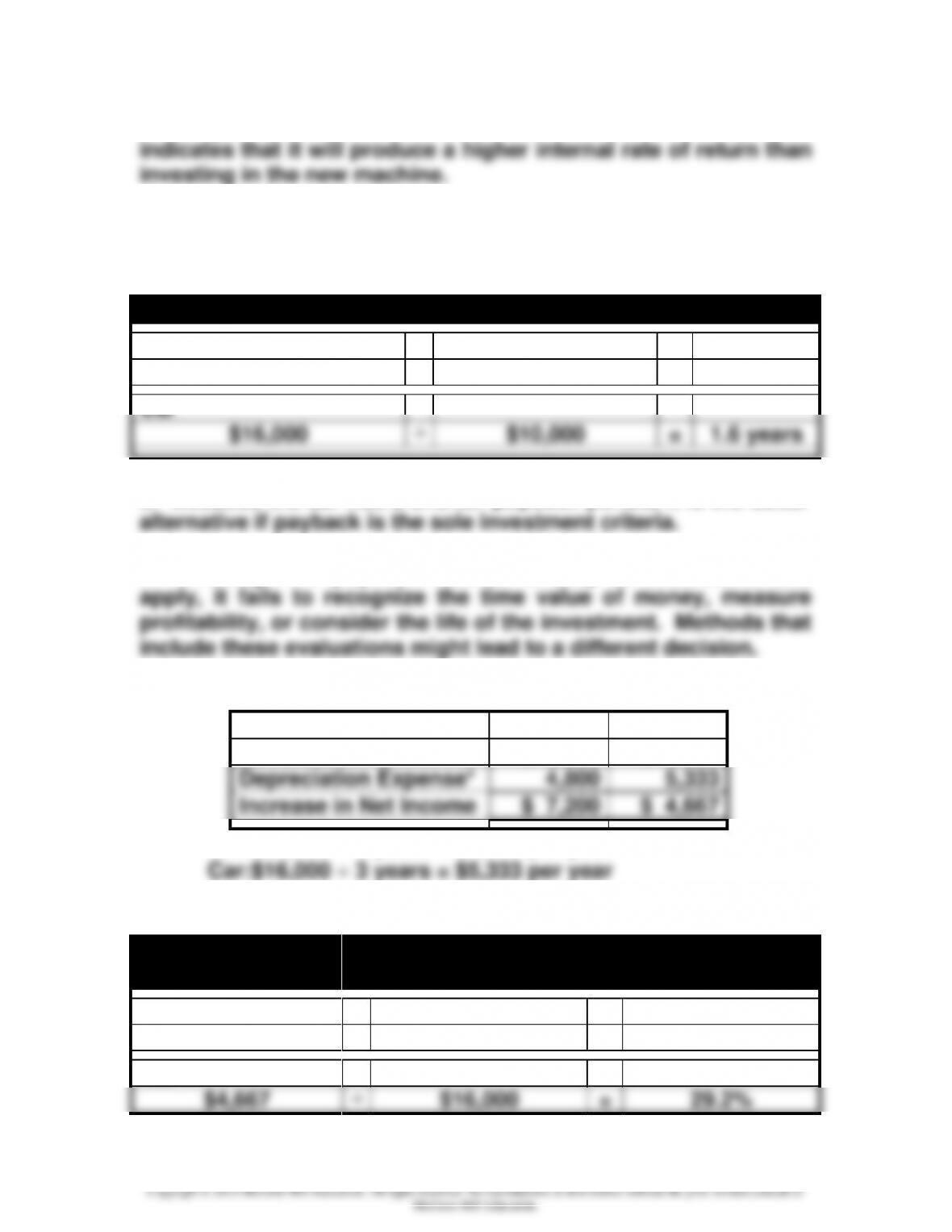

a. b. Payback period:

Cash Cost of Investment

÷

Annual Cash Inflow

=

Payback

Van

$24,000

÷

$12,000

=

2 years

Car

$16,000

÷

$10,000

=

1.6 years

c. Because the car has a shorter payback period, it is the better

d. Although the payback method is easy to understand and

e. First, determine the average annual increase in net income:

Van

Car

Revenue

$12,000

$10,000

Depreciation Expense*

4,800

5,333

Increase in Net Income

$ 7,200

$ 4,667

*Van: $24,000 ÷ 5 years = $4,800 per year

Next, determine the unadjusted rate of return:

Increase in Annual

Net Income

÷

Cost of Investment

=

Unadjusted Rate

of Return

Van

$7,200

÷

$24,000

=

30%

Car

$4,667

÷

$16,000

=

29.2%

Chapter 16 – Planning for Capital Investments

16–11

Demonstration Problem 16-1 Work Papers

a. Present value of cash flow savings

Annual Savings

x

Present Value

Table Factor

=

Present

Value

x

1

=

$47,385

1Table ___, n=___, r=___%

b.

Net present value of modernization project

Present value of cash flow savings

Cost of modernization

Net present value

$ 2,385

c.

Net present value of investing in new machine

Present Value of Cash Inflows

Future Value

x

Present Value

Table Factor

=

Present

Value

$ annual cash inflow

x

1

=

$ salvage value

x

2

=

Present value of cash inflows

Cost of new machine

Net present value

$ 2,846

1Table ___, n=___, r=___%

2Table ___, n=___, r=___%Demonstration Problem 16–1

Work Papers

d.

Present value index for modernization project

Present Value of Cash Inflows

=

=

1.053

Present Value of Cash Outflows