Answers to questions

1. A cost object is something whose cost one is trying to determine the cost. Cost objects

2. Managers need timely cost information. They may have to sacrifice accuracy in order

to get the information in time for decision making. For instance, managers need cost

3. For product costing one needs to accumulate the costs necessary to produce the

product, which are direct materials, direct labor, and overhead.

4. A direct cost is a cost that is easily traceable to a cost object. A cost–benefit analysis

5. A direct cost can be either a fixed or variable cost, and an indirect cost can be either

a fixed or variable cost. For example, supervisor salaries are usually fixed costs but

6. The depreciation on machinery used in only one department is a direct cost to that

7. The cost driver chosen to use in allocating a cost should be some activity that drives

the cost. In other words, the cost driver should be the activity responsible for changes in the

8. To determine an allocation rate divide the total cost to be allocated by the total cost

9. Direct material and direct labor costs are direct costs of the product. Overhead costs

10. It is not possible to trace some costs, such as the utility cost of heating a factory, to

individual products. It is not cost effective to trace other manufacturing costs to

11. Overhead costs are allocated to the product in order to estimate the total cost of

manufacturing the product and to evenly spread overhead costs over the units

12. The volume of production may vary from month to month. If an equal amount of

13. The statement is incorrect. Choosing an inappropriate allocation base can result in

inaccurate product costs which can cause poor decisions. An allocation base that does

14. Both students are correct. Costs should be estimated beforehand to determine the

project’s merits and to plan expenditures. Projected costs have to be estimated costs

15. A cost pool is the accumulation of individual costs into a single total. Cost pools

eliminate the need to allocate every single indirect cost the company incurs. By

accumulating similar costs that are linked to a common cost driver into a single pool,

one allocation can be made for the entire cost pool.

Exercise 12-1A

a.

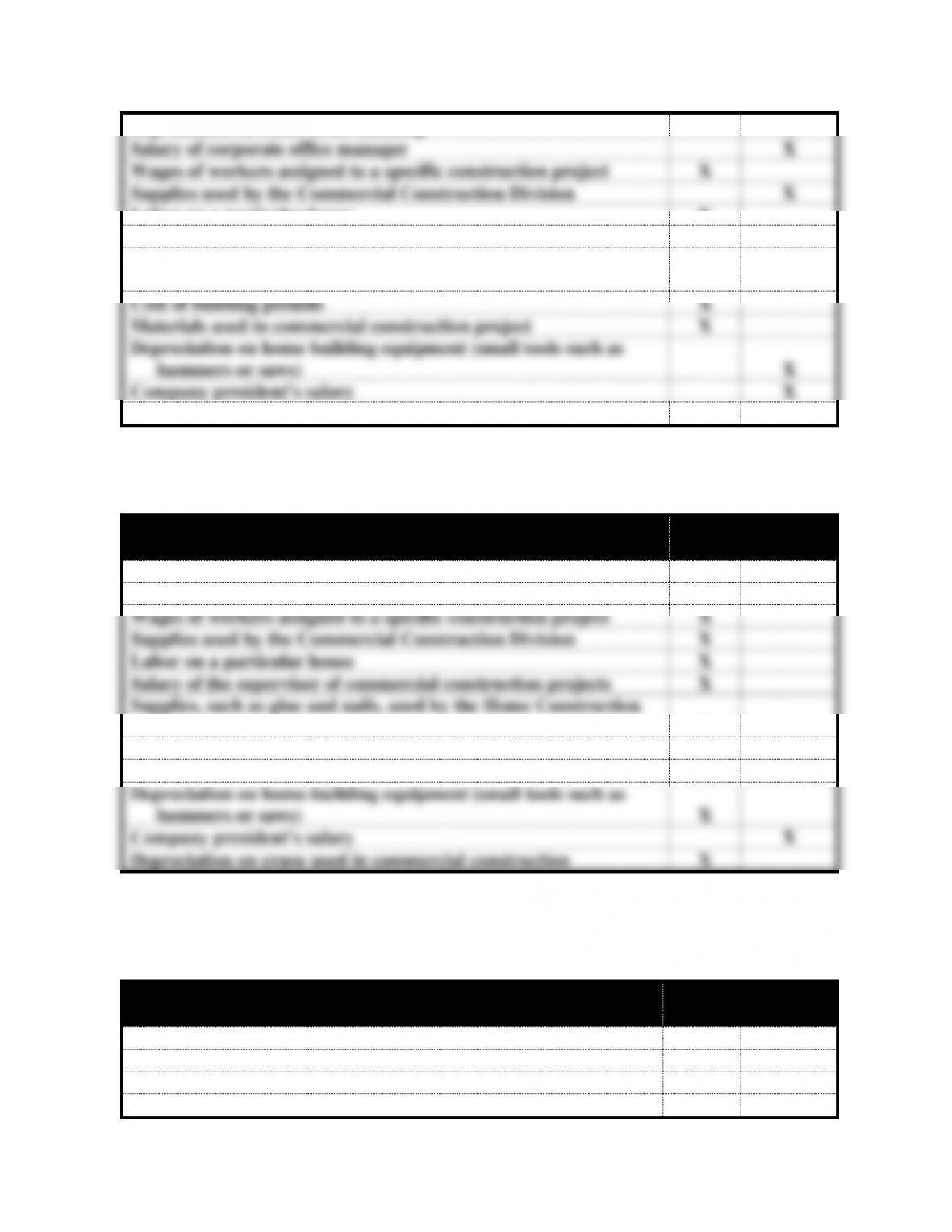

Items

Direct

Cost

Indirect

Cost

Depreciation on home office building

X

Salary of corporate office manager

X

Wages of workers assigned to a specific construction project

X

Supplies used by the Commercial Construction Division

X

Labor on a particular house

X

Salary of the supervisor of commercial construction projects

X

Supplies, such as glue and nails, used by the Home Construction

Division

X

Cost of building permits

X

Materials used in commercial construction project

X

Depreciation on home building equipment (small tools such as

hammers or saws)

X

Company president’s salary

X

Depreciation on crane used in commercial construction

X

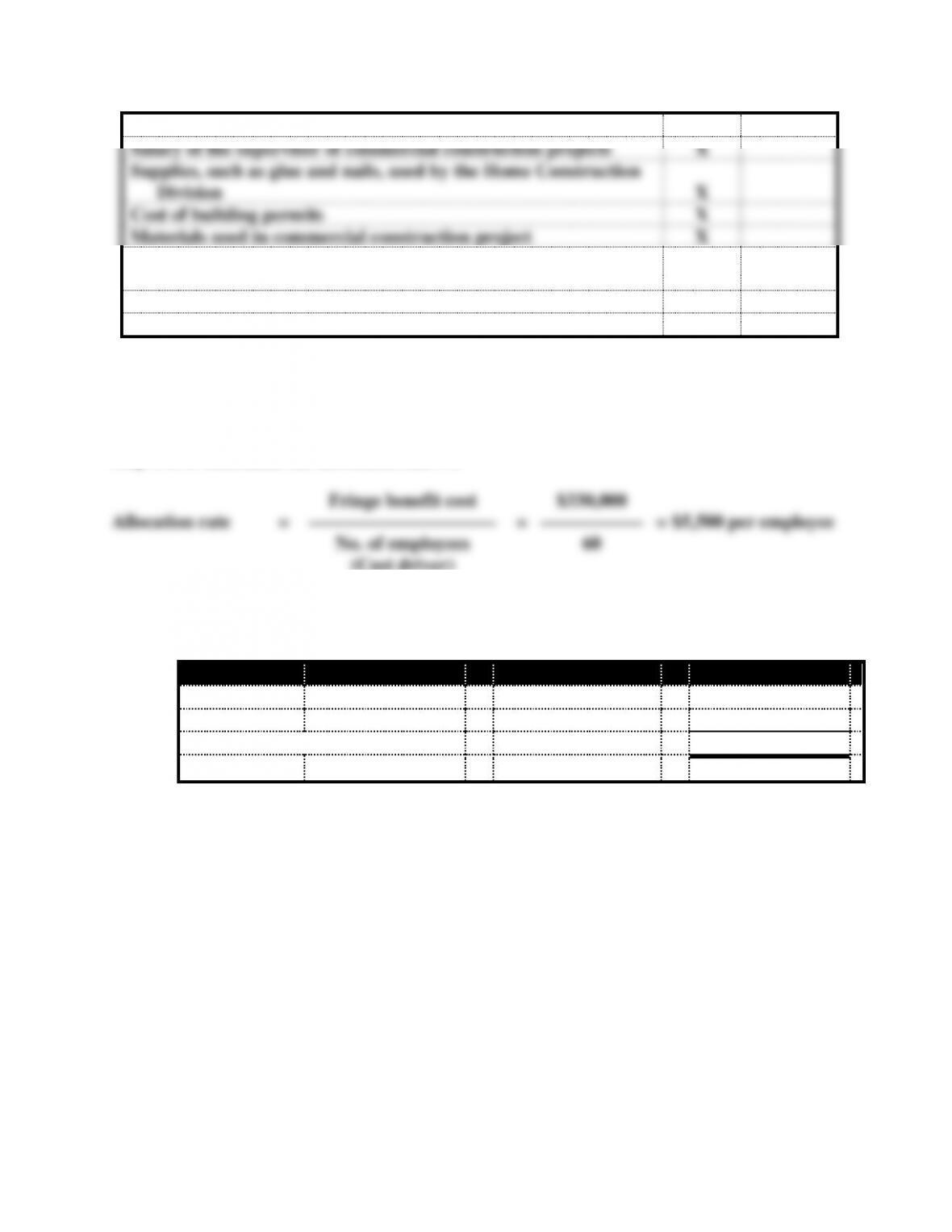

b.

Items

Direct

Cost

Indirect

Cost

Depreciation on home office building

X

Salary of corporate office manager

X

Wages of workers assigned to a specific construction project

X

Supplies used by the Commercial Construction Division

X

Labor on a particular house

X

Salary of the supervisor of commercial construction projects

X

Supplies, such as glue and nails, used by the Home Construction

Division

X

Cost of building permits

X

Materials used in commercial construction project

X

Depreciation on home-building equipment (small tools such as

hammers or saws)

X

Company president’s salary

X

Depreciation on crane used in commercial construction

X

Exercise 12-1 (continued)

c.

Items

Direct

Cost

Indirect

Cost

Depreciation on home office building

X

Salary of corporate office manager

X

Wages of worker assigned to a specific construction project

X

Supplies used by the Commercial Construction Division

X

Labor on a particular house

X

Salary of the supervisor of commercial construction projects

X

Supplies, such as glue and nails, used by the Home Construction

Division

X

Cost of building permits

X

Materials used in commercial construction project

X

Depreciation on home-building equipment (small tools such as

hammers or saws)

X

Company president’s salary

X

Depreciation on crane used in commercial construction

X

Exercise 12-2

Step 1 is to determine the allocation rate: 30

Fringe benefit cost

$330,000

Allocation rate

=

––––––––––––––––––––

=

–––––––––––

=

$5,500 per employee

No. of employees

60

(Cost driver)

Step 2 is to assign the cost by multiplying the allocation rate by the weight of the base

(i.e., cost driver) for each division:

Division

Allocation Rate

x

Weight of Base

=

Allocated Cost

A

$5,500

x

36

=

$198,000

B

$5,500

x

24

=

132,000

Total allocated cost

$330,000

Exercise 12-3

a.

Month

Jan

Feb

Mar

Apr

Total

Number of units

5,000

6,500

2,500

4,000

18,000

Allocation rate

Overhead cost

$72,000 x 4

for

=

–––––––––––––––

=

––––––––––––––

=

$16 per unit

overhead

No. of units

18,000

b. Assign the cost by multiplying the allocation rate by the weight of the base (cost

driver) for each month:

Month

Allocation Rate

x

Weight of Base

=

Allocated Cost

Jan.

$16

x

5,000

=

$ 80,000

Feb.

16

x

6,500

=

104,000

Mar.

16

x

2,500

=

40,000

Apr.

16

x

4,000

=

64,000

Total

$288,000

c. Computation of cost per unit:

Month

Jan.

Feb.

Mar.

Apr.

Number of units (a)

5,000

6,500

2,500

4,000

Expected cost

Overhead (b)

$ 80,000

$104,000

$40,000

$ 64,000

Direct costs (c = a x $18)

90,000

117,000

45,000

72,000

Total cost (d)

$170,000

$221,000

$85,000

$136,000

Cost per unit (d ÷ a)

$34.00

$34.00

$34.00

$34.00

Exercise 12-4

Cost Pool

÷

Base

Computation

Allocation Rate

Total overhead

÷

No. units

$300,000 ÷ 12,000 =

$25 per unit

b.

Allocation

Rate

x

Weight

of Base

=

January

Number of units (a)

1,600

a.

Indirect overhead costs

$25

x

1,600

=

$40,000

Direct materials (a x $64)

102,400

Direct labor (a x $52)

83,200

Total

$225,600

c. The amount computed in requirement b is an estimated amount. Accuracy could be

improved by waiting until December to determine the amount of product cost.

However, a manager may need to know the cost of products in January. Indeed, there

are necessary for a variety of decisions required to run a business.

Exercise 12-5

a.

Cost Items

Indirect

Materials

Indirect

Labor

Indirect

Utilities

Vacation pay

x

Sewer bill

x

Staples

x

Natural gas bill

x

Pens

x

Ink cartridges

x

Payroll taxes

x

Paper rolls for cash registers

x

Medical insurance

x

Salaries of secretaries

x

Water bill

x

b. Consumption of indirect materials is mostly related to sales activities. Therefore, sales

c. Accountants use cost pools to accumulate the costs of similar activities in the same

Exercise 12-6

a. Step 1 is to determine the allocation rate:

Allocation rate

Overhead cost

$360,000

for

=

–––––––––––––––––––

=

–––––––––––

=

$30 per DL hour

overhead cost

Direct labor hours

12,000

Step 2 is to assign the cost by multiplying the allocation rate by the weight of the base

(cost driver):

Product

Allocation Rate

x

Weight of Base

=

Allocated Cost

Vogue

$30

x

2,000

=

$ 60,000

Beauty

30

x

4,000

=

120,000

Glamour

30

x

6,000

=

180,000

Total

$360,000

b. Step 1 is to determine the allocation rate:

Allocation rate

for

$90 per machine hour

overhead cost

Product

Allocation Rate

x

Weight of Base

=

Allocated Cost

Vogue

$90

x

1,200

=

$108,000

Beauty

90

x

1,400

=

126,000

Glamour

90

x

1,400

=

126,000

Total

$360,000

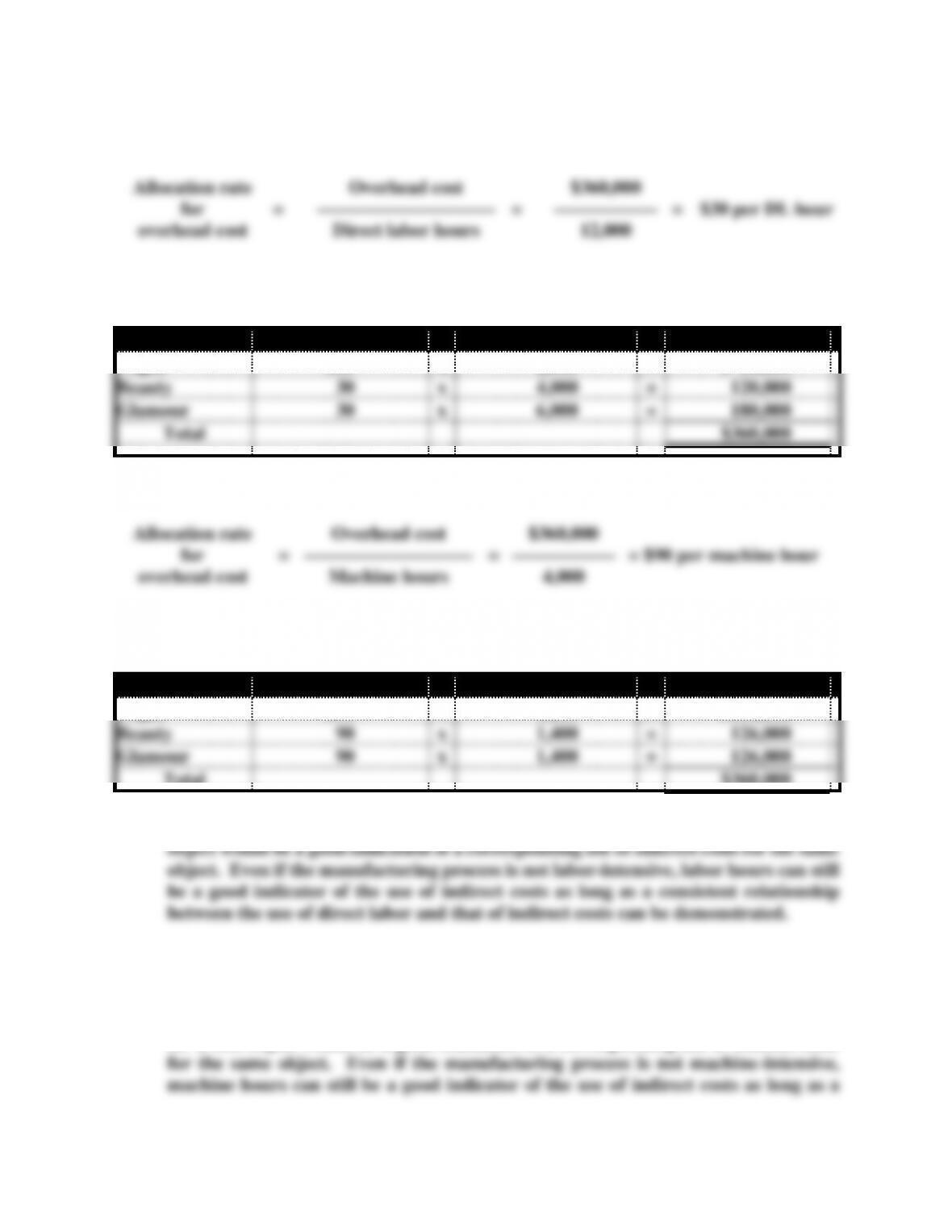

Exercise 12-7

a. Step 1 is to determine the allocation rate:

Allocation rate

Overhead cost

$250,000

for

=

–––––––––––––––

=

–––––––––––

=

$156.25 per machine hour

overhead cost

Machine hours

1,600

Step 2 is to assign the cost by multiplying the allocation rate by the weight of the base

(cost driver):

Product

Allocation Rate

x

Weight of Base

=

Allocated Cost

Cups

$156.25

x

200

=

$ 31,250

Tablecloths

156.25

x

600

=

93,750

Bottles

156.25

x

800

=

125,000

Total

$250,000

b. Cain may have chosen machine hours as the cost driver because the manufacturing

Exercise 12-8

There is a logical cause and effect relationship between the fringe benefits cost and

the direct labor hours. The more labor is employed, the more fringe benefits cost

are incurred. In other words, labor is driving the fringe benefits cost. Accordingly,

the measure of labor hours is a rational allocation base for fringe benefits cost.

Similarly, the measure of direct materials is a rational cost driver for indirect

materials cost. The more direct materials (e.g., lumber) are used, the more indirect

materials (e.g., nails, glue) are utilized. Accordingly, the measure of direct materials

cost is a rational base for the allocation of indirect materials cost. The computations

for the allocations and the total cost figures are shown below:

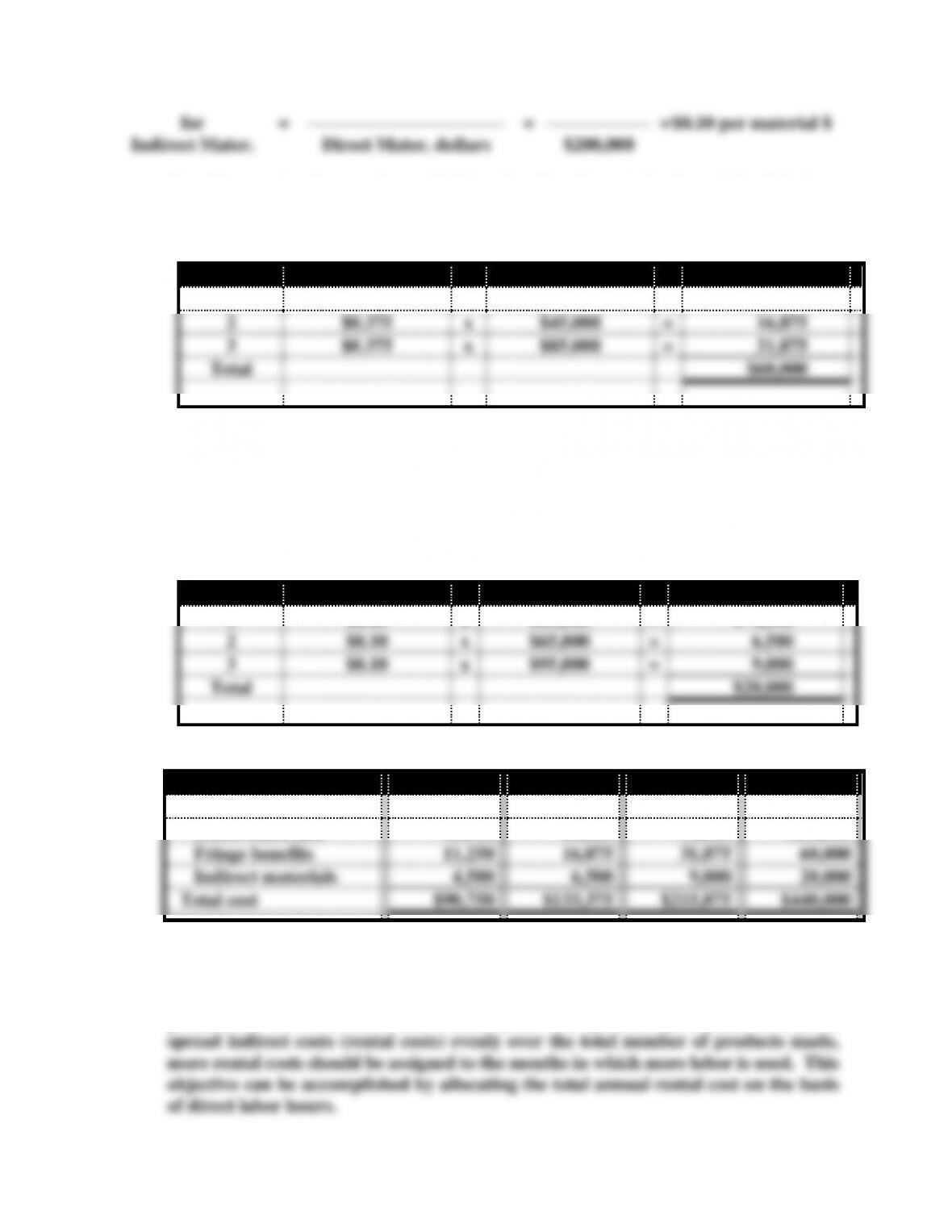

Step 1 is to determine the allocation rates:

Allocation rate

Fringe benefit cost

$60,000

for

=

––––––––––––––––––––

=

–––––––––––

=

$0.375 per labor $

Fringe benefits

Direct labor dollars

$160,000

Allocation rate

Indirect Mater. cost

$20,000

for

=

–––––––––––––––––––––

=

–––––––––––

=

$0.10 per material $

Indirect Mater.

Direct Mater. dollars

$200,000

Step 2 is to assign the costs by multiplying the allocation rate by the weight of the base

(i.e., cost driver) for each month:

Fringe Benefits

House

Allocation Rate

x

Weight of Base

=

Allocated Cost

1

$0.375

x

$30,000

=

$11,250

2

$0.375

x

$45,000

=

16,875

3

$0.375

x

$85,000

=

31,875

Total

$60,000

Exercise 12-8 (continued)

Indirect Materials

House

Allocation Rate

x

Weight of Base

=

Allocated Cost

1

$0.10

x

$45,000

=

$ 4,500

2

$0.10

x

$65,000

=

6,500

3

$0.10

x

$95,000

=

9,000

Total

$20,000

Step 3 sums the cost components to determine the total cost of each house:

Expected Costs

Home 1

Home 2

Home 3

Total

Direct labor

$30,000

$ 45,000

$ 85,000

$160,000

Direct materials

45,000

65,000

90,000

200,000

Fringe benefits

11,250

16,875

31,875

60,000

Indirect materials

4,500

6,500

9,000

20,000

Total cost

$90,750

$133,375

$215,875

$440,000

Exercise 12-9

There is a logical relationship between the amount of labor and the level of

production. The more labor hours worked, the more products produced. In order to

Step 1 is to determine the allocation rate:

Annual rent

$90,000*

Allocation rate

=

––––––––––––––––––––

=

–––––––––––

=

$18 per labor hour

Annual labor hours

5,000

(Cost driver)

*$7,500 x 12 = $90,000

Step 2 is to assign the cost by multiplying the allocation rate by the weight of the base

(cost driver) for each month:

Month

Allocation Rate

x

Weight of Base

=

Allocated Cost

Jan.

$18

x

300

=

$ 5,400

Feb.

18

x

600

=

10,800

Exercise 12-10

A problem exists because the insurance premium is paid only in July. If all of the cost

Step 1 is to determine the allocation rate:

Insurance cost

$96,000

Allocation rate

=

––––––––––––––––––––

=

––––––––––

=

$2.40 per hour

No. of labor hours

40,000

(Cost driver)

Step 2 is to assign the cost by multiplying the allocation rate by the weight of the base

(cost driver) for each month:

Month

Allocation Rate

x

Weight of Base

=

Allocated Cost

January

$2.40

x

3,000

=

$7,200

February

2.40

x

2,000

=

4,800

Exercise 12-11

a. The annual salary of the customer relations representative could be allocated by

computing an allocation rate based on the total number of complaints expected to

occur during the year. A monthly charge could be determined by multiplying the

rate by the weight of the base. The computations for such an allocation are shown

below:

Step 1 is to determine the allocation rate:

$72,000*

Allocation rate

=

=

$2.25 per complaint

Step 2 is to assign the cost by multiplying the allocation rate by the weight of the base

(cost driver) for each month:

Month

Allocation Rate

x

Weight of Base

=

Allocated Cost

January

$2.25

x

1,000

=

$2,250

February

2.25

x

1,300

=

2,925

b. An important question that must be addressed is why one would make such an

allocation. Since you do not charge for processing customer complaints, the

information would not be useful for pricing decisions. Since the representative has

no control over the number of complaints received, the cost per complaint would have