Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

5-1

ANSWERS TO QUESTIONS - CHAPTER 5

1. Accounts receivable are the expected future receipts that arise

when a company permits its customers to buy now and pay later.

rate, and other credit terms.

2. The net realizable value is the amount expected to be collected

3. Allowance for Doubtful Accounts is a contra asset account.

4. Estimating uncollectible accounts expense improves the accuracy

5. When using the allowance method, uncollectible accounts

6. The most common format for reporting accounts receivable on

the balance sheet is gross receivables less the allowance for

7. The practice of reestablishing a previously written off account,

5-2

8. Factors for use in estimating uncollectible accounts include:

(1) the percentage of uncollectible accounts from years past.

9. Recognizing uncollectible accounts expense reduces accounts

10. A write-off of an uncollectible account when the allowance

11. The recovery of an uncollectible account when the allowance

12. The primary advantage of using the allowance method is that it

13. If the company is an established business, it will examine its

credit history; that is, the actual write-offs for the previous year as

14. The percent of receivables is a more accurate measure because it

5-3

15. An aging of accounts receivable schedule classifies all receivables

by their due date. When using an aging schedule for estimating

16. A promissory note is a legal document that sets forth credit terms

17. a. Maker: The borrower or debtor.

b. Payee: The person to whom the note is made

payable.

e. Maturity date: The date on which the maker must repay

the principal and any unpaid interest.

18. Interest is computed as:

Principal x Annual interest rate x Time outstanding

20. The matching concept matches revenue and expenses to the

period in which they are earned or incurred. By accruing interest,

5-4

21. Liquidity refers to how quickly assets are expected to be

22. The adjusting entry for accrued interest is generally recorded

23. Big Corp. would report interest revenue of $360 for 2014

computed as follows:

24. When Big Corp. collects the $12,720, $12,000 will be reported as

25. It is generally beneficial to accept major credit cards because the

26. The acceptance of major credit cards enables a business to avoid

the cost of uncollectible accounts and the clerical costs of

27. (1) First In, First Out - The inventory cost flow method that

assumes that the first items purchased are the first items

sold for the purpose of computing cost of goods sold and

inventory.

5-5

(4) Specific Identification - The inventory cost flow method that

assigns cost to cost of goods sold based on the specific cost

of each unit sold.

28. One advantage of the specific identification method is that both

the inventory account and cost of goods sold reflect the actual

29. FIFO allocates the cost of the first units purchased to the first

units sold; consequently, in a period of rising prices, this would

30. LIFO allocates the cost of the last units purchased to the first

units sold; consequently, in a period of rising prices, this would

5-6

31. In an inflationary period, i.e., a period where prices are

consistently rising, FIFO will produce the highest amount of

income. This is true because the items purchased first (and at the

32. In an inflationary period, FIFO will produce the largest amount of

total assets. (Refer to the discussion for Question 31.) The

33. Flow of costs refers to the assumption that is made for the

purpose of determining the cost of inventory items that are sold

when preparing financial statements. The cost flow assumption

that a business makes may have nothing to do with the actual

34. In a world where there is no income tax, the choice of cost flow

method would not affect the statement of cash flows because it

is simply allocating some of the cost of inventory purchased to

5-7

35. Key Company (first year of operations):

Beginning inventory $ -0-

Merchandise purchased 1,000 units @ $25 25,000

Cost of Goods Sold 850 units @ $25 21,250

36. The amount of cost of goods sold for Key Company will be

different using different cost flow assumptions because the units

purchased during the second year have a different cost than

those purchased the previous year.

Beginning inventory 150 units @ $25 $ 3,750

Merchandise purchased 1,500 units @ $27 40,500

Total 1,650 $44,250

Units sold 1,500

5-8

Cost of Goods Sold $40,500

Weighted Average: Total Cost Total Units = Cost per unit

37. It may be advantageous to use FIFO for financial statement

purposes because it produces the smallest cost of goods sold and

consequently, the highest gross margin and net income. It also

38. In an inflationary period, for a business subject to income tax,

39. A deflationary period, i.e., a period of falling prices, would

produce results opposite of those for an inflationary period. FIFO

SOLUTIONS TO EXERCISES - CHAPTER 5

EXERCISE 5-1

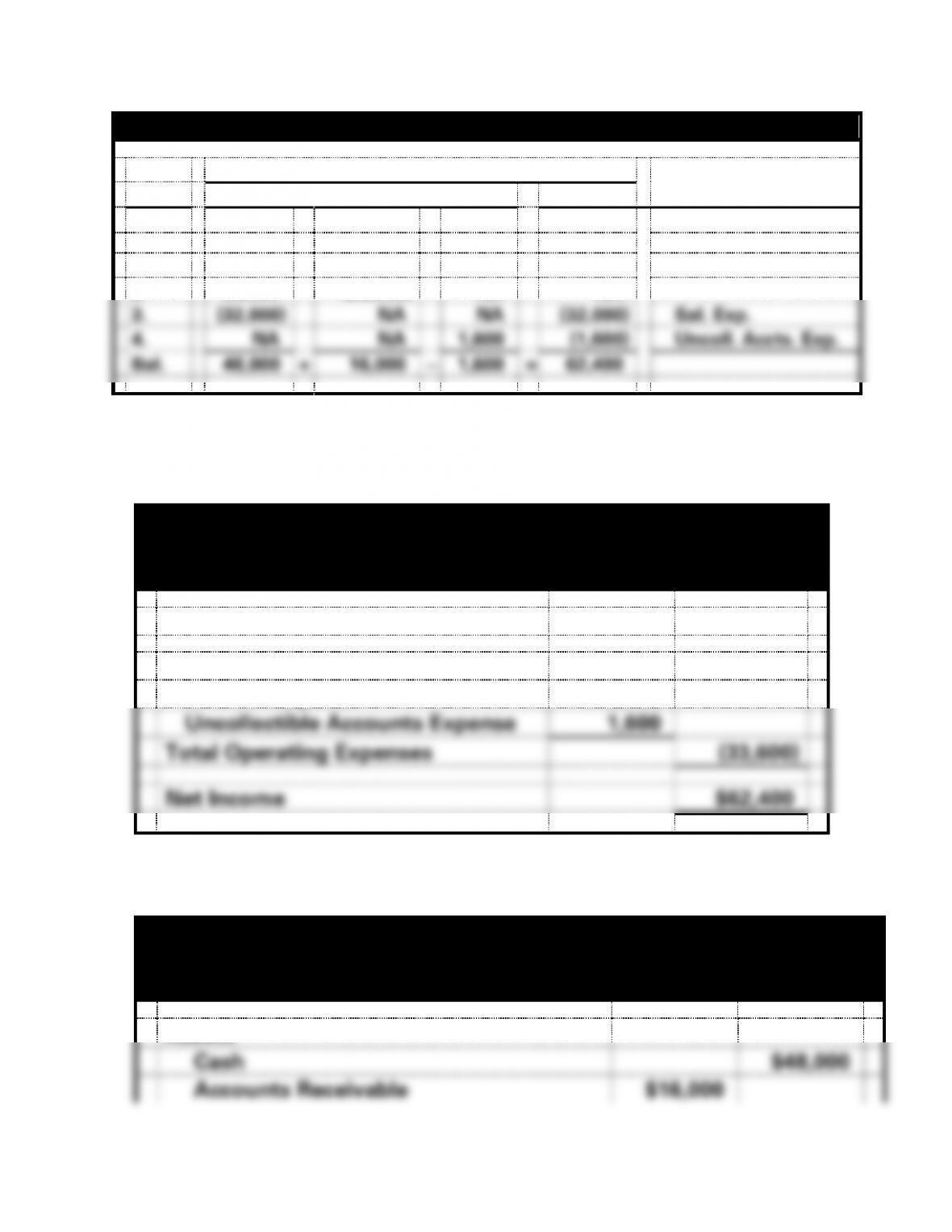

a.

Michelle’s Accounting Service

5-9

Horizontal Statements Model

Balance Sheet

Acct. Titles

Event

Assets

=

Equity

for R/E

Cash

+

Acct. Rec.

−

Allow.

Ret. Ear.

2014

1.

NA

96,000

NA

96,000

Svc. Rev.

2.

80,000

(80,000)

NA

NA

3.

(32,000)

NA

NA

(32,000)

Sal. Exp.

4.

NA

NA

1,600

(1,600)

Uncoll. Accts. Exp.

Bal.

48,000

+

16,000

−

1,600

=

62,400

b.

Michelle’s Accounting Service

Income Statement

For the Year Ended December 31, 2014

Service Revenue

$96,000

Operating Expenses

Salaries Expense

$32,000

Uncollectible Accounts Expense

1,600

Total Operating Expenses

(33,600)

Net Income

$62,400

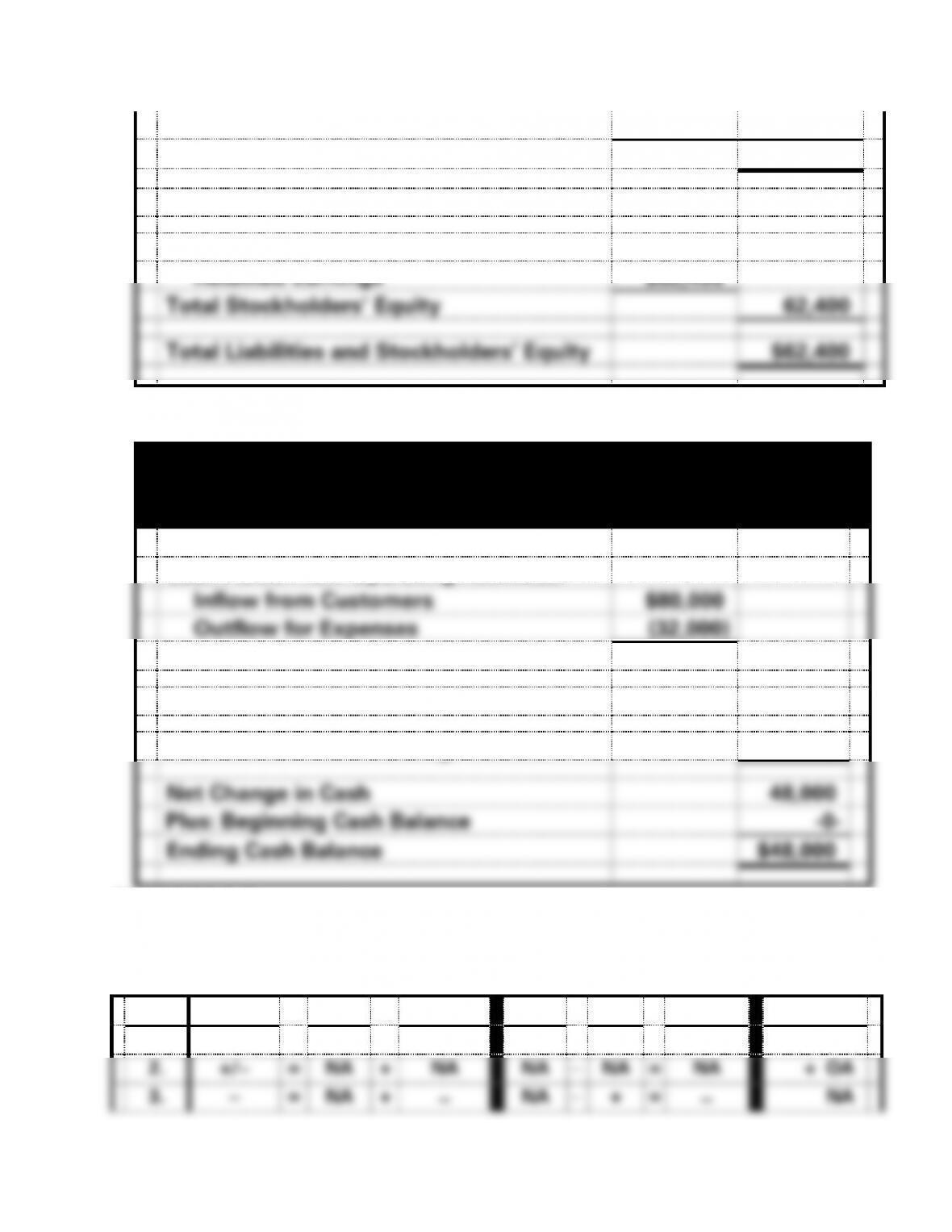

EXERCISE 5-1 b. (cont.)

Michelle’s Accounting Service

Balance Sheet

As of December 31, 2014

Assets

Cash

$48,000

Accounts Receivable

$16,000

5-10

Less: Allowance for Doubtful Accounts

(1,600)

14,400

Total Assets

$62,400

Liabilities

$ -0-

Stockholders’ Equity

Retained Earnings

$62,400

Total Stockholders’ Equity

62,400

Total Liabilities and Stockholders’ Equity

$62,400

Michelle’s Accounting Service

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash Flows From Operating Activities:

Inflow from Customers

$80,000

Outflow for Expenses

(32,000)

Net Cash Flow from Operating Activities

$48,000

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities

-0-

Net Change in Cash

48,000

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$48,000

EXERCISE 5-2

Event

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

1.

+

=

NA

+

+

+

−

NA

=

+

NA

2.

+/−

=

NA

+

NA

NA

−

NA

=

NA

+ OA

3.

−

=

NA

+

−

NA

−

+

=

−

NA

5-11

4.

+/−

=

NA

+

NA

NA

−

NA

=

NA

NA

5-12

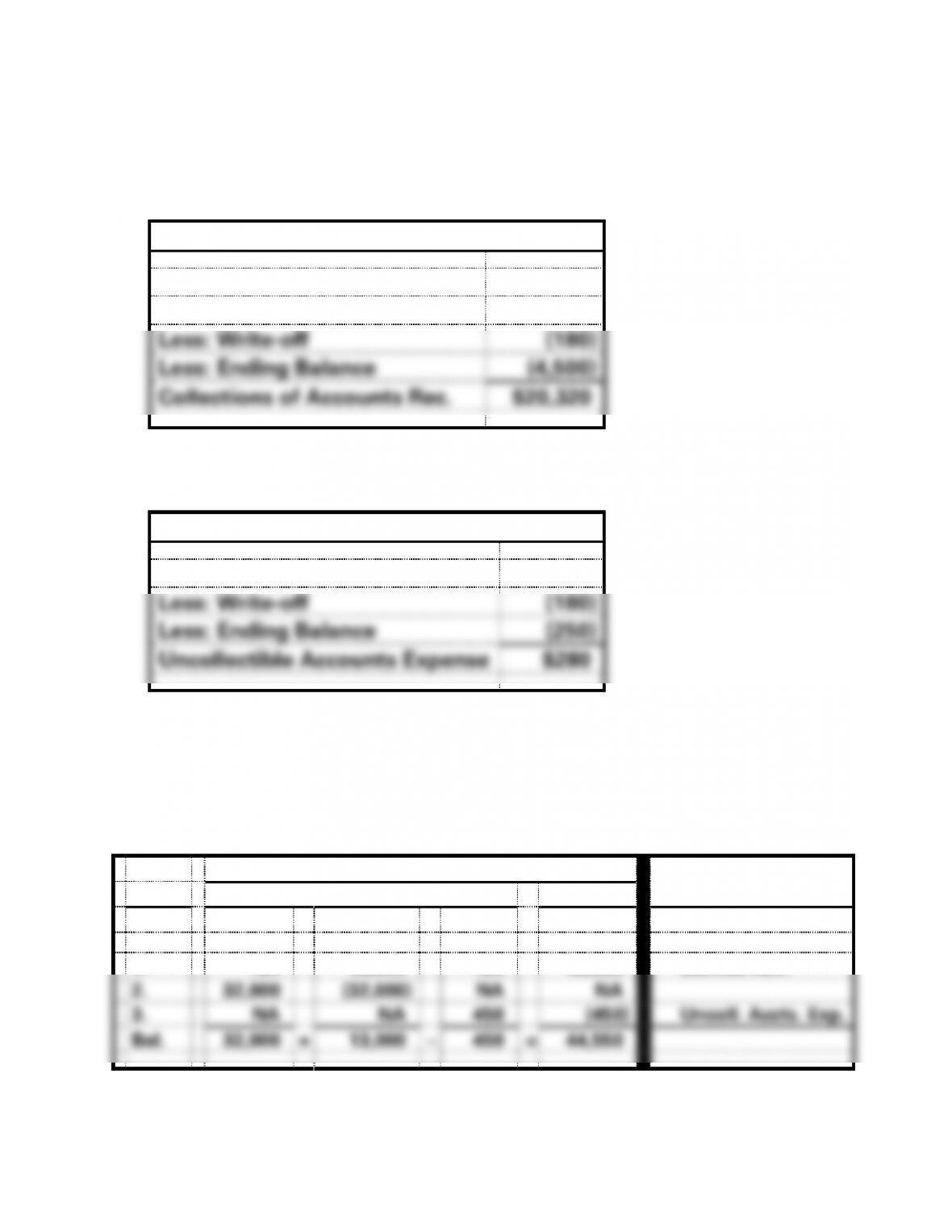

EXERCISE 5-3

a. Analyze the Accounts Receivable account:

Accounts Receivable

Beginning Balance

$ 4,000

Plus: Revenue on Account

21,000

Less: Write-off

(180)

Less: Ending Balance

(4,500)

Collections of Accounts Rec.

$20,320

b. Analyze the Allowance for Doubtful Accounts account:

Allowance for Doubtful Accounts

Beginning Balance

$150

Less: Write-off

(180)

Less: Ending Balance

(250)

Uncollectible Accounts Expense

$280

EXERCISE 5-4

a.

Balance Sheet

Acct. Titles for

Event

Assets

=

Equity

Retained Earnings

Cash

+

Acct. Rec.

−

Allow.

Ret. Ear.

2014

1.

NA

45,000

NA

45,000

Service Rev.

2.

32,000

(32,000)

NA

NA

3.

NA

NA

450

(450)

Uncoll. Accts. Exp.

Bal.

32,000

+

13,000

−

450

=

44,550

5-13

Balance Sheet

Acct. Titles for

Event

Assets

=

Equity

Retained Earnings