Archives

978-0078025792 Chapter 1 Chapter Problem

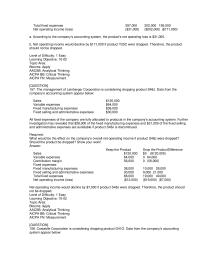

Problem 1-14B (45 minutes) 1. Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Solutions Manual “B” Problems, Chapter 1 1-1 House Of Pianos, Inc. Traditional Income Statement For […]

978-0078025792 Chapter 1 Lecture Note

Chapter 01 Lecture Notes 1 Chapter 1 Lecture Notes Chapter theme: This chapter explains how managers need to rely on different cost classifications for different purposes. The four main purposes emphasized in this chapter include assigning costs to cost objects, […]

978-0078025792 Chapter 1 Solution Manual Part 1

Chapter 1 Managerial Accounting and Cost Concepts Solutions to Questions 1-1 The three major elements of product costs in a manufacturing company are direct materials, direct labor, and manufacturing overhead. constant, but total variable cost changes in direct proportion to […]

978-0078025792 Chapter 1 Solution Manual Part 2

Exercise 1-13 (20 minutes) 1. Traditional income statement The Alpine House, Inc. Traditional Income Statement Sales ………………………………………………………. $150,000 Cost of goods sold ($30,000 + $100,000 – $40,000) ………………… 90,000 Gross margin …………………………………………….. 60,000 Selling and administrative expenses: Selling expenses (($50 […]

978-0078025792 Chapter 1 Solution Manual Part 3

Problem 1-22A (continued) 3. The high-low estimate of fixed costs is $170.90 lower than the estimate provided by least-squares regression. The high-low estimate of the variable cost per unit is $1.82 higher than the estimate provided by least-squares regression. A […]

978-0078025792 Chapter 10 Chapter Problem Part 1

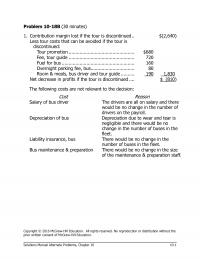

Problem 10-18B (30 minutes) 1. Contribution margin lost if the tour is discontinued .. $(2,640) Less tour costs that can be avoided if the tour is discontinued: Tour promotion ………………………………………… $680 Fee, tour guide ………………………………………… 720 Fuel for bus …………………………………………….. […]

978-0078025792 Chapter 10 Chapter Problem Part 2

Problem 10-24B (continued) Alternative approach: Keep the Plant Open Close the Plant Sales (5,438 units × $40 per unit) ……… $ 217,520 $ 0 Variable expenses (5,438 units × $29 per unit) …………… 157,702 0 Contribution margin ………………………… 59,818 0 […]

978-0078025792 Chapter 10 Lecture Note

Chapter 10 Lecture Notes 1 Chapter 10 Lecture Notes Chapter theme: Making decisions is one of the basic functions of a manager. To be successful in decision making, managers must be able to perform differential analysis, which focuses on identifying […]

978-0078025792 Chapter 10 Solution Manual Part 1

Chapter 10 Differential Analysis: The Key to Decision Making Solutions to Questions 10-1 A relevant cost is a cost that differs in total between the alternatives in a decision. the fixed costs that would be avoided. Even in 10-2 An […]

978-0078025792 Chapter 10 Solution Manual Part 2

Exercise 10–11 (20 minutes) The costs that can be avoided as a result of purchasing from the outside are relevant in a make-or-buy decision. The analysis is: Per Unit Differential Costs 30,000 Units Make Buy Make Buy Cost of purchasing […]

978-0078025792 Chapter 10 Solution Manual Part 3

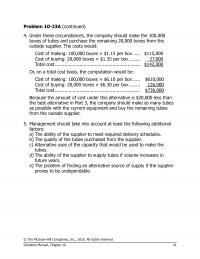

Problem 10-23A (continued) 4. Under these circumstances, the company should make the 100,000 boxes of tubes and purchase the remaining 20,000 boxes from the outside supplier. The costs would: Cost of making: 100,000 boxes × $1.15 per box ….. $115,000 […]

978-0078025792 Chapter 10 Solution Manual Part 4

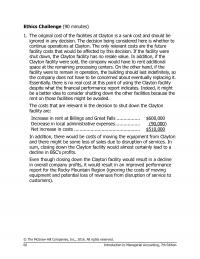

Ethics Challenge (90 minutes) 1. The original cost of the facilities at Clayton is a sunk cost and should be ignored in any decision. The decision being considered here is whether to continue operations at Clayton. The only relevant costs […]

978-0078025792 Chapter 11 Chapter Problem

Problem 11-12B (15 minutes) Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Solutions Manual Alternate Problems, Chapter 11 11-1 Item Year(s) Amount of Cash Flows 19% Factor Present […]

978-0078025792 Chapter 11 Lecture Note

Chapter 11 Capital Budgeting Decisions 1 Chapter 11 Lecture Notes Chapter theme: The term capital budgeting is used to describe how managers plan significant cash outlays on projects that have long-term implications such as the purchase of new equipment and […]

978-0078025792 Chapter 11 Solution Manual Part 1

Chapter 11 Capital Budgeting Decisions Solutions to Questions 11-1 A capital budgeting screening decision is concerned with whether a proposed investment project passes a preset hurdle, such as a 15% rate of return. A capital budgeting preference decision is concerned […]

978-0078025792 Chapter 11 Solution Manual Part 2

Problem 11-13A (continued) 2. The simple rate of return is computed as follows: Annual incremental net operating income Simple rate of return = Initial investment $400,000 = = 11.4% $3,500,000 3. The company would want Casey to invest in the […]

978-0078025792 Chapter 11 Solution Manual Part 3

Problem 11-25A (continued) 2. Considering all three investments together, Linda did not earn a 16% rate of return. The computation is: Net Present Value Common stock ……………………. $ 7,560 Preferred stock ……………………. (8,650) Bonds ……………………………….. (2,743) Overall net present value […]

978-0078025792 Chapter 11A Lecture Note

Chapter 11 Capital Budgeting Decisions I. Appendix 11A: the concept of present value (Slide #1 is the title slide for this appendix) Learning Objective 11-5: Understand present value concepts and the use of present value tables. A. The mathematics of […]

978-0078025792 Chapter 12 Chapter Problem Part 1

Problem 12-7B (30 minutes) 1. Net cash provided by operating activities: Step 1: The following equation can be applied to the Accumulated Depreciation account to compute the depreciation to add back to net income: Beginning balance – Debits + Credits […]

978-0078025792 Chapter 12 Chapter Problem Part 2

Problem 12-11B (45 minutes) To begin the problem, fill in the question mark pertaining to item “a” using the following T-account: Retained Earnings Dividends 10,800 Net income 86,100 Change 75,300 The change in the retained earnings balance is $75,300 and […]

978-0078025792 Chapter 12 Lecture Note

Chapter 12 Statement of Cash Flows Chapter 12 Lecture Notes Chapter theme: This chapter explains how to prepare and interpret the statement of cash flows. I. Statement of cash flows A. Setting the stage i. The statement of cash flows […]

978-0078025792 Chapter 12 Solution Manual Part 1

Chapter 12 Statement of Cash Flows Solutions to Questions 12-1 The statement of cash flows highlights the major activities that impact cash flows and hence affect the overall cash balance. borrowing of $500,000 must both be shown “gross” on the […]

978-0078025792 Chapter 12 Solution Manual Part 2

Problem 12-8A (20 minutes) Transaction Operating Investing Financing Cash Inflow Cash Outflow a. Paid suppliers for inventory purchases ….. X X b. Bought equipment for cash ……………….. X X c. Paid cash to repurchase its own stock ….. X X […]

978-0078025792 Chapter 12 Solution Manual Part 3

Problem 12-13A (continued) The decrease in the long-term investments account ($20,000) equals the cost of the long-term investment sold; therefore, Rusco did not purchase any long-term investments during the year. The proceeds from the sale of the long-term investment ($30,000) […]

978-0078025792 Chapter 12A Lecture Note

Chapter 12 Statement of Cash Flows I. Appendix 12A: The direct method of determining the net cash provided by operating activities (Slide #1 is a title slide for the appendix) Learning Objective 12-4: Use the direct method to determine the […]

978-0078025792 Chapter 13 Chapter Problem

Problem 13-13B (60 minutes) Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Solutions Manual Alternate Problems, Chapter 13 13-1 This Year Last Year 1. a. Current assets (a) […]

978-0078025792 Chapter 13 Lecture Note

Chapter 13 Financial Statement Analysis 1 Chapter 13 Lecture Notes Chapter theme: This chapter focuses on financial statement analysis which managers use to assess the financial health of their companies. It includes examining trends in key financial data, comparing financial […]

978-0078025792 Chapter 13 Solution Manual Part 1

Chapter 13 Financial Statement Analysis Solutions to Questions 13-1 Horizontal analysis examines how a particular item on a financial statement such as sales or cost of goods sold behaves over time. Vertical analysis involves analysis of items on an income […]

978-0078025792 Chapter 13 Solution Manual Part 2

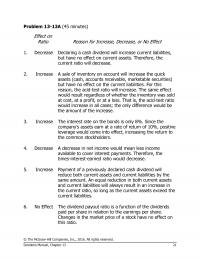

Problem 13-13A (45 minutes) Effect on Ratio Reason for Increase, Decrease, or No Effect 1. Decrease Declaring a cash dividend will increase current liabilities, but have no effect on current assets. Therefore, the current ratio will decrease. 2. Increase A […]

978-0078025792 Chapter 13 Solution Manual Part 3

Problem 13-18A (continued) b. Sabin Electronics Common-Size Income Statements This Year Last Year Sales …………………………………………….. 100.0 % 100.0 % Cost of goods sold ……………………………. 77.5 79.3 Gross margin ………………………………….. 22.5 20.7 Selling and administrative expenses …….. 13.1 12.6 Net operating […]

978-0078025792 Chapter 2 Chapter Problem Part 1

Problem 2-21B (30 minutes) 1. The predetermined overhead rate was: Y = $1,278,000 + $3.40 per hour × 82,000 hours Estimated fixed manufacturing overhead ……………… $1,278,000 Estimated variable manufacturing overhead $3.40 per computer hour × 82,000 hours…………… 278,800 Estimated total […]

978-0078025792 Chapter 2 Chapter Problem Part 2

2-12 Introduction to Managerial Accounting, 6th edition Problem 2-25B (continued) Rent Expense Cost of Goods Sold (h) 17,000 (l) 530,000 Sales (l) 1,100,000 3. Mariya Company Schedule of Cost of Goods Manufactured Direct materials: Raw materials inventory, beginning ………………. $ […]

978-0078025792 Chapter 2 Lecture Note

Chapter 02 Lecture Notes 2-1 Chapter 2 Lecture Notes Chapter theme: Managers need to assign costs to products to facilitate external financial reporting and internal decision making. This chapter illustrates an absorption costing approach to calculating product costs known as […]

978-0078025792 Chapter 2 Solution Manual Part 1

Chapter 2 Job-Order Costing Solutions to Questions 2-1 By definition, manufacturing overhead consists of costs that cannot be practically traced to jobs. Therefore, if these costs are to be as- signed to jobs, they must be allocated rather than reason, […]

978-0078025792 Chapter 2 Solution Manual Part 2

Exercise 2-14 (20 minutes) 1. The estimated total manufacturing overhead cost is computed as fol- lows: Y = $650,000 + ($3.00 per MH)(100,000 MHs) Estimated fixed manufacturing overhead ………………. $650,000 Estimated variable manufacturing overhead: $3.00 per MH × 100,000 MHs […]

978-0078025792 Chapter 2 Solution Manual Part 3

Problem 2-25A (continued) 5. The amount of overhead cost in Work in Process was: $24,000 direct materials cost × 160% = $38,400 The amount of direct labor cost in Work in Process is: Total ending work in process …………… $70,000 […]

978-0078025792 Chapter 2 Solution Manual Part 4

Teamwork in Action 1. The types of transactions that are posted to the accounts may be sum- marized in T-account form as follows: Raw Materials Beginning balance Purchases Direct materials used (to Work in Process) Accounts Payable Beginning balance Payments […]

978-0078025792 Chapter 3 Chapter Problem

Problem 3-12B (30 minutes) 1. Under the traditional direct labor-dollar based costing system, manufacturing overhead is applied to products using the predetermined overhead rate computed as follows: Predetermined overhead rate = Estimated total manufacturing overhead cost ÷ Estimated total direct […]

978-0078025792 Chapter 3 Lecture Note

Chapter 03 Activity-Based Costing 3-1 Chapter 3 Lecture Notes Chapter theme: Overhead costs cannot be easily traced to products. Using a plantwide predetermined overhead rate as described in Chapter 2 is simple but may inaccurately assign costs to products. Activity-based […]

978-0078025792 Chapter 3 Solution Manual Part 1

Chapter 3 Activity-Based Costing Solutions to Questions 3-1 The most common methods of assigning overhead costs to products are plantwide over– head rates, departmental overhead rates, and activity-based costing. stage, costs are assigned to activity cost pools. In the second […]

978-0078025792 Chapter 3 Solution Manual Part 2

Exercise 3-9 (continued) 2. Activity costs are assigned to the two hospitals as follows: City General: Activity Cost Pool (a) Activity Rate (b) Activity (a) × (b) ABC Cost Customer deliveries …………. $80.00 per delivery 10 deliveries $ 800 Manual […]

978-0078025792 Chapter 3 Solution Manual Part 3

Problem 3-18A (30 minutes) 1. The activity rates are computed as follows: Activity Cost Pool (a) Estimated Overhead Cost (b) Expected Activity (a) ÷ (b) Activity Rate Labor related ……… $35,000 7,000 DLHs $5 per DLH Production orders … $4,000 […]

978-0078025792 Chapter 3 Solution Manual Part 4

Analytical Thinking (continued) 2. The unit product cost of each product under activity-based costing is given below. For comparison, the costs computed by the company’s accounting department using conventional costing are also provided. Activity-Based Costing Direct Labor-Hour Base Standard Specialty […]

978-0078025792 Chapter 4 Chapter Problem

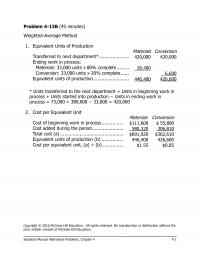

Problem 4-13B (45 minutes) Weighted-Average Method Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Solutions Manual Alternative Problems, Chapter 4 4-1 1. Equivalent Units of Production Materials Conversion […]

978-0078025792 Chapter 4 Lecture Note

Chapter 4 Process Costing 1 Chapter 4 Lecture Notes Chapter theme: Managers need to assign costs to products to facilitate external financial reporting and internal decision making. This chapter illustrates an absorption costing approach to calculating product costs known as […]

978-0078025792 Chapter 4 Solution Manual Part 1

Chapter 4 Process Costing Solutions to Questions 4-1 A process costing system should be used in situations where a homogeneous product is produced on a continuous basis in large quantities. 4-2 Job-order and processing costing are similar in the following […]

978-0078025792 Chapter 4 Solution Manual Part 2

Problem 4-15A (45 minutes) Weighted-Average Method 1. Equivalent units of production: Materials Conversion Transferred to next department …………………… 160,000 160,000 Ending work in process: Materials: 40,000 units x 100% complete ……. 40,000 Conversion: 40,000 units x 25% complete …… 10,000 […]

978-0078025792 Chapter 4 Solution Manual Part 3

Exercise 4-10 (10 minutes) Weighted-Average Method Materials Labor & Overhead Pounds transferred to the Packing Department during July* ……………………………………………… 377,000 377,000 Work in process, July 31: Materials: 25,000 pounds × 100% complete ……. 25,000 Labor and overhead: 25,000 pounds × […]

978-0078025792 Chapter 5 Chapter Problem Part 1

Problem 5-19B (60 minutes) 1. Profit = Unit CM × Q − Fixed expenses $0 = (($58 − $37.60) × Q) − $401,880 $0 = ($20.40 × Q) − $401,880 $20.40Q = $401,880 Q = $401,880 ÷ $20.40 per shirt […]

978-0078025792 Chapter 5 Chapter Problem Part 2

Problem 5-25B (45 minutes) 1. Sales (25,600 units × SFr92 per unit) ………………. SFr2,355,200 Variable expenses (25,600 units × SFr62 per unit) ……………………. 1,587,200 Contribution margin ……………………………………… 768,000 Fixed expenses ……………………………………………. 831,000 Net operating loss ……………………………………….. SFr (63,000) 2. Unit […]

978-0078025792 Chapter 5 Chapter Problem Part 3

Problem 5-28B (continued) 5. a. Contribution margin $105,000 Degree of operating leverage= = = 7.00 Net operating income $15,000 b. 7.00 × 10% sales increase = 70% increase in net operating income. Thus, net operating income next year would be: […]

978-0078025792 Chapter 5 Lecture Note

Chapter 5 Lecture Notes 5-1 Chapter 5 Lecture Notes Chapter theme: Cost-volume-profit (CVP) analysis helps managers understand the interrelationships among cost, volume, and profit by focusing their attention on the interactions among the prices of products, volume of activity, per […]

978-0078025792 Chapter 5 Solution Manual Part 2

Exercise 5-11 (20 minutes) a. Case #1 Case #2 Number of units sold .. 15,000 * 4,000 Sales …………………….. $180,000 * $12 $100,000 * $25 Variable expenses ……. 120,000 * 8 60,000 15 Contribution margin …. 60,000 $ 4 40,000 […]

978-0078025792 Chapter 5 Solution Manual Part 3

Problem 5-20A (continued) c. This problem illustrates the difficulty faced by some companies. When variable labor costs increase, it is often difficult to pass these cost increases along to customers in the form of higher prices. Thus, companies are forced […]

978-0078025792 Chapter 5 Solution Manual Part 4

Problem 5-28A (continued) 2. The sales mix has shifted over the last year from Standard sets to Deluxe sets. This shift has caused a decrease in the company’s overall CM ratio from 54.2% in April to 47.1% in May. For […]

978-0078025792 Chapter 5 Solution Manual Part 5

Analytical Thinking (continued) Allocation of common fixed expenses on the basis of sales revenue: Velcro Metal Nylon Total Sales …………………………….. $165,000 $300,000 $340,000 $805,000 Percentage of total sales …… 20.497% 37.267% 42.236% 100.0% Allocated common fixed expense* …………………….. $49,193 $ […]

978-0078025792 Chapter 6 Chapter Problem Part 1

Problem 6-18B (45 minutes) 1. a. The unit product cost under absorption costing is: Direct materials ……………………………… $17 Direct labor …………………………………… 8 Variable manufacturing overhead ………. 1 Fixed manufacturing overhead ($882,000 ÷ 49,000 units) …………….. 18 Absorption costing unit product […]

978-0078025792 Chapter 6 Chapter Problem Part 2

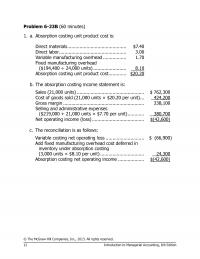

Problem 6-23B (60 minutes) 1. a. Absorption costing unit product cost is: Direct materials ……………………………………. $7.40 Direct labor …………………………………………. 3.00 Variable manufacturing overhead …………….. 1.70 Fixed manufacturing overhead ($194,400 ÷ 24,000 units) …………………… 8.10 Absorption costing unit product cost …………. […]

978-0078025792 Chapter 6 Lecture Note

Chapter 6 Lecture Notes Chapter 6 Lecture Notes Chapter theme: Two general approaches are used for valuing inventories and cost of goods sold. One approach, called absorption costing, is generally used for external reporting purposes. The other approach, called variable […]

978-0078025792 Chapter 6 Solution Manual Part 2

Exercise 6-11 (20 minutes) 1. Division Total Company East Central West Sales ………………………… $1,000,000 $250,000 $400,000 $350,000 Variable expenses ……….. 390,000 130,000 120,000 140,000 Contribution margin …….. 610,000 120,000 280,000 210,000 Traceable fixed expenses . 535,000 160,000 200,000 175,000 Divisional […]

978-0078025792 Chapter 6 Solution Manual Part 3

Problem 6-23A (60 minutes) 1. a. Absorption costing unit product cost is: Direct materials ……………………………. $ 3.50 Direct labor …………………………………. 12.00 Variable manufacturing overhead …….. 1.00 Fixed manufacturing overhead ($300,000 ÷ 30,000 units) …………… 10.00 Absorption costing unit product cost […]

978-0078025792 Chapter 6 Solution Manual Part 4

Analytical Thinking (continued) 2. a. No, the cookbook line should not be eliminated. The cookbook is covering all of its own costs and is generating an $18,000 segment margin toward covering the company’s common costs and toward profits. (Note: Problems […]

978-0078025792 Chapter 7 Chapter Problem Part 1

Problem 7-17B (30 minutes) 1. September cash sales ………………………………………. $ 9,500 September collections on account: July sales: $21,000 × 21% ……………………………… 4,410 August sales: $26,000 × 65% …………………………. 16,900 September sales: $37,000 × 10% …………………….. 3,700 Total cash collections ……………………………………….. […]

978-0078025792 Chapter 7 Chapter Problem Part 2

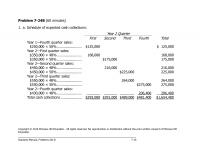

Problem 7-24B (60 minutes) 1. a. Schedule of expected cash collections: Year 2 Quarter First Second Third Fourth Total Year 1—Fourth quarter sales: $250,000 × 50% ………………….. $125,000 $ 125,000 Year 2—First quarter sales: $350,000 × 48% ………………….. 168,000 168,000 […]

978-0078025792 Chapter 7 Lecture Note Part 1

Chapter 7 Lecture Notes 1 Chapter 7 Lecture Notes Chapter theme: This chapter describes how organizations define their financial goals by preparing numerous budgets that collectively form an integrated business plan known as a master budget. The master budget communicates […]

978-0078025792 Chapter 7 Lecture Note Part 2

Chapter 7 Lecture Notes 12 4. The fourth step is to calculate the materials to be purchased for May (221,500 pounds). Notice: a. April’s desired ending inventory becomes May’s beginning inventory. 5. The fifth step is to calculate the materials […]

978-0078025792 Chapter 7 Solution Manual Part 1

Chapter 7 Master Budgeting Solutions to Questions 7-1 A budget is a detailed quantitative plan for the acquisition and use of financial and other resources over a given time period. Budgetary control involves using budgets to increase the likelihood that […]

978-0078025792 Chapter 7 Solution Manual Part 2

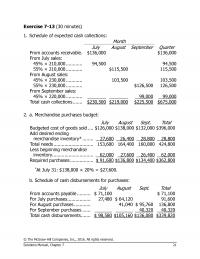

Exercise 7-13 (30 minutes) 1. Schedule of expected cash collections: Month July August September Quarter From accounts receivable . $136,000 $136,000 From July sales: 45% × 210,000 ………… 94,500 94,500 55% × 210,000 ………… $115,500 115,500 From August sales: 45% […]

978-0078025792 Chapter 7 Solution Manual Part 3

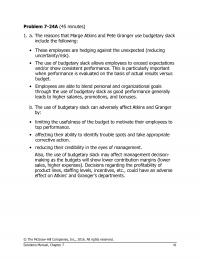

Problem 7-24A (45 minutes) 1. a. The reasons that Marge Atkins and Pete Granger use budgetary slack include the following: • These employees are hedging against the unexpected (reducing uncertainty/risk). • The use of budgetary slack allows employees to exceed […]

978-0078025792 Chapter 7 Solution Manual Part 4

Ethics Challenge (continued) It would take tremendous courage for Keri to take the problem all the way up to Stokes himself—particularly in view of his less-than-humane treatment of subordinates. And going to the Board of Directors is unlikely to work […]

978-0078025792 Chapter 7 Solution Manual Part 5

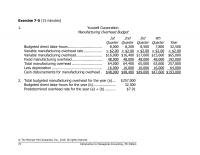

Exercise 7-5 (15 minutes) 1. Yuvwell Corporation Manufacturing Overhead Budget 1st Quarter 2nd Quarter 3rd Quarter 4th Quarter Year Budgeted direct labor-hours ………………………….. 8,000 8,200 8,500 7,800 32,500 Variable manufacturing overhead rate …………….. × $2.00 × $2.00 × $2.00 × […]

978-0078025792 Chapter 8 Chapter Problem Part 1

Problem 8-18B (45 minutes) 1. a. Standard Quantity Allowed for Actual Output, at Standard Price (SQ × SP) Actual Quantity of Input, at Standard Price (AQ × SP) Actual Quantity of Input, at Actual Price (AQ × AP) 28,000 pounds* […]

978-0078025792 Chapter 8 Chapter Problem Part 2

Problem 8-21B (continued) 2. The computations to follow will require the standard quantities allowed for the actual output for each material. Standard Quantity Allowed Material X342: Production of Alpha8 (1.5 kilos per unit × 1,200 units) …… 1,800 kilos Production […]

978-0078025792 Chapter 8 Lecture Note

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis 8-1 Chapter 8 Lecture Notes Chapter theme: This chapter explains how to prepare flexible budgets and how to compare them to actual results for the purposes of computing revenue and spending […]

978-0078025792 Chapter 8 Solution Manual Part 1

Chapter 8 Flexible Budgets, Standard Costs, and Variance Analysis Solutions to Questions 8-1 The planning budget is prepared for the planned level of activity. It is static because it is not adjusted even if the level of activity subsequently changes. […]

978-0078025792 Chapter 8 Solution Manual Part 2

Exercise 8-12 (45 minutes) 1. The planning budget based on 3 courses and 45 students appears below: Gourmand Cooking School Planning Budget For the Month Ended September 30 Budgeted courses (q1) ………………………………………. 3 Budgeted students (q2) ……………………………………… 45 Revenue ($800q2) […]

978-0078025792 Chapter 8 Solution Manual Part 3

Problem 8-20A (continued) 3. Both the labor efficiency and variable overhead efficiency variances are affected by inefficient use of labor time. Excess of actual over standard cost per unit ……. $0.08 U Less portion attributable to labor inefficiency: Labor efficiency […]

978-0078025792 Chapter 8 Solution Manual Part 4

Case (continued) 2. The spending variances are computed as follows: The Little Theatre Spending Variances For the Year Ended December 31 Actual Results Spending Variances Flexible Budget Number of productions (q1) …….. 7 7 Number of performances (q2) ….. 168 […]

978-0078025792 Chapter 8 Solution Manual Part 5

Problem 8A-9A (continued) Fixed overhead variances: Actual Fixed Overhead Budgeted Fixed Overhead Fixed Overhead Applied to Work in Process $209,400 $210,000 32,000 hours × $6 per hour = $192,000 Budget Variance = $600 F Volume Variance = […]

978-0078025792 Chapter 8 Solution Manual Part 6

Exercise 8B-2 (45 minutes) 1. a. Actual Quantity of Input, at Actual Price Actual Quantity of Input, at Standard Price Standard Quantity Allowed for Output, at Standard Price (AQ × AP) (AQ × SP) (SQ × SP) 10,000 yards × […]

978-0078025792 Chapter 8A Lecture Note

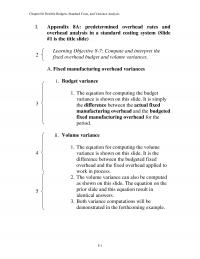

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis 8-1 I. Appendix 8A: predetermined overhead rates and overhead analysis in a standard costing system (Slide #1 is the title slide) Learning Objective 8-7: Compute and interpret the fixed overhead budget […]

978-0078025792 Chapter 8B Lecture Note

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis 8-1 I. Appendix 8B: General Ledger Entries to Record Variances (Slide #1 is the title slide) Learning Objective 8-8: Prepare journal entries to record standard costs and variances. A. Glacier Peak […]

978-0078025792 Chapter 9 Chapter Problem

Problem 9-14B (30 minutes) Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Solutions Manual, Chapter 9 9-1 1. Present New Line Total (1) Sales ……………………. $22,000,000 $10,290,000 $32,290,000 […]

978-0078025792 Chapter 9 Lecture Note

Chapter 9 Performance Measurement in Decentralized Organizations 1 Chapter 9 Lecture Notes Chapter theme: Managers in large organizations have to delegate some decisions to those who are at lower levels in the organization. This chapter explains how responsibility accounting systems, […]

978-0078025792 Chapter 9 Solution Manual Part 1

Chapter 9 Performance Measurement in Decentralized Organizations Solutions to Questions 9-1 In a decentralized organization, decision-making authority isn’t confined to a few top executives; instead, decision-making authority is spread throughout the organization. 9-6 If ROI is used to evaluate performance, […]

978-0078025792 Chapter 9 Solution Manual Part 2

Exercise 9-11 (30 minutes) 1. Net operating income Margin = Sales $70,000 = = 5% $1,400,000 Sales Turnover = Average operating assets $1,400,000 = = 4 $350,000 ROI = Margin × Turnover = 5% × 4 = 20% 2. Net […]

978-0078025792 Chapter 9 Solution Manual Part 3

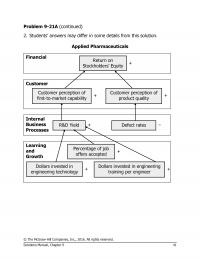

Problem 9-21A (continued) 2. Students’ answers may differ in some details from this solution. Applied Pharmaceuticals Return on Stockholders’ Equity Financial Customer perception of first-to-market capability Customer perception of product quality Customer R&D Yield Defect rates Internal Business Processes Dollars […]

978-0078025792 Chapter 9 Solution Manual Part 4

Chapter 9 Take Two Solutions Exercise 9-1 (10 minutes) 1. Net operating income Margin = Sales $600,000 = = 7.5% $8,000,000 2. Sales Turnover = Average operating assets $8,000,000 = = 1.6 $5,000,000 3. ROI = Margin × Turnover = […]

978-0078025792 Lecture Note Chapter 4 Supplement

Chapter 4 Process Costing I. Supplement: FIFO method (slide 1: title slide) A. FIFO vs. weighted-average method i. The FIFO method (generally considered more accurate than the weighted-average method) differs from the weighted-average method in two ways: 1. The computation […]

Accounting Chapter 08 1 Sulema Inc Repairs And Refinishes Antique

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1. A company has a standard cost system in which fixed and variable manufacturing overhead costs are applied to products […]

Accounting Chapter 08 1 When The Actual Amount Raw Material

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1. If the actual quantity of materials used is less than the standard quantity of materials allowed for the actual […]

Accounting Chapter 08 2 Semaan Corporation Applies Manufacturing Overhead Products

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 29. Semaan Corporation applies manufacturing overhead to products on the basis of standard machine-hours. Budgeted and actual overhead costs for […]

Accounting Chapter 08 2 Widman Inc Makes And Sells Only

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 31. Widman, Inc. makes and sells only one product and uses standard costing. The standard cost sheet for one unit […]

Accounting Chapter 08 3 Cafferty Corporation Has Provided The Following

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 47. Cafferty Corporation has provided the following data concerning its direct labor costs for March: Standard wage rate $12.80 per […]

Accounting Chapter 08 3 The Dillon Corporation Makes And Sells

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 46. The Dillon Corporation makes and sells a single product. Overhead costs are applied on the basis of standard direct […]

Accounting Chapter 08 4 Pohl Corporation Uses Standard Cost System

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. SH = 13,000 units × 1.4 machine-hours per unit = 18,200 machine-hours SR = ($10,000) ÷ 20,000 machine-hours = $0.50 […]

Accounting Chapter 08 5 Manufacturer Playground Equipment Uses Standard Costing

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 72. A manufacturer of playground equipment uses a standard costing system in which standard machine-hours (MHs) is the measure of […]

Accounting Chapter 08 7 Nova Corporation Produces Single Product And

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. App8A-120 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 08-01 Prepare a flexible budget. […]

Accounting Chapter 1 1 Country Charm Restaurant Open Hours Day

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1. Selling costs can be either direct or indirect costs. TRUE AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: FN […]

Accounting Chapter 1 2 The Cost Direct Materials Cost Classified

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Remember Learning Objective: 01-03 Understand cost […]

Accounting Chapter 1 3 The Following Data Pertains Activity And

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 73. The following data pertains to activity and costs for two months: June July Activity level in units 10,000 12,000 […]

Accounting Chapter 1 4 Gambino Corporation Wholesaler That Sells Single

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 88. Gambino Corporation is a wholesaler that sells a single product. Management has provided the following cost data for two […]

Accounting Chapter 1 5 Management Lewallen Corporation Has Asked Your

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 104. Management of Lewallen Corporation has asked your help as an intern in preparing some key reports for September. Direct […]

Accounting Chapter 10 1 Measurement feed back keep The Computer sell The Computer Differential annual Operating

File: 7e_BGN_CH10_TB, Chapter 10, Differential Analysis: The Key to Decision Making True/False [QUESTION] 1. Only future costs that differ between alternatives are relevant in decision making. [QUESTION] 2. Future costs that do not differ between the alternatives in a decision […]

Accounting Chapter 10 2 Variable Expenses contribution Margin traceable Fixed Expenses fixed Manufacturing Expenses fixed

58. Part S00 is used in one of Morsey Corporation’s products. The company makes 6,000 units of this part each year. The company’s Accounting Department reports the following costs of producing the part at this level of activity: Per Unit […]

Accounting Chapter 10 3 Direct Labor Variable Cost question Talbot Chooses Buy

[QUESTION] 89. What is the differential cost of Alternative B over Alternative A, including all of the relevant costs? A) $150,000 B) $100,000 C) $125,000 D) $50,000 90. The sunk cost in this situation is: A) $40,000 B) $750,000 C) […]

Accounting Chapter 10 4 Contribution Margin Per Unit The Constrained

122. How much will the company’s profits be increased or (decreased) if it prices the 100 units at $7 each? A) $(30) B) $150 C) $0 D) $310 Answer: B Level of Difficulty: 2 Medium Learning Objective: 10–04 Topic Area: […]

Accounting Chapter 10 5 What would be the effect on the company’s overall net operating

Level of Difficulty: 1 Easy Learning Objective: 10–02 Topic Area: Blooms: Apply AACSB: Analytical Thinking AICPA BB: Critical Thinking AICPA FN: Measurement [QUESTION] 157. The management of Leinberger Corporation is considering dropping product S48J. Data from the company’s accounting system […]

Accounting Chapter 10 6 How Many Minutes Mixing Machine Time Would

Manufacturing $294,400 Selling and administrative $94,720 The company has just received a special one-time order for 1,200 trophies at $61 each. For this particular order, no variable selling and administrative costs would be incurred. This order would also have no […]

Accounting Chapter 11 1 Computing The Present Value Future Dollars Known

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1. The present value of a given amount increases as the number of years over which it is to be […]

Accounting Chapter 11 1 Which The Following Will Have The

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1. In the payback method, depreciation is deducted from net operating income when computing the annual net cash flow. FALSE […]

Accounting Chapter 11 2 Beaver Corporation Investigating The Purchase New

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 31. Beaver Corporation is investigating the purchase of a new threading machine that costs $18,000. The machine would save about […]

Accounting Chapter 11 3 The Management Cantell Corporation Considering Project

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 54. The management of Cantell Corporation is considering a project that would require an initial investment of $47,000. No other […]

Accounting Chapter 11 4 Jimbas Inc Has Purchased New Donut

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 11-04 Compute the simple rate of […]

Accounting Chapter 11 5 Westland College Has Telephone System That

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 89. Westland College has a telephone system that is in poor condition. The system either can be overhauled or replaced […]

Accounting Chapter 11 6 Burba Inc Considering Investing Project That

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 11-101 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 11-02 Evaluate the acceptability of […]

Accounting Chapter 11 7 Mark Stevens Considering Opening Hobby And

11-113 112. Mark Stevens is considering opening a hobby and craft store. He would invest $50,000 to purchase equipment and furnishings and another $100,000 for inventories and other working capital needs. Rent on the building used by the business will […]

Accounting Chapter 12 1 During The Year The Balance The Accounts

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1. Under the direct method of determining the net cash provided by operating activities on the statement of cash flows, […]

Accounting Chapter 12 1 Statement Cash Flows The Sale Long term

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1. Collecting the principal on a loan to another company would be reported on the investing activities section of the […]

Accounting Chapter 12 2 Cash Dividends Were 12 The Company Did

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Cash dividends were $12. The company did not retire or sell any property, plant, and equipment during the year. The […]

Accounting Chapter 12 3 The Change Each Kendall Corporations Balance

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Financing activities: Repaying principal on bonds payable ($71 – $100) ($29) Issuance of common stock ($32 – $30) 2 Paying […]

Accounting Chapter 12 4 Van Beeber Corporations Comparative Balance Sheet

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 43. Van Beeber Corporation’s comparative balance sheet and income statement for last year appear below: Comparative Balance Sheet Ending Balance […]

Accounting Chapter 12 5 The Changes Each Balance Sheet Account

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 12–78 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 12-04 (Appendix 12A) Use the […]

Accounting Chapter 12 8 The Most Recent Comparative Balance Sheet

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 119. The most recent comparative balance sheet of Giacomelli Corporation appears below: Ending Balance Beginning Balance Assets: Current assets: Cash […]

Accounting Chapter 12 9 Burns Corporations Net Income Last Year

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Net income $126 Adjustments to convert net income to a cash basis: Depreciation ($206 – $172) $34 Decrease in accounts […]

Accounting Chapter 13 1 Selling Used Equipment Book Value For

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1. Vertical analysis of financial statements is accomplished by preparing common-size statements. TRUE AACSB: Reflective Thinking AICPA: BB Critical Thinking […]

Accounting Chapter 13 10 deacon corporation has provided the following financial

13-181 189. Mahoe Corporation has provided the following financial data: Balance Sheet December 31, Year 2 and Year 1 Assets Year 2 Year 1 Current assets: Cash $105,000 $190,000 Accounts receivable 255,000 220,000 Inventory 206,000 200,000 Prepaid expenses 44,000 50,000 […]

Accounting Chapter 13 11 Net Income 36500 Dividends Common Stock During

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Net income $36,500 Dividends on common stock during Year 2 totaled $4,500. The market price of common stock at the […]

Accounting Chapter 13 12 Kearin Corporation Has Provided The Following

13-221 217. Kearin Corporation has provided the following financial data: Balance Sheet December 31, Year 2 and Year 1 Assets Year 2 Year 1 Current assets: Cash $33,000 $100,000 Accounts receivable 281,000 250,000 Inventory 122,000 130,000 Prepaid expenses 68,000 80,000 […]

Accounting Chapter 13 13 Recher Corporations Common Stock Has Par

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 230. Recher Corporation’s common stock has a par value of $3 per share and has been stable at a total […]

Accounting Chapter 13 14 Wowk Corporation Has Provided The Following

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 13-02 Compute and interpret financial ratios […]

Accounting Chapter 13 15 Tworivers Inc Tri Manufactures Variety Consumer

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. *Average total assets = ($1,395,000 + $1,360,000) ÷ 2 = $1,377,500 **Average stockholders’ equity = ($981,000 + $960,000) ÷ 2 […]

Accounting Chapter 13 16 Berry The Managing Director Ltd Small

13-301 **Average stockholders’ equity = ($683,000 + $650,000) ÷ 2 = $666,500 m. Net profit margin percentage = Net income ÷ Sales = $37,000 ÷ $1,360,000 = 2.7% (rounded) n. Gross margin percentage = Gross margin ÷ Sales = $560,000 […]

Accounting Chapter 13 17 Gambino Corporation Has Provided The Following

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 269. Babbitt Corporation has provided the following data from its most recent income statement: Net operating income $94,000 Interest expense […]

Accounting Chapter 13 18 Times Interest Earned Net Operating Income Interest

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 13-341 a. Times interest earned = Net operating income ÷ Interest expense = $26,308 ÷ $14,000 = 1.88 (rounded) b. […]

Accounting Chapter 13 19 What is the company’s return on total assets for Year 2

13-358 Income taxes (35%) 14,862 Net income $27,600 Dividends on common stock during Year 2 totaled $5,600. The market price of common stock at the end of Year 2 was $5.60 per share. Required: a. What is the company’s net […]

Accounting Chapter 13 2 Accounts Receivable Turnover Will Normally Decrease

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Analyze Learning Objective: 13-02 Compute and […]

Accounting Chapter 13 3 Laverde Corporation Has Provided The Following

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 77. Laverde Corporation has provided the following data: Year 2 Year 1 Inventory $185,000 $200,000 Total assets $1,489,000 $1,470,000 Sales […]

Accounting Chapter 13 4 Broch Corporations Income Statement Appears Below

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 97. Broch Corporation’s income statement appears below: Income Statement Sales (all on account) $1,220,000 Cost of goods sold 760,000 Gross […]

Accounting Chapter 13 5 Tempel Corporation Has Provided The Following

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 117. Tempel Corporation has provided the following data: Year 2 Year 1 Common stock, $4 par value $240,000 $240,000 Total […]

Accounting Chapter 13 6 Dividends Common Stock During Year Totaled 7200

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Dividends on common stock during Year 2 totaled $7,200. The market price of common stock at the end of Year […]

Accounting Chapter 13 7 Net Income Before Taxes 136 Income Taxes

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Net income before taxes 136 Income taxes (30%) 41 Net income $95 The average collection period for Year 2 is […]

Accounting Chapter 13 8 Financial Statements For Maraby Corporation Appear

13-141 160. Financial statements for Maraby Corporation appear below: Maraby Corporation Balance Sheet December 31, Year 2 and Year 1 (dollars in thousands) Year 2 Year 1 Current assets: Cash and marketable securities $220 $190 Accounts receivable, net 190 160 […]

Accounting Chapter 13 9 Dahn Corporation Has Provided The Following

13-161 176. Dahn Corporation has provided the following financial data: Balance Sheet December 31, Year 2 and Year 1 Assets Year 2 Year 1 Current assets: Cash $227,000 $150,000 Accounts receivable 134,000 130,000 Inventory 150,000 130,000 Prepaid expenses 83,000 80,000 […]

Accounting Chapter 2 3 During October Dorinirl Corporation Incurred

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 48. During October, Dorinirl Corporation incurred $60,000 of direct labor costs and $5,000 of indirect labor costs. The journal entry […]

Accounting Chapter 2 5 Meyers Corporation Had The Following Inventory

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 85. Meyers Corporation had the following inventory balances at the beginning and end of November: November 1 November 30 Raw […]

Accounting Chapter 2 6 The credits to the Work in Process account as a consequence of the raw

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 104. On August 1, Shead Corporation had $35,000 of raw materials on hand. During the month, the company purchased an […]

Accounting Chapter 2 7 The Following Partially Completed T accounts Summarize

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 117. The following partially completed T-accounts summarize transactions for Farwest Corporation during the year: Raw Materials Beg Bal 4,700 10,000 […]

Accounting Chapter 2 8 Allenton Company Manufacturing Firm That Uses

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 129. Huckeby Corporation bases its predetermined overhead rate on the estimated machine– hours for the upcoming year. Data for the […]

Accounting Chapter 2 9 The Commonwealth Company Uses Job order Costing

2-158 137. The Commonwealth Company uses a job-order costing system and applies manufacturing overhead cost to jobs using a predetermined overhead rate based on the cost of materials used in production. At the beginning of the year, the following estimates […]

Accounting Chapter 3 1 Which The Following Would Classified Product level

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1. Direct labor is an appropriate allocation base for overhead when overhead costs and direct labor are highly correlated. TRUE […]

Accounting Chapter 3 10 activity-based costing system with the following activity cost pools

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 106. Olide, Inc., manufactures and sells two products: Product B9 and Product C8. The annual production and sales of Product […]

Accounting Chapter 3 11 Hypochondriac has decided to switch to an activity based costing

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 114. Aboud, Inc., manufactures and sells two products: Product Q6 and Product Z7. Data concerning the expected production of each […]

Accounting Chapter 3 12 required to produce that output appear below

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. A. $72.50 per DLH B. $238.33 per DLH C. $15.23 per DLH D. $48.33 per DLH Activity rate = Estimated […]

Accounting Chapter 3 13 If the company allocates all of its overhead based on direct labor-hours

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Overhead cost per unit (a) ÷ (b) $756.23 Computation of unit product costs under activity-based costing. Product O8 Direct materials […]

Accounting Chapter 3 14 Adams Company Has Two Products And

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 3-261 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 03-02 Compute activity rates for […]

Accounting Chapter 3 15 the overhead assigned to each unit of Product G5 would be closest to

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 3-281 Activity Cost Pools (a) Estimated Overhead Cost (b) Total Expected Activity (a) ÷ (b) Activity Rate Labor-related $205,296 4,200 […]

Accounting Chapter 3 16 Paolello Inc Manufactures And Sells Two

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. B. $98.72 per unit C. $534.24 per unit D. $314.56 per unit Predetermined overhead rate = Estimated total overhead ÷ […]

Accounting Chapter 3 17 if the company allocates all of its overhead based

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 3-321 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 03-02 Compute activity rates for […]

Accounting Chapter 3 18 estimated expected activity activity cost pools activity

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 169. Brenneis, Inc., manufactures and sells two products: Product T9 and Product T2. Data concerning the expected production of each […]

Accounting Chapter 3 19 Swimm Company allocates materials handling cost

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 177. Betenbaugh, Inc., manufactures and sells two products: Product E4 and Product L8. Data concerning the expected production of each […]

Accounting Chapter 3 2 The company is considering adopting an activity-based costing system

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 37. Marchan, Inc., manufactures and sells two products: Product K1 and Product S6. Data concerning the expected production of each […]

Accounting Chapter 3 20 data concerning the expected production of each product and

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 185. Mellencamp, Inc., manufactures and sells two products: Product A3 and Product Y6. Data concerning the expected production of each […]

Accounting Chapter 3 21 Computation Activity Rates Activity Cost Pools A

3-401 Computation of activity rates: Activity Cost Pools (a) Estimated Overhead Cost (b) Total Expected Activity (a) ÷ (b) Activity Rate Labor-related $235,536 11,200 DLHs $21.03 per DLH Production orders $27,234 900 orders $30.26 per order General factory $173,180 7,000 […]

Accounting Chapter 3 22 Meiler Inc Manufactures And Sells Two

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Computation of unit product costs under activity-based costing. Product O5 Product F4 Direct materials $164.00 $139.80 Direct labor: Product O5: […]

Accounting Chapter 3 23 Ermitanio Inc Manufactures And Sells Two

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 3-441 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 03-02 Compute activity rates for […]

Accounting Chapter 3 24 The company currently uses a traditional costing method

3-461 Required: In all computations involving dollars in the following requirements, round off your answer to the nearest whole cent. a. The company currently uses a traditional costing method in which overhead is applied to products based solely on direct […]

Accounting Chapter 3 25 Required All Computations Involving Dollars The Following

3-481 Required: In all computations involving dollars in the following requirements, round off your answer to the nearest whole cent. a. Determine the unit product cost of each product under the company’s traditional costing method. b. Determine the unit product […]

Accounting Chapter 3 26 Hammer Inc Manufactures And Sells Two

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Relative to the activity-based costing system, the traditional costing system undercosts the job by $162.50 3-497 AACSB: Analytical Thinking AICPA: […]

Accounting Chapter 3 3 Dobles Corporation has provided the following data from its activity-based

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 48. Randolph, Inc., manufactures and sells two products: Product T5 and Product Y7. Data concerning the expected production of each […]

Accounting Chapter 3 4 Pat Company Uses Activity based Costing The

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 3-61 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 03-02 Compute activity rates for […]

Accounting Chapter 3 5 Activity Cost Pools A Estimated Overhead Cost

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 3-81 Activity Cost Pools (a) Estimated Overhead Cost (b) Total Expected Activity (a) ÷ (b) Activity Rate Labor-related $321,724 9,200 […]

Accounting Chapter 3 6 Trisdale Inc Manufactures And Sells Two

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 68. Trisdale, Inc., manufactures and sells two products: Product V5 and Product X3. Data concerning the expected production of each […]

Accounting Chapter 3 7 concerning the expected production of each product and the expected

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Predetermined overhead rate = Estimated total overhead ÷ Total direct labor-hours = $475,248 ÷ 2,300 DLHs = $206.63 per DLH […]

Accounting Chapter 3 8 the direct materials cost per unit is

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. A. $49.30 per MH B. $80.93 per MH C. $62.33 per MH D. $90.98 per MH Activity rate = Estimated […]

Accounting Chapter 3 9 The activity rate for the batch setup activity cost pool is closest to

3-161 D. $1,146.32 per unit Computation of activity rates: Activity Cost Pools (a) Estimated Overhead Cost (b) Total Expected Activity (a) ÷ (b) Activity Rate Labor-related $598,016 12,800 DLHs $46.72 per DLH Machine setups $12,024 900 setups $13.36 per setup […]

Accounting Chapter 4 1 Pulo Corporation Uses Weighted average Process Costing

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1. When materials are purchased in a process costing system, a materials account is debited with the cost of the […]

Accounting Chapter 4 2 paxton corporation uses the weighted-average method

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 4-21 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 04-02 Compute the equivalent units […]

Accounting Chapter 4 3 February One The Processing Departments Manger

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 45. In February, one of the processing departments at Manger Corporation had beginning work in process inventory of $25,000 and […]

Accounting Chapter 4 4 Evans Corporation Uses The Weighted average Method

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 58. Evans Corporation uses the weighted-average method in its process costing system. This month, the beginning inventory in the first […]

Accounting Chapter 4 5 Percent complete with respect to conversion

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 68. Lumb Corporation uses the weighted-average method in its process costing system. Data concerning the first processing department for the […]

Accounting Chapter 4 6 data concerning the first processing department for the most recent

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 79. Kuzuck Corporation uses the weighted-average method in its process costing system. Data concerning the first processing department for the […]

Accounting Chapter 4 7 Carmon Corporation Uses The Weighted average Method

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 89. Carmon Corporation uses the weighted-average method in its process costing system. This month, the beginning inventory in the first […]

Accounting Chapter 4 8 The Following Information Relates The Assembly

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 99. The following information relates to the Assembly Department of Jataca Corporation for the month of November. Jataca uses a […]

Accounting Chapter 4 9 Able Inc Uses The Weighted average Method

4-161 113. Able Inc. uses the weighted-average method in its process costing system. The following data concern the operations of the company’s first processing department for a recent month. Work in process, beginning: Units in process 300 Percent complete with […]

Accounting Chapter 4s 1 Any difference in the equivalent units calculated under the weighted

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1. The equivalent units of production will be the same under the weighted-average and the FIFO method if there is […]

Accounting Chapter 4s 2 Index Corporation Uses The FIFO Method

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 22. Index Corporation uses the FIFO method in its process costing system. The first processing department, the Forming Department, started […]

Accounting Chapter 4s 3 Information About Units Processed And Processing

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 33. Information about units processed and processing costs incurred during a recent month in the Refining Department of a manufacturing […]

Accounting Chapter 4s 5 Conversion Complete Beginning Work Process Conversion 600

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Conversion To complete beginning work in process: Conversion: 600 units (100% – 10%) 540 Units started and completed 6,700 […]

Accounting Chapter 4s 6 Pushkin Corporation Uses The Fifo Method

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 63. Pushkin Corporation uses the FIFO method in its process costing system. Data concerning the first processing department for the […]

Accounting Chapter 4s 7 Darver Inc Uses The FIFO Method

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Conversion: 300 units 70% 210 Equivalent units of production 22,180 22,310 4S-121 AACSB: Analytical Thinking AICPA: BB Critical Thinking […]

Accounting Chapter 5 1 Contribution Margin The Amount Remaining After

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1. Incremental analysis is generally the most complicated and least direct approach to decision making. TRUE AACSB: Analytical Thinking AICPA: […]

Accounting Chapter 5 10 the product’s current sales are

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 175. Gauani Corporation produces and sells a single product. Data concerning that product appear below: Selling price per unit $150.00 […]

Accounting Chapter 5 2 Lepage Corporation has provided its contribution format

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 36. Lepage Corporation has provided its contribution format income statement for January. The company produces and sells a single product. […]

Accounting Chapter 5 3 Steeler Corporation Planning Sell 100000 Units

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 55. Steeler Corporation is planning to sell 100,000 units for $2.00 per unit and will break even at this level […]

Accounting Chapter 5 4 Renfrew Corporation has provided the following data concerning its only

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 75. A product sells for $10 per unit and has variable expenses of $6 per unit. Fixed expenses total $45,000 […]

Accounting Chapter 5 5 Lasseter Corporation Has Provided Its Contribution

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 94. Lasseter Corporation has provided its contribution format income statement for August. The company produces and sells a single product. […]

Accounting Chapter 5 6 Manufacturer Cedar Shingles Has Supplied The

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 112. A manufacturer of cedar shingles has supplied the following data: Bundles of cedar shakes produced and sold 280,000 Sales […]

Accounting Chapter 5 7 Boenisch Corporation Produces And Sells Single

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 5-121 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 05-04 Show the effects on […]

Accounting Chapter 5 8 Mcallister Corporation Has Provided The Following

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 143. Mcallister Corporation has provided the following data concerning its only product: Selling price $150 per unit Current sales 39,900 […]

Accounting Chapter 5 9 Education data Concerning Sumter Corporations Single Product Appear

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 5-161 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 05-04 Show the effects on […]

Accounting Chapter 6 1 Routsong Corporation Had The Following Sales

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1. Under variable costing, product costs consist of direct materials, direct labor, and variable manufacturing overhead. TRUE AACSB: Reflective Thinking […]

Accounting Chapter 6 10 During Its First Year Operations Carlos

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 6-181 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 06-01 Explain how variable costing […]

Accounting Chapter 6 11 Romasanta Corporation Manufactures Single Product The

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 158. Romasanta Corporation manufactures a single product. The following data pertain to the company’s operations over the last two years: […]

Accounting Chapter 6 12 Oneill Incorporated’s Segmented Income Statement For

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 173. O’Neill, Incorporated’s segmented income statement for the most recent month is given below. Total Company Store A Store B […]

Accounting Chapter 6 13 Keefe Corporation Has Two Divisions Western

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 6-241 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 06-05 Compute companywide and segment […]

Accounting Chapter 6 14 Sproull Inc Which Produces Single Product

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 206. Ivancevic Inc., which produces a single product, has provided the following data for its most recent month of operation: […]

Accounting Chapter 6 15 Qabar Corporation Which Has Only One

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Variable selling and administrative ($7 per unit × 8,200 units) $57,400 Fixed selling and administrative 106,600 164,000 Net operating income […]

Accounting Chapter 6 16 Walkenhorst Corporation Has Two Divisions Bulb

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 224. Pen Corporation manufactures a single product. Last year, the company’s variable costing net operating income was $55,700 and ending […]

Accounting Chapter 6 17 Minick Corporation Has Two Divisions Grocery

6-312 232. Minick Corporation has two divisions: Grocery Division and Convenience Division. The following report is for the most recent operating period: Total Company Grocery Division Convenience Division Sales $572,000 $222,000 $350,000 Variable expenses 178,940 59,940 119,000 Contribution margin 393,060 […]

Accounting Chapter 6 2 National Retail Company Has Segmented Its

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Understand Learning Objective: 06-04 Prepare a […]

Accounting Chapter 6 3 Manufacturing Company That Produces Single Product

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 56. A manufacturing company that produces a single product has provided the following data concerning its most recent month of […]

Accounting Chapter 6 6 Jarvix Corporation Which Has Only One

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 99. Jarvix Corporation, which has only one product, has provided the following data concerning its most recent month of operations: […]

Accounting Chapter 6 7 the company’s variable costs per unit and total fixed

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 6-121 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 06-01 Explain how variable costing […]

Accounting Chapter 6 8 Aaker Corporation Which Has Only One

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 120. Aaker Corporation, which has only one product, has provided the following data concerning its most recent month of operations: […]

Accounting Chapter 6 9 Yankee Corporation Manufactures Single Product The

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 130. Yankee Corporation manufactures a single product. The company has the following cost structure: Variable costs per unit: Production $4 […]

Accounting Chapter 7 1 Which The Following Budgets Are Prepared

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1. The cash budget is usually prepared after the budgeted income statement. FALSE AACSB: Reflective Thinking AICPA: BB Critical Thinking […]

Accounting Chapter 7 3 Sparks Corporation Has Cash Balance 7500

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 71. Sparks Corporation has a cash balance of $7,500 on April 1. The company must maintain a minimum cash balance […]

Accounting Chapter 7 4 Dilbert Farm Supply Located Small Town

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 87. Dilbert Farm Supply is located in a small town in the rural west. Data regarding the store’s operations follow: […]

Accounting Chapter 7 5 Noel Enterprises Has Budgeted Sales Units

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 103. Noel Enterprises has budgeted sales in units for the next five months as follows: June 6,800 units July 5,400 […]

Accounting Chapter 7 6 The Covey Corporation Preparing Its Manufacturing

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 127. The Covey Corporation is preparing its Manufacturing Overhead Budget for the fourth quarter of the year. The budgeted variable […]

Accounting Chapter 7 8 The Fraley Corporation Merchandising Firm Has

7-136 159. The Fraley Corporation, a merchandising firm, has planned the following sales for the next four months: March April May June Total budgeted sales $50,000 $70,000 $90,000 $60,000 Sales are made 40% for cash and 60% on account. From […]

Accounting Chapter 8 1 Major Weakness Flexible Budgets That They

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1. A planning budget is prepared before the period begins and is valid for whatever the actual level of activity […]

Accounting Chapter 8 10 tabeling corporation manufactures and sells a single product

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. D. $11,400 Revenue per tenant-day $32.10 Total variable expense per tenant-day 22.10 Contribution margin per tenant-day $10.00 Total fixed expense […]

Accounting Chapter 8 11 Buonocore Clinic Uses Client visits Its Measure

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Actual results $132,124 Flexible budget ($46.20 × 2,770) 127,974 Revenue variance $4,150 Because the actual revenue is greater than the […]

Accounting Chapter 8 12 the clinic has provided the following data concerning the formulas

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Actual results $18,048 Flexible budget [$12,100 + ($1.70 × 3,040)] 17,268 Spending variance $780 Because the actual expense is greater […]

Accounting Chapter 8 13 Perla Kennel Uses Tenant days Its Measure

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. C. $18,568 D. $18,408 Cost = Fixed cost + (Variable cost per unit × q) = $2,800 + ($7.30 × […]

Accounting Chapter 8 14 Wesolick Clinic Uses Client visits Its Measure