Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 15 Performance Evaluation

15-1

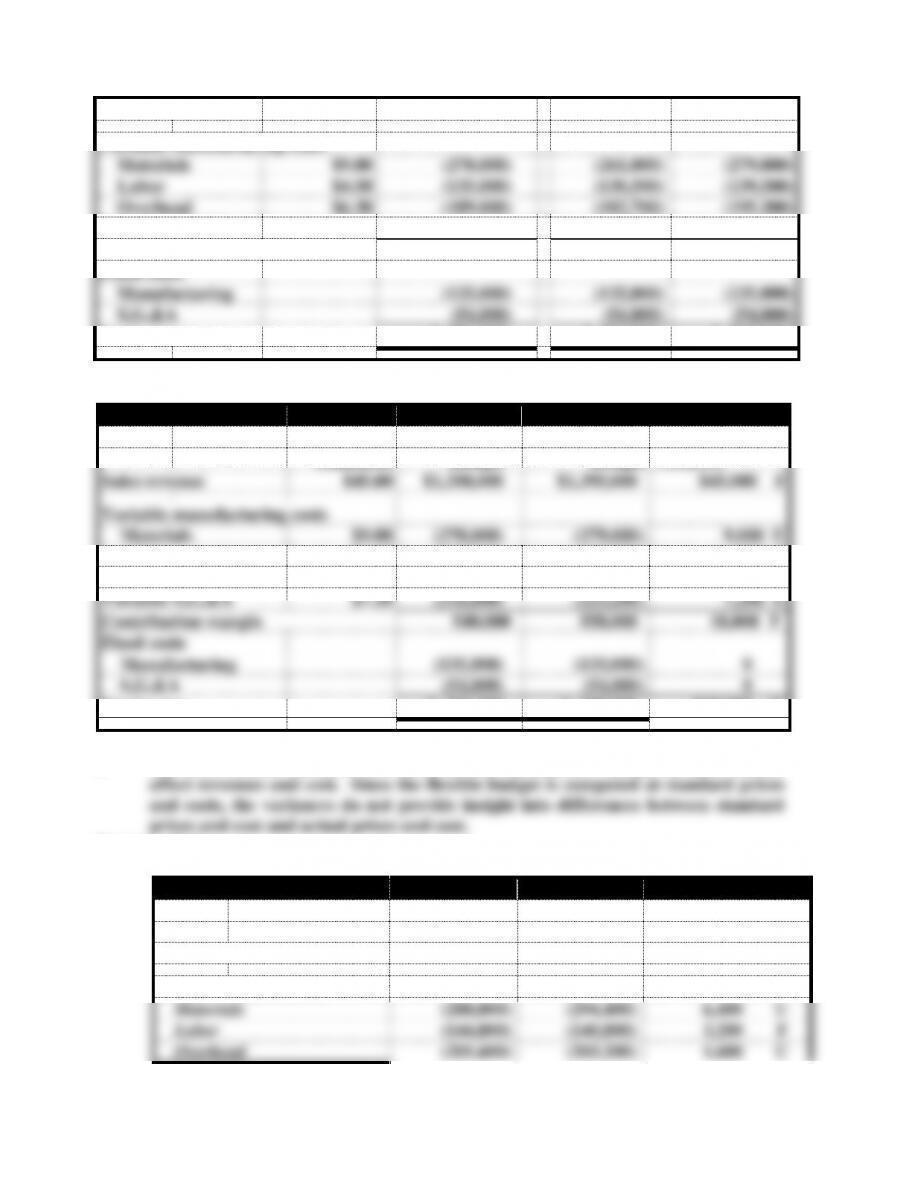

Sales revenue

$45.00

$1,350,000

$1,305,000

$1,395,000

Variable manufacturing costs

Materials

$9.00

(270,000)

(261,000)

(279,000)

Labor

$4.50

(135,000)

(130,500)

(139,500)

Overhead

$6.30

(189,000)

(182,700)

(195,300)

Variable S,G,&A

$7.20

(216,000)

(208,800)

(223,200)

Contribution margin

540,000

522,000

558,000

Fixed costs

Manufacturing

(135,000)

(135,000)

(135,000)

S,G,&A

(54,000)

(54,000)

(54,000)

Net income

$ 351,000

$ 333,000

$ 369,000

c. & d.

Number of units

30,000

31,000

Per Unit

Master

Flexible

Volume

Standards

Budget

Budget

Variances

Sales revenue

$45.00

$1,350,000

$1,395,000

$45,000 F

Variable manufacturing costs

Materials

$9.00

(270,000)

(279,000)

9,000 U

Labor

$4.50

(135,000)

(139,500)

4,500 U

Overhead

$6.30

(189,000)

(195,300)

6,300 U

Variable S,G,&A

$7.20

(216,000)

(223,200)

7,200 U

Contribution margin

540,000

558,000

18,000 F

Fixed costs

Manufacturing

(135,000)

(135,000)

0

S,G,&A

(54,000)

(54,000)

0

Net income

$ 351,000

$ 369,000

$18,000 F

e. The sales volume variances are useful in determining how changes in sales volume

Problem 15-21

a. & b.

Number of units

32,000

32,000

Flexible

Actual

Flexible Budget

Budget

Results

Variances

Sales revenue

$1,440,000

$1,392,000

$48,000 U

Variable manuf. costs

Materials

(288,000)

(294,400)

6,400 U

Labor

(144,000)

(140,800)

3,200 F

Overhead

(201,600)

(203,200)

1,600 U

Chapter 15 Performance Evaluation

15-2

Variable G,S,&A

(230,400)

(224,000)

6,400 F

Contribution margin

576,000

529,600

46,400 U

Fixed costs

Manufacturing

(135,000)

(125,000)

10,000 F

G,S,&A

(54,000)

(58,000)

4,000 U

Net income

$ 387,000

$ 346,600

$40,400 U

c. Upper-level marketing managers are responsible for the sales variance. These managers

are normally responsible for establishing the sales price. In this case the actual sales price

Many different managers may be responsible for fixed manufacturing cost variances. For

example, the personnel manager may be responsible for supervisory salaries while

production managers may be responsible for the cost of equipment rentals. In this case, the

Problem 15-22

a. Operating profit margin = Operating income ÷ Sales = $50,000 ÷ $1,000,000 = 5.00%

c. ROI = Operating profit margin x Turnover = 5.00% x 2 = 10.00%

d2. ROI = Operating profit margin x Turnover

= ($52,000 ÷ $1,000,000) x ($1,000,000 ÷ $500,000) = 10.40%

Problem 15-23

a. Operating income, instead of net Income, should be used to determine the ROI for the

Morrison investment center because operating income is a better measurement of

Chapter 15 Performance Evaluation

15-3

b. Operating assets, instead of total assets, should be used to determine the ROI for the

c. Operating Assets = Total Assets – Non-Operating Assets

Operating Assets = $197,682 – $9,000 = $188,682

d. If ROI is the only performance measure for Morrison’s performance, the new investment

would hurt Morrison’s manager if the new ROI decreases. Morrison’s return on the new

Income from New Investment = $96,000 x 12% = $11,520

e. If Cole’s objective is profit maximization, residual income (RI), rather than ROI can

measure operating performance to reflect that objective better. Further computation

follows.

Original RI = $43,500 – ($188,682 x 10%) = $24,632 (rounded)

New RI = $55,020 – ($284,682 x 10%) = $26,552 (rounded)

Chapter 15 Performance Evaluation

15-4

Problem 15-24

a. Because the expected ROI (i.e., 18%) on the proposed investment is higher than

b. Computation of ROI if the proposed investment is accepted:

Operating

Assets

x

ROI

=

Operating

Income

Current

$6,000,000

x

.20

=

$1,200,000

Proposed

1,500,000

x

.18

=

270,000

Total

$7,500,000

=

$1,470,000

Accepting the proposed project would result in a decline of the division's ROI from 20% to

19.60%.

c. Residual income if investment is accepted:

Operating income – (Operating assets x Desired ROI) = RI

($7,500,000 x .196) – ($7,500,000 x .16) = $270,000

d. In this case, the ROI approach for performance evaluation may result in

suboptimization. In other words, the manager would be required to reduce the

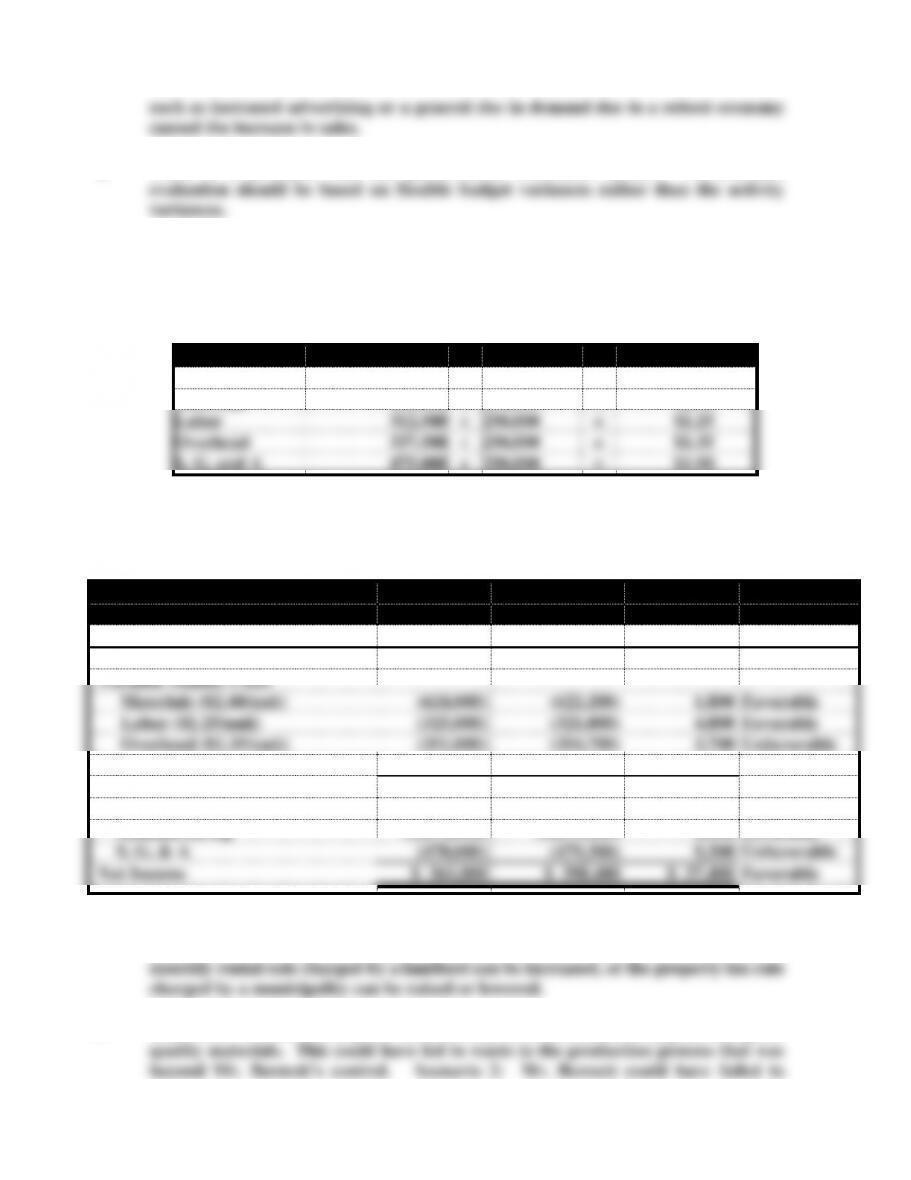

ATC 15-1

a. The increase in sales volume was not achieved by lowering the sales price. The

Chapter 15 Performance Evaluation

15-5

b. There is a problem with the performance evaluation system. Performance

c. To prepare a flexible budget, first determine the budgeted sales price, and the standard

cost per unit for materials, labor, overhead, and G,S,&A. These amounts are shown

below:

Dollars

Units

Cost Per Unit

Sales Price

$3,750,000

÷

250,000

=

$15.00

Materials

600,000

÷

250,000

=

$2.40

Labor

312,500

÷

250,000

=

$1.25

Overhead

337,500

÷

250,000

=

$1.35

S, G, and A

475,000

÷

250,000

=

$1.90

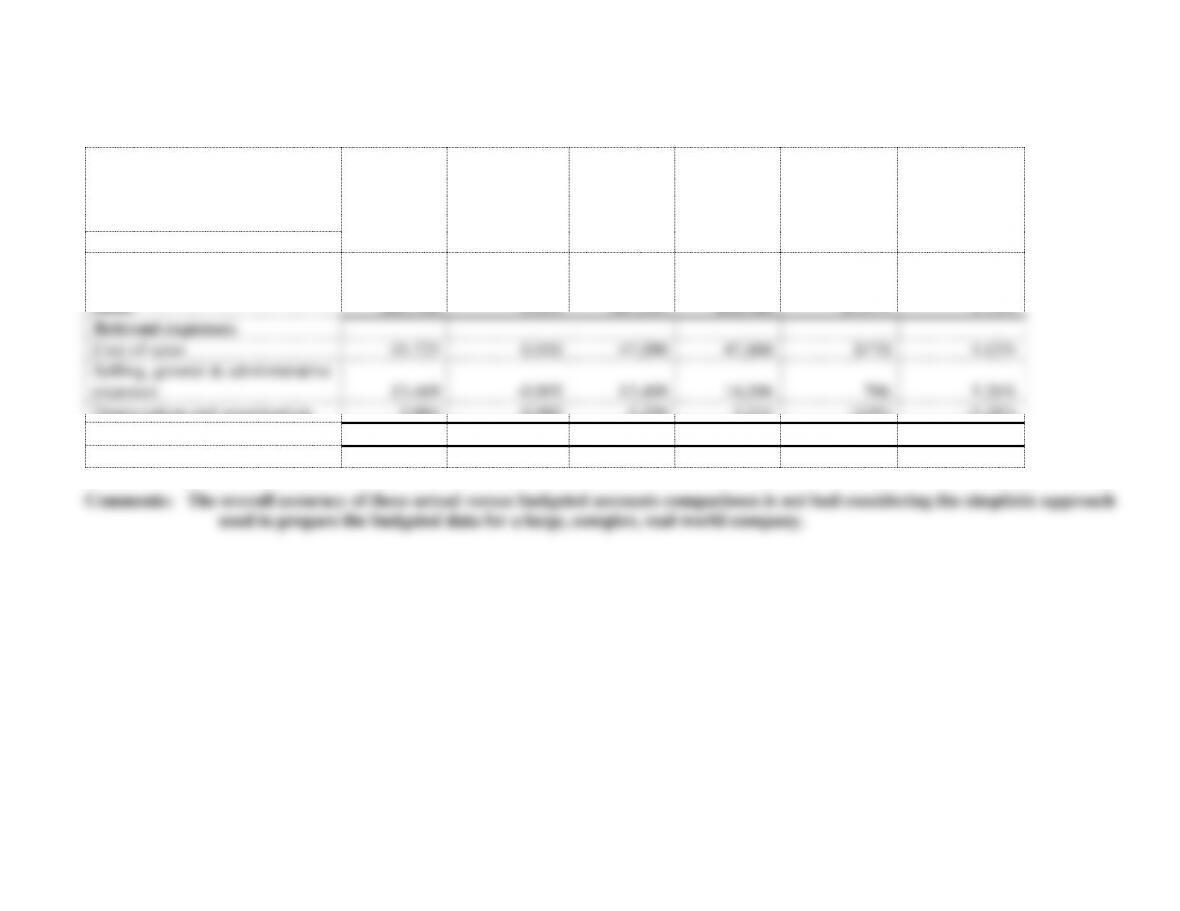

ATC 15-1 (continued)

The flexible budget variances are shown below.

Flexible

Actual

Budget

Results

Variances

Number of Units

260,000

260,000

0

Sales Revenue

$3,900,000

$3,950,000

$50,000

Favorable

Variable Manuf. Costs

Materials ($2.40/unit)

(624,000)

(622,200)

1,800

Favorable

Labor ($1.25/unit)

(325,000)

(321,000)

4,000

Favorable

Overhead ($1.35/unit)

(351,000)

(354,700)

3,700

Unfavorable

Variable S, G, & A ($1.90/unit)

(494,000)

(501,300)

7,300

Unfavorable

Contribution Margin ($8.10/unit)

2,106,000

2,150,800

44,800

Favorable

Fixed Costs

Manufacturing

(1,275,000)

(1,273,100)

1,900

Favorable

S, G, & A

(470,000)

(479,300)

9,300

Unfavorable

Net Income

$ 361,000

$ 398,400

$ 37,400

Favorable

d. A cost is defined as fixed if it does not change when there is a change in activity, but

there are other things that can cause a “fixed” cost to change. For example, the

e. Scenario 1: The favorable price variance may have been attained by purchasing low

Chapter 15 Performance Evaluation

15-6

ATC 15-1 (continued)

f. Recall that the total variance is composed of price and usage variances. Note that

g. The fixed overhead volume variance was favorable, because more units were

Chapter 15 Performance Evaluation

15-7

ATC 15-2

1. Current ROI $8,640,000 ÷ $72,000,000 = 12%

ROI with additional investment $9,960,000* ÷ $84,000,000** = 11.86%

**$72,000,000 + $12,000,000

Since the new investment would decrease Bellco’s ROI, it would have a negative effect

2. Current residual income

$8,640,000 − (10% x $72,000,000) = $1,440,000

Residual Income with additional investment

Since the new investment would increase Bellco’s residual income, it would have a

3. & 4. In-class requirements.

5. ROI is more likely to produce suboptimization because an opportunity that would

Chapter 15 Performance Evaluation

15-8

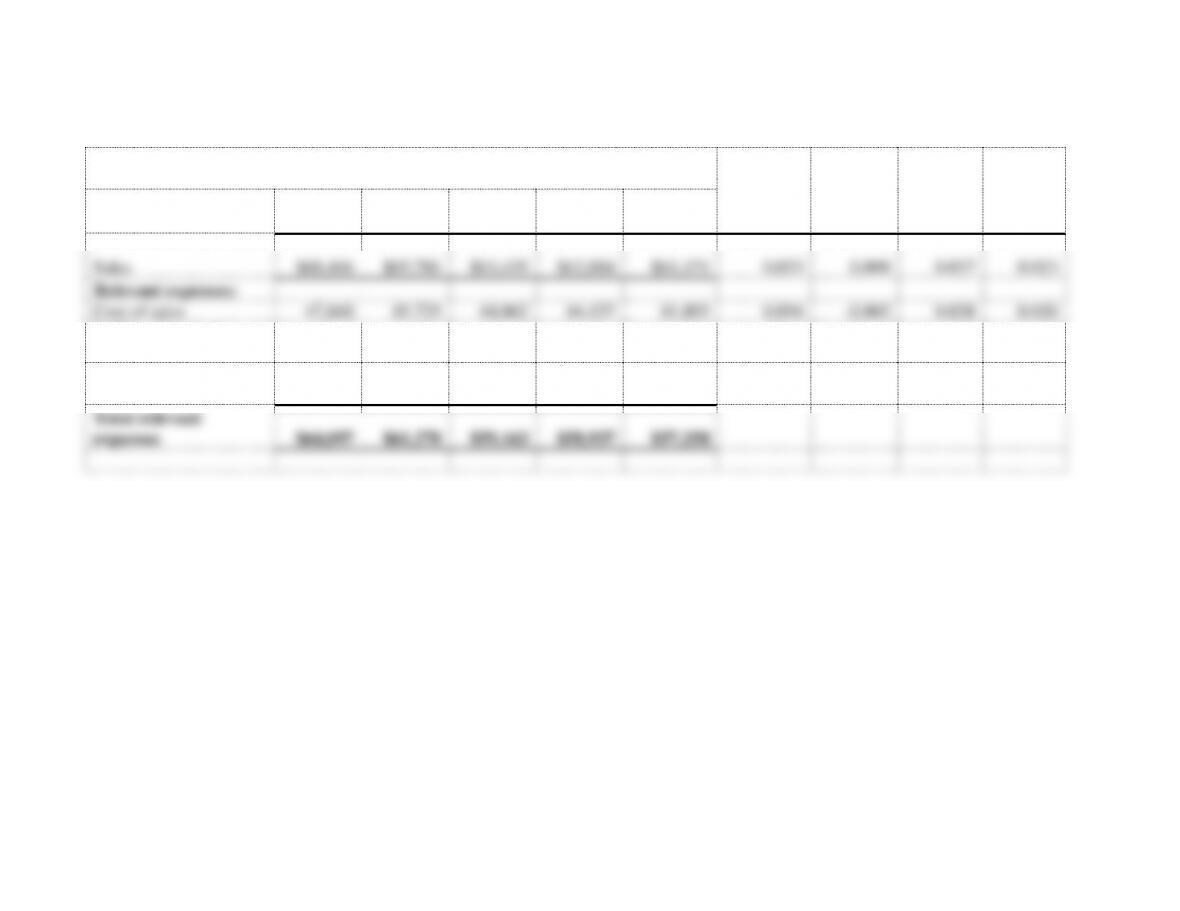

ATC 15-3

Raw Data and Percentage Analysis from Target’s 2008 to 2012 Income

Statements

% of

change

2008 -

2009

% of

change

2009 -

2010

% of

change

2010 –

2011

Average

2008 –

2011

(dollar amounts in

millions)

2012

2011

2010

2009

2008

Sales

$68,466

$65,786

$63,435

$62,884

$61,471

0.023

0.009

0.037

0.023

Relevant expenses:

Cost of sales

47,860

45,725

44,062

44,157

41,895

0.054

-0.002

0.038

0.030

Selling, general &

administrative expenses

14,106

13,469

13,078

12,954

13,704

-0.055

0.010

0.030

-0.005

Depreciation and

amortization

2,131

2,084

2,023

1,826

1,659

0.101

0.108

0.030

0.080

Total relevant

expenses

$64,097

$61,278

$59,163

$58,937

$57,258

Chapter 15 Performance Evaluation

15-9

ATC 15-3 continued

Target’s Budgeted and Actual

Income Statement Accounts

Actual **

2011

3 year

Average

Change

2008 to 2011

Budget

2012

Actual

2012

Difference

% Different

from budget

(dollar amounts in millions)

Sales

$65,786

0.023

$67,295

$68,466

$1,171

1.74%

Relevant expenses:

Cost of sales

45,725

0.030

47,090

47,860

$770

1.63%

Selling, general & administrative

expenses

13,469

-0.005

13,400

14,106

706

5.26%

Depreciation and amortization

2,084

0.080

2,250

2,131

(119)

-5.28%

Total relevant expenses

$61,278

$62,740

$64,097

$1,357

2.16%

Chapter 15 Performance Evaluation

15-10

ATC 15-4

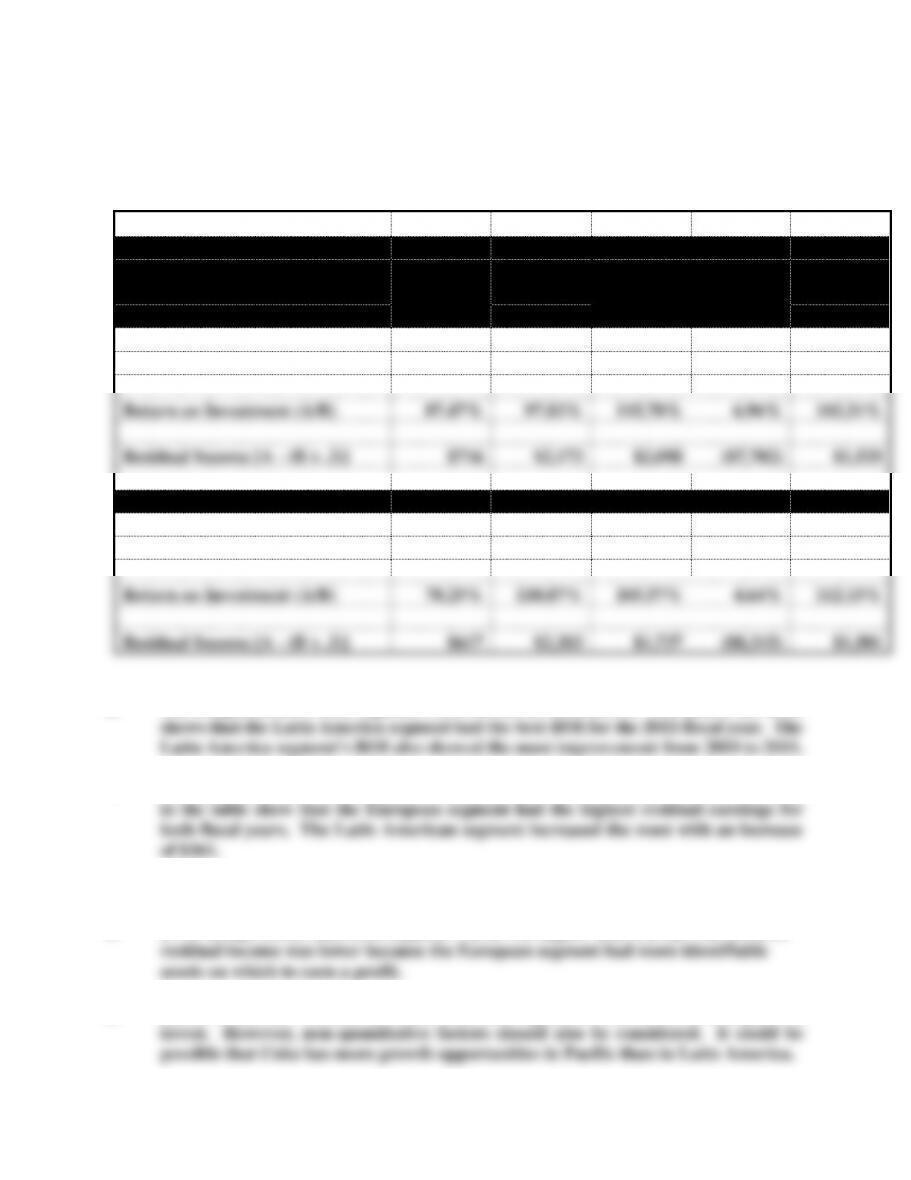

The computations below are used to answer requirements a., b., c., and d.

Dollar amounts in millions

Eurasia

Latin

North

2011 FY

& Africa

Europe

America

America

Pacific

(A) Segment income

1,089

3,134

2,832

2,325

2,154

(B) Identifiable assets

1,245

3,204

2,446

33,422

2,085

Return on Investment (A/B)

87.47%

97.82%

115.78%

6.96%

103.31%

Residual Income [A - (B x .3)]

$716

$2,173

$2,098

($7,702)

$1,529

2010 FY

(A) Segment income

1,000

3,020

2,426

1,523

2,049

(B) Identifiable assets

1,278

2,724

2,298

32,793

1,827

Return on Investment (A/B)

78.25%

110.87%

105.57%

4.64%

112.15%

Residual Income [A - (B x .3)]

$617

$2,203

$1,737

($8,315)

$1,501

a. The computations of each segment’s ROI are in the table above. The data in the table

b. The computations of each segment’s residual income are in the table above. The data

ATC 15-1 (continued)

c. Even though Latin American segment’s ROI was higher than Europe’s in 2011, its

d. Based on the ROI’s alone, the Latin American segment seems to be the best place to

Chapter 15 Performance Evaluation

15-11

ATC 15-5

a. Mr. Dawson is hoping that his workers will work faster if they think the standard is 21

b. In the short-term the workers may very well try to meet the 21 minute standard. If they

In the long-run, several problems may arise. If they cannot meet the standard, they may

become disillusioned with the standard costing system and simply stop trying to work

efficiently. This could lead to even poorer performance due to their having no faith in the

If the workers should learn that Mr. Dawson has lied to them about the proper standard,

his effectiveness as a manager will be greatly compromised. In the future, anytime they