Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

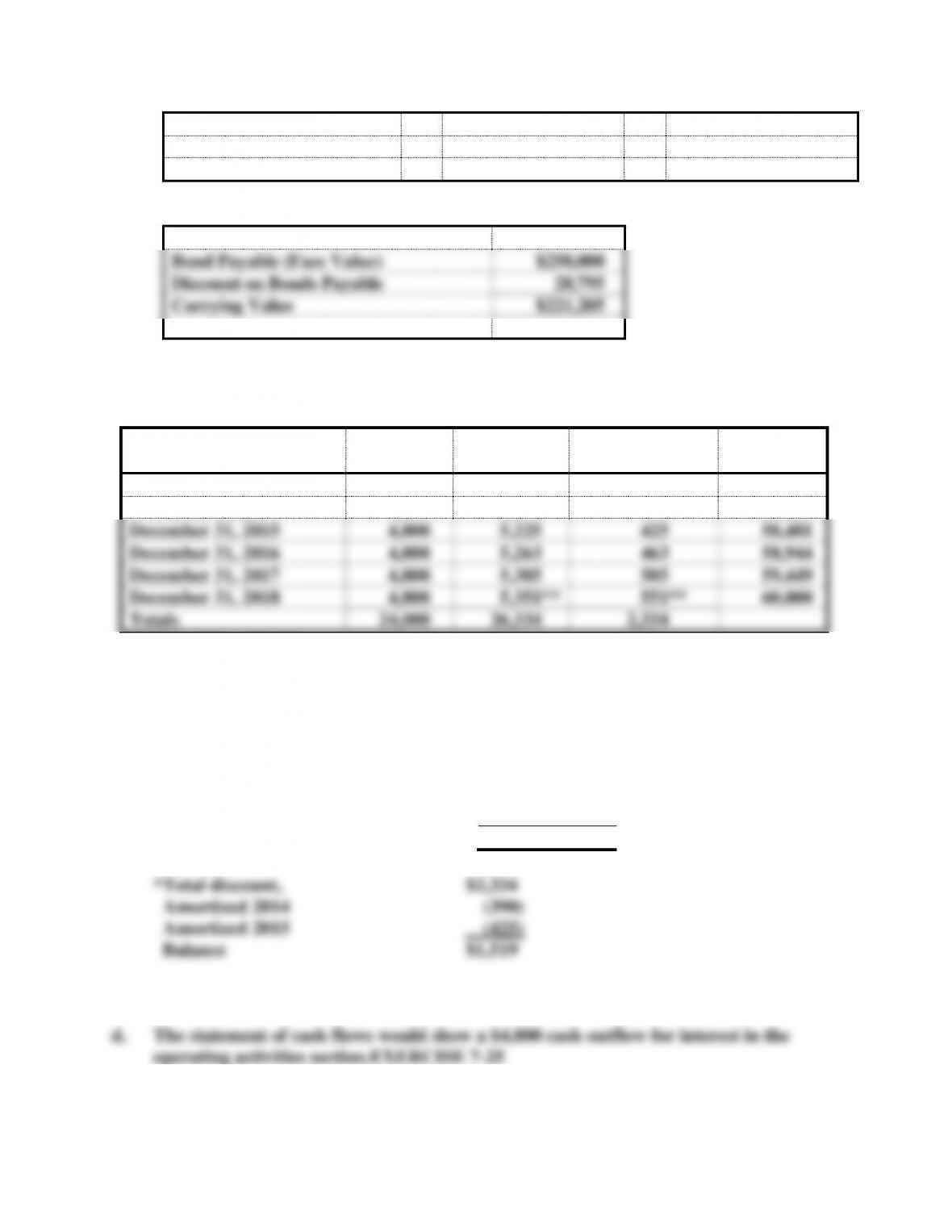

$21,928

−

$20,000

=

$1,928

Beginning Discount

−

Amortization

=

Ending Discount

$30,723

−

$1,928

=

$28,795

Bond Carrying Value as of December 31, 2014

Bond Payable (Face Value)

$250,000

Discount on Bonds Payable

28,795

Carrying Value

$221,205

EXERCISE 7-24

a.

Date

Cash

Payment

Interest

Expense

Discount

Amortization

Carrying

Value

January 1, 2014

57,666

December 31, 2014

4,800

5,190*

390

58,056

December 31, 2015

4,800

5,225

425

58,481

December 31, 2016

4,800

5,263

463

58,944

December 31, 2017

4,800

5,305

505

59,449

December 31, 2018

4,800

5,351**

551**

60,000

Totals

24,000

26,334

2,334

*$57,666 x 9% = $5,190 rounded

**adjusted the final year for rounding

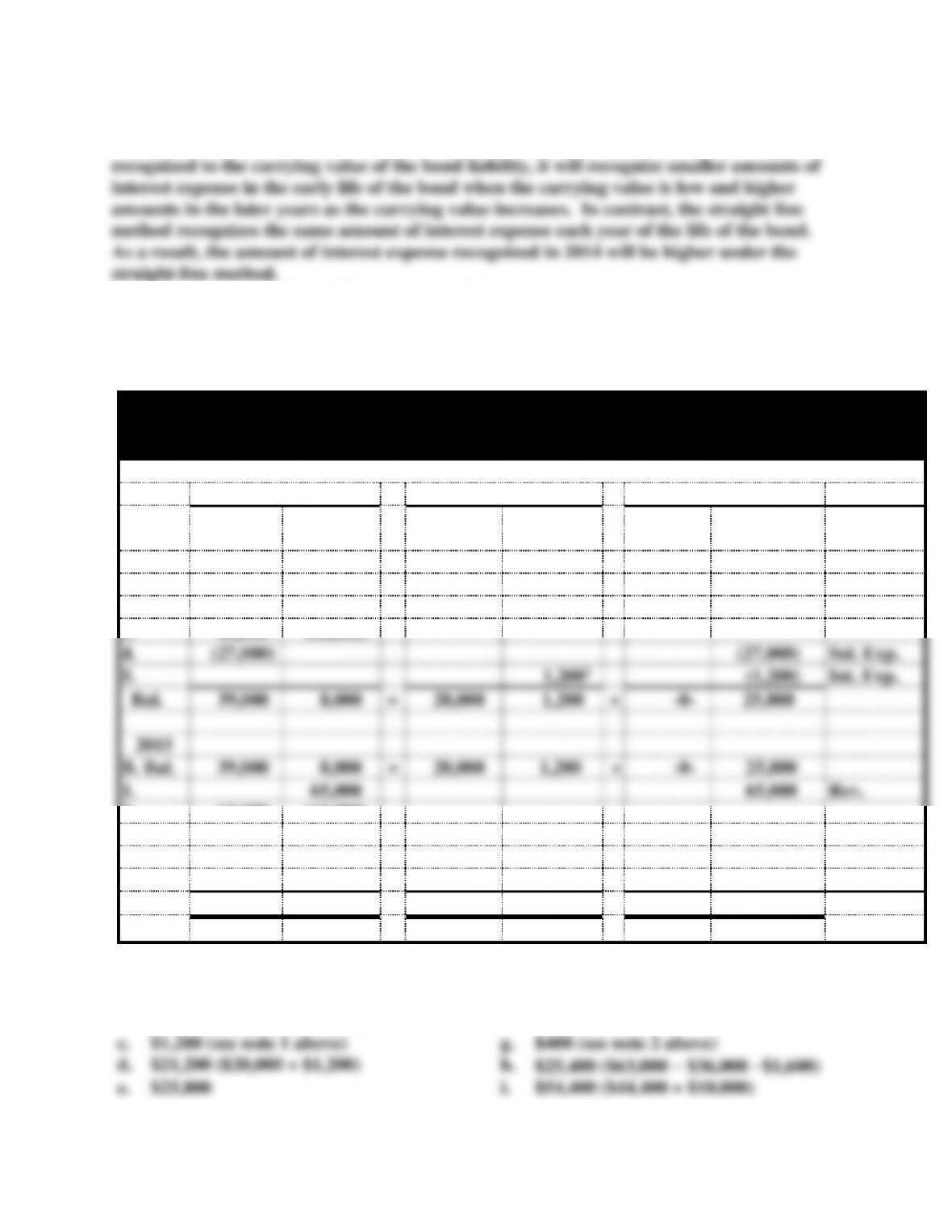

b. The balance sheet would show the carrying value of the bond liability. The carrying

value could be shown net of the discount, $58,481. Alternatively, the face value less

the discount could be shown as follows:

Bond liability

$60,000

Less: Bond discount

1,519*

Carrying value

$58,481

c. The income statement would show $5,225 of interest expense.

Since the stated rate of interest is lower than the effective interest rate the bonds will sell at

a discount. Because the effective interest rate method ties the amount of interest expense

SOLUTIONS TO PROBLEMS – CHAPTER 7

PROBLEM 7-26

a.

Powell Co.

Effect of Events on the General Ledger

2014 and 2015

Assets

=

Liabilities

+

Stockholders’ Equity

Event

Cash

Accts.

Rec.

=

Notes

Pay.

Int.

Pay.

+

Com.

Stock

Retained

Earnings

Acct.

Title/RE

2014

1.

20,000

20,000

2.

54,000

54,000

Rev.

3.

46,000

(46,000)

4.

(27,000)

(27,000)

Sal. Exp.

5.

1,2001

(1,200)

Int. Exp.

Bal.

39,000

8,000

=

20,000

1,200

+

-0-

25,800

2015

B. Bal.

39,000

8,000

=

20,000

1,200

+

-0-

25,800

1.

65,000

65,000

Rev.

2.

63,000

(63,000)

3.

(36,000)

(36,000)

Sal. Exp.

4.

4002

(400)

Int. Exp.

5.

(21,600)

(20,000)

(1,600)

Bal.

44,400

10,000

=

-0-

-0-

+

-0-

54,400

1$20,000 x 8% x 9/12 = $1,200

2$20,000 x 8% x 3/12 = $400

b.

$19,000 ($46,000− $27,000)

f.

$20,000 (loan)

c.

$1,200 (see note 1 above)

g.

$400 (see note 2 above)

d.

$21,200 ($20,000 + $1,200)

h.

$25,400 ($63,000 − $36,000 −$1,600)

e.

$25,800

i.

$54,400 ($44,400 + $10,000)

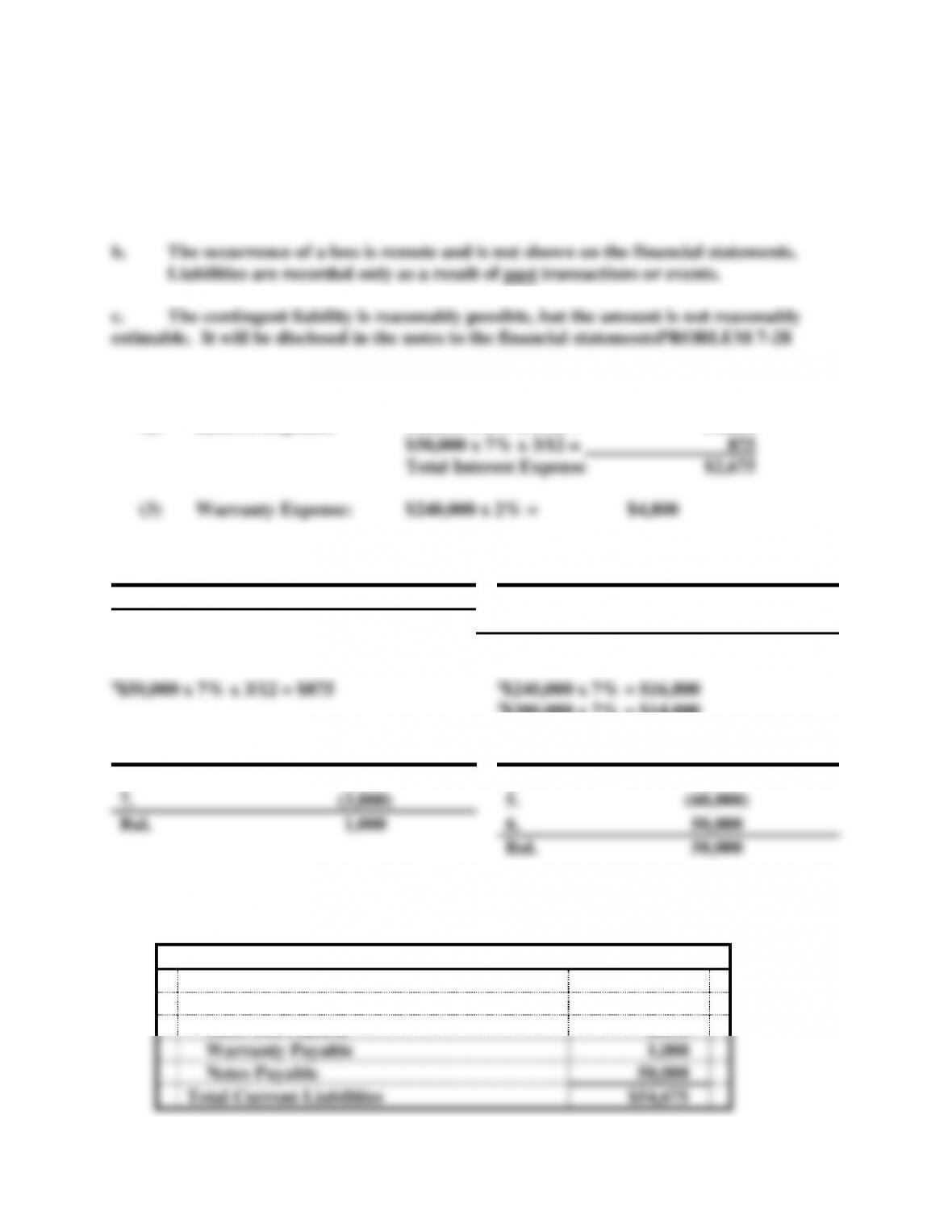

Problem 7-27

a. This contingent liability would be recorded on the books and reported on the

financial statements inclusive of note disclosure.

a. (1) Cash paid for interest: $60,000 x 6% x 6/12 = $1,800

(2) Interest Expense: $60,000 x 6% x 6/12 = $1,800

b.

Interest Payable

Sales Tax Payable

6.1 875

2.2 16,800

Bal. 875

4.3 (14,000)

Bal. 2,800

3$200,000 x 7% = $14,000

Warranties Payable

Notes Payable

3.4 4,800

1. 60,000

7. (3,800)

5. (60,000)

Bal. 1,000

6. 50,000

Bal. 50,000

4$240,000 x 2% = $4,800

Aliceville Company

Current Liabilities

Interest Payable

$ 875

Sales Tax Payable

2,800

Warranty Payable

1,000

Notes Payable

50,000

Total Current Liabilities

$54,675

Note: The contingent liability is not recorded since the attorney believes the lawsuit is

without merit (assumes remote likelihood of loss).

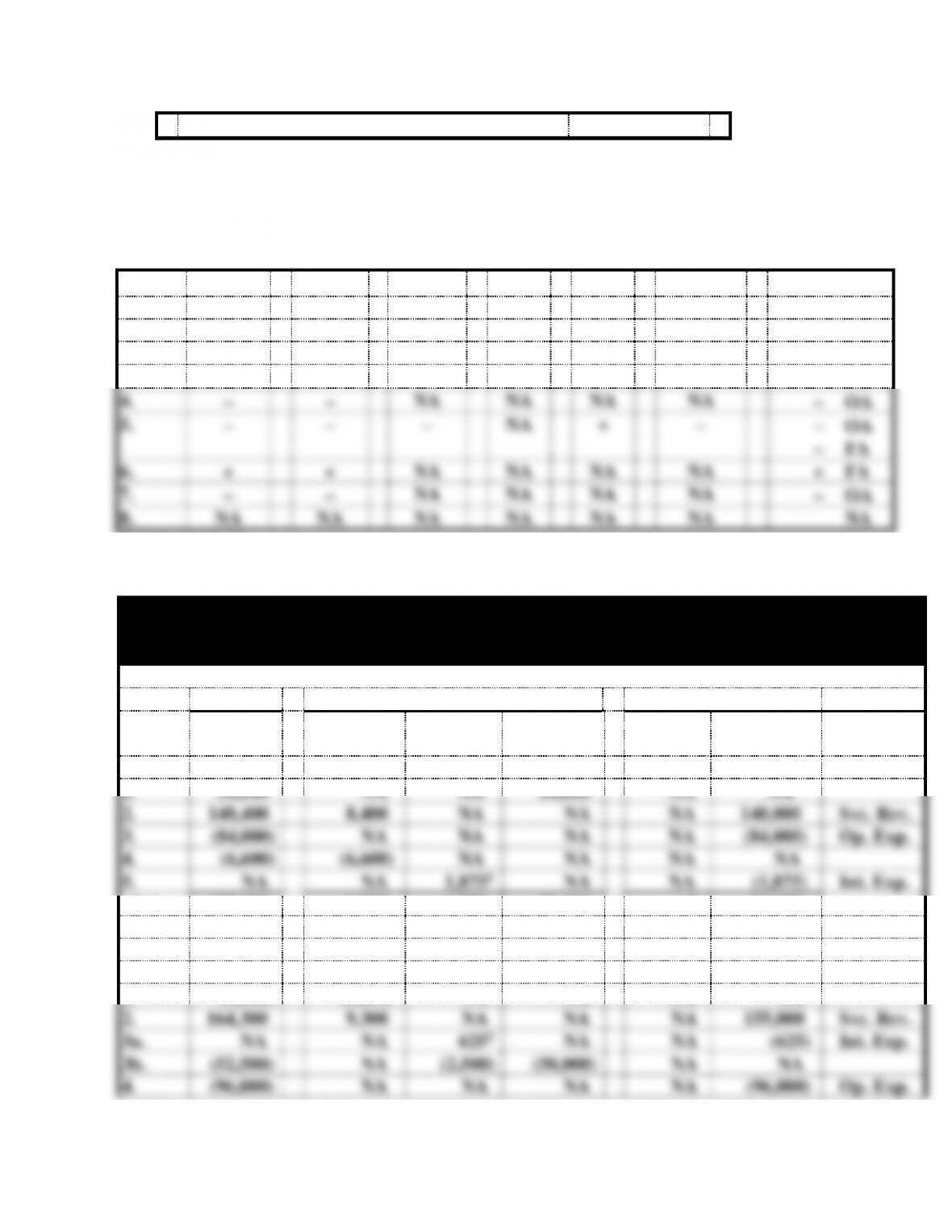

PROBLEM 7-28 (cont.)

c.

Event

Assets

=

Liab.

+

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

1.

+

+

NA

NA

NA

NA

+ FA

2.

+

+

+

+

NA

+

+ OA

3.

NA

+

−

NA

+

−

NA

4.

−

−

NA

NA

NA

NA

− OA

5.

−

−

−

NA

+

−

− OA

− FA

6.

+

+

NA

NA

NA

NA

+ FA

7.

−

−

NA

NA

NA

NA

− OA

8.

NA

NA

NA

NA

NA

NA

NA

PROBLEM 7-29

a.

Ocktoc Co.

Effect of Events on the General Ledger

2014 and 2015

Assets

=

Liabilities

+

Stockholders’ Equity

Event

Cash

=

Sales Tax

Pay.

Int.

Pay.

Notes Pay.

+

Com.

Stock

Retained

Earnings

Acct.

Title/RE

2014

1.

50,000

NA

NA

50,000

NA

NA

2.

148,400

8,400

NA

NA

NA

140,000

Svc. Rev.

3.

(84,000)

NA

NA

NA

NA

(84,000)

Op. Exp.

4.

(6,600)

(6,600)

NA

NA

NA

NA

5.

NA

NA

1,8751

NA

NA

(1,875)

Int. Exp.

Bal.

107,800

=

1,800

1,875

50,000

-0-

54,125

2015

B. Bal.

107,800

=

1,800

1,875

50,000

-0-

54,125

1.

(1,800)

(1,800)

NA

NA

NA

NA

2.

164,300

9,300

NA

NA

NA

155,000

Svc. Rev.

3a.

NA

NA

6252

NA

NA

(625)

Int. Exp.

3b.

(52,500)

NA

(2,500)

(50,000)

NA

NA

4.

(96,000)

NA

NA

NA

NA

(96,000)

Op. Exp.

5.

(8,100)

(8,100)

NA

NA

NA

NA

Bal.

113,700

=

1,200

-0-

-0-

-0-

112,500

1$50,000 x 5% x 9/12 = $1,875

2$50,000 x 5% x 3/12 = $625

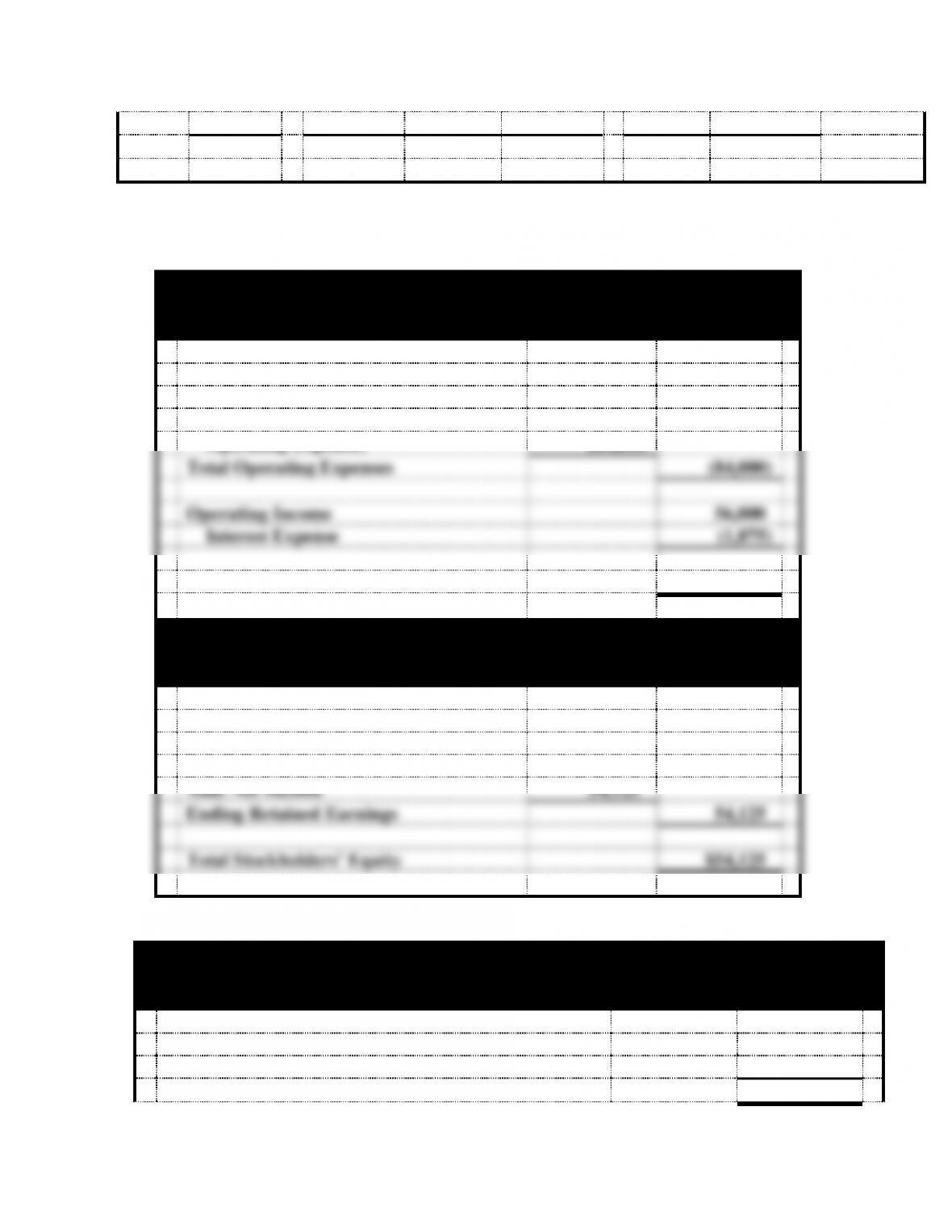

PROBLEM 7-29 (cont.)

b.

Ocktoc Co.

Income Statement

For the Year Ended December 31, 2014

Service Revenue

$140,000

Expenses

Operating Expenses

$84,000

Total Operating Expenses

(84,000)

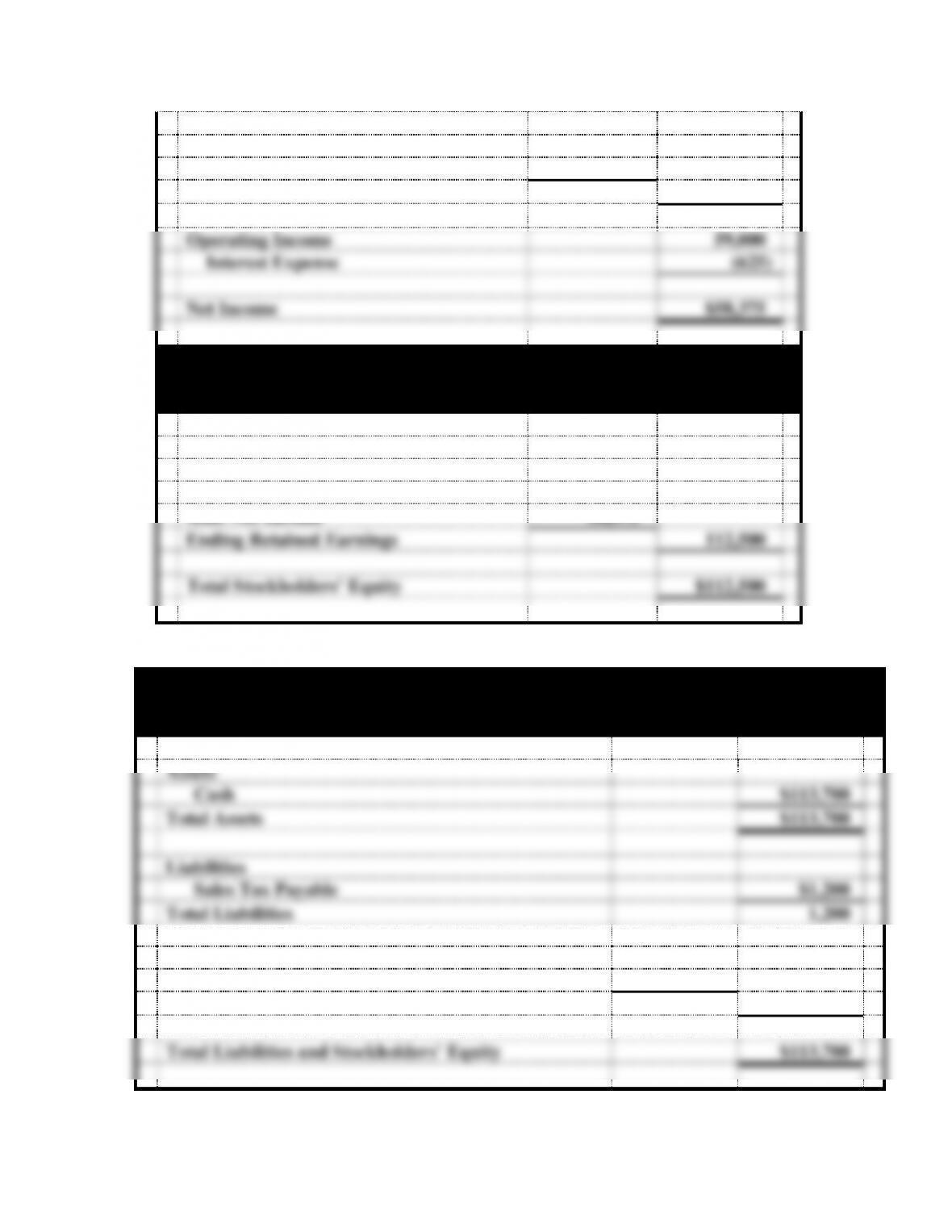

Operating Income

56,000

Interest Expense

(1,875)

Net Income

$54,125

Ocktoc Co.

Statement of Changes of Stockholders’ Equity

For the Year Ended December 31, 2014

Common Stock

$ -0-

Beginning Retained Earnings

$ -0-

Add: Net Income

54,125

Ending Retained Earnings

54,125

Total Stockholders’ Equity

$54,125

PROBLEM 7-29 b. (cont.)

Ocktoc Co.

Balance Sheet

As of December 31, 2014

Assets

Cash

$107,800

Total Assets

$107,800

Liabilities

Sales Tax Payable

$ 1,800

Interest Payable

1,875

Notes Payable

50,000

Total Liabilities

53,675

Stockholders’ Equity

Retained Earnings

$54,125

Total Stockholders’ Equity

54,125

Total Liabilities and Stockholders’ Equity

$107,800

Ocktoc Co.

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash Flows From Operating Activities:

Inflow from Customers

$140,000

Inflow from Sales Tax

8,400

Outflow for Expenses

(84,000)

Outflow for Sales Tax

(6,600)

Net Cash Flow from Operating Activities

$ 57,800

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Inflow from Loan

$ 50,000

Net Cash Flow from Financing Activities

50,000

Net Change in Cash

107,800

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$107,800

PROBLEM 7-29 (cont.)

f.

Ocktoc Co.

Income Statement

For the Year Ended December 31, 2015

Service Revenue

$155,000

Expenses

Operating Expenses

$96,000

Total Operating Expenses

(96,000)

Operating Income

59,000

Interest Expense

(625)

Net Income

$58,375

Ocktoc Co.

Statement of Changes of Stockholders’ Equity

For the Year Ended December 31, 2015

Common Stock

$ -0-

Beginning Retained Earnings

$54,125

Add: Net Income

58,375

Ending Retained Earnings

112,500

Total Stockholders’ Equity

$112,500

PROBLEM 7-29 f. (cont.)

Ocktoc Co.

Balance Sheet

As of December 31, 2015

Assets

Cash

$113,700

Total Assets

$113,700

Liabilities

Sales Tax Payable

$1,200

Total Liabilities

1,200

Stockholders’ Equity

Retained Earnings

$112,500

Total Stockholders’ Equity

112,500

Total Liabilities and Stockholders’ Equity

$113,700

Ocktoc Co.

Statement of Cash Flows

For the Year Ended December 31, 2015

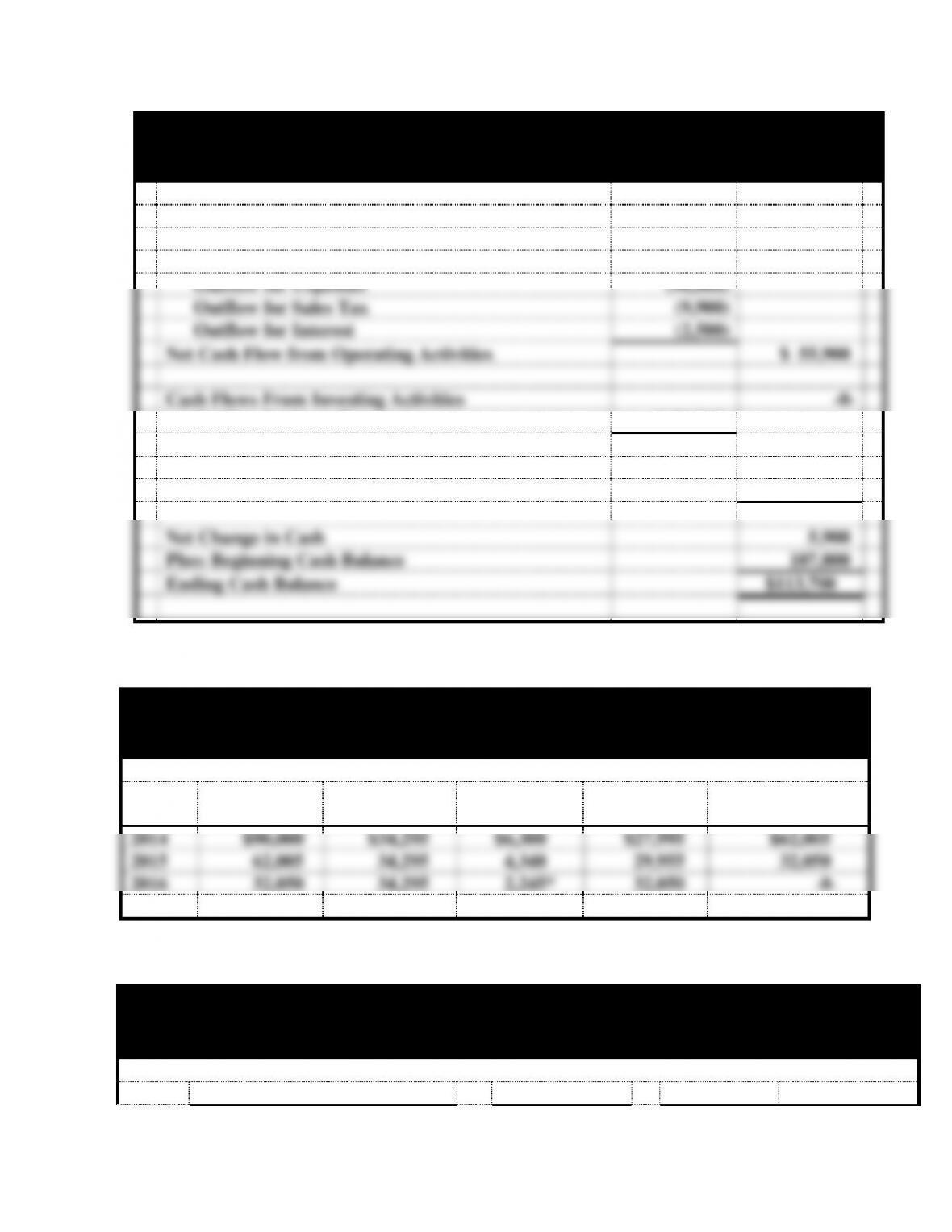

Cash Flows From Operating Activities:

Inflow from Customers

$155,000

Inflow from Sales Tax

9,300

Outflow for Expenses

(96,000)

Outflow for Sales Tax

(9,900)

Outflow for Interest

(2,500)

Net Cash Flow from Operating Activities

$ 55,900

Cash Flows From Investing Activities

-0-

Outflow for Loan Payment

$(50,000)

Net Cash Flow from Investing Activities

(50,000)

Cash Flows From Financing Activities

-0-

Net Change in Cash

5,900

Plus: Beginning Cash Balance

107,800

Ending Cash Balance

$113,700

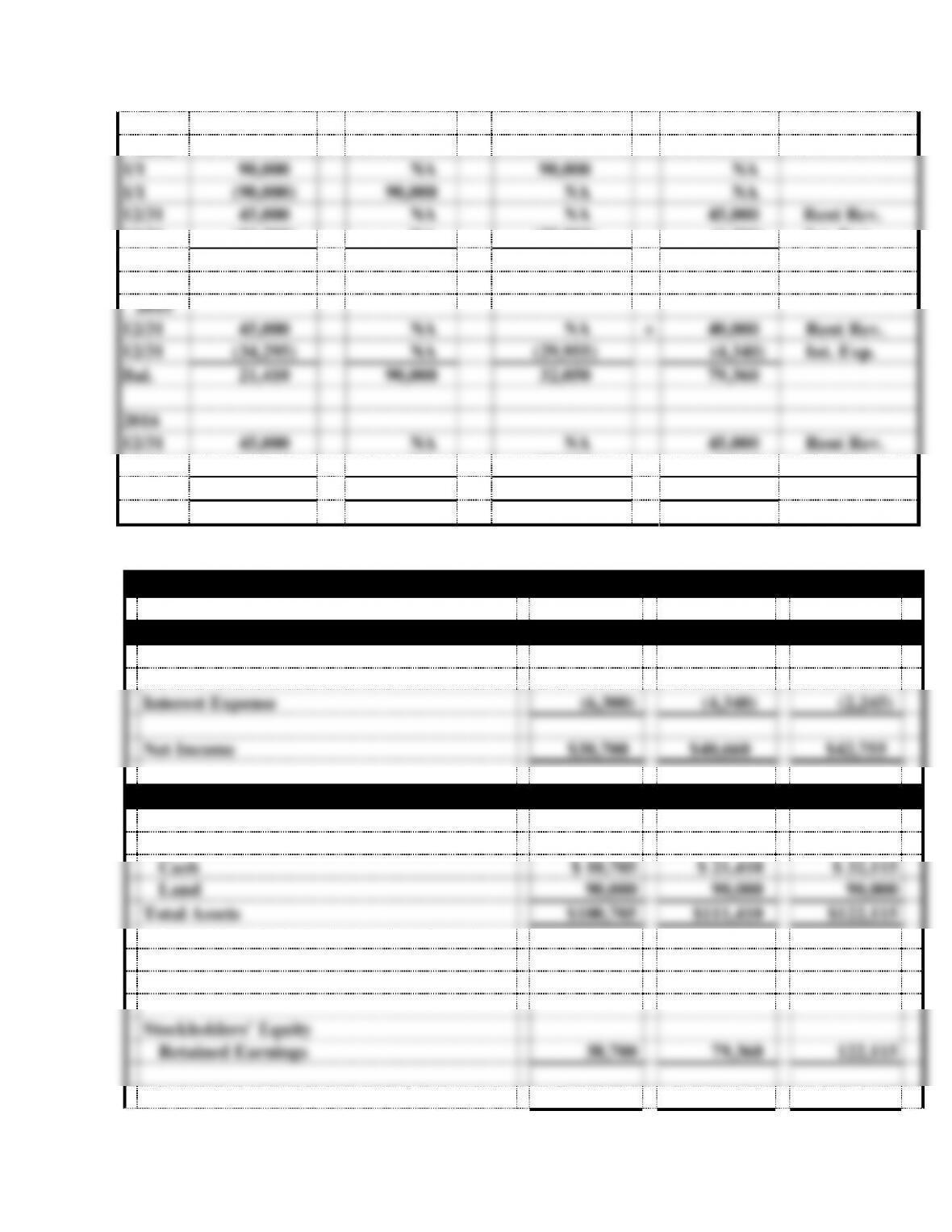

PROBLEM 7-30

a.

Mixon Co.

Amortization Schedule

$90,000, 3-Yr. Term Note, 7% Interest Rate

Year

Prin. Bal. on

Jan 1

Cash Pay.

Dec. 31

Applied to

Interest

Applied to

Principal

Prin. Bal.

End of Period

2014

$90,000

$34,295

$6,300

$27,995

$62,005

2015

62,005

34,295

4,340

29,955

32,050

2016

32,050

34,295

2,245*

32,050

-0-

*rounded for final year

b.

Mixon Co.

Effect of Events on the General Ledger

2014, 2015 and 2016

Assets

=

Liabilities

+

Stk. Equity

Event

Cash

+

Land

=

Note Pay.

+

Ret. Earn.

Acct. Title/RE

2014

1/1

90,000

NA

90,000

NA

1/1

(90,000)

90,000

NA

NA

12/31

45,000

NA

NA

45,000

Rent Rev.

12/31

(34,295)

NA

(27,995)

(6,300)

Int. Exp.

Bal.

10,705

90,000

62,005

+

38,700

2015

12/31

45,000

NA

NA

+

40,000

Rent Rev.

12/31

(34,295)

NA

(29,955)

(4,340)

Int. Exp.

Bal.

21,410

90,000

32,050

79,360

2016

12/31

45,000

NA

NA

45,000

Rent Rev.

12/31

(34,295)

NA

(32,050)

(2,245)

Int. Exp.

Bal.

32,115

90,000

-0-

+

122,115

PROBLEM 7-30 b. (cont.)

Mixon Co.

Financial Statements

2014

2015

2016

Income Statements for the Year Ended December 31

Lease Revenue

$45,000

$45,000

$45,000

Interest Expense

(6,300)

(4,340)

(2,245)

Net Income

$38,700

$40,660

$42,755

Balance Sheets as of December 31

Assets

Cash

$ 10,705

$ 21,410

$ 32,115

Land

90,000

90,000

90,000

Total Assets

$100,705

$111,410

$122,115

Liabilities

Notes Payable

$ 62,005

$ 32,050

$ -0-

Stockholders’ Equity

Retained Earnings

38,700

79,360

122,115

Total Liab. and Stockholders’ Equity

$100,705

$111,410

$122,115

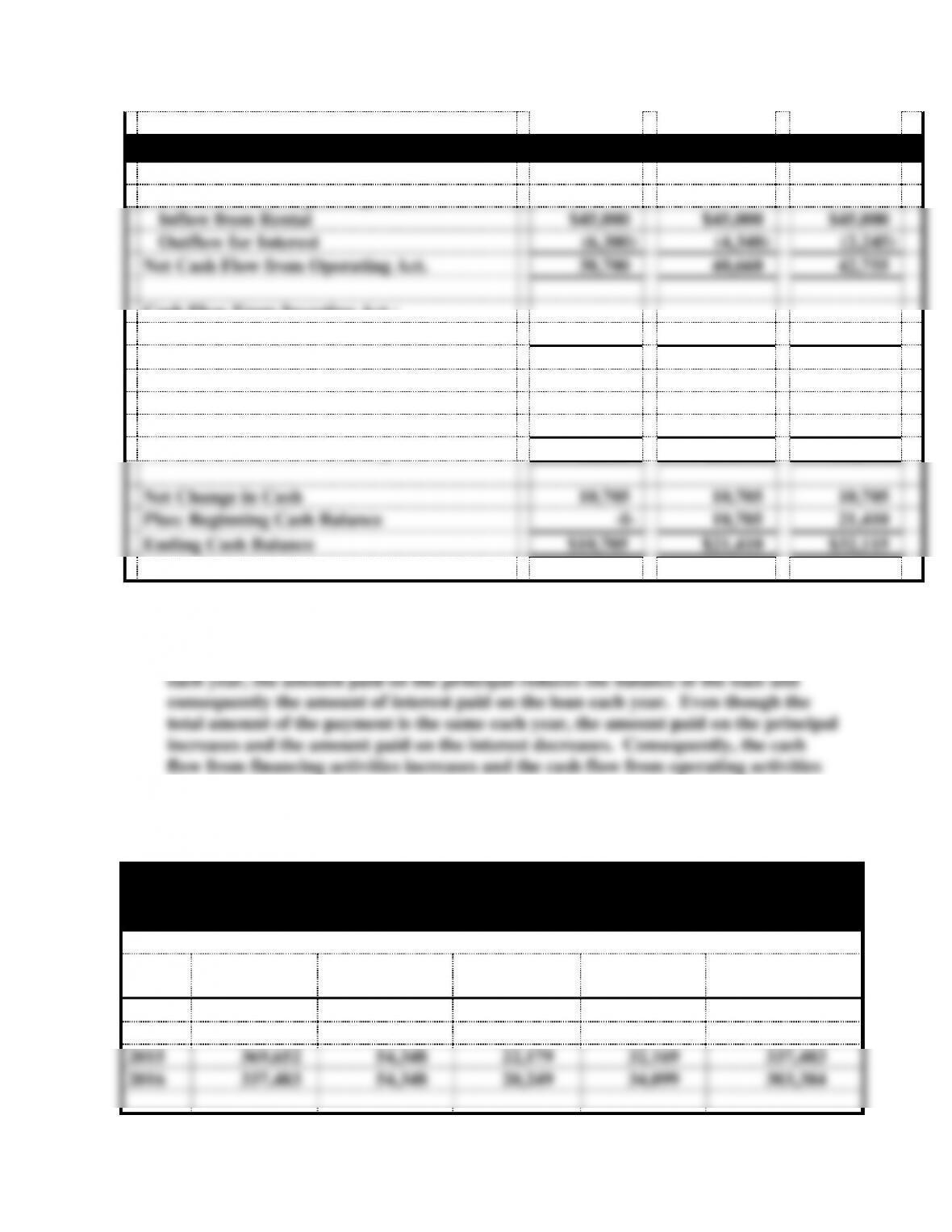

Statements of Cash Flows for the Year Ended December 31

Cash Flows From Operating Act.:

Inflow from Rental

$45,000

$45,000

$45,000

Outflow for Interest

(6,300)

(4,340)

(2,245)

Net Cash Flow from Operating Act.

38,700

40,660

42,755

Cash Flow From Investing Act.:

Outflow to Purchase Land

(90,000)

-0-

-0-

Cash Flow From Financing Act.:

Inflow from Loan

90,000

-0-

-0-

Outflow to Repay Loan

(27,995)

(29,955)

(32,050)

Net Cash Flow from Financing Act.

62,005

(29,955)

(32,050)

Net Change in Cash

10,705

10,705

10,705

Plus: Beginning Cash Balance

-0-

10,705

21,410

Ending Cash Balance

$10,705

$21,410

$32,115

PROBLEM 7-30 (cont.)

c. Because the company is making both principal and interest payments on the loan

decreases.

PROBLEM 7-31

Provided for the use of the instructor:

Stegal Company

Amortization Schedule

$400,000, 10-Yr. Term Note, 6% Interest Rate

Year

Prin. Bal. on

Jan 1

Cash Pay. Dec.

31

Applied to

Interest

Applied to

Principal

Prin. Bal.

End of Period

2014

$400,000

$54,348

$24,000

$30,348

$369,652

2015

369,652

54,348

22,179

32,169

337,483

2016

337,483

54,348

20,249

34,099

303,384

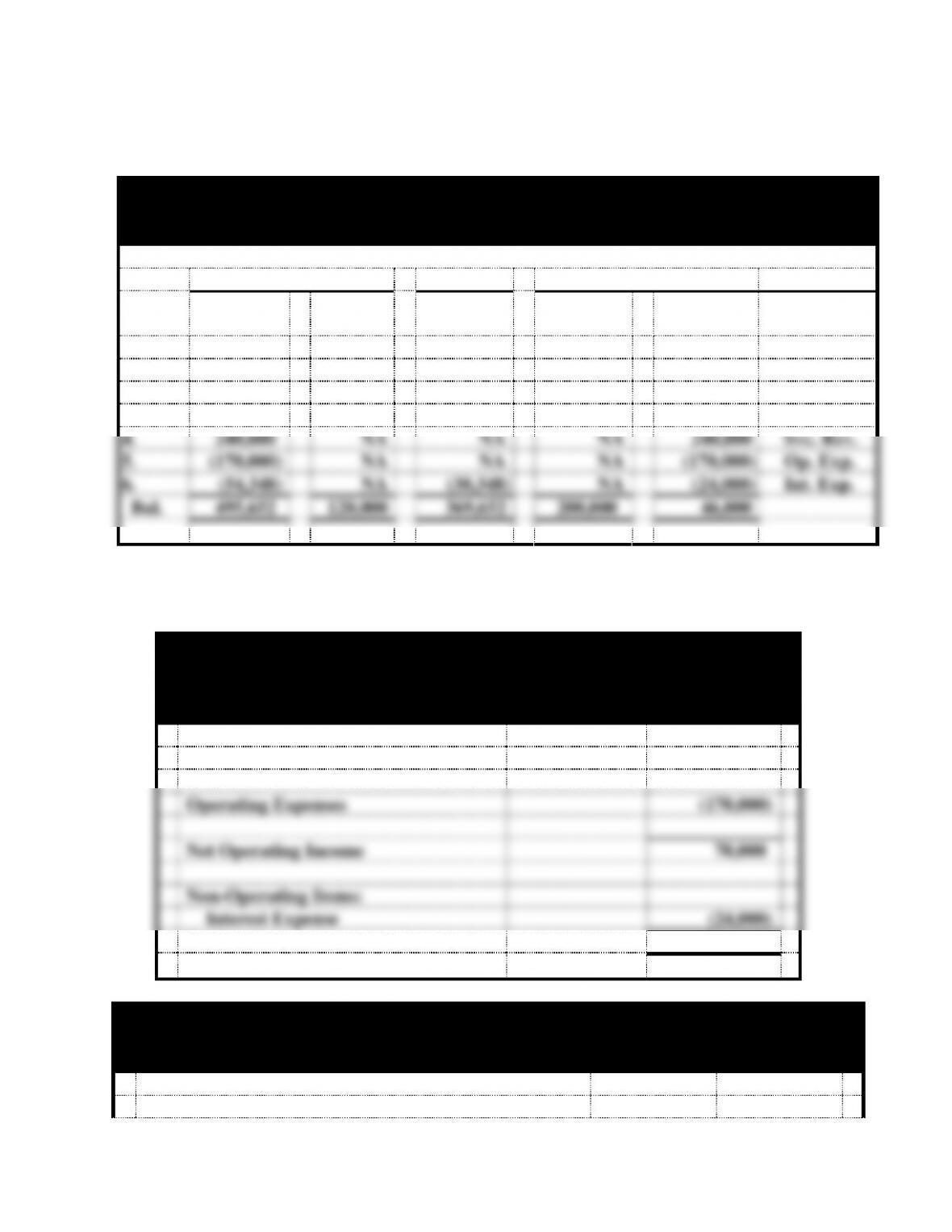

a.

Stegal Company

Effect of Events on the General Ledger

2014

Assets

=

Liabilities

+

Stk. Equity

Event

Cash

+

Land

=

Note Pay.

+

Comm.

Stock

+

Ret. Earn.

Acct.

Title/RE

2014

1.

200,000

NA

NA

200,000

NA

2.

400,000

NA

400,000

NA

NA

3.

(120,000)

120,000

NA

NA

NA

4.

240,000

NA

NA

NA

240,000

Svc. Rev.

5.

(170,000)

NA

NA

NA

(170,000)

Op. Exp.

6.

(54,348)

NA

(30,348)

NA

(24,000)

Int. Exp.

Bal.

495,652

120,000

369,652

200,000

46,000

PROBLEM 7-31 (cont.)

b.

Stegal Company

Income Statement

For the Year Ended December 31, 2014

Service Revenue

$240,000

Operating Expenses

(170,000)

Net Operating Income

70,000

Non-Operating Items:

Interest Expense

(24,000)

Net Income

$46,000

Stegal Company

Balance Sheet

As of December 31, 2014

Assets