Exercise 11-16

a.

Contribution margin

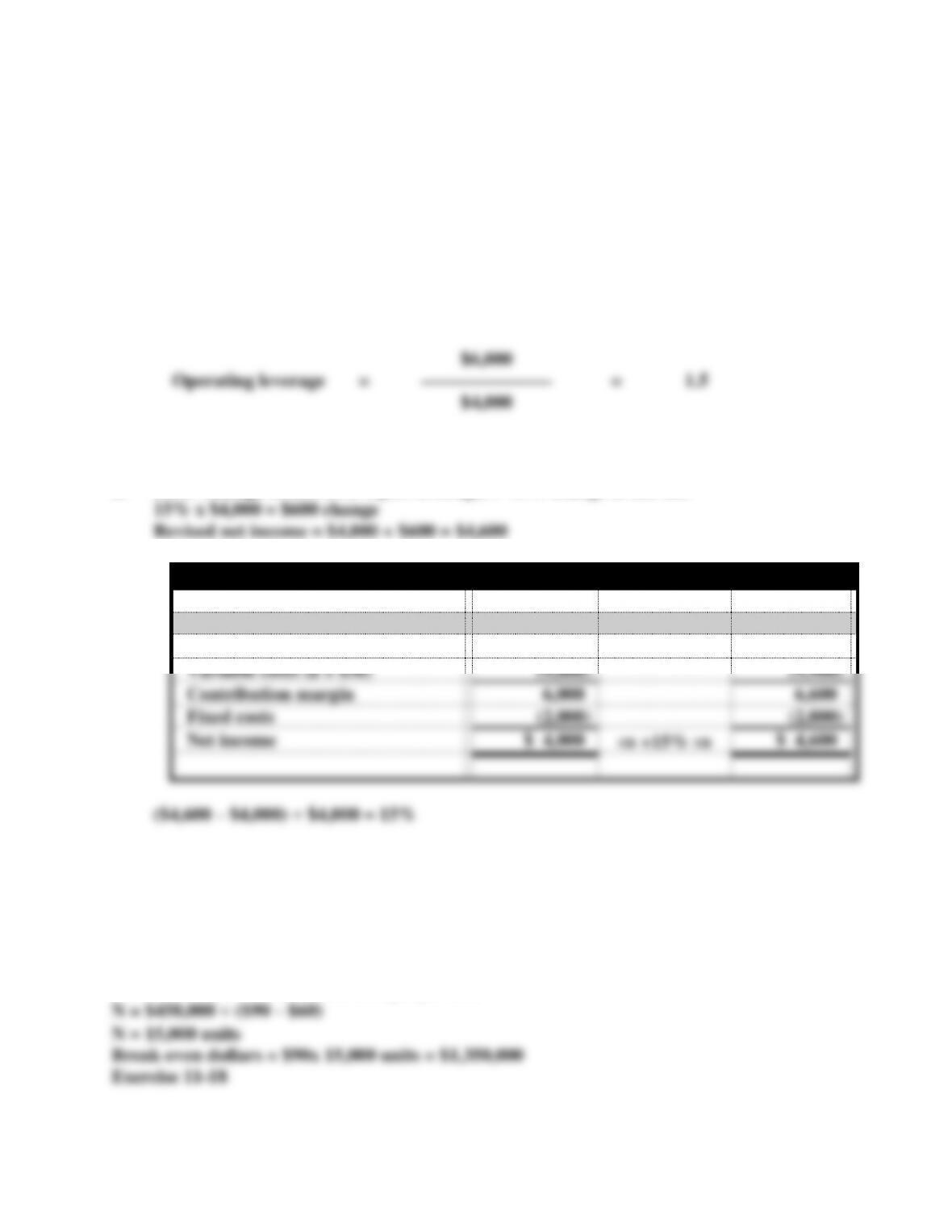

Operating leverage

=

—–––———————

Net income

$6,000

Operating leverage

=

———————

=

1.5

$4,000

b. (10% Change in rev. x 1.5 Oper. leverage) = 15% change in net inc.

Annual Income Statements

Sales volume in units (a)

250

% Change

275

Sales revenue (a x $60)

$15,000

+10%

$16,500

Variable costs (a x $36)

(9,000)

(9,900)

Contribution margin

6,000

6,600

Fixed costs

(2,000)

(2,000)

Net income

$ 4,000

+15%

$ 4,600

Exercise 11-17

N = Number of units to break-even

N = Fixed cost ÷ Contribution margin per unit

c.

Contribution margin = Sales price – Variable cost/Unit

= $64 – $40 = $24

Contribution margin ratio = Contribution margin per unit ÷ Sales price

Contribution margin ratio = $24 ÷ $64 = 37.50%

Exercise 11-19

a.

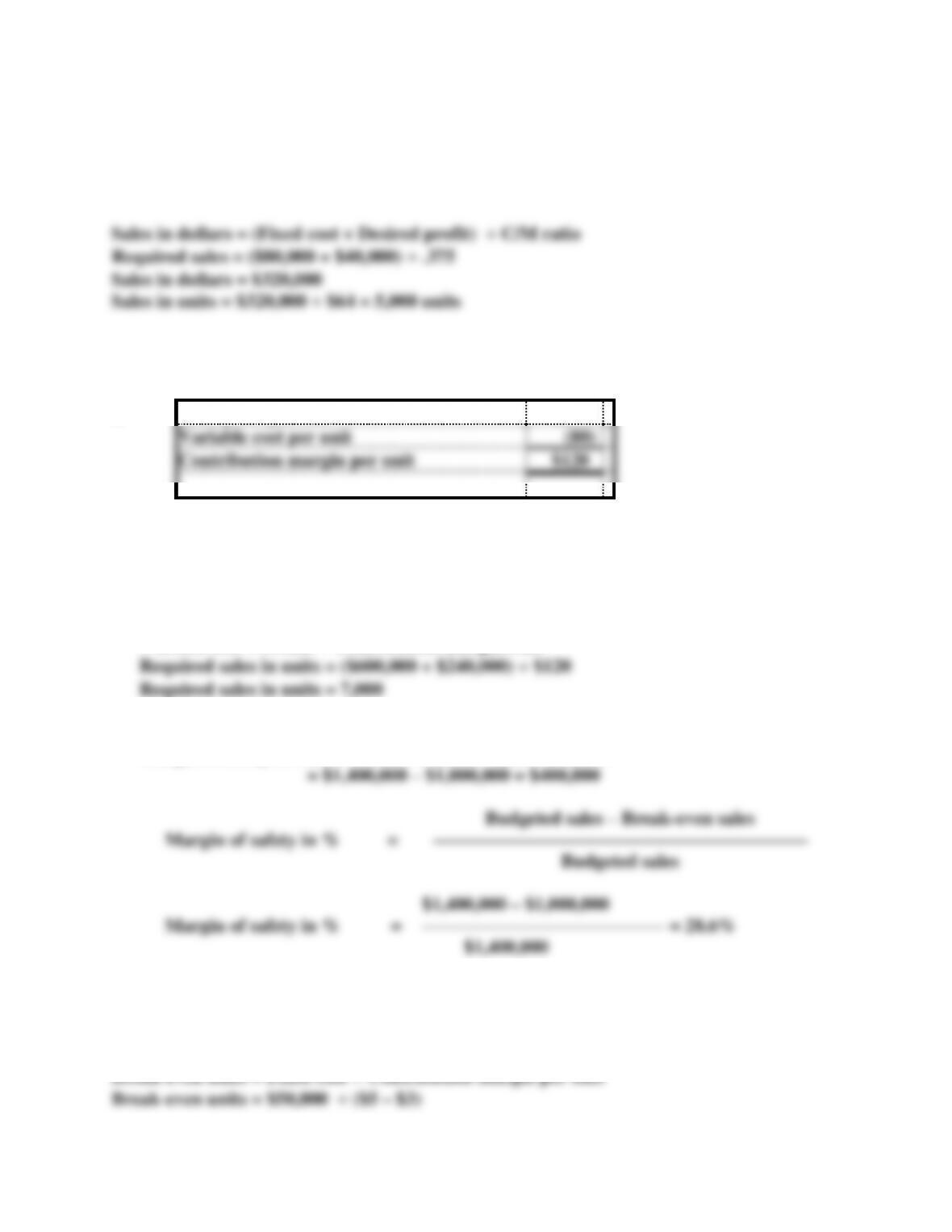

Sales price per unit

$200

Variable cost per unit

(80)

Contribution margin per unit

$120

b. Break-even in units = Fixed cost ÷ Contribution margin per unit

Break-even in units = $600,000 ÷ $120

Break-even in units = 5,000

c. Required sales in units

= (Fixed cost + Profit) ÷ Contribution margin/Unit

d. Margin of safety in units = 7,000 – 5,000 = 2,000 units

Margin of safety in sales $ = ($200 x 7,000) – ($200 x 5,000)

=

$1,400,000

Margin of safety computations:

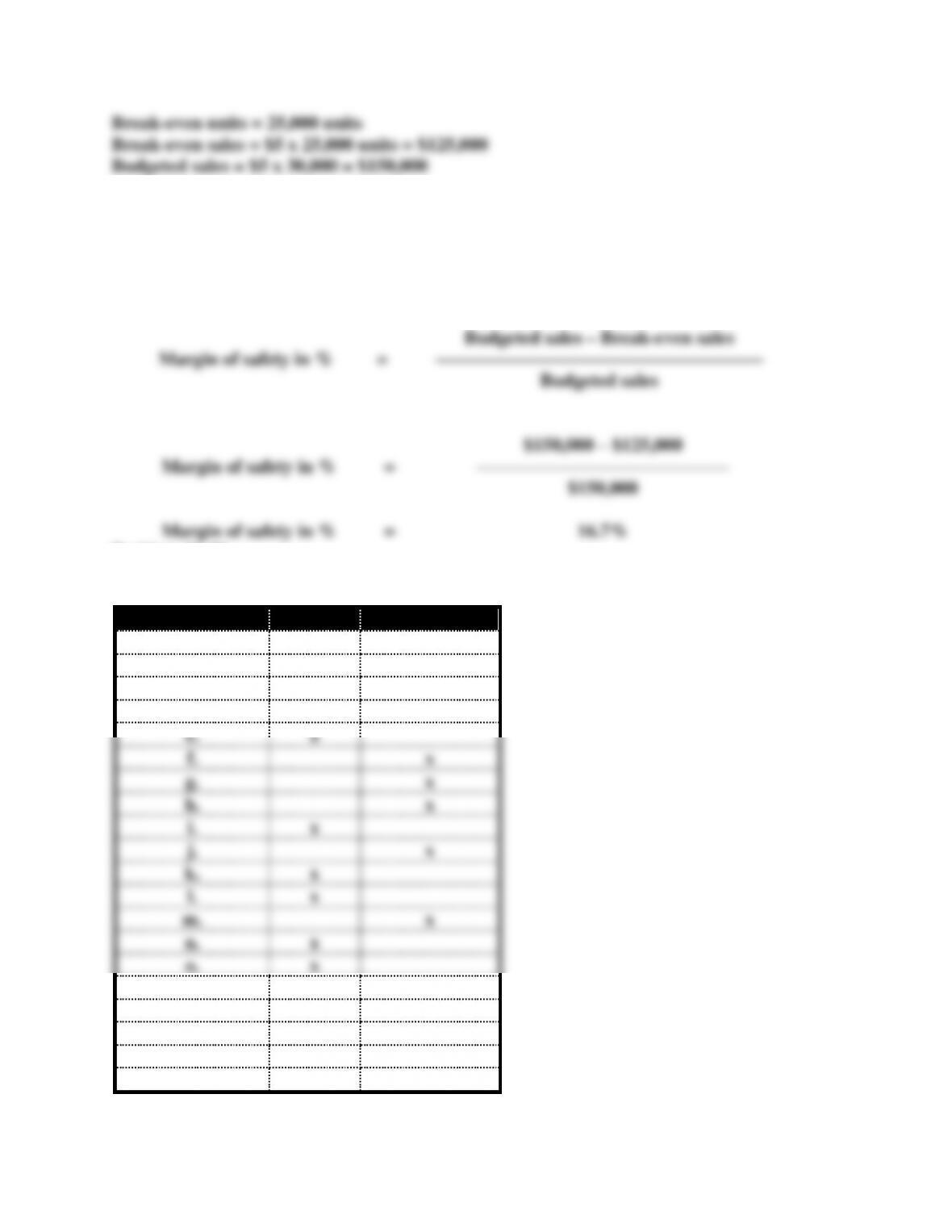

Margin of safety in units = 30,000 – 25,000 = 5,000 units

Margin of Safety in $ = $150,000 – $125,000 = $25,000

Budgeted sales – Break-even sales

Margin of safety in %

=

–––––––––––––––––––––––––––––––––––

Budgeted sales

$150,000 – $125,000

Margin of safety in %

=

–––––––––––––––––––––––––––

$150,000

Margin of safety in %

=

16.7%

Problem 11-21

Requirement

Fixed

Variable

a.

x

b.

x

c.

x

d.

x

e.

x

f.

x

g.

x

h.

x

i.

x

j.

x

k.

x

l.

x

m.

x

n.

x

o.

x

p.

x

q.

x

r.

x

s.

x

t.

x

Problem 11-22

a.

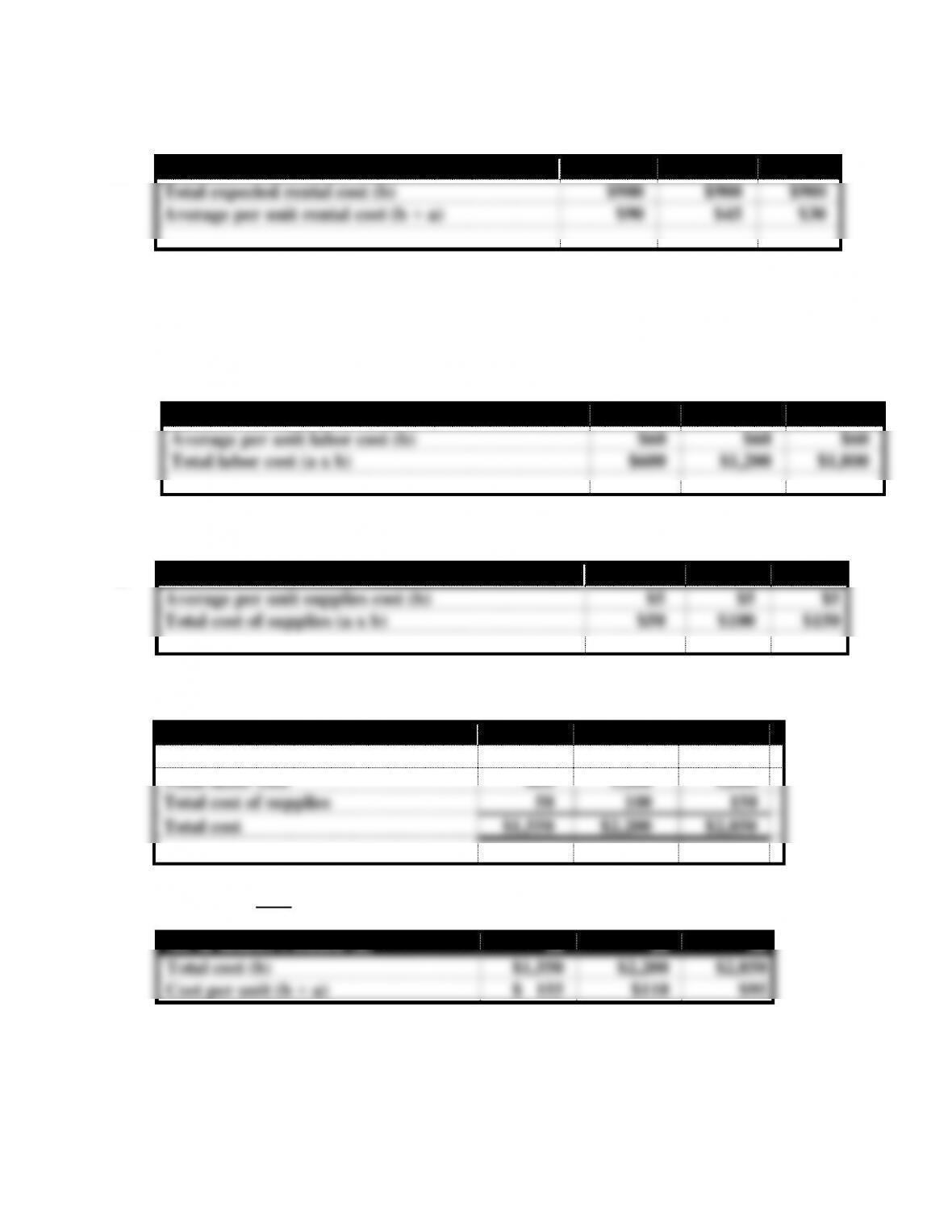

No. of Houses Cleaned (a)

10

20

30

Total expected rental cost (b)

$900

$900

$900

Average per unit rental cost (b ÷ a)

$90

$45

$30

Type of Cost: Since the total rental cost remains constant at $900 regardless of the number

of houses cleaned, it is a fixed cost.

Problem 11-22 (continued)

b.

No. of Houses Cleaned (a)

10

20

30

Average per unit labor cost (b)

$60

$60

$60

Total labor cost (a x b)

$600

$1,200

$1,800

Type of Cost: Since the total labor cost increases proportionately with the number of houses

cleaned, it is a variable cost.

c.

No. of Houses Cleaned (a)

10

20

30

Average per unit supplies cost (b)

$5

$5

$5

Total cost of supplies (a x b)

$50

$100

$150

Type of Cost: Since the total cost of supplies increases proportionately with the number of houses

cleaned, supplies cost is a variable cost.

d.

No. of Houses Cleaned

10

20

30

Total expected rental cost

$ 900

$ 900

$ 900

Total labor cost

600

1,200

1,800

Total cost of supplies

50

100

150

Total cost

$1,550

$2,200

$2,850

e. The amount of total cost shown below was determined in part d.

No. of Houses Cleaned (a)

10

20

30

Total cost (b)

$1,550

$2,200

$2,850

Cost per unit (b ÷ a)

$ 155

$110

$95

The decline in the cost per unit is caused by the fixed cost behavior that is applicable to the

equipment rental.

f. Ms. Buchanan means average cost per unit. It would be virtually impossible to determine

actual cost per unit. Consider these questions. Exactly how much window cleaner was

Problem 11-23

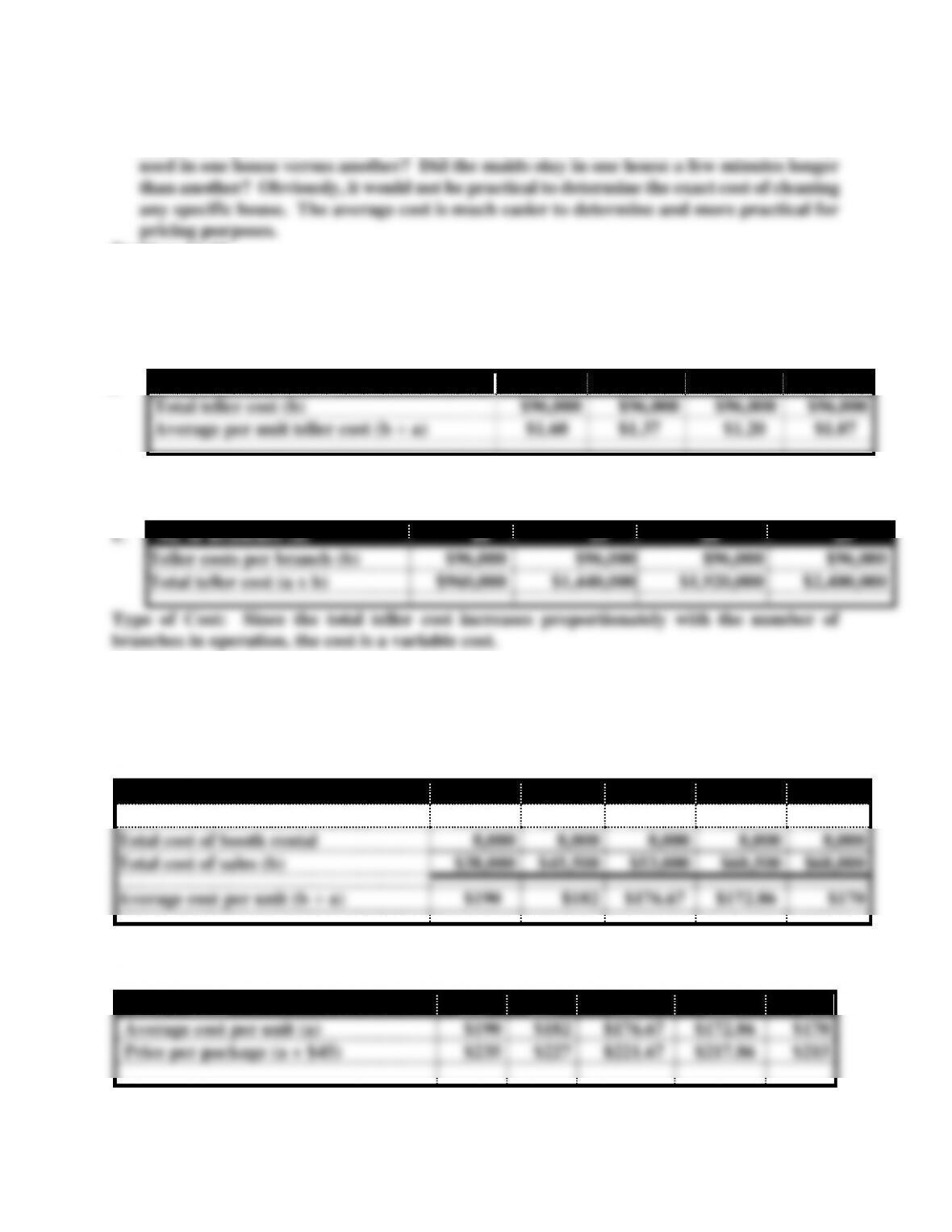

a. If a branch fails to process at least 60,000 transactions, the branch is closed. Branches

that process more than 90,000 transactions are transferred out of the start-up division.

Accordingly, the relevant range is 60,000 to 90,000 transactions.

b.

No. of Transactions (a)

60,000

70,000

80,000

90,000

Total teller cost (b)

$96,000

$96,000

$96,000

$96,000

Average per unit teller cost (b ÷ a)

$1.60

$1.37

$1.20

$1.07

Type of Cost: Since the total teller cost remains constant at $96,000 regardless of the number

of transactions processed, it is a fixed cost.

c.

No. of Branches (a)

10

15

20

25

Teller costs per branch (b)

$96,000

$96,000

$96,000

$96,000

Total teller cost (a x b)

$960,000

$1,440,000

$1,920,000

$2,400,000

Type of Cost: Since the total teller cost increases proportionately with the number of

branches in operation, the cost is a variable cost.

Problem 11-24

a.

Sales Volume in Units (a)

200

250

300

350

400

Total cost of software (a x $150)

$30,000

$37,500

$45,000

$52,500

$60,000

Total cost of booth rental

8,000

8,000

8,000

8,000

8,000

Total cost of sales (b)

$38,000

$45,500

$53,000

$60,500

$68,000

Average cost per unit (b ÷ a)

$190

$182

$176.67

$172.86

$170

The cost of booth space is fixed.

b.

Sales Volume

200

250

300

350

400

Average cost per unit (a)

$190

$182

$176.67

$172.86

$170

Price per package (a + $45)

$235

$227

$221.67

$217.86

$215

Problem 11-24 (continued)

c.

Trade Shows Attended (a)

1

2

3

4

5

Cost of booth rental (a x $8,000)

$8,000

$16,000

$24,000

$32,000

$40,000

The cost of booth space is variable.

d. The additional cost is $30 ÷ 50 units = $0.60 per unit.

Problem 11-25

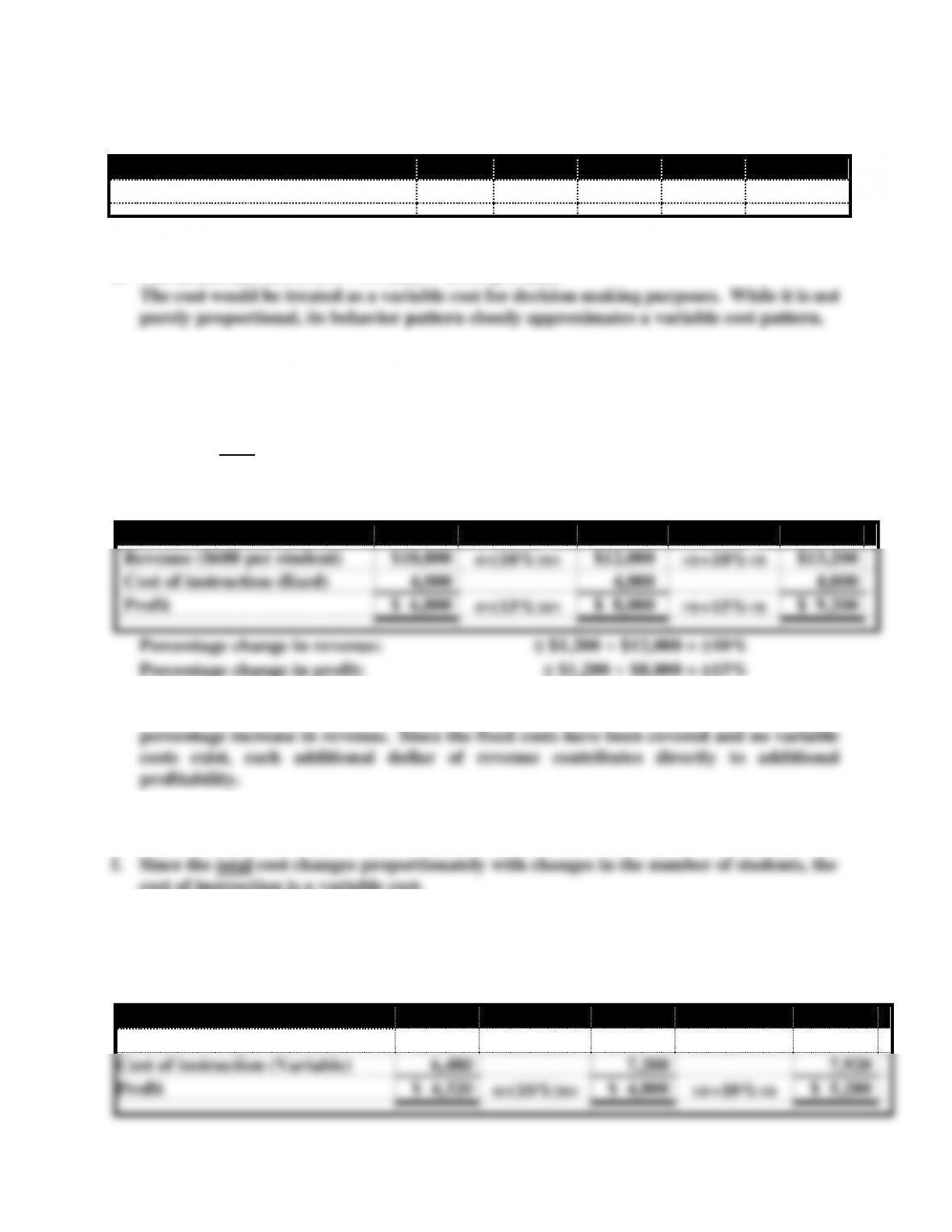

Part 1

a. Since the total cost remains constant at $4,000 regardless of how many students attend

the course, the cost of instruction is a fixed cost.

b. c. and d.

Number of Students

18

% Change

20

% Change

22

Revenue ($600 per student)

$10,800

(10%)

$12,000

+10%

$13,200

Cost of instruction (fixed)

4,000

4,000

4,000

Profit

$ 6,800

(15%)

$ 8,000

+15%

$ 9,200

Percentage change in revenue: $1,200 ÷ $12,000 = 10%

Percentage change in profit: $1,200 ÷ $8,000 = 15%

e. Operating leverage caused the percentage increase in profitability to be greater than the

Part 2

cost of instruction is a variable cost.

Problem 11-25 (continued)

g. h. and i.

Number of Students

18

% Change

20

% Change

22

Revenue ($600 per student)

$10,800

(10%)

$12,000

+10%

$13,200

Cost of instruction (Variable)

6,480

7,200

7,920

Profit

$ 4,320

(10%)

$ 4,800

+10%

$ 5,280

j. Since costs as well as revenue change with changes in the number of students attending

the course, the change in profit is proportional to the change in revenue.

Part 3

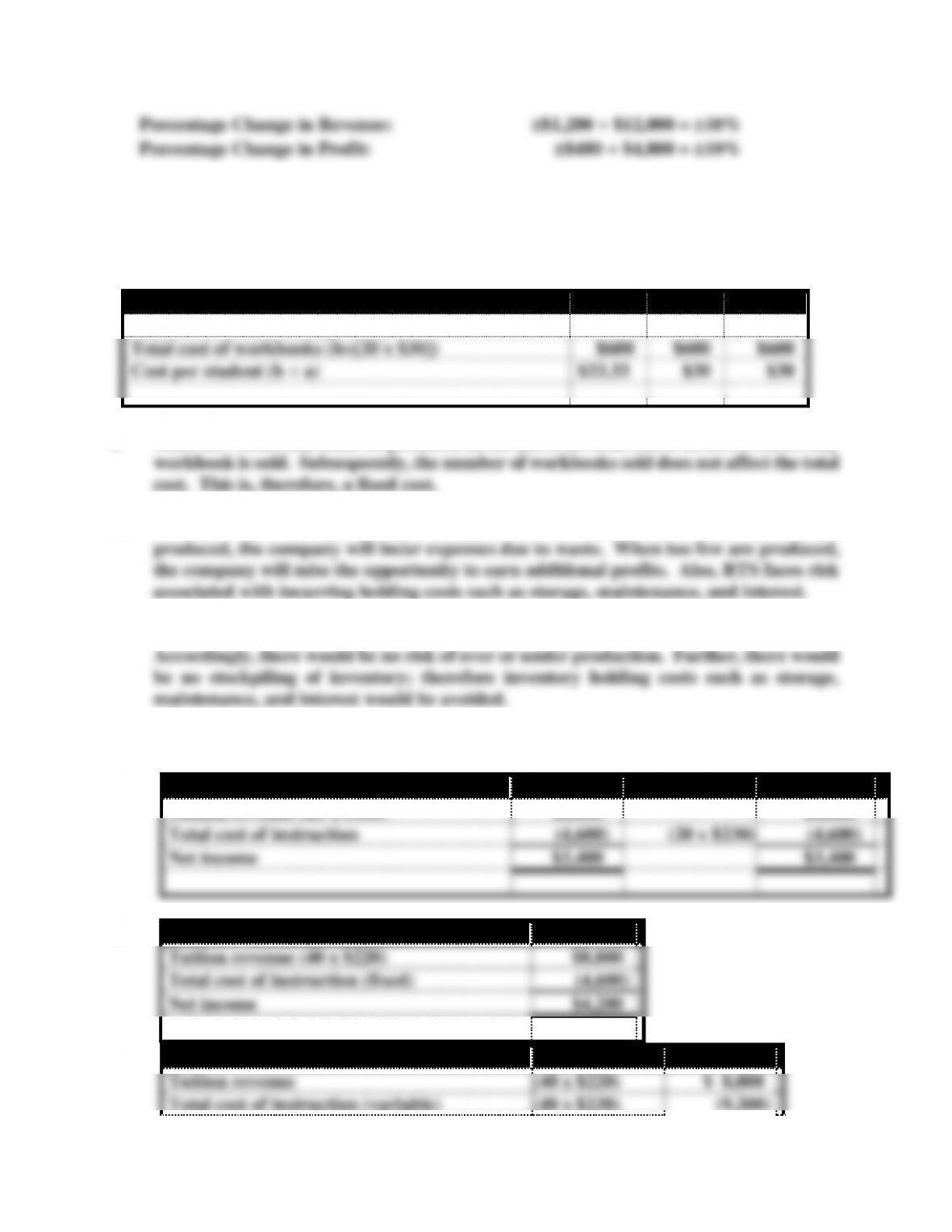

k.

Number of Students Attempting to Attend

18

20

22

Number of students accepted (a)

18

20

20

Total cost of workbooks (b=[20 x $30])

$600

$600

$600

Cost per student (b ÷ a)

$33.33

$30

$30

l. Since the workbooks must be produced in advance, the total cost is incurred before any

m. RTS faces the risk of producing too many or too few workbooks. When too many are

n. A just-in-time inventory system would produce goods as needed to meet sales demand.

Problem 11-26

a.

University

Orlando

Diego

Tuition revenue (20 x $400)

$8,000

$8,000

Total cost of instruction

(4,600)

(20 x $230)

(4,600)

Net income

$3,400

$3,400

c.

University

Diego

Tuition revenue

(40 x $220)

$ 8,800

Total cost of instruction (variable)

(40 x $230)

(9,200)

b.

University

Orlando

Tuition revenue (40 x $220)

$8,800

Total cost of instruction (fixed)

(4,600)

Net income

$4,200

Net income (loss)

$ (400)

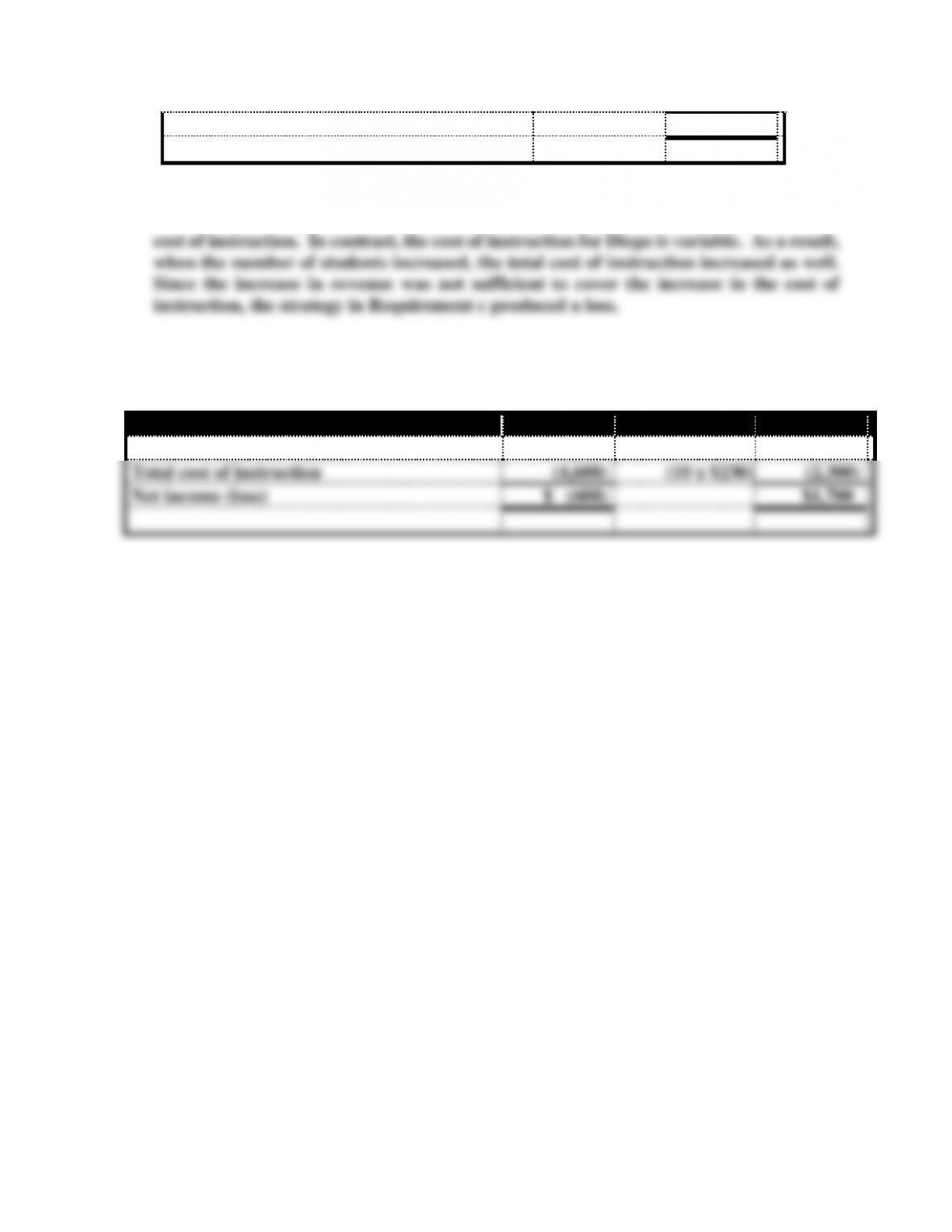

d. The strategy in Requirement b produced a profit because Orlando’s cost of instruction

is fixed. Accordingly, the increase in the number of students did not increase the total

e.

University

Orlando

Diego

Tuition revenue (10 x $400)

$ 4,000

$4,000

Total cost of instruction

(4,600)

(10 x $230)

(2,300)

Net income (loss)

$ (600)

$1,700

Problem 11-26 (continued)

f. When volume is insufficient to produce revenue that is above the level of fixed cost, the

g. When the revenue per unit is below the variable cost per unit, the enterprise will incur

additional losses for each unit produced and sold. This condition is depicted in

Problem 11-27

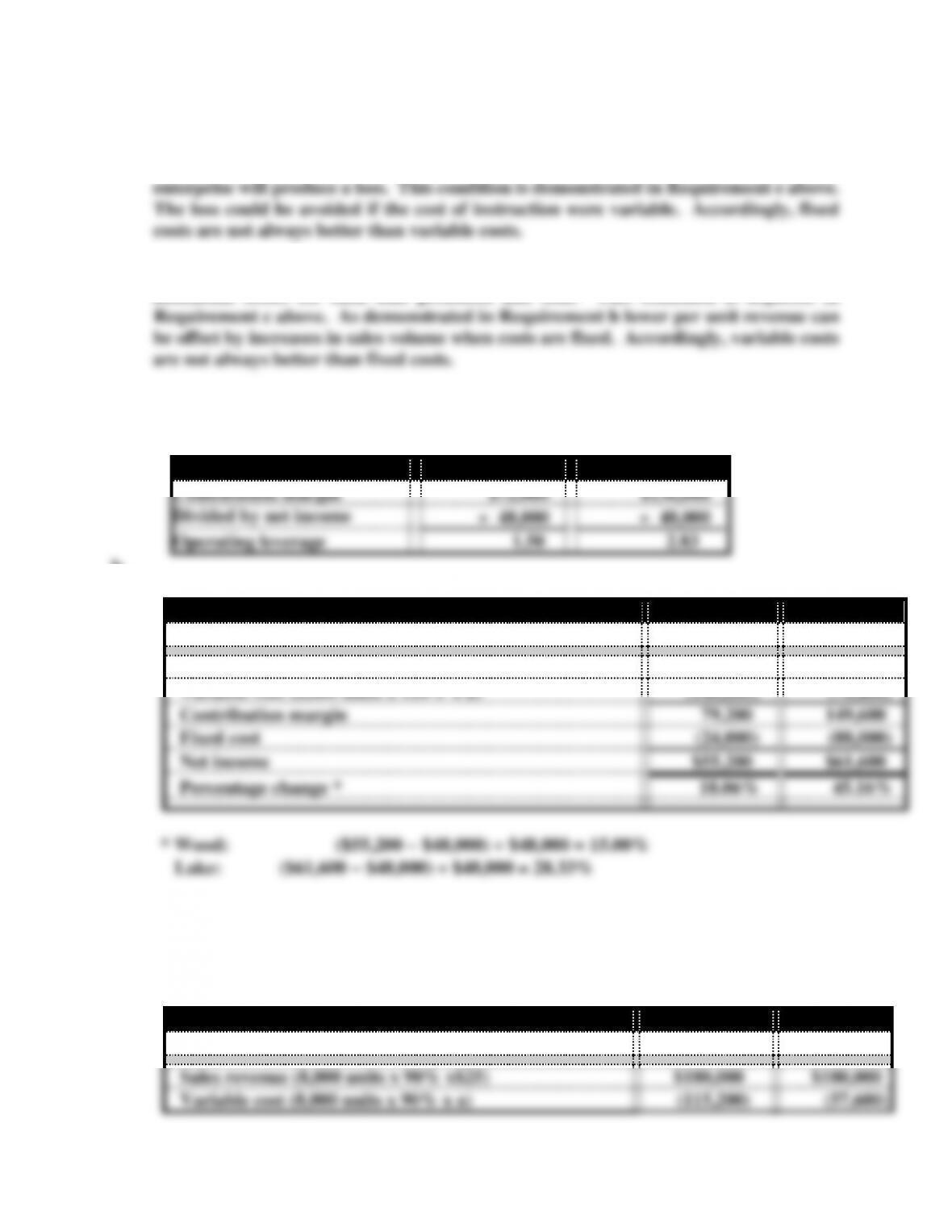

a.

Company Name

Wood

Lake

Contribution margin

$72,000

$136,000

Divided by net income

48,000

48,000

Operating leverage

1.50

2.83

b.

Company Name

Wood

Lake

Variable cost per unit (a)

$16.00

$8.00

Sales revenue (8,000 units x 110% x$25)

$220,000

$220,000

Variable cost (8,000 units x 110% x a)

(140,800)

(70,400)

Contribution margin

79,200

149,600

Fixed cost

(24,000)

(88,000)

Net income

$55,200

$61,600

Percentage change *

18.06%

45.16%

Problem 11-27 (continued)

c.

Company Name

Wood

Lake

Variable cost per unit (a)

$16.00

$8.00

Sales revenue (8,000 units x 90% x$25)

$180,000

$180,000

Variable cost (8,000 units x 90% x a)

(115,200)

(57,600)

Contribution margin

64,800

122,400

Fixed cost

(24,000)

(88,000)

Net income

$40,800

$34,400

Percentage change **

(18.06%)

(45.16%)

** Wood: ($40,800 − $48,000) $48,000 = (15.00%)

Lake: ($34,400 − $48,000) $48,000 = (28.33%)

d. The following memo is just an example. Students can form different opinions from

Memorandum

TO: Mr. Palvo Sorokin

FROM: John Doe

SUBJECT: Analysis and Recommendation Regarding Investment Opportunities

DATE: September 29, 2014

I have evaluated the income statements of Wood and Lake. Even though both companies

If the economy prospers in the long run, Lake will be the better choice for investment.

Problem 11-28

a. N = Number of units to break-even

Sales − Variable cost − Fixed cost = Profit

(Sales price x N) − (Variable cost per unit x N) = Fixed cost + Profit

b. N = Number of units to break-even

N = Fixed cost ÷ Contribution margin per unit