Chapter 13 Relevant Information for Special Decisions

Problem 13-28

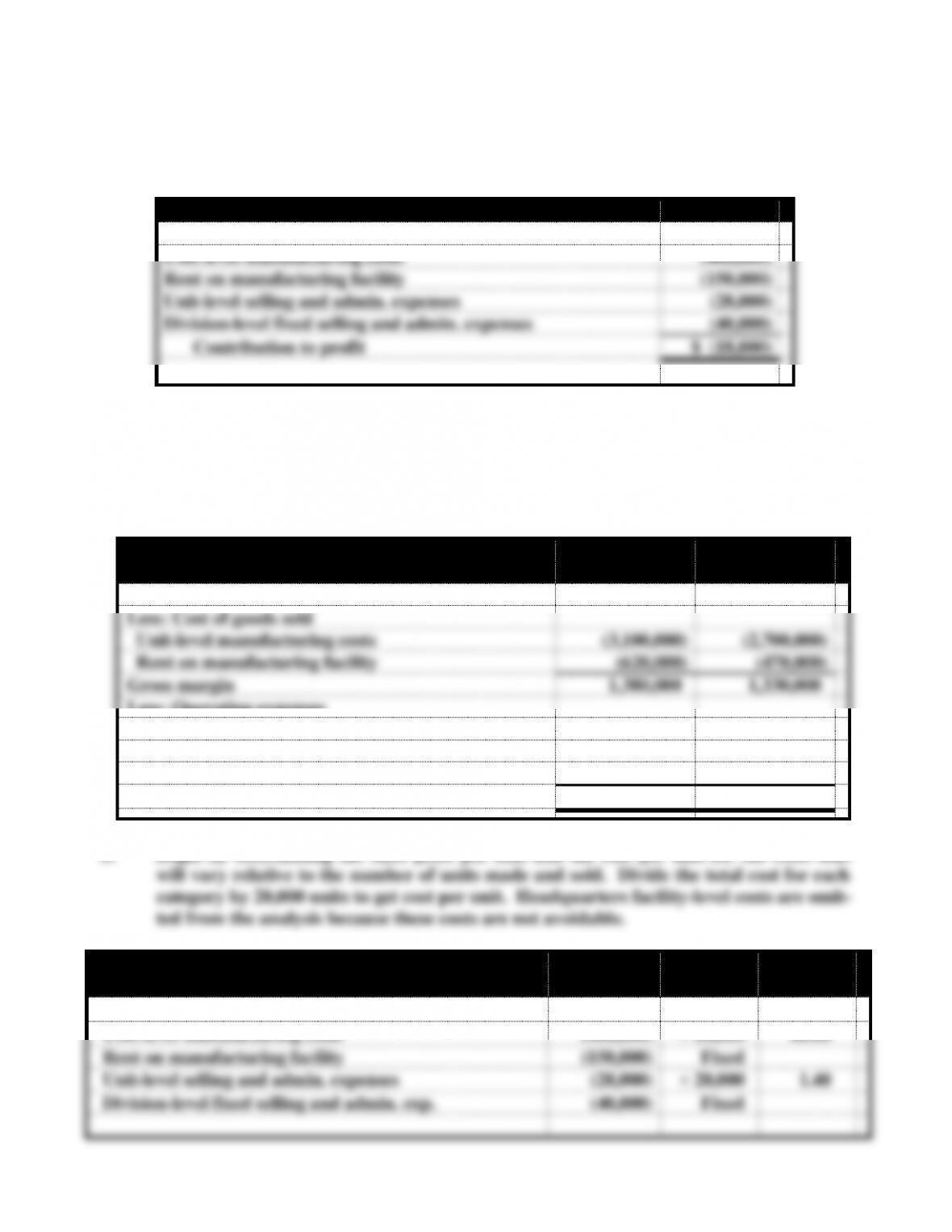

a.

Decision

Division B

Sales

$ 600,000

Unit-level manufacturing costs

(400,000)

Rent on manufacturing facility

(150,000)

Unit-level selling and admin. expenses

(28,000)

Division-level fixed selling and admin. expenses

(40,000)

Contribution to profit

$ (18,000)

Problem 13-28 (continued)

Since Division B’s contribution to profit is negative, the division should be eliminated.

The following companywide income statements support this conclusion.

Companywide Income Statements If:

Keep

Division B

Eliminate

Division B

Sales

$ 5,100,000

$4,500,000

Less: Cost of goods sold

Unit-level manufacturing costs

(3,100,000)

(2,700,000)

Rent on manufacturing facility

(620,000)

(470,000)

Gross margin

1,380,000

1,330,000

Less: Operating expenses

Unit-level selling and admin. expenses

(309,000)

(281,000)

Division-level fixed selling and admin. exp.

(400,000)

(360,000)

Headquarters facility-level costs

(300,000)

(300,000)

Net income (loss)

$ 371,000

$ 389,000

b. Begin by determining the sales price per unit and the cost per unit for the costs that

Division B

÷ No. of

Units

Per Unit

Amounts

Sales

$600,000

÷ 20,000

$30.00

Unit-level manufacturing costs

(400,000)

÷ 20,000

20.00

Rent on manufacturing facility

(150,000)

Fixed

Unit-level selling and admin. expenses

(28,000)

÷ 20,000

1.40

Division-level fixed selling and admin. exp.

(40,000)

Fixed

Chapter 13 Relevant Information for Special Decisions

Problem 13-28 (continued)

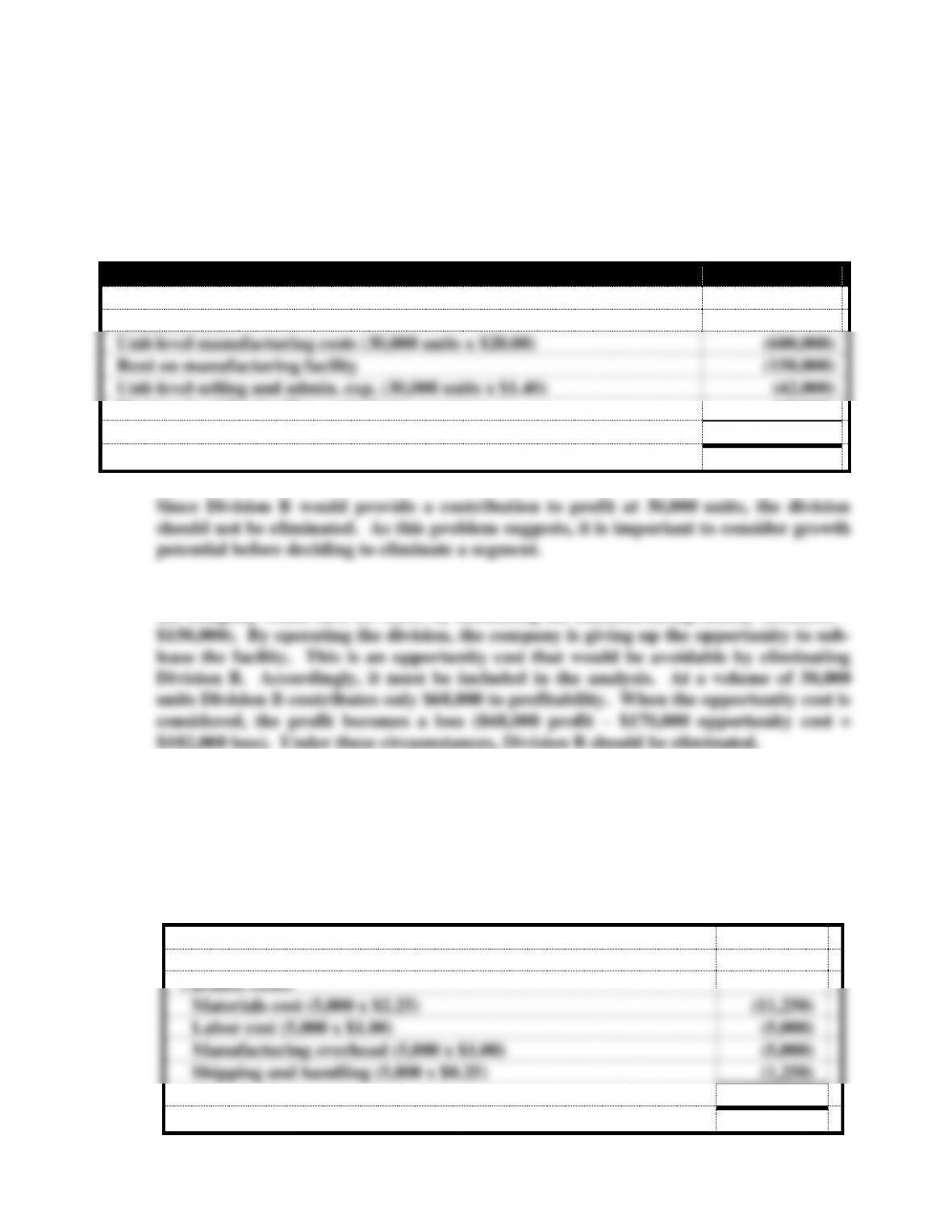

Next, compare differential revenues with avoidable cost.

Division B

Sales revenue (30,000 units x $30.00)

$900,000

Avoidable costs:

Unit-level manufacturing costs (30,000 units x $20.00)

(600,000)

Rent on manufacturing facility

(150,000)

Unit-level selling and admin. exp. (30,000 units x $1.40)

(42,000)

Division-level fixed selling and admin. expenses

(40,000)

Contribution to profit

$ 68,000

c. Given that Borris is paying $150,000 to lease the manufacturing facility for Division B,

the company could earn $170,000 by subleasing the manufacturing facility ($320,000 –

Problem 13-29

a. Since Lang doesn’t have to pay sales commissions in this situation, the company should

remove that item from consideration. All of the fixed expenses must be eliminated

from consideration because they cannot be avoided regardless of whether the special

order is accepted or rejected. The differential revenue and relevant (i.e., avoidable)

costs are shown below:

Revenue (5,000 units x $5.50)

$27,500

Variable costs:

Materials cost (5,000 x $2.25)

(11,250)

Labor cost (5,000 x $1.00)

(5,000)

Manufacturing overhead (5,000 x $1.00)

(5,000)

Shipping and handling (5,000 x $0.25)

(1,250)

Contribution margin

$ 5,000

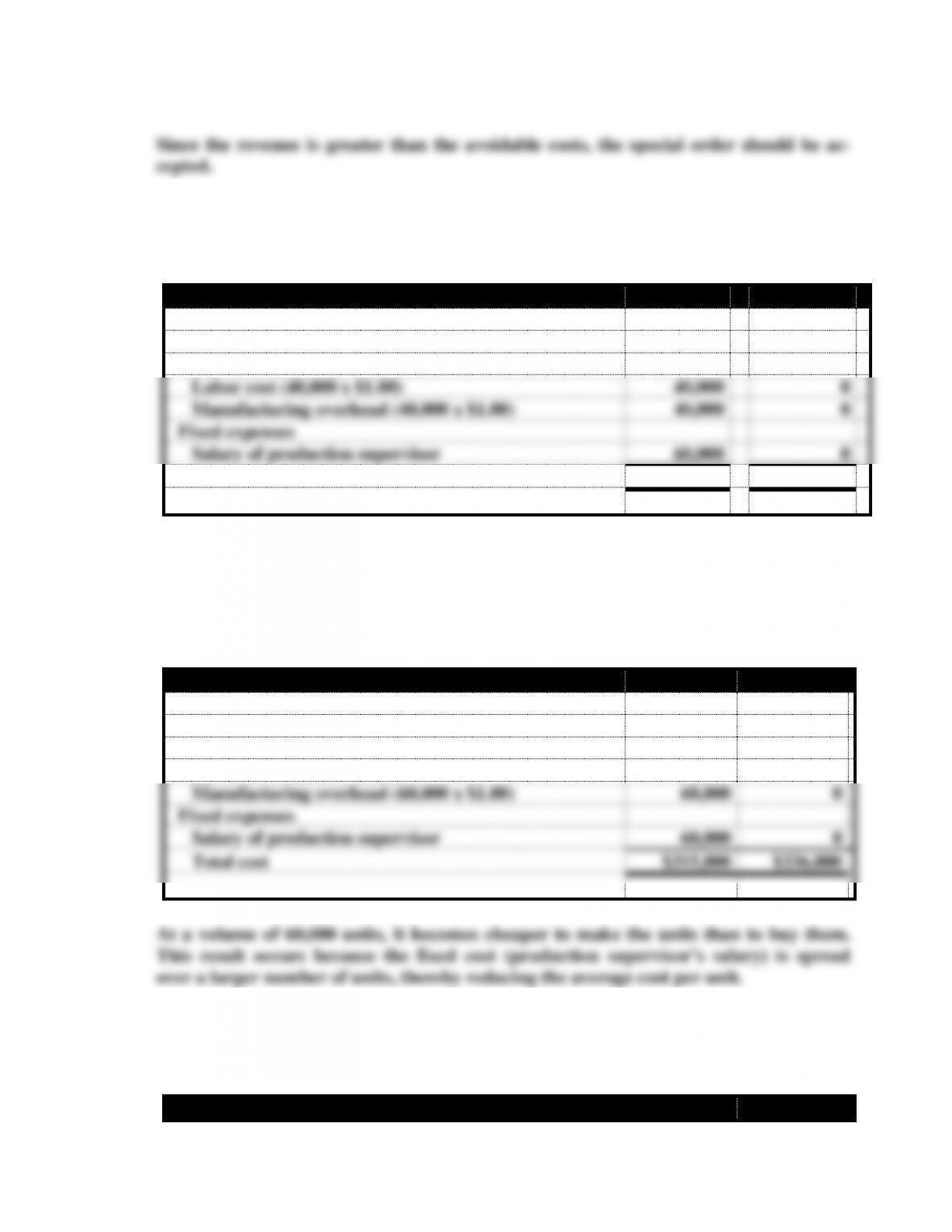

Chapter 13 Relevant Information for Special Decisions

b. The revenue, shipping and handling, sales commissions, advertising costs, and general

company expenses must be eliminated from consideration because they do not differ

between the alternatives. The relevant information is as follows:

Decision

Make

Buy

Unit-level costs

Purchase price (40,000 x $5.60)

$224,000

Materials cost (40,000 x $2.25)

$ 90,000

0

Labor cost (40,000 x $1.00)

40,000

0

Manufacturing overhead (40,000 x $1.00)

40,000

0

Fixed expenses

Salary of production supervisor

60,000

0

Total cost

$230,000

$224,000

At 40,000 units, Lang should buy the calculators.

Problem 13-29 (continued)

Relevant data at 60,000 units of product:

Decision

Make

Buy

Unit-level costs

Purchase price (60,000 x $5.60)

$336,000

Materials cost (60,000 x $2.25)

$135,000

0

Labor cost (60,000 x $1.00)

60,000

0

Manufacturing overhead (60,000 x $1.00)

60,000

0

Fixed expenses

Salary of production supervisor

60,000

0

Total cost

$315,000

$336,000

At a volume of 60,000 units, it becomes cheaper to make the units than to buy them.

c. The general company expenses must be eliminated from consideration because they do

not differ between the alternatives. The differential revenue and avoidable costs are

shown below:

Decision

Chapter 13 Relevant Information for Special Decisions

Revenue (40,000 units x $9.00)

$360,000

Variable costs:

Materials cost (40,000 x $2.25)

(90,000)

Labor cost (40,000 x $1.00)

(40,000)

Manufacturing overhead (40,000 x $1.00)

(40,000)

Shipping and handling (40,000 x $0.25)

(10,000)

Sales commissions (40,000 x $1.00)

(40,000)

Contribution margin

140,000

Fixed expenses

Advertising costs

(20,000)

Salary of production supervisor

(60,000)

Impact on profitability

$ 60,000

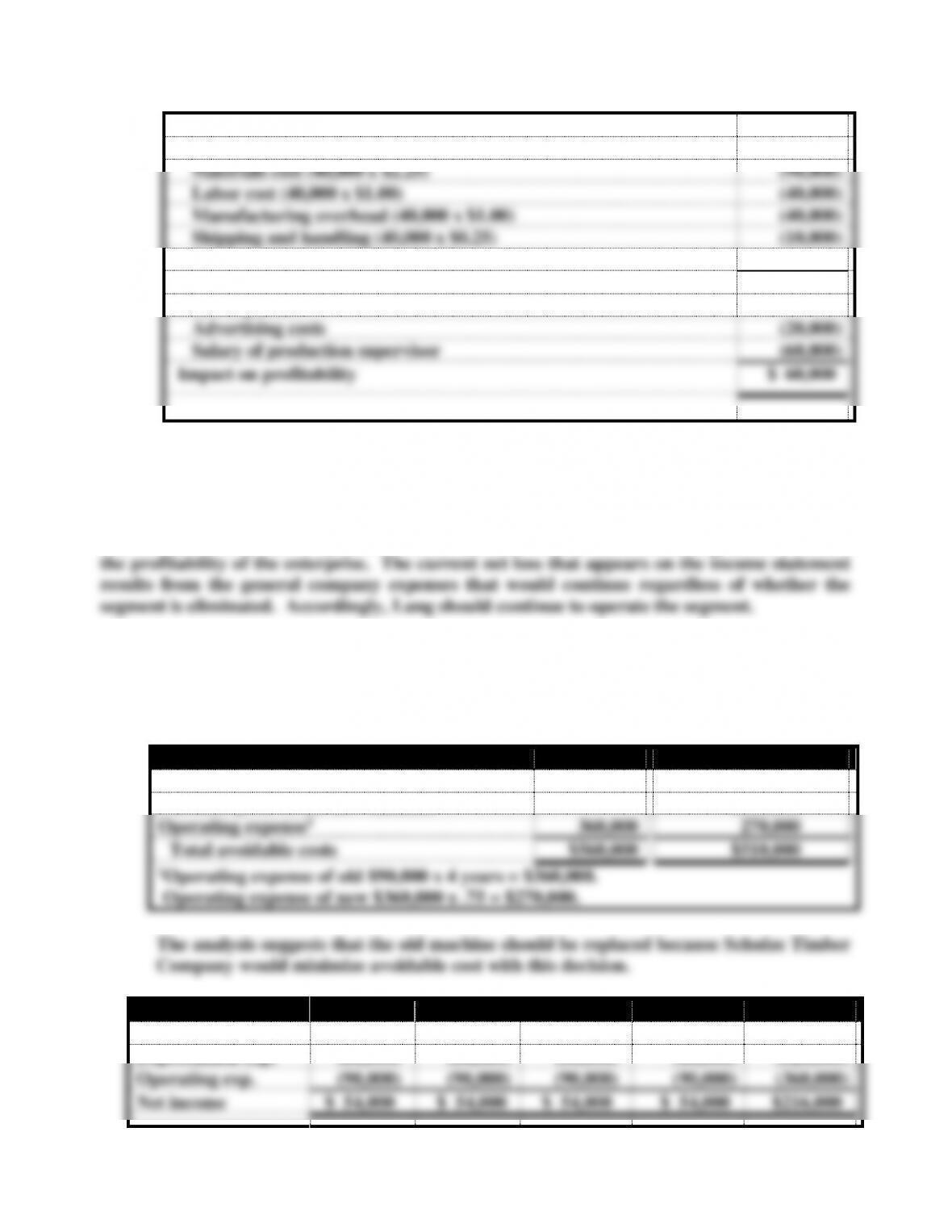

Problem 13-29 (continued)

The analysis shows that the production and sale of calculators is contributing $60,000 toward

Problem 13-30

a. The historical cost of the old machine is a sunk cost and therefore is irrelevant. The

relevant (avoidable) costs for each alternative are shown below:

Decision

Keep Old

Replace With New

Opportunity cost of old machine

$200,000

Purchase price of the new machine

$240,000

Operating expense1

360,000

270,000

Total avoidable costs

$560,000

$510,000

1Operating expense of old $90,000 x 4 years = $360,000.

Operating expense of new $360,000 x .75 = $270,000.

The analysis suggests that the old machine should be replaced because Schulze Timber

b.

2015

2016

2017

2018

Total

Revenue

$224,000

$224,000

$224,000

$224,000

$896,000

Depreciation exp.

(80,000)

(80,000)

(80,000)

(80,000)

(320,000)

Operating exp.

(90,000)

(90,000)

(90,000)

(90,000)

(360,000)

Net income

$ 54,000

$ 54,000

$ 54,000

$ 54,000

$216,000

Chapter 13 Relevant Information for Special Decisions

c.

2015

2016

2017

2018

Total

Revenue

$224,000

$224,000

$224,000

$224,000

$896,000

Depreciation exp.

(60,000)

(60,000)

(60,000)

(60,000)

(240,000)

Operating exp.

(67,500)

(67,500)

(67,500)

(67,500)

(270,000)

Loss on disposal*

(120,000)

(120,000)

Net income (loss)

$(23,500)

$ 96,500

$ 96,500

$ 96,500

$266,000

Problem 13-30 (continued)

d. The computations shown in requirements b and c support the avoidable cost analysis

in Requirement a. The company will earn $50,000 more over the four years by replac-

ing the machine. However, the loss on disposal causes net income in 2015 to be lower

ATC 13–1

a. By eliminating 25 percent of its inventory items, Supervalu can reduce its costs by:

• Reducing the amount of warehouse space it needs to stock its inventory. The

• Reducing the record-keeping cost of keeping track of its inventory.

• Reducing the number of errors related to pricing its products. Having to price

multiple sizes of the same product can result in errors.

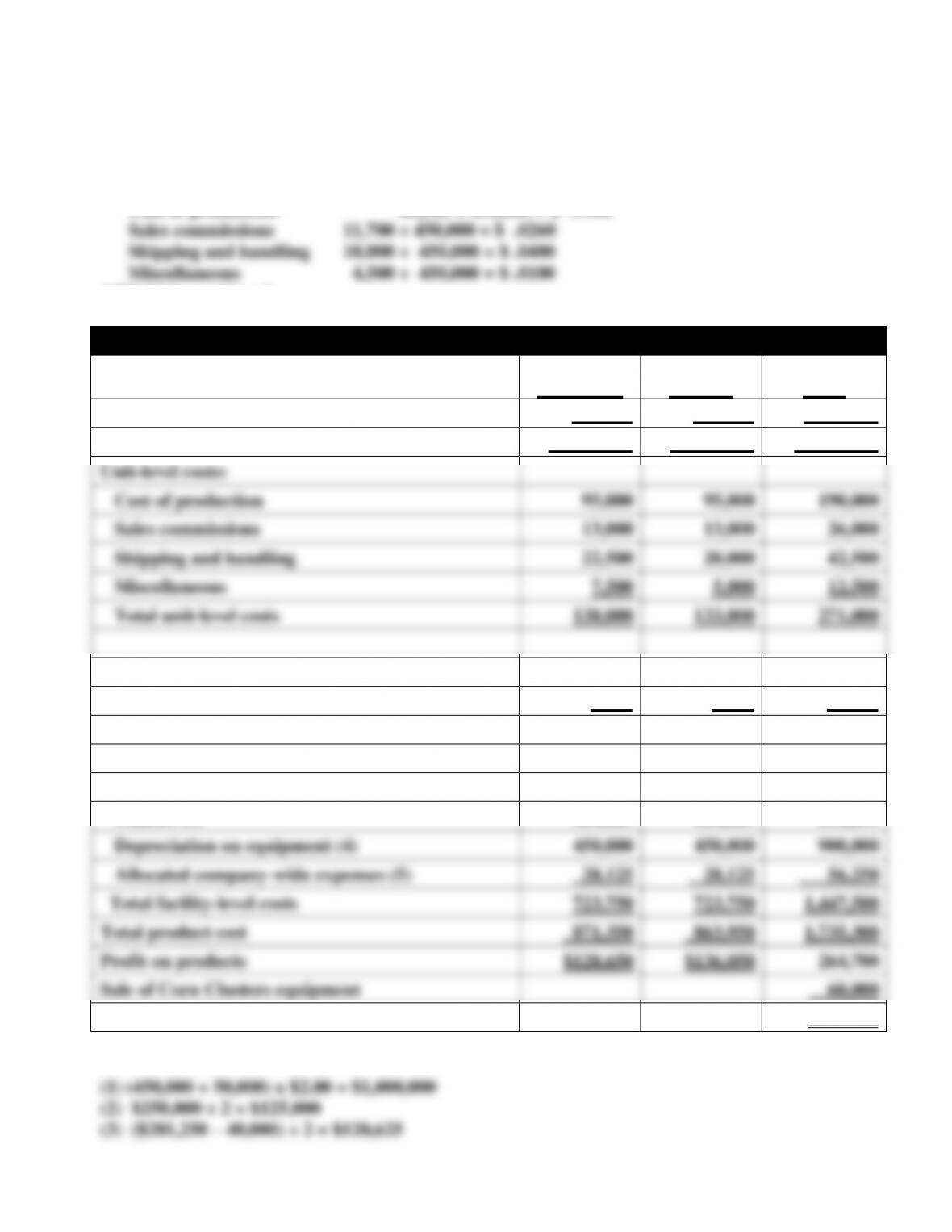

b. Per unit data must be calculated for sales and unit-level costs. These are (remember,

dollar amounts are in thousands):

Oat Flakes:

Sales $900,000 ÷ 450,000 = $2.0000

Chapter 13 Relevant Information for Special Decisions

Miscellaneous 6,750 ÷ 450,000 = $ .0150

Fiber Squares:

Sales $900,000 ÷ 450,000 = $2.0000

Cost of production 85,500 ÷ 450,000 = $ .1900

ATC 13-1 continued

Revised Product-line Earnings Statements

Annual Costs of Operating Each Product Line

Oat Flakes

Fiber

Squares

Total

Sales in units

500,000

500,000

1,000,000

Sales in dollars (1)

$1,000,000

$1,000,000

$2,000,000

Unit-level costs:

Cost of production

95,000

95,000

190,000

Sales commissions

13,000

13,000

26,000

Shipping and handling

22,500

20,000

42,500

Miscellaneous

7,500

5,000

12,500

Total unit-level costs

138,000

133,000

271,000

Product-level costs:

Supervisors salaries

9,600

7,200

16,800

Facility-level costs:

Rent (2)

125,000

125,000

250,000

Utilities (3)

120,625

120,625

241,250

Depreciation on equipment (4)

450,000

450,000

900,000

Allocated company-wide expenses (5)

28,125

28,125

56,250

Total facility-level costs

723,750

723,750

1,447,500

Total product cost

871,350

863,950

1,735,300

Profit on products

$128,650

$136,050

264,700

Sale of Corn Clusters equipment

60,000

Segment earnings

$324,700

Chapter 13 Relevant Information for Special Decisions

ATC 13–2

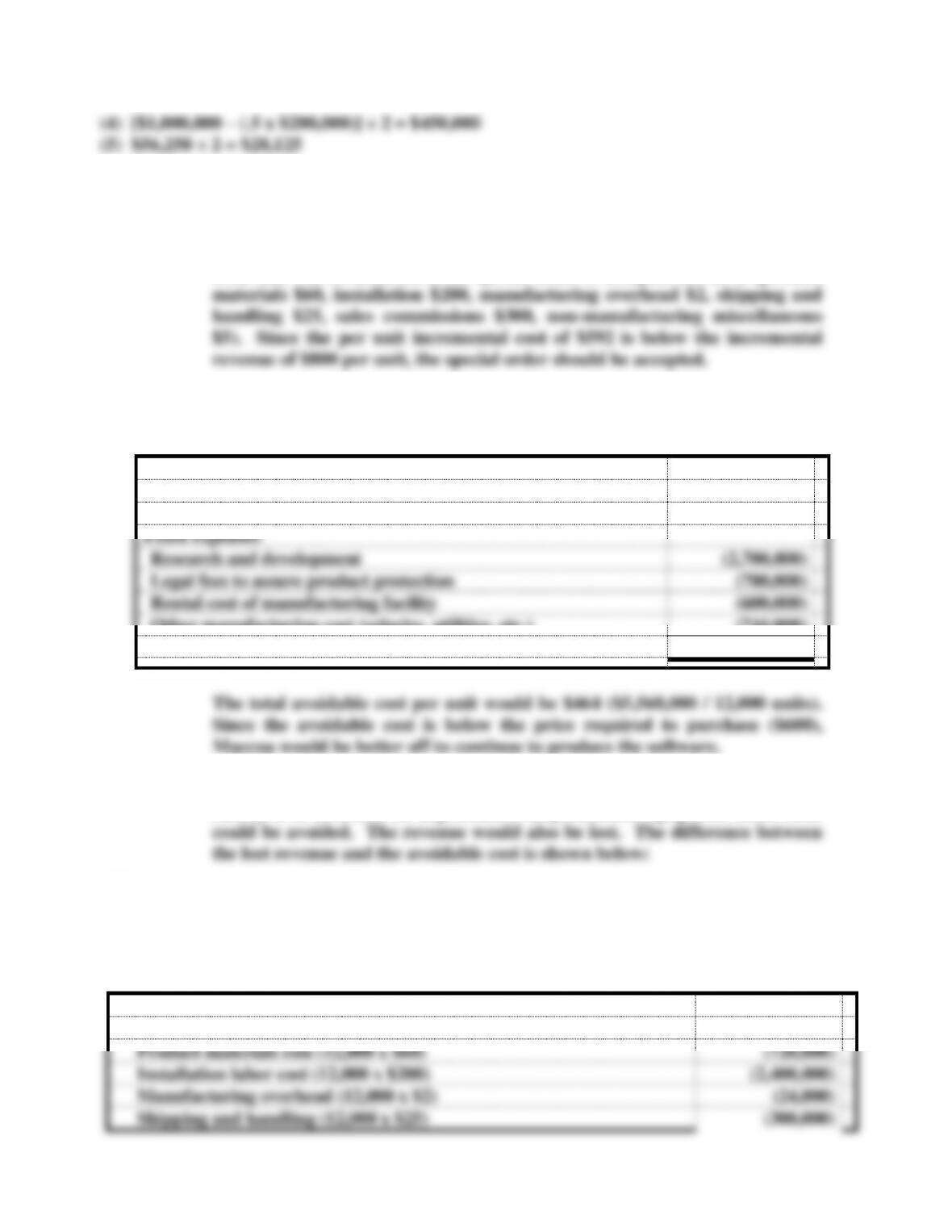

a. Task 1 The fixed costs are not relevant because they will remain the same regard-

less of whether the special order is accepted. The total unit-level incremental

costs that will be incurred if the special order is accepted are $592 (product

Task 2 The costs that could be avoided if the manufacturing process were to be

outsourced are the following:

Unit-level variable costs

Product materials cost (12,000 x $60)

$ (720,000)

Manufacturing overhead (12,000 x $2)

(24,000)

Fixed expenses

Research and development

(2,700,000)

Legal fees to assure product protection

(780,000)

Rental cost of manufacturing facility

(600,000)

Other manufacturing cost (salaries, utilities, etc.)

(744,000)

Total avoidable costs

$(5,568,000)

Task 3 If the division were eliminated, all costs except the allocated companywide

facility-level cost and the depreciation on production equipment (sunk cost)

ATC 13-2 (continued)

Revenue (12,000 units x $1,200)

$14,400,000

Unit-level variable costs

Product materials cost (12,000 x $60)

(720,000)

Installation labor cost (12,000 x $200)

(2,400,000)

Manufacturing overhead (12,000 x $2)

(24,000)

Shipping and handling (12,000 x $25)

(300,000)

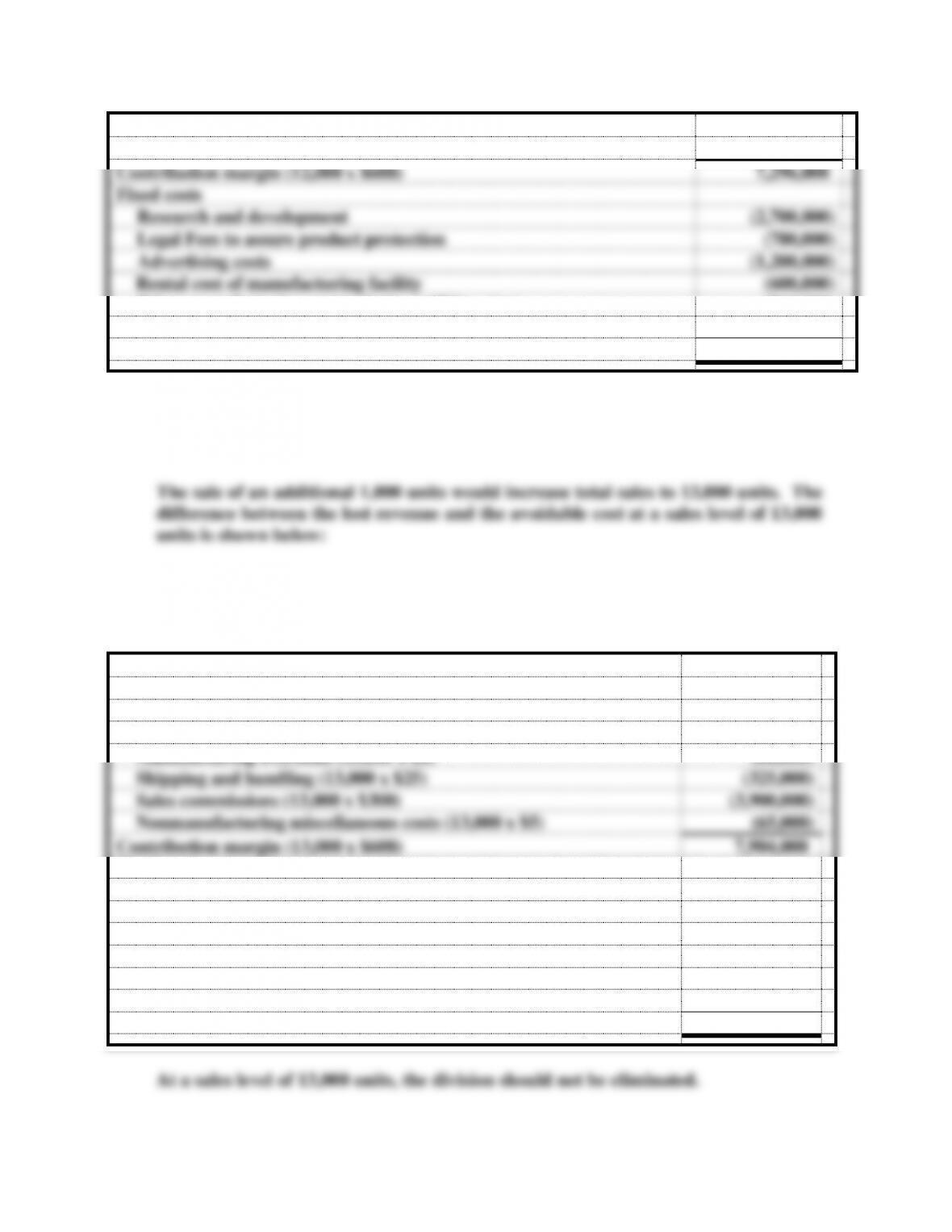

Chapter 13 Relevant Information for Special Decisions

Sales commissions (12,000 x $300)

(3,600,000)

Nonmanufacturing miscellaneous costs (12,000 x $5)

(60,000)

Contribution margin (12,000 x $608)

7,296,000

Fixed costs

Research and development

(2,700,000)

Legal Fees to assure product protection

(780,000)

Advertising costs

(1,200,000)

Rental cost of manufacturing facility

(600,000)

Other manufacturing cost (salaries, utilities, etc.)

(744,000)

Division-level facility sustaining cost

(1,730,000)

Net income (loss)

$ (458,000)

Since the avoidable costs exceed the incremental revenue, the division should be

eliminated.

ATC 13-2 (continued)

Revenue (13,000 units x $1,200)

$15,600,000

Unit-level variable costs

Product materials cost (13,000 x $60)

(780,000)

Installation labor cost (13,000 x $200)

(2,600,000)

Manufacturing overhead (13,000 x $2)

(26,000)

Shipping and handling (13,000 x $25)

(325,000)

Sales commissions (13,000 x $300)

(3,900,000)

Nonmanufacturing miscellaneous costs (13,000 x $5)

(65,000)

Contribution margin (13,000 x $608)

7,904,000

Fixed costs

Research and development

(2,700,000)

Legal Fees to assure product protection

(780,000)

Advertising costs

(1,200,000)

Rental cost of manufacturing facility

(600,000)

Other manufacturing cost (salaries, utilities, etc.)

(744,000)

Division-level facility sustaining cost

(1,730,000)

Net income

$150,000

b.

Chapter 13 Relevant Information for Special Decisions

(1) All variable costs are not always relevant. For example, assume that the special

order customer approaches management directly, thereby eliminating the need to

Chapter 13 Relevant Information for Special Decisions

ATC 13-2 (continued)

(2) Research and development costs are relevant because they are not incurred if the

oriented.

(3) Increases in volume cause the total contribution margin to increase. Accordingly,

more margin is available to cover fixed costs or to contribute to profitability.

ATC 13-3

a.

• Declining volume of mail.

• Inability to raise prices beyond inflation rate.

b. In 2011, first class mail comprised 43.8% of volume and 66.8% of profit.

these costs are fixed.

d. A 1% increase in volume is estimated to increase revenue by $0.6 billion and profit by

$0.2 billion, while a 1% increase in price revenue by $0.3 billion and profit by $0.4 bil-

volume.

e. Changes proposed by the USPS management include:

The proposed changes are estimated to produce cost savings of $20 billion per year, but $10

billion of these savings depend on changes that require legislative approval.

Chapter 13 Relevant Information for Special Decisions

ATC 13-4

Each memo will be different. The instructor should evaluate responses on the basis of

logic. Some representative arguments for each requirement are listed below as examples.

a. It is the incompetence of the state that causes the full cost of providing collection

b. The State Department of Revenue is required to incur costs on behalf of the state.

ATC 13–5

b. The $110,000 purchase price is a sunk cost. The current market price of $75,000 is an

c. Mr. Dillworth’s conclusion is not supported by quantitative analysis. The opportunity

cost of holding on to the old site is $75,000 while the cost of acquiring the new lot is

d. While interpretations may vary, there are at least three standards that could be

considered to be violated by Mr. Dillworth’s refusal to disclose the alternative site