Problem 6-18B (45 minutes)

1. a. The unit product cost under absorption costing is:

Direct materials ………………………………

$17

Direct labor ……………………………………

8

Variable manufacturing overhead ……….

1

Fixed manufacturing overhead

($882,000 ÷ 49,000 units) ……………..

18

Absorption costing unit product cost ……

$44

b. The absorption costing income statement is:

Sales (44,000 units × $78 per unit) ………………………

$3,432,000

Cost of goods sold (44,000 units × $44 per unit) …….

1,936,000

Gross margin …………………………………………………..

1,496,000

Selling and administrative expenses

(44,000 units × $3 per unit) + $563,000 ……………..

695,000

Net operating income ………………………………………..

$ 801,000

2. a. The unit product cost under variable costing is:

Direct materials ………………………………

$17

Direct labor ……………………………………

8

Variable manufacturing overhead ……….

1

Variable costing unit product cost ……….

$26

b. The variable costing income statement is:

Sales (44,000 units × $78 per unit) …………..

$3,432,000

Variable expenses:

Variable cost of goods sold

(44,000 units × $26 per unit) ………………

$1,144,000

Variable selling expense

(44,000 units × $3 per unit) ……………….

132,000

1,276,000

Contribution margin ……………………………….

2,156,000

Fixed expenses:

Fixed manufacturing overhead ……………….

882,000

Fixed selling and administrative expense ….

563,000

1,445,000

Net operating loss …………………………………

$ 711,000)

Problem 6-18B (continued)

3. The difference in the ending inventory relates to a difference in the

handling of fixed manufacturing overhead costs. Under variable costing,

these costs have been expensed in full as period costs. Under

absorption costing, these costs have been added to units of product at

(2) above.

Problem 6-19B (45 minutes)

1. The break-even point in units sold can be computed using the

contribution margin per unit as follows:

Selling price per unit …………………

$52

Variable cost per unit ………………..

44

Contribution margin per unit ………

$ 8

Break-even unit sales = Fixed expenses ÷ Unit contribution margin

= $480,000 ÷ $8 per unit

= 60,000 units

2 a. Under variable costing, only the variable manufacturing costs are

included in product costs.

Year 1

Year 2

Year 3

Direct materials ………………………………

$22

$22

$22

Direct labor …………………………..……….

14

14

14

Variable manufacturing overhead ……….

5

5

5

Variable costing unit product cost ……….

$41

$41

$41

Note that selling and administrative expenses are not treated as

product costs; that is, they are not included in the costs that are

inventoried. These expenses are always treated as period costs.

Problem 6-19B (continued)

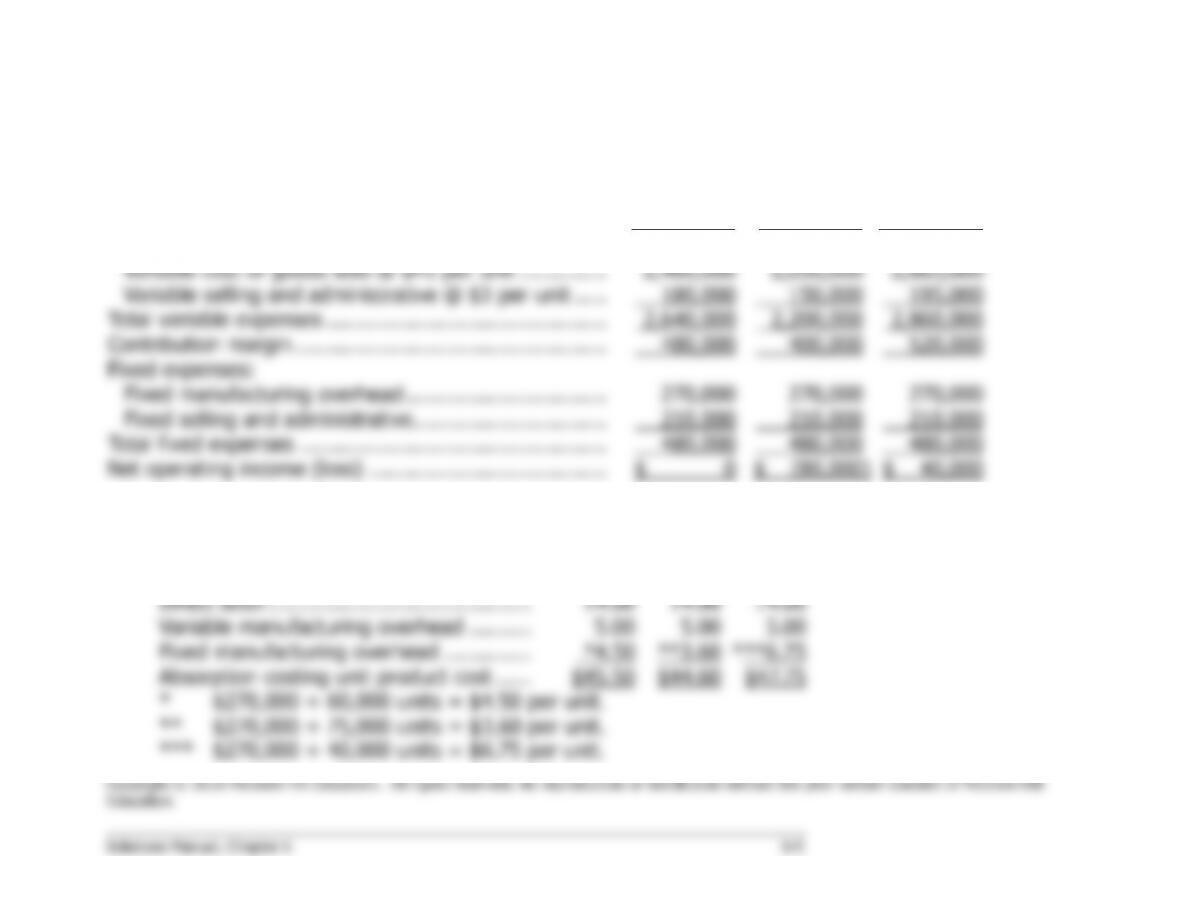

2. b. The variable costing income statements appear below:

Year 1

Year 2

Year 3

Sales ………………………………………………………………

$3,120,000

$2,600,000

$3,380,000

Variable expenses:

Variable cost of goods sold @ $41 per unit …………..

2,460,000

2,050,000

2,665,000

Variable selling and administrative @ $3 per unit …..

180,000

150,000

195,000

Total variable expenses ………………………………………

2,640,000

2,200,000

2,860,000

Contribution margin …………………………………………..

480,000

400,000

520,000

Fixed expenses:

Fixed manufacturing overhead …………………………..

270,000

270,000

270,000

Fixed selling and administrative ………………………….

210,000

210,000

210,000

Total fixed expenses ………………………………………….

480,000

480,000

480,000

Net operating income (loss) ………………………………..

$ 0

$ (80,000)

$ 40,000

3. a. The unit product costs under absorption costing:

Year 1

Year 2

Year 3

Direct materials ………………………………

$22.00

$22.00

$22.00

Direct labor …………………………..……….

14.00

14.00

14.00

Variable manufacturing overhead ……….

5.00

5.00

5.00

Fixed manufacturing overhead …………..

*4.50

**3.60

***6.75

Absorption costing unit product cost ……

$45.50

$44.60

$47.75

* $270,000 ÷ 60,000 units = $4.50 per unit.

** $270,000 ÷ 75,000 units = $3.60 per unit.

*** $270,000 ÷ 40,000 units = $6.75 per unit.

Problem 6-19B (continued)

3. b. The absorption costing income statements appears below:

Year 1

Year 2

Year 3

Sales ……………………………………………..

$3,120,000

$2,600,000

$3,380,000

Cost of goods sold…………………………….

2,730,000

2,230,000

3,025,000

Gross margin …………………………………..

390,000

370,000

355,000

Selling and administrative expenses ……..

390,000

360,000

405,000

Net operating income (loss) ………………..

$ 0

$ 10,000

$ (50,000)

Cost of goods sold computations:

Year 1: 60,000 units × $45.50 per unit = $2,730,000

Year 2: 50,000 units × $44.60 per unit = $2,230,000

Year 3: (25,000 × $44.60 per unit) + (40,000 × $47.75 per unit) = $3,025,000

4.

Year 1

Year 2

Year 3

Units sold …………………………………………………..

60,000

50,000

65,000

Break-even point in units ……………………………….

60,000

60,000

60,000

Units above (below) break-even point ………………

0

(10,000)

5,000

Variable costing net operating income (loss) ………

$0

$(80,000)

$ 40,000

Absorption costing net operating income (loss) …..

$0

$ 10,000

$(50,000)

The absorption costing net operating incomes in years 2 and 3 are counterintuitive. In year 2, the

number of units sold is below the break-even point; however, absorption costing reports a net

operating income greater than zero. In year 3, the number of units sold is above the break-even

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw–Hill

Education.

Solutions Manual, Chapter 6 6-7

point; however, absorption costing reports a net operating income less than zero.

Sales …………………………………………………

Variable expenses:

Total variable expenses ………………………….

Contribution margin ………………………………

Fixed expenses:

Total fixed expenses ……………………………..

Net operating income (loss) ……………………

Variable costing net operating income (loss)

Absorption costing net operating income …..

Problem 6-20B (30 minutes)

1. The unit product cost under the variable costing is computed as follows:

Direct materials ………………………………

$ 7

Direct labor ……………………………………

12

Variable manufacturing overhead ……….

2

Variable costing unit product cost ……….

$21

Problem 6-21B (45 minutes)

1.

a. and b.

Absorption

Costing

Variable

Costing

Direct materials ………………………………

$ 83

$83

Variable manufacturing overhead ……….

5

5

Fixed manufacturing overhead

($252,000 ÷ 4,000 units) ……………….

63

—

Unit product cost …………………………....

$151

$88

2. Absorption costing income statement:

Sales (3,200 units × $340 per unit) ………………….

$1,088,000

Cost of goods sold (3,200 units × $151 per unit) …

483,200

Gross margin ……………………………………………….

604,800

Selling and administrative expenses

(8% × $1,088,000 + $158,000) ……………………

245,040

Net operating income ……………………………………

$ 359,760

3. Variable costing income statement:

Sales (3,200 units × $340 per unit) ………

$1,088,000

Variable expenses:

Variable cost of goods sold (3,200 units

× $88 per unit) …………………………..

$281,600

Variable selling and administrative

expense ($1,088,000 × 8%) …………..

87,040

368,640

Contribution margin …………………………..

719,360

Fixed expenses:

Fixed manufacturing overhead …………..

252,000

Fixed selling and administrative …………

158,000

410,000

Net operating income ………………………..

$309,360)

Problem 6-21B (continued)

4. A manager may prefer to take the statement prepared under the

absorption approach in part (2), because it shows a higher profit for the

5.

Variable costing net operating income …………………………...

$ 309,360)

Add fixed manufacturing overhead cost deferred in

inventory under absorption costing (800 units × $63 per

unit) …………………………………………………………………….

50,400

Absorption costing net operating income ………………………..

$359,760

Problem 6-22B (45 minutes)

1.

a. and b.

Absorption

Costing

Variable

Costing

Direct materials ………………………………

$ 3

$ 3

Direct labor ……………………………………

12

12

Variable manufacturing overhead ……….

3

3

Fixed manufacturing overhead

($120,000 ÷ 24,000 units) ……………..

5

—

Unit product cost …………………………....

$23

$18

2.

May

June

Sales ………………………………………………….

$960,000

$1,344,000

Variable expenses:

Variable cost of goods sold @ $18 per unit .

360,000

504,000

Variable selling and administrative expense

@ $3 per unit ………………………………….

60,000

84,000

Total variable expenses …………………………..

420,000

588,000

Contribution margin ……………………………….

540,000

756,000

Fixed expenses:

Fixed manufacturing overhead ……………….

120,000

120,000

Fixed selling and administrative expenses …

166,000

166,000

Total fixed expenses ………………………………

286,000

286,000

Net operating income (loss) …………………….

$254,000)

$ 470,000

3.

May

June

Variable costing net operating income (loss)

$254,000)

$470,000

Add fixed manufacturing overhead cost

deferred in inventory under absorption

costing (4,000 units × $5 per unit) ………..

20,000

Deduct fixed manufacturing overhead cost

released from inventory under absorption

costing (4,000 units × $5 per unit) ………..

(20,000)

Absorption costing net operating income …..

$274,000

$450,000