Problem 5-25B (45 minutes)

1.

Sales (25,600 units × SFr92 per unit) ……………….

SFr2,355,200

Variable expenses

(25,600 units × SFr62 per unit) …………………….

1,587,200

Contribution margin ………………………………………

768,000

Fixed expenses …………………………………………….

831,000

Net operating loss ………………………………………..

SFr (63,000)

2.

Unit sales to break even

=

Fixed expenses

Unit contribution margin

=

SFr831,000

=

27,700 units

SFr30 per unit

3. See the next page.

4. At a selling price of SFr82 per unit, the contribution margin is SFr20 per

unit. Therefore:

Unit sales to break even

=

Fixed expenses

Unit contribution margin

=

SFr831,000

=

41,550 units

SFr20 per unit

41,550 units × SFr82 per unit = SFr3,407,100 to break even.

This break–even point is different from the break-even point in (2)

because of the change in selling price. With the change in selling price,

the unit contribution margin drops from SFr30 to SFr20, resulting in an

increase in the break-even point.

Problem 5-25B (continued)

3.

Unit

Selling

Price

Unit

Variable

Expense

Unit

Contribution

Margin

Volume

Total

Contribution

Margin

Fixed

Expenses

Net

Operating

Income

(SFrs)

(SFrs)

(SFrs)

(Units)

(SFrs)

(SFrs)

(SFrs)

92

62

30

25,600

768,000

831,000

(63,000)

90

62

28

30,600

856,800

831,000

25,800

88

62

26

35,600

925,600

831,000

94,600

86

62

24

40,600

974,400

831,000

143,400

84

62

22

45,600

1,003,200

831,000

172,200

82

62

20

50,600

1,012,000

831,000

181,000

80

62

18

55,600

1,000,800

831,000

169,800

Problem 5-26B (60 minutes)

1. The income statements would be:

Present

Amount

Per Unit

%

Sales …………………………

$1,218,000

$29.00

100%

Variable expenses …………

852,600

20.30

70%

Contribution margin ………

365,400

$ 8.70

30%

Fixed expenses …………….

292,320

Net operating income ……

$ 73,080

Proposed

Amount

Per Unit

%

Sales …………………………

$1,218,000

$29.00

100%

Variable expenses* ……….

487,200

11.6

40%

Contribution margin ………

730,800

$17.40

60%

Fixed expenses …………….

657,720

Net operating income ……

$ 73,080

*$20.30 – $8.70 = $11.60

2. a. Degree of operating leverage:

Present:

Degree of operating leverage

=

Contribution margin

Net operating income

=

$365,400

=

5

$73,080

Proposed:

Degree of operating leverage

=

Contribution margin

Net operating income

=

$730,800

=

10

$73,080

Problem 5-26B (continued)

2. b. Dollar sales to break even:

Present:

Dollar sales to break even

=

Fixed expenses

CM ratio

=

$292,320

=

$974,400

.30

Proposed:

Dollar sales to break even

=

Fixed expenses

CM ratio

=

$657,720

=

$1,096,200

.60

c. Margin of safety:

Present:

Margin of safety

=

Actual sales – Break-even sales

$1,218,000 – $974,400 = $243,600

Margin of safety percentage

=

Margin of safety

Actual sales

=

$243,600

=

20%

$1,218,000

Proposed:

Margin of safety

=

Actual sales – Break-even sales

$1,218,000 – $1,096,200 = $121,800

Margin of safety percentage

=

Margin of safety

Actual sales

=

$121,800

=

10%

$1,218,000

Problem 5-26B (continued)

3. The major factor would be the sensitivity of the company’s operations to

cyclical movements in the economy. Because the new equipment will

increase the CM ratio, in years of strong economic activity, the company

4. No information is given in the problem concerning the new variable

expenses or the new contribution margin ratio. Both of these items must

be determined before the new break-even point can be computed. The

computations are:

New variable expenses:

Profit

= (Sales − Variable expenses) − Fixed expenses

$91,350**

= ($1,827,000* – Variable expenses) – $365,400

Variable expenses

= $1,827,000 – $365,400 – $91,350

= $1,370,250

*

New level of sales: $1,218,000 × 1.5 = $1,827,000

**

New level of net operating income: $73,080 × 1.25 = $91,350

New CM ratio:

Sales ………………………………

$1,827,000

100%

Variable expenses ………………

1,370,250

75%

Contribution margin ……………

$ 456,750

25%

With the above data, the new break–even point can be computed:

Dollar sales to break even

=

Fixed expenses

CM ratio

=

$365,400

=

$1,416,600

.25

Problem 5-26B (continued)

The greatest risk is that the increases in sales and net operating income

predicted by the marketing manager will not happen and that sales will

remain at their present level. Note that the present level of sales is

Problem 5-27B (30 minutes)

1. The numbered components are as follows:

(1)

Dollars of revenue and costs.

(2)

Volume of output, expressed in units, % of capacity, sales,

or some other measure of activity.

(3)

Total expense line.

(4)

Variable expense area.

(5)

Fixed expense area.

(6)

Break-even point.

(7)

Loss area.

(8)

Profit area.

(9)

Revenue line.

2.

a.

Line 3:

Remain unchanged.

Line 9:

Have a flatter slope.

Break-even point:

Increase.

b.

Line 3:

Have a steeper slope.

Line 9:

Remain unchanged.

Break-even point:

Increase.

c.

Line 3:

Shift downward.

Line 9:

Remain unchanged.

Break-even point:

Decrease.

d.

Line 3:

Remain unchanged.

Line 9:

Remain unchanged.

Break-even point:

Remain unchanged.

e.

Line 3:

Shift upward and have a steeper slope.

Line 9:

Remain unchanged.

Break-even point:

Probably change, but the direction is

uncertain.

f.

Line 3:

Have a flatter slope.

Line 9:

Have a flatter slope.

Break-even point:

Remain unchanged in terms of units;

decrease in terms of total dollars of sales.

Problem 5-27B (continued)

g.

Line 3:

Shift downward.

Line 9:

Remain unchanged.

Break-even point:

Decrease.

h.

Line 3:

Shift upward and have a flatter slope.

Line 9:

Remain unchanged.

Break-even point:

Probably change, but the direction is

uncertain.

Problem 5-28B (60 minutes)

1.

Sales =

Variable expenses + Fixed expenses + Profits

$50.00Q =

$30.00Q + $90,000 + $0

$20.00Q =

$90,000

Q =

$90,000 ÷ $20.00 per pair

Q =

4,500 pairs

in dollar sales CM ratio 0.40

2. See the graph on the following page.

3.

Sales =

Variable expenses + Fixed expenses + Profits

$50.00Q =

$30.00Q + $90,000 + $25,000

$20.00Q =

$115,000

Q =

$115,000 ÷ $20.00 per pair

Q =

5,750 pairs

Incremental fixed salary cost ……………………………………

Increased net operating income …………………………..

Problem 5-28B (continued)

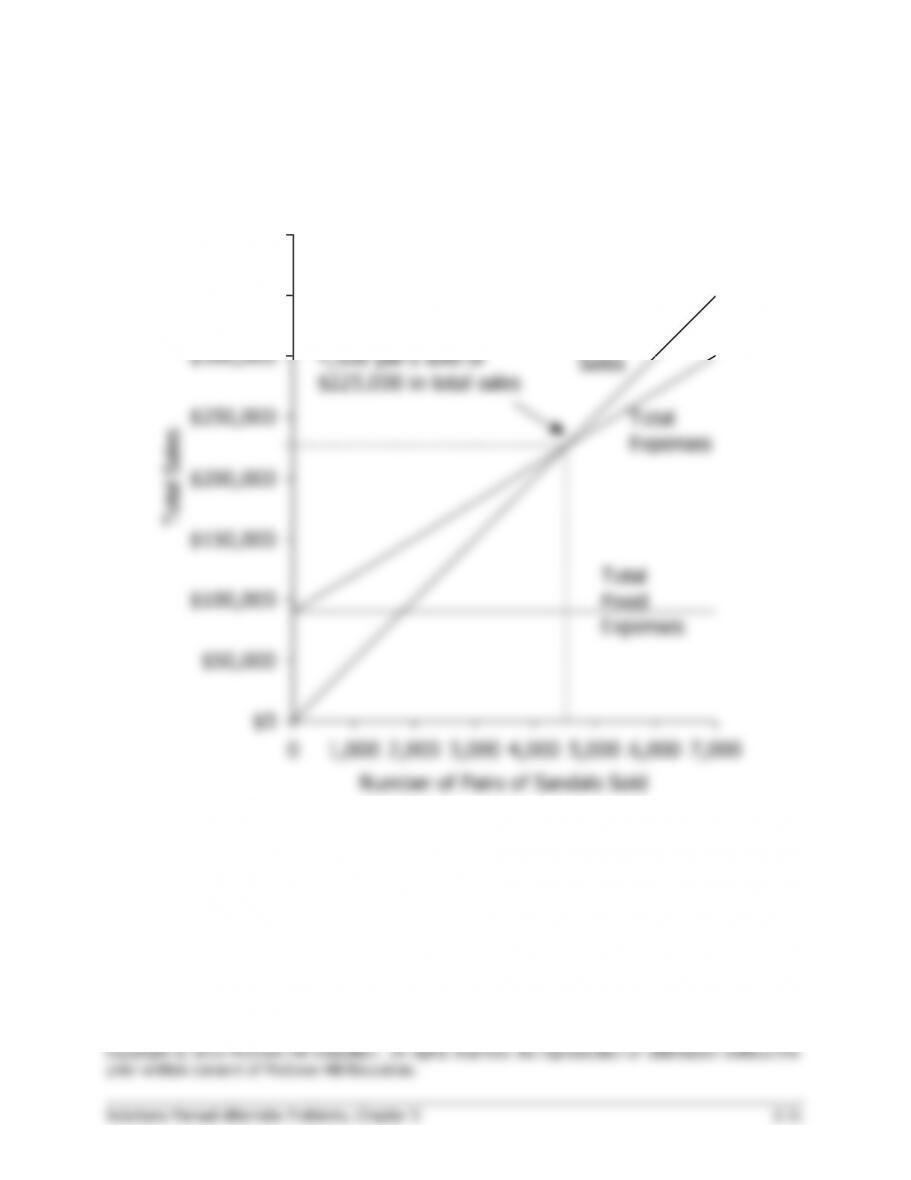

2. Cost-volume-profit graph:

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000

Number of Pairs of Sandals Sold

Total Sales

Break-Even Point:

4,500 pairs sold or

$225,000 in total sales

Total

Sales

Total

Expenses

Total

Fixed

Expenses