A business’s temporary accounts include revenues, expenses, and retained earnings.

A company may recognize a revenue or expense without a corresponding cash

collection or payment in the same accounting period.

Indicate whether each of the following statements about financial statement analysis is

true or false.

1> The asset turnover ratio is calculated by dividing net income by average total assets.

2> The asset turnover ratio is likely to be high in an industry in which operations

require only a minimal investment in assets.

3> Return on equity measures the wealth generated by the amount of assets invested in

a business.

4> A higher value for the return on investment ratio would generally indicate more

effective company management.

5> The use of financial leverage often causes a business’s return on equity to be lower

than its return on investment.

Indicate whether each of the following statements about financial statement analysis is

true or false.

1> The reason behind a financial statement ratio or percentage analysis result is usually

self evident and does not require further study or analysis.

2> In horizontal percentage analysis, an item from the financial statements is expressed

as a percentage of the same item from a previous year’s financial statements.

3> Horizontal analysis for several years can be done by choosing one year as a base

year and calculating increases or decreases in relation to that year.

4> One form of horizontal analysis is the preparation of common size financial

statements.

5> Vertical analysis compares two or more financial statement items within the same

time period.

When a capital investment is expected to provide unequal annual cash inflows, the

payback period cannot be calculated.

Financial accounting information is usually more detailed than managerial accounting

information.

Cash paid to production workers should be recorded as Wages Expense in the income

statement for the period incurred.

Indicate whether each of the following statements about financial statement analysis is

true or false.

1> Both dividends and earnings performance are indicators of the value of a company’s

stock.

2> The most widely quoted measure of a company’s earnings performance is return on

equity.

3> Earnings per share is calculated for a company’s common stock.

4> Investors need to understand that the value of a company’s earnings per share is

affected by its choices of accounting principles and assumptions.

5> The book value per share measures the market value of a corporation’s stock.

Depreciation on a capital investment (such as equipment) has the effect of decreasing

the amount of income taxes that the company owning the asset must pay.

A manufacturing business paid $3,000 to purchase inventory. As a result, assets would

increase by $3,000.

Cash inflows from a capital investment may include the terminal value of capital assets

and increases in revenues.

The value created by a business may be called income or earnings.

Misclassifying a period cost as a product cost will usually correct itself in the following

period.

Benton Corporation acquired real estate that contained land, building and equipment.

The property cost Benton $825,000. Benton paid $175,000 in cash and issued a Note

Payable for the remainder of the cost. An appraisal of the property reported the

following values: Land, $85,000; Building, $625,000; and Equipment, $250,000.

Assume that Benton uses the units-of-production method when depreciating its

equipment. Benton estimates that the purchased equipment will produce 1,200,000 units

over its 5 years useful life and has salvage value of $7,500. Benton produced 265,000

units with the equipment by the end of the first year of purchase. The equipment costs

214,841.89. What amount will Benton record for depreciation expense on the

equipment in the first year?

A.$8,408

B.$41,469

C.$45,788

D.$82,938

Which of the following are issued by the SEC, as needed, to supplement Regulation

S-X and Regulation S-K?

A.SABs.

B.ASRs.

C.FRRs.

D.ARBs.

E.SRBs.

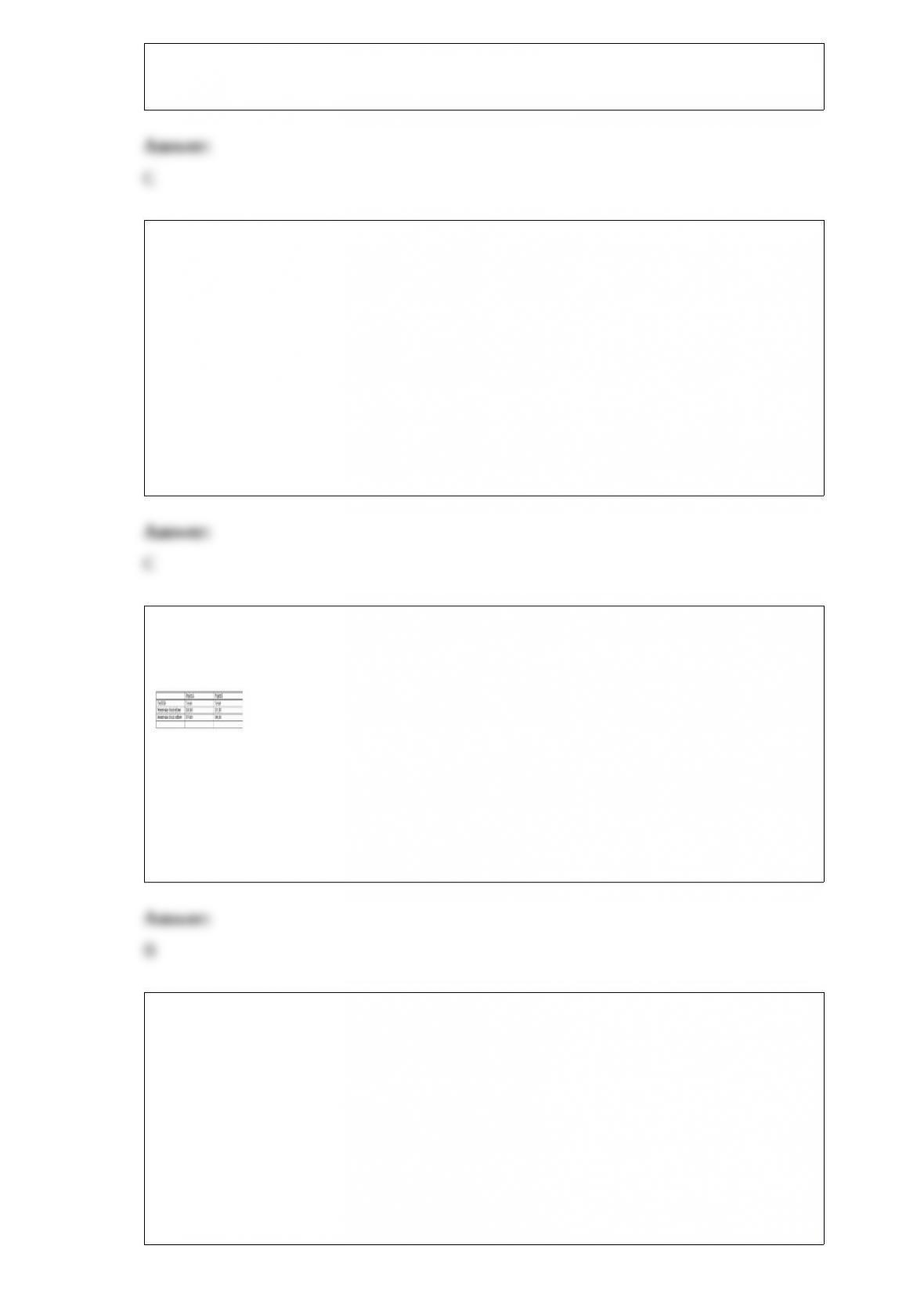

Findell Corporation is considering two projects, A and B, and it has gathered the

following estimates for the projects:

What is the net present value for project B?

A.$7,360

B.$6,100

C.$1,260

D.None of these answers is correct.

On a statement of financial affairs, a company’s liabilities should be valued at

A.the present value of future cash flows.

B.net realizable value.

C.the amount required for settlement.

D.replacement cost.

E.the amount expected to be paid if the company could honor its debts.

Select the incorrect statement regarding ratio analysis.

A.Ratio analysis is a specific form of horizontal analysis.

B.There are many different ratios available for evaluating a firm’s performance.

C.Some ratios involve an account from the balance sheet and one from the income

statement.

D.Ratio analysis involves making comparisons between different accounts in the same

set of financial statements.

What is the primary focus of the Sarbanes-Oxley Act?

A.Accounting standards and the registration of securities.

B.Regulation of the continuous reporting by publicly owned companies.

C.Accounting standards and registration of investment companies that engage in

investing and trading in securities.

D.Accounting standards and penalties against persons who profit from illegal use of

inside information.

E.Regulation of independent audit firms and audit standards.

Which of the following is not a responsibility of the bankruptcy trustee?

A.Recover all property belonging to the insolvent company.

B.Liquidate common stock of the company.

C.Preserve the estate from any further deterioration.

D.Make distributions to the proper claimants.

E.Void preferences made by the debtor within 90 days prior to the filing of the

bankruptcy petition if the company was already insolvent.

Indicate whether each of the following statements is true or false.

_____ a) Margin is calculated by dividing operating income by net income.

_____ b) Turnover is a measure of the profits generated from sales.

_____ c) Return on investment can be improved by increasing sales, decreasing

expenses, or increasing the asset base.

_____ d) An increase in sales may cause a company’s return on investment to increase

because of the effects of fixed costs.

_____ e) Return on investment combines many aspects of managerial performance into

a single ratio.

Sparkman Co. filed a bankruptcy petition and liquidated its noncash assets. Sparkman

was paying forty cents on the dollar for unsecured claims. Bailey Co. held a mortgage

of $150,000 on land that was sold for $110,000. The total amount of payment that

Bailey should have received is calculated to be

A.$110,000.

B.$44,000.

C.$126,000.

D.$150,000.

E.$60,000.

Adkins Company experienced an accounting event that affected its financial statements

as indicated below:

Which of the following accounting events could have caused these effects on ABC’s

statements?

A.Issued common stock.

B.Earned cash revenue.

C.Earned revenue on account.

D.Collected cash from accounts receivable.

EDGAR stands for:

A.Electronic Debits, Gains, Assets and Revenues System.

B.Electronic Data Gathering, Analysis, and Retrieval System.

C.Explanatory Data Gathering, Analysis, and Retrieval System.

D.Explanatory Debits, Gains, Assets and Revenues System.

E.Electronic Data, Gross Analysis, and Revenues System.

A partnership began its first year of operations with the following capital balances:

Young, Capital: $143,000

Eaton, Capital: $104,000

Thurman, Capital: $143,000

The Articles of Partnership stipulated that profits and losses be assigned in the

following manner:

Young was to be awarded an annual salary of $26,000 with $13,000 salary assigned to

Thurman.

Each partner was to be attributed with interest equal to 10% of the capital balance as of

the first day of the year.

The remainder was to be assigned on a 5:2:3 basis to Young, Eaton, and Thurman,

respectively.

Each partner withdrew $13,000 per year.

Assume that the net loss for the first year of operations was $26,000 with net income of

$52,000 in the second year.

What was the balance in Young’s Capital account at the end of the second year?

A.$133,380.

B.$84,760.

C.$105,690.

D.$132,860.

E.$71,760.

What is private placement of securities?

A.A procedure that allows a company to register securities and then sell them over a

period of two years without reregistering.

B.A procedure that allows the sale of securities to a small group of sophisticated

knowledgeable investors, without any general solicitation.

C.A method of filing Form 10-K with the SEC.

D.the registration of mutual funds that engage in investing and trading securities.

E.A sale of securities to 35 or fewer accredited investors.

Which of the following is not an IFRS pronouncement originally issued by the IASB?

A.Business Combinations.

B.First-Time Adoption of IFRS.

C.Financial Instruments: Disclosures.

D.Agriculture.

E.Operating Segments.

Regulation S-X specifies:

A.requirements for the nonfinancial information to be filed with the SEC.

B.which form a company must file to register new securities.

C.that the financial statements included in a company’s annual report must be audited.

D.the form and content of financial statements to be filed with the SEC.

E.the internal controls a publicly traded company must maintain.

Which of the following is not a characteristic of a partnership?

A.The partnership itself pays no income taxes.

B.It is easy to form a partnership.

C.Any partner can be held personally liable for all debts of the business.

D.A partnership requires written Articles of Partnership.

E.Each partner has the power to obligate the partnership for liabilities.

Which of the following statements is correct regarding the admission of a new partner?

A.A new partner must purchase a partnership interest directly from the business.

B.The right of co-ownership in the business property can be transferred to a new partner

without the consent of other existing partners.

C.The right to participate in management of the business cannot be conveyed without

the consent of other existing partners.

D.The right to share in profits and losses can be sold to a new partner without the

consent of other existing partners.

E.A new partner always pays book value.

Canton Company was formed in 2013 and experienced the following accounting events

during the year:

1) issued common stock for $10,000 cash

2) earned cash revenue of $15,000

3) paid cash expenses of $13,000.

These were the only events that affected the company during the year.

Required:

a) Write the accounting equation and record the effects of each accounting event under

the appropriate general ledger account heading.

b) Prepare an income statement for 2013 and a balance sheet as of December 31, 2013.

Identify the false statement regarding how product costs in a manufacturing company

differ from product costs in a service or merchandising company.

A.Both manufacturing companies and service companies incur costs for supplies.

B.Manufacturing companies accumulate product costs in inventory accounts, while

service companies do not.

C.Products of service companies such as restaurants are consumed immediately.

D.Most labor costs for merchandising companies are treated as product costs.

Classify each of the following events as an asset source (AS), asset use (AU), asset

exchange (AX), or not applicable (NA).

_______ 1) Borrowed cash from the bank.

_______ 2) Issued stock for cash.

_______ 3) Invested cash in the common stock of another company.

_______ 4) Paid cash for operating expense.

_______ 5) Performed services and collected cash.

_______ 6) Purchased equipment for cash.

_______ 7) Repaid the bank loan with cash.

_______ 8) Dividends paid to the stockholders.

The following events apply to Bowen’s Cleaning Service for 2013.

1) Issued stock for $14,000 cash.

2) On May 1, paid $9,000 for one year’s rent in advance.

3) Purchased on account $2,500 of supplies to be used in the business.

4) Performed services of $18,400 and received cash.

5) At December 31, an inventory of supplies showed that $360 of supplies were still

unused.

6) At December 31, adjusted the records for the expired rent.

Required:

Draw an accounting equation and record the effects of the above events under the

appropriate account headings. Show the year-end total for each account.

What problems are caused by diverse accounting practices?

Berry Company is going through Chapter 11 bankruptcy reorganization. Prepare the

income statement for the calendar year 2013 using the following information. The

effective tax rate is 20%.

What are the three categories of assets in a Statement of Financial Affairs?

Yang Company reported the following balance sheet for the end of 2012:

During 2013, Yang reported the following transactions:

– Repaid $8,000 to a local bank on a note payable

– Provided services to clients for $26,400 cash

– Paid operating expenses of $19,200

– Paid $3,500 cash dividends to stockholders

Required:

Prepare Yang Company’s balance sheet as of December 31, 2013.

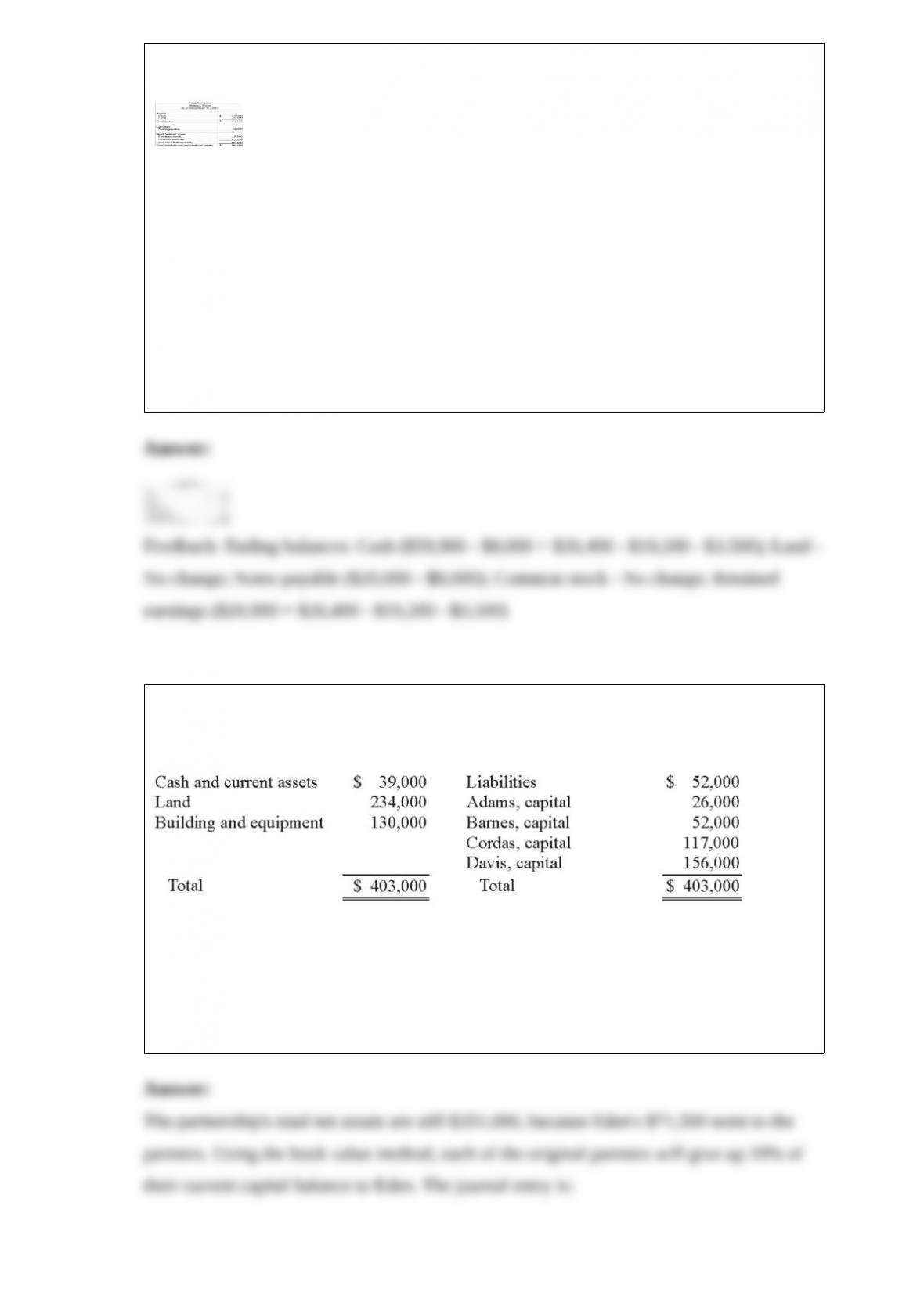

The ABCD Partnership has the following balance sheet at January 1, 2012, prior to the

admission of new partner, Eden.

Eden acquired a 20% interest in the partnership by contributing a total of $71,500

directly to the other four partners. No goodwill is to be recorded. Profits and losses have

previously been split according to the following percentages: Adams, 15%, Barnes,

35%, Cordas, 30%, and Davis, 20%. After Eden made his investment, what were the

individual capital balances?

Name and briefly describe each of the four financial statements.

Jarvis Company experienced the following events during 2012 (all were cash events):

1) issued a note

2) purchased land

3) provided services to customers

4) repaid part of the note in event 1

5) paid operating expenses

6) paid a dividend to stockholders

7) issued common stock

Required:

Indicate how each of these events affects the accounting equation by writing the letter I

for increase, the letter D for decrease, and NA for no effect under each of the

components of the accounting equation. The first is done for you as an example.

What are duties of the creditors committee in Chapter 7 liquidation?

Indicate how each event affects the elements of financial statements. Use the following

letters to record your answer in the box shown below each element. You do not need to

enter amounts.

Ferguson Co. issued common stock for $50,000 cash.