Chapter 01 – An Introduction to Accounting

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

1-1

Demonstration Problem 1-1: Solution, part a. Equation Approach

Effect of Events on the Accounting Equation

For Year 2014

Equity

Events

Assets

=

Liabilities

+

Common

Stock

+

Retained

Earnings

Beginning Balances

$ 0

=

$ 0

+

$ 0

+

$ 0

1. Effect of Stock Issue

9,000

9,000

2. Effect of Borrowing

5,000

5,000

3. Effect of Revenue

4,000

4,000

4. Effect of Expense

(2,900)

(2,900)

5. Effect of Dividends

(500)

(500)

−−−−−

−−−−−

−−−−−

−−−−−

Ending Balances

$14,600

=

$5,000

+

$9,000

+

$ 600

=====

═════

═════

═════

For Year 2015

Equity

Events

Assets

=

Liabilities

+

Common

Stock

+

Retained

Earnings

Beginning Balances

$14,600

=

$5,000

+

$ 9,000

+

$ 600

1. Effect of Stock Issue

4,500

4,500

2. Effect of Debt Repay.

(2,000)

(2,000)

3. Effect of Revenue

6,700

6,700

4. Effect of Expense

(4,300)

(4,300)

5. Effect of Dividends

(700)

(700)

−−−−−

−−−−−

−−−−−

−−−−−

Ending Balances

$18,800

=

$3,000

+

$13,500

+

$ 2,300

═════

═════

═════

═════

For Year 2016

Assets

=

Liab.

+

Equity

Events

Cash

+

Land

=

Liab.

+

Common

Stock

+

Retained

Earnings

Beginning Balances

$18,800

$3,000

+

$13,500

+

$ 2,300

1. Effect of Stock Issue

2,500

2,500

2. Effect of Borrowing

1,000

1,000

3. Effect of Revenue

7,400

7,400

4. Effect of Expense

(7,900)

(7,900)

5. Effect of Dividends

(300)

(300)

6. Effect of Land Purch.

(9,000)

$9,000

−−−−−

−−−−

−−−−

−−−−−

−−−−−

Ending Balances

$12,500

+

$9,000

=

$4,000

+

$16,000

+

$1,500

═════

════

════

═════

═════

Demonstration Problem 1-1: Solution, part b. Financial Statements

Chapter 01 – An Introduction to Accounting

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

1-2

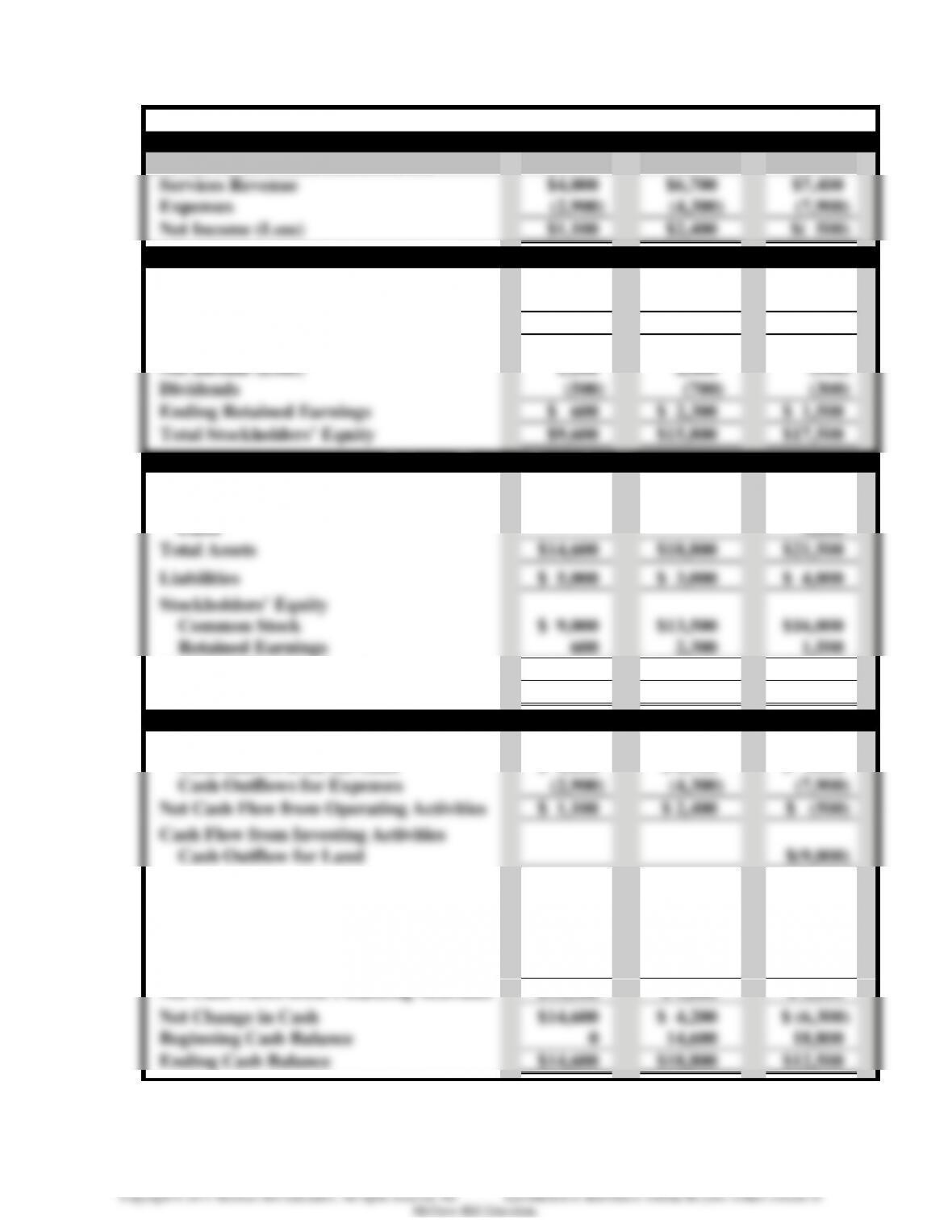

Video Services Company

Income Statements

For the Years Ended December 31,

2014

2015

2016

Services Revenue

$4,000

$6,700

$7,400

Expenses

(2,900)

(4,300)

(7,900)

Net Income (Loss)

$1,100

$2,400

$( 500)

Statements of Changes in Stockholders’ Equity

Beginning Common Stock

$ 0

$ 9,000

$13,500

Plus: Common Stock Issued

9,000

4,500

2,500

Ending Common Stock

$9,000

$13,500

$16,000

Beginning Retained Earnings

$ 0

$ 600

$ 2,300

Net Income (Loss)

1,100

2,400

(500)

Dividends

(500)

(700)

(300)

Ending Retained Earnings

$ 600

$ 2,300

$ 1,500

Total Stockholders’ Equity

$9,600

$15,800

$17,500

Balance Sheets at December 31

Assets

Cash

$14,600

$18,800

$12,500

Land

9,000

Total Assets

$14,600

$18,800

$21,500

Liabilities

$ 5,000

$ 3,000

$ 4,000

Stockholders’ Equity

Common Stock

$ 9,000

$13,500

$16,000

Retained Earnings

600

2,300

1,500

Total Stockholders’ Equity

$ 9,600

$15,800

$17,500

Total Liabilities and Stockholders’ Equity

$14,600

$18,800

$21,500

Statements of Cash Flows

Cash Flows from Operating Activities

Cash Inflows from Revenue

$ 4,000

$ 6,700

$ 7,400

Cash Outflows for Expenses

(2,900)

(4,300)

(7,900)

Net Cash Flow from Operating Activities

$ 1,100

$ 2,400

$ (500)

Cash Flow from Investing Activities

Cash Outflow for Land

$(9,000)

Cash Flows from Financing Activities

Cash Inflows from Borrowed Funds

$ 5,000

$ 1,000

Cash Outflows to Reduce Debt

$(2,000)

Cash Inflows from Stock Issues

9,000

4,500

2,500

Cash Outflows for Dividends

(500)

(700)

(300)

Net Cash Flows from Financing Activities

$13,500

$ 1,800

$ 3,200

Net Change in Cash

$14,600

$ 4,200

$ (6,300)

Beginning Cash Balance

0

14,600

18,800

Ending Cash Balance

$14,600

$18,800

$12,500

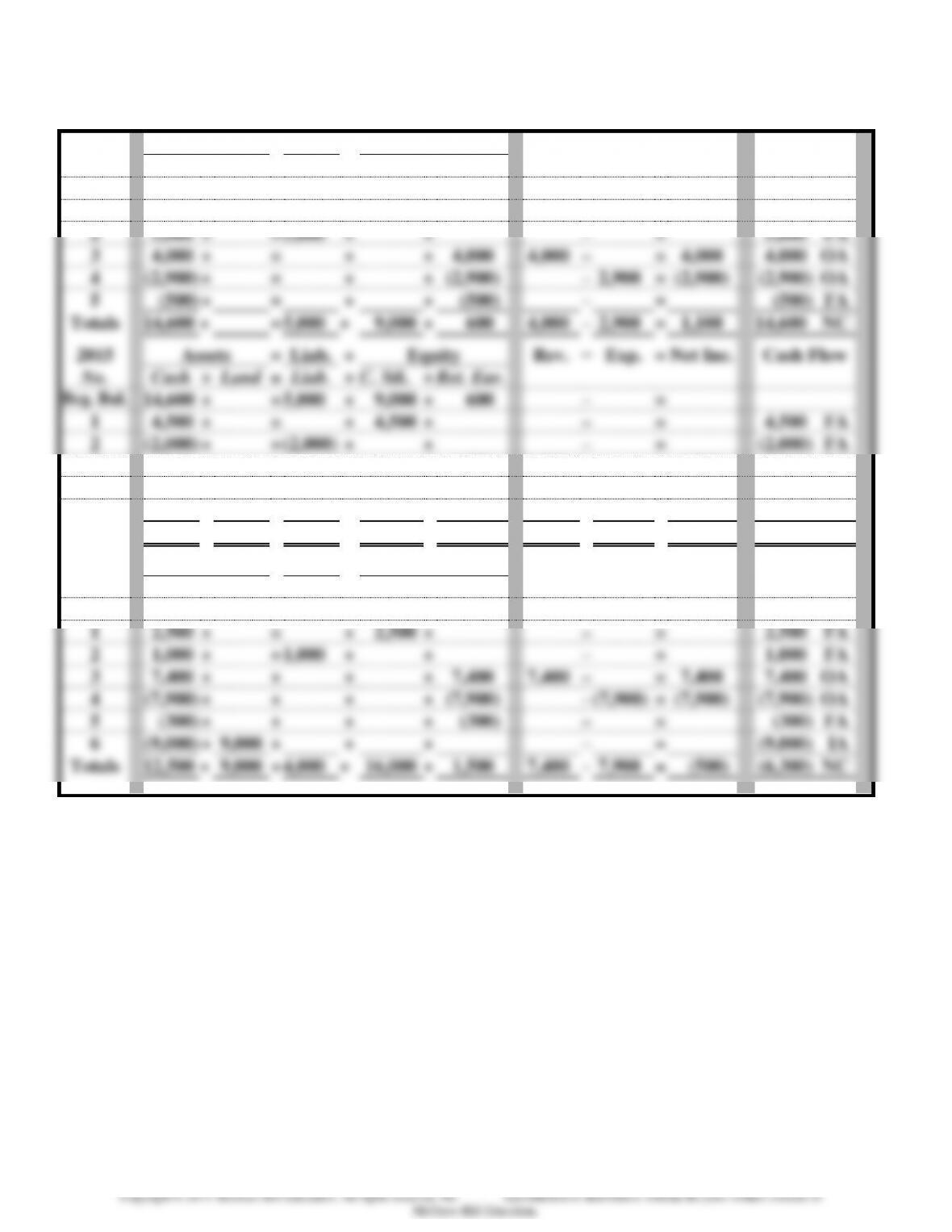

Demonstration Problem 1-1: Solution, part a.

Statements Model Approach

Chapter 01 – An Introduction to Accounting

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

1-3

2014

Assets

=

Liab.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

No.

Cash

+

Land

=

Liab.

+

C. Stk.

+

Ret. Ear.

Beg. Bal.

+

=

+

+

–

=

1

9,000

+

=

+

9,000

+

–

=

9,000 FA

2

5,000

+

=

5,000

+

+

–

=

5,000 FA

3

4,000

+

=

+

+

4,000

4,000

–

=

4,000

4,000 OA

4

(2,900)

+

=

+

+

(2,900)

–

2,900

=

(2,900)

(2,900) OA

5

(500)

+

=

+

+

(500)

–

=

(500) FA

Totals

14,600

+

=

5,000

+

9,000

+

600

4,000

–

2,900

=

1,100

14,600 NC

2015

Assets

=

Liab.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

No.

Cash

+

Land

=

Liab.

+

C. Stk.

+

Ret. Ear.

Beg. Bal.

14,600

+

=

5,000

+

9,000

+

600

–

=

1

4,500

+

=

+

4,500

+

–

=

4,500 FA

2

(2,000)

+

=

(2,000)

+

+

–

=

(2,000) FA

3

6,700

+

=

+

+

6,700

6,700

–

=

6,700

6,700 OA

4

(4,300)

+

=

+

+

(4,300)

–

4,300

=

(4,300)

(4,300) OA

5

(700)

+

=

+

+

(700)

–

=

(700) FA

Totals

18,800

+

=

3,000

+

13,500

+

2,300

6,700

–

4,300

=

2,400

4,200 NC

2016

Assets

=

Liab.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

No.

Cash

+

Land

=

Liab.

+

C. Stk.

+

Ret. Ear.

Beg. Bal.

18,800

+

=

3,000

+

13,500

+

2,300

–

=

1

2,500

+

=

+

2,500

+

–

=

2,500 FA

2

1,000

+

=

1,000

+

+

–

=

1,000 FA

3

7,400

+

+

+

+

7,400

7,400

–

=

7,400

7,400 OA

4

(7,900)

+

+

+

+

(7,900)

–

(7,900)

=

(7,900)

(7,900) OA

5

(300)

+

+

+

+

(300)

–

=

(300) FA

6

(9,000)

+

9,000

+

+

+

–

=

(9,000) IA

Totals

12,500

+

9,000

+

4,000

+

16,000

+

1,500

7,400

–

7,900

=

(500)

(6,300) NC

WORK PAPERS FOR

DEMONSTRATION PROBLEM

Chapter 01 – An Introduction to Accounting

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

1-4

The work papers are designed for student use. You may copy them

and distribute the hard copies to your students. However, a more

efficient way to distribute them is to cut and paste them into a

Demonstration Problem 1-1: Work Paper, part a. Equation Approach

Effect of Events on the Accounting Equation

For Year 2014

Equity

Events

Assets

=

Liabilities

+

Common

Stock

+

Retained

Earnings

Beginning Balances

$ 0

=

$ 0

+

$ 0

+

$ 0

1. Effect of Stock Issue

2. Effect of Borrowing

3. Effect of Revenue

4. Effect of Expense

5. Effect of Dividends

−−−−−

−−−−−

−−−−−

−−−−−

Ending Balances

$14,600

=

$5,000

+

$9,000

+

$ 600

═════

═════

═════

═════

For Year 2015

Equity

Events

Assets

=

Liabilities

+

Common

Stock

+

Retained

Earnings

Beginning Balances

=

+

+

1. Effect of Stock Issue

2. Effect of Debt Repay.

3. Effect of Revenue

4. Effect of Expense

5. Effect of Dividends

−−−−−

−−−−−

−−−−−

−−−−−

Ending Balances

$18,800

=

$3,000

+

$13,500

+

$ 2,300

═════

═════

═════

═════

For Year 2016

Assets

=

Liab.

+

Equity

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

1-5

Events

Cash

+

Land

=

Liab.

+

Common

Stock

+

Retained

Earnings

Beginning Balances

+

+

1. Effect of Stock Issue

2. Effect of Borrowing

3. Effect of Revenue

4. Effect of Expense

5. Effect of Dividends

6. Effect of Land Purch.

−−−−−

−−−−

−−−−

−−−−−

−−−−−

Ending Balances

$12,500

+

$9,000

=

$4,000

+

$16,000

+

$1,500

═════

════

════

═════

═════

Demonstration Problem 1-1: Work Paper, part b. Financial Statements

Video Services Company

Income Statements

For the Years Ended December 31,

2014

2015

2016

Services Revenue

Expenses

Net Income (Loss)

$1,100

$2,400

$( 500)

Statements of Changes in Stockholders’ Equity

Beginning Common Stock

$ 0

$ 9,000

$13,500

Plus: Common Stock Issued

Ending Common Stock

Beginning Retained Earnings

Net Income (Loss)

Dividends

Ending Retained Earnings

Total Stockholders’ Equity

$9,600

$15,800

$17,500

Balance Sheets at December 31

Assets

Cash

Land

Total Assets

$14,600

$18,800

$21,500

Liabilities

Stockholders’ Equity

Common Stock

Retained Earnings

Total Stockholders’ Equity

Total Liabilities and Stockholders’ Equity

$14,600

$18,800

$21,500

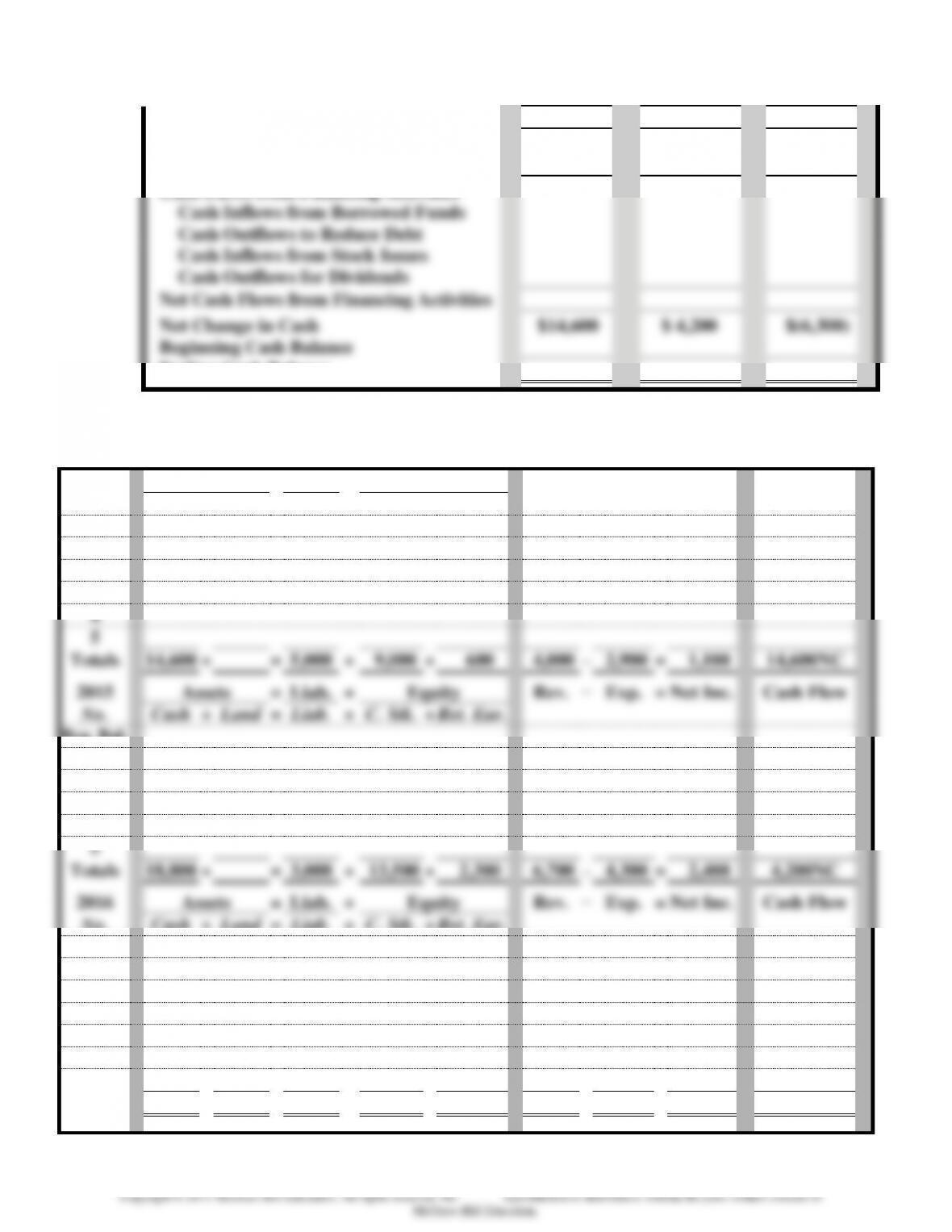

Statements of Cash Flows

Cash Flows from Operating Activities

Cash Inflows from Revenue

$ 4,000

$ 6,700

$ 7,400

Cash Outflows for Expenses

Chapter 01 – An Introduction to Accounting

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

1-6

Net Cash Flow from Operating Activities

Cash Flow from Investing Activities

Cash Outflows for Land

Cash Flows from Financing Activities

Cash Inflows from Borrowed Funds

Cash Outflows to Reduce Debt

Cash Inflows from Stock Issues

Cash Outflows for Dividends

Net Cash Flows from Financing Activities

Net Change in Cash

$14,600

$ 4,200

$(6,300)

Beginning Cash Balance

Ending Cash Balance

Demonstration Problem 1-1: Work Paper, part a.

Statements Model Approach

2014

Assets

=

Liab.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

No.

Cash

+

Land

=

Liab.

+

C. Stk.

+

Ret. Ear.

Beg. Bal.

+

=

+

+

–

=

1

2

3

4

5

Totals

14,600

+

=

5,000

+

9,000

+

600

4,000

–

2,900

=

1,100

14,600NC

2015

Assets

=

Liab.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

No.

Cash

+

Land

=

Liab.

+

C. Stk.

+

Ret. Ear.

Beg. Bal.

1

2

3

4

5

Totals

18,800

+

=

3,000

+

13,500

+

2,300

6,700

–

4,300

=

2,400

4,200NC

2016

Assets

=

Liab.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

No.

Cash

+

Land

=

Liab.

+

C. Stk.

+

Ret. Ear.

Beg. Bal.

1

2

3

4

5

6

Totals

12,500

+

9,000

+

4,000

+

16,000

+

1,500

7,400

–

7,900

=

(500)

(6,300) NC

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

1-7

Quiz Questions for Chapter 1

The following information pertains to the next four questions. At the beginning of 2014, X Company had assets

of $300, liabilities of $150, and common stock of $50. During 2014 the company earned revenue of $400, incurred

expenses of $250, and paid dividends of $100. All transactions were cash transactions.

1. What is the amount of retained earnings at the beginning of 2014?

a. $ 50.

b. $100.

c. $150.

d. none of the above.

2. The amount of net income reported on the 2014 income statement would be

a. $400.

b. $150.

c. $ 50.

d. none of the above.

3. The amount of retained earnings reported on the December 31, 2014 balance sheet would be

a. $100.

b. $250.

c. $650.

d. none of the above.

4. The amount of total assets reported on the December 31, 2014 balance sheet would be

a. $350.

b. $300.

c. $450.

d. $ 50.

5. Z Company borrowed $500 cash from the National Bank. As a result of this transaction, Z Company’s

a. assets would increase by $500.

b. liabilities would decrease by $500.

c. equity would increase by $500.

d. revenue would decrease by $500.

The following information pertains to the next two questions. XYZ Company borrowed $800 from the State

Bank and used $500 of this money to purchase land.

6. As a result of these transactions, XYZ’s total assets would increase by

a. $1,300.

b. $ 800.

c. $ 500.

d. $ 300.

7. The statement of cash flows for XYZ Company would report

a. an inflow of $500 from financing activities.

b. an outflow of $800 for investing activities.

c. an inflow of $800 from financing activities.

d. an outflow of $500 for operating activities.

8. Select the correct statement from the choices listed below.

a. Revenue is a decrease in assets resulting from operating activities.

b. Dividends are decreases in assets incurred for the purpose of producing revenue.

c. A company incurs expenses when it borrows money.

d. Net income is an increase in equity resulting primarily from operating activities.

Chapter 01 – An Introduction to Accounting

9. If revenue exceeds expenses, there are no dividends, and total liabilities remain unchanged, then

a. Equity will increase.

b. Retained earnings will decrease.

c. Total assets will increase.

d. Both a and c.

The following information pertains to the next two questions. Person A paid $10,000 cash to buy land from

Person B.

10. Select the statement that is true.

a. Total liabilities of Person B would increase.

b. Total assets of Person A would be unaffected.

c. Person A’s equity would increase.

d. None of the above.

11. Select the statement that is true.

a. Person A would have a cash outflow from investing activities.

b. Person B would have a cash inflow from investing activities.

c. The balance in the cash account on Person A’s books would decrease, while the balance in the cash

account on Person B’s books would increase.

d. All of the above statements are true.

12. Revenue is less than expenses. If liabilities and common stock were unchanged, then

a. cash flows from operating activities were greater than cash flows from investing activities.

b. total assets decreased.

c. retained earnings were less than net income during the period.

d. the company must have purchased assets with cash.

13. Among other items, the balance sheet of XYZ Company reports retained earnings of $50,000 and total

liabilities of $40,000. Based on this information alone, you would know that

a. since the company’s inception, the total amount of net income exceeded total dividends by at least

$50,000.

b. XYZ Company has enough cash to pay off its liabilities.

c. stockholders’ equity of the company amounted to $10,000.

d. total assets amounted to $90,000.

14. The Southern Company began the accounting period with assets of $600, common stock of $200, and

retained earnings of $250. During the period, revenue was $300, expenses were $200, and dividends were

$50. Common stock was unchanged during the accounting period. Liabilities decreased by $100. Based on

this information,

a. net income amounted to $50.

b. total assets at the end of the period were $550.

c. retained earnings at the end of the period amounted to $350.

d. liabilities at the end of the period amounted to $100.

15. Which of the following illustrates how a cash dividend affects a company’s financial statements?

Balance Sheet

Income Statement

Statement of

Assets

=

Liab.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

a.

+

n/a

+

n/a

n/a

n/a

+ FA

b.

+

n/a

+

+

n/a

+

+ OA

c.

−

n/a

−

n/a

+

−

− OA

d.

−

n/a

−

n/a

n/a

n/a

− FA

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

1-9

Solutions to Quiz Questions

Question

Answer

1

B

2

B

3

D

4

A

5

A

6

B

7

C

8

D

9

D

10

B

11

D

12

B

13

A

14

B

15

D

Summary Outline of a Lesson Plan for Chapter 1

(Equation Approach)

Chapter 01 – An Introduction to Accounting

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

1-10

I. Distribute copies of Demonstration Problem 1-1.

II. Define assets. Assets are things of value to a business. The value is the capacity of the

asset to be used in the production of greater quantities of other assets.

III. Introduce the accounting equation.

IV. Use the demonstration problem to introduce new terms and to elaborate on the

interrelationships represented by the accounting equation. There are three primary

sources of assets.

A. Event No. 1 introduces common stock (owner interest).

B. Event No. 2 introduces liabilities (creditor interest).

C. Event No. 3 introduces revenue (increase in assets from earnings activities).

There are two asset use transactions.

D. Event No. 4 introduces expenses (decreases in assets from earnings activities).

E. Event No. 5 introduces dividends (wealth transfer).

V. Have students record the events for the second accounting cycle in an accounting

equation.

VI. Time considerations. Introducing the accounting equation, including student

participation with 2015 data, requires approximately one hour.

. VII. Homework assignments. Problem 1-32 is similar to the demonstration problem.

VIII. Introduce financial statements.

A. Income Statement. Because revenues increase and expenses decrease assets, net

income represents the change in wealth resulting from business operations during

the accounting period.

B. Statement of Changes in Stockholders’ Equity. Distinguish between expenses and

dividends.

C. Balance Sheet. This statement summarizes the accounting equation.

D. Statement of Cash Flows. Use the direct method; analyze the cash account.

IX. Have students prepare financial statements for the 2015 transactions.

X. Introduce the horizontal financial statements model.

XI. Filling in the gaps. Remind students they must read the text to fill in the gaps.

XII. Enrichment. If time permits, have students complete ATC Case 1-1 (financial statement

analysis).

Summary Outline of a Lesson Plan for Chapter 1

(Statements Model Approach)

I. Use the problem-based learning case, “Ask Me Anything,” to introduce financial

statements to students.

Chapter 01 – An Introduction to Accounting

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

1-11

II. Create a collaborative experience where students reach consensus on their

questions. Have each group select a spokesperson.

III. Briefly introduce the basic financial statements. Introduce: 1) the balance sheet, 2)

the income statement, and 3) the statement of cash flows.

IV. Use student input to demonstrate the usefulness of financial statement information.

Ask the group spokespersons to share the questions their group would like to have the

accountant answer. Identify information that would or would not appear in financial

statements. Students should learn to name three financial statements and to describe the

specific elements that appear in each statement.

V. Distribute copies of Demonstration Problem 1-1. Show students how to record

business events directly into a set of financial statements (part b).

VI. Create a financial statements model for Demonstration Problem 1-1 (part a). Present

and explain a financial statements model for the students. Analyze and record the

transactions.

VII. Actively involve the students in learning. After explaining the 2014 accounting

transactions, show how this year’s ending balances become next year’s beginning

balances. Require the students to record the transactions for the 2015 accounting cycle in

the model. Assist as needed. Instruct the faster students to record 2016 transactions.

Have those students who do not finish the third cycle in class complete part a of the

problem as a homework assignment.

VIII. Introduce the accounting equation. Explain that the accounting equation can be

represented, Assets = Claims, and that it is the logic underlying the balance sheet.

IX. Assign homework. Problem 1-34 will give students practice in recording transactions in

horizontal financial statements models.

X. Filling in the gaps. Remind students that they are responsible for reading the textbook to

fill in the gaps because not all information can be presented in class.

XI. Enrichment. If time permits, have students complete ATC Case 1-1 (financial statement

analysis).