Problem 1-14B (45 minutes)

1.

House Of Pianos, Inc.

Traditional Income Statement

For the Month Ended September 30

Sales (60 pianos × $3,300 per piano) ……………..

$198,000

Cost of goods sold

(60 pianos × $1,492 per piano) …………………..

89,520

Gross margin …………………………………………….

108,480

Selling and administrative expenses:

Selling expenses:

Advertising …………………………………………..

$ 955

Delivery of pianos

(60 pianos × $61 per piano)…………………..

3,660

Sales salaries and commissions

[$4,823 + (4% × $198,000)] …………………

12,743

Utilities ………………………………………………..

633

Depreciation of sales facilities …………………..

4,944

Total selling expenses ……………………………….

22,935

Administrative expenses:

Executive salaries …………………………………..

13,490

Depreciation of office equipment ……………….

943

Clerical

[$2,499 + (60 pianos × $37 per piano)] …..

4,719

Insurance …………………………………………….

719

Total administrative expenses ……………………..

19,871

Total selling and administrative expenses …………

42,806

Net operating income ………………………………….

$ 65,674

1-2 Introduction to Managerial Accounting, 6th edition

Problem 1-14B (continued)

2.

House Of Pianos, Inc.

Contribution Format Income Statement

For the Month Ended September 30

Total

Per Unit

Sales (60 pianos × $3,300 per piano) ……………..

$198,000

$3,300

Variable expenses:

Cost of goods sold

(60 pianos × $1,492 per piano) ………………..

89,520

1,492

Delivery of pianos

(60 pianos × $61 per piano) …………………….

3,660

61

Sales commissions (4% × $198,000) ……………

7,920

132

Clerical (60 pianos × $37 per piano) …………….

2,220

37

Total variable expenses …………………………...

103,320

1,722

Contribution margin …………………………………….

94,680

$1,578

Fixed expenses:

Advertising ……………………………………………..

955

Sales salaries …………………………………………..

4,823

Utilities …………………………………………………..

633

Depreciation of sales facilities ……………………..

4,944

Executive salaries …………………………………….

13,490

Depreciation of office equipment …………………

943

Clerical …………………………………………………..

2,499

Insurance ……………………………………………….

719

Total fixed expenses ……………………………………

29,006

Net operating income ………………………………….

$ 65,674

3. Fixed costs remain constant in total but vary on a per unit basis with

changes in the activity level. For example, as the activity level increases,

Problem 1-15B (30 minutes)

1.

a.

11

b.

9

c.

3

d.

4

e.

1

f.

7

g.

10

h.

6

i.

2

2. Without an understanding of the underlying cost behavior patterns, it

would be difficult, if not impossible for a manager to properly analyze

1-4 Introduction to Managerial Accounting, 6th edition

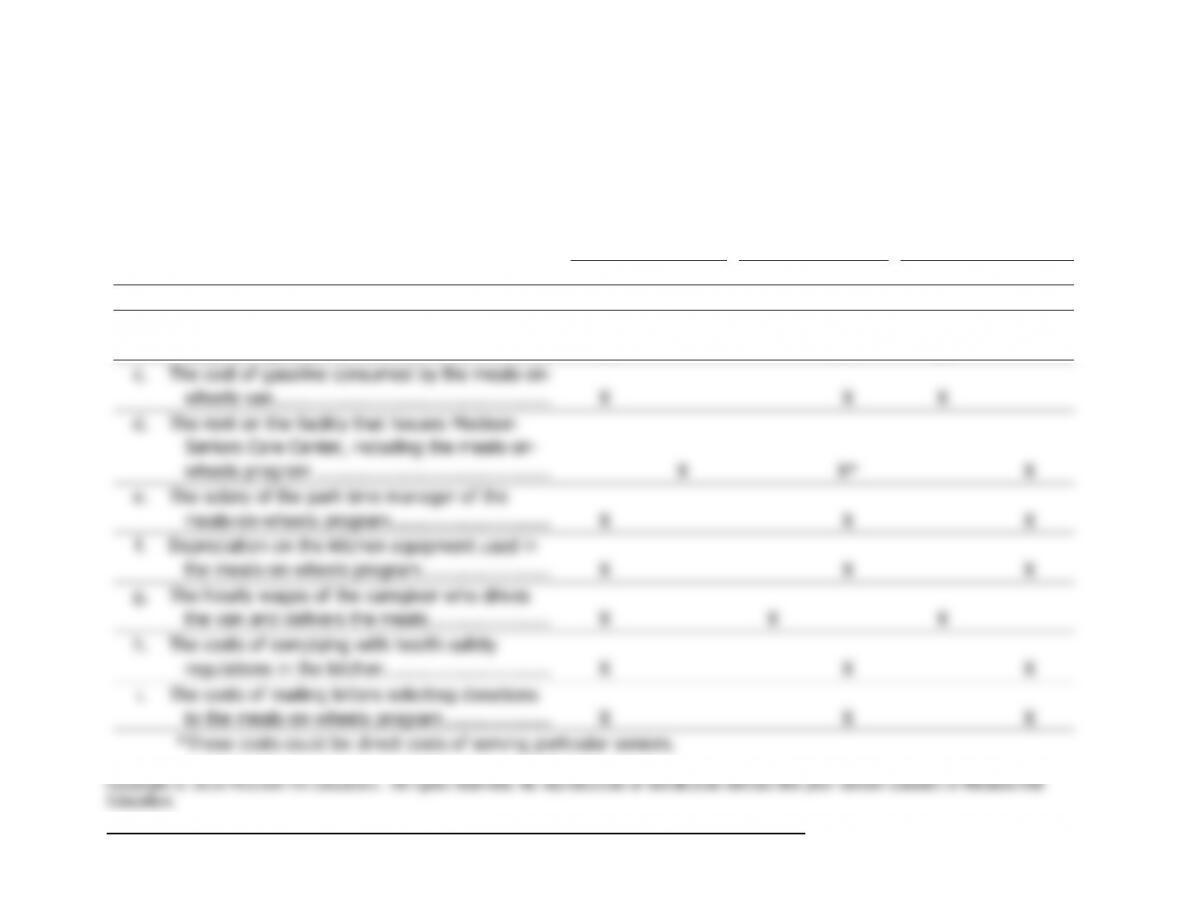

Problem 1-16B (20 minutes)

Direct or Indirect

Cost of the Meals-

On-Wheels

Program

Direct or Indirect

Cost of Particular

Seniors Served

by the Meals-On–

Wheels Program

Variable or Fixed

with Respect to the

Number of Seniors

Served by the

Meals-On-Wheels

Program

Item

Description

Direct

Indirect

Direct

Indirect

Variable

Fixed

a.

The cost of leasing the meals-on-wheels van …..

X

X

X

b.

The cost of incidental supplies such as salt,

pepper, napkins, and so on ……………………….

X

X*

X

c.

The cost of gasoline consumed by the meals-on–

wheels van …………………………………………….

X

X

X

d.

The rent on the facility that houses Madison

Seniors Care Center, including the meals–on–

wheels program ……………………………………..

X

X*

X

e.

The salary of the part-time manager of the

meals-on-wheels program …………………………

X

X

X

f.

Depreciation on the kitchen equipment used in

the meals-on-wheels program ……………………

X

X

X

g.

The hourly wages of the caregiver who drives

the van and delivers the meals …………………..

X

X

X

h.

The costs of complying with health safety

regulations in the kitchen ………………………….

X

X

X

i.

The costs of mailing letters soliciting donations

to the meals-on-wheels program ………………..

X

X

X

1-6 Introduction to Managerial Accounting, 6th edition

Problem 1-17B (30 minutes)

1. Maintenance cost at the 63,600 machine-hour level of activity can be

isolated as follows:

Level of Activity

47,700 MH

63,600 MH

Total factory overhead cost ..

248,560

pesos

277,180

pesos

Deduct:

Indirect materials @ 1.30

pesos per MH* ……………

62,010

82,680

Rent …………………………...

135,000

135,000

Maintenance cost …………….

51,550

pesos

59,500

pesos

2. High-low analysis of maintenance cost:

Machine-Hours

Maintenance Cost

High activity level …………..

63,600

59,500

pesos

Low activity level ……………

47,700

51,550

Change observed ……………

15,900

7,950

pesos

Variable

cost

=

Change in cost

=

7,950 pesos

=

0.50 peso

per MH

Change in activity

15,900 MHs

Fixed cost element:

Total cost at the low level of activity ……………….

51,550

pesos

Less variable cost element

(47,700 MHs × 0.50 pesos per MH) ………………

23,850

Fixed cost element ……………………………………..

27,700

pesos

Problem 1-17B (continued)

3. Total factory overhead cost at 52,470 machine-hours is:

Indirect materials (52,470 MHs ×

1.30 pesos per MH) …………………..

68,211

pesos

Rent …………………………………………

135,000

Maintenance:

Variable cost element (52,470 MHs

× 0.50 peso per MH) ……………….

26,235

pesos

Fixed cost element …………………….

27,700

53,935

Total factory overhead cost ……………

257,146

pesos

1-8 Introduction to Managerial Accounting, 6th edition

Problem 1-18B (45 minutes)

1.

Cost of goods sold ………………..

Variable

Shipping expense …………………

Mixed

Advertising expense ……………..

Fixed

Salaries and commissions ………

Mixed

Insurance expense ……………….

Fixed

Depreciation expense ……………

Fixed

2. Analysis of the mixed expenses:

Units

Shipping

Expense

Salaries and

Comm. Expense

High level of activity …..

4,800

£77,300

£218,400

Low level of activity ……

1,800

41,300

104,400

Change ……………………

3,000

£36,000

£114,000

Shipping

Expense

Salaries and

Comm. Expense

Cost at high level of activity …

£77,300

£218,400

Less variable cost element:

4,800 units × £12 per unit …

57,600

4,800 units × £38 per unit …

182,400

Fixed cost element …………….

£19,700

£ 36,000

Problem 1-18B (continued)

The cost formulas are:

3.

Arnall Ltd.

Income Statement

For the Month Ended June 30

Sales revenue ……………………………………..

£835,200

Variable expenses:

Cost of goods sold

(4,800 units × £67 per unit) ………………

£321,600

Shipping expense

(4,800 units × £12 per unit) ……………..

57,600

Salaries and commissions expense

(4,800 units × £38 per unit) ………………

182,400

561,600

Contribution margin ………………………………

273,600

Fixed expenses:

Shipping expense ………………………………

19,700

Advertising ……………………………………….

70,000

Salaries and commissions …………………….

36,000

Insurance …………………………………………

9,900

Depreciation ……………………………………..

42,300

177,900

Net operating income …………………………...

£ 95,700

1-10 Introduction to Managerial Accounting, 6th edition

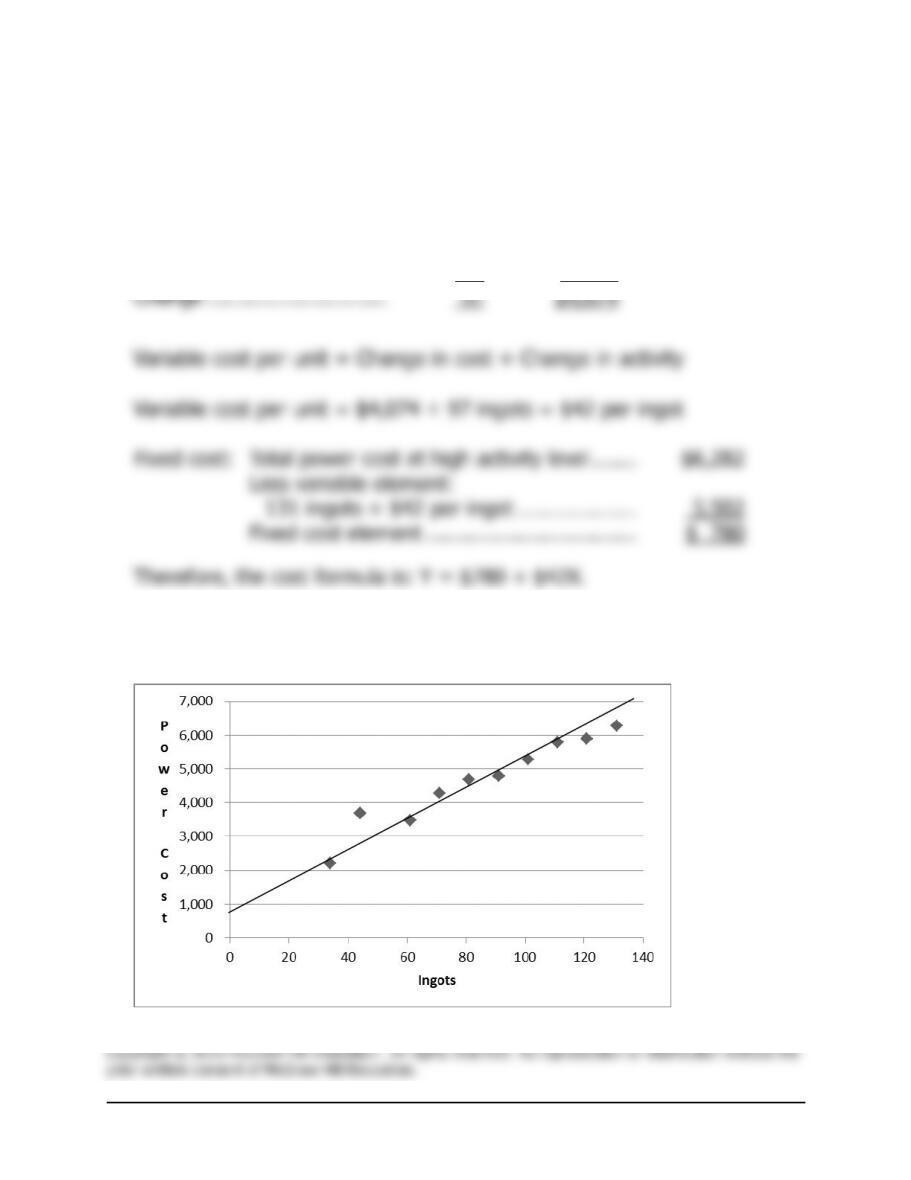

Problem 1-19B (45 minutes)

1. High-low method:

Number of

Ingots

Power

Cost

High activity level …………..

131

$6,282

Low activity level ……………

34

2,208

Change ………………………..

97

$4,074

Variable cost per unit = Change in cost ÷ Change in activity

Variable cost per unit = $4,074 ÷ 97 ingots = $42 per ingot

Fixed cost:

Total power cost at high activity level …….

$6,282

Less variable element:

131 ingots × $42 per ingot ……………….

5,502

Fixed cost element …………………………….

$ 780

Therefore, the cost formula is: Y = $780 + $42X.

2. Scattergraph with a straight line drawn through the high and low data

points:

Problem 1-19B (continued)

3. The high-low estimate of fixed costs is $658.20 (or $1,438.20 – $780.00)

$37.783) higher than the estimate provided by least-squares regression.

A straight line that minimized the sum of the squared errors would

Problem 1-20B (45 minutes)

1. Maintenance cost at the 73,000 machine-hour level of activity can be

isolated as follows:

Level of Activity

43,000 MH

73,000 MH

Total factory overhead cost ………….

$166,500

$238,500

Deduct:

Utilities cost @ $1.20 per MH* ……

51,600

87,600

Supervisory salaries …………………

49,000

49,000

Maintenance cost ………………………

$ 65,900

$101,900

*$51,600 ÷ 43,000 MHs = $1.20 per MH

2. High-low analysis of maintenance cost:

Machine-

Hours

Maintenance

Cost

High activity level …………..

73,000

$101,900

Low activity level ……………

43,000

65,900

Change ………………………..

30,000

$36,000

Variable cost per unit of activity:

Variable cost per unit = Change in cost ÷ Change in activity

Variable cost per unit = $36,000 ÷ 30,000 MHs = $1.20 per MH

Total fixed cost:

Total maintenance cost at the low activity level …………

$65,900

Less the variable cost element

(43,000 MHs × $1.20 per MH) …………………………….

51,600

Fixed cost element ……………………………………………..

$14,300

Therefore, the cost formula is $14,300 per month plus $1.20 per

machine-hour or:

Y = $14,300 + $1.20X

Problem 1-20B (continued)

3.

Variable Rate per

Machine-Hour

Fixed Cost

Maintenance cost …………..

$1.20

$14,300

Utilities cost ………………….

1.20

Supervisory salaries cost ….

49,000

Totals ………………………….

$2.40

$63,300

Thus, the cost formula is: Y = $63,300 + $2.40X.

4. Total overhead cost at an activity level of 48,000 machine-hours:

Fixed costs ………………………………………………….

$ 63,300

Variable costs: $2.40 per MH × 48,000 MHs……….

115,200

Total overhead costs ……………………………………..

$178,500

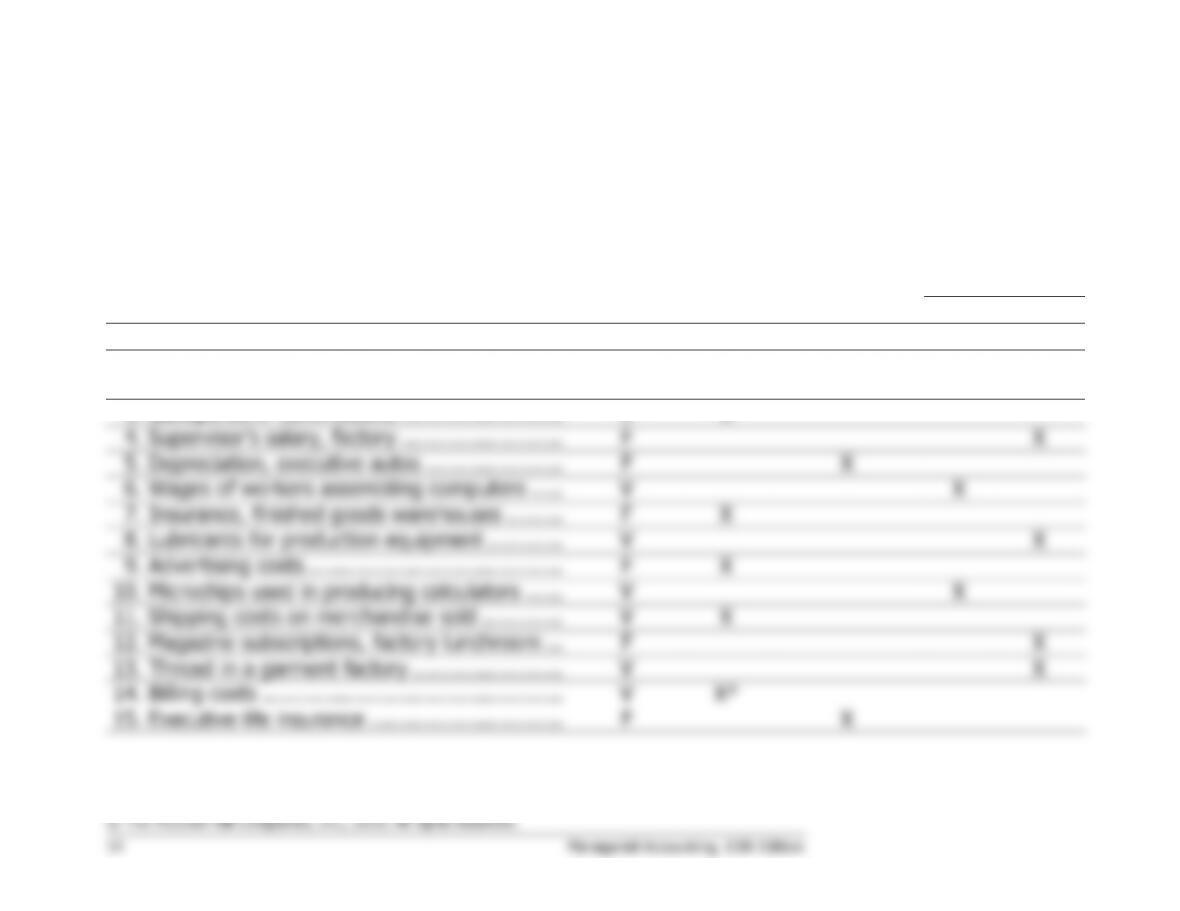

Problem 1-21B (30 minutes)

Note to the Instructor: There may be some exceptions to the answers below. The purpose of this

problem is to get the student to start

thinking

about cost behavior and cost purposes; try to avoid

lengthy discussions about how a particular cost is classified.

Variable or

Selling

Administrative

Manufacturing

(Product) Cost

Cost Item

Fixed

Cost

Cost

Direct

Indirect

1.

Property taxes, factory …………………………..

F

X

2.

Boxes used for packaging detergent

produced by the company …………………….

V

X

3.

Salespersons’ commissions ……………………..

V

X

4.

Supervisor’s salary, factory ……………………..

F

X

5.

Depreciation, executive autos ………………….

F

X

6.

Wages of workers assembling computers …..

V

X

7.

Insurance, finished goods warehouses ………

F

X

8.

Lubricants for production equipment …………

V

X

9.

Advertising costs …………………………………..

F

X

10.

Microchips used in producing calculators ……

V

X

11.

Shipping costs on merchandise sold ………….

V

X

12.

Magazine subscriptions, factory lunchroom …

F

X

13.

Thread in a garment factory ……………………

V

X

14.

Billing costs …………………………………………

V

X*

15.

Executive life insurance ………………………….

F

X

Problem 1-21B (continued)

Variable or

Selling

Administrative

Manufacturing

(Product) Cost

Cost Item

Fixed

Cost

Cost

Direct

Indirect

16.

Ink used in textbook production ……………….

V

X

17.

Fringe benefits, assembly-line workers ………

V

X**

18.

Yarn used in sweater production ………………

V

X

19.

Wages of receptionist, executive offices …….

F

X

Problem 1-22B (45 minutes)

1. High-low method:

Units

Sold

Shipping

Expense

High activity level …………..

47,000

$245,000

Low activity level ……………

29,000

173,000

Change ………………………..

18,000

$72,000

Total shipping expense at high activity

level ……………………………………………..

$245,000

Less variable element:

47,000 units × $4 per unit …………………

188,000

Fixed cost element …………………………….

$ 57,000

Problem 1-22B (continued)

2.

McKenzie Company

Budgeted Income Statement

For the First Quarter of Year 3

Sales (35,000 units × $56 per unit) ……………….

$1,960,000

Variable expenses:

Cost of goods sold

(35,000 units × $26 per unit) ………………….

$910,000

Shipping expense

(35,000 units × $4 per unit) …………………….

140,000

Sales commission ($1,960,000 × .07) ………….

137,200

Total variable expenses ………………………………..

1,187,200

Contribution margin …………………………………….

772,800

Fixed expenses:

Shipping expenses ……………………………………

57,000

Advertising expense ………………………………….

183,000

Administrative salaries ………………………………

93,000

Depreciation expense ………………………………..

63,000

Total fixed expenses ……………………………………

396,000

Net operating income ………………………………….

$ 376,800

Problem 1-23B (45 minutes)

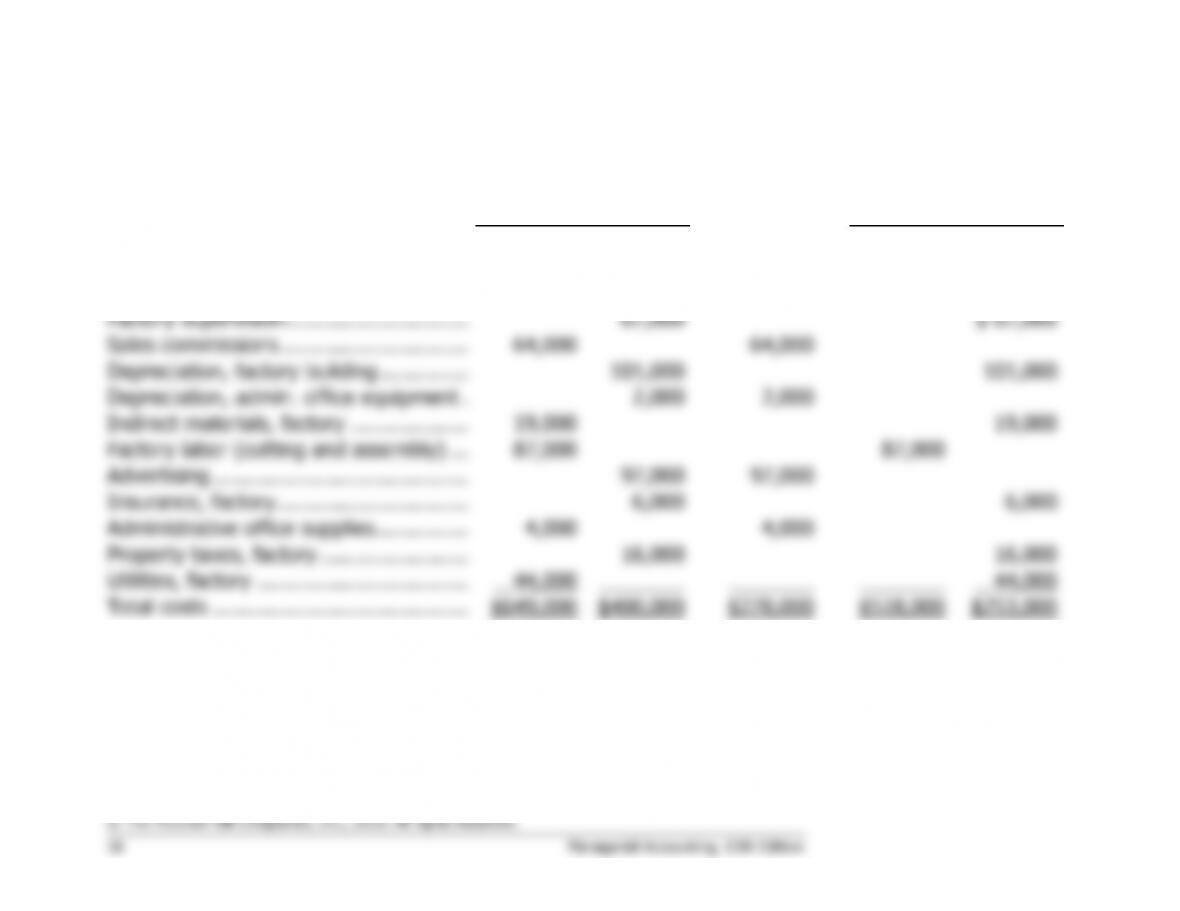

1.

Selling or

Cost Behavior

Administrative

Product Cost

Cost Item

Variable

Fixed

Cost

Direct

Indirect

Direct materials used (wood, glass) …..

$431,000

$431,000

Administrative office salaries ……………

$111,000

$111,000

Factory supervision ………………………..

67,000

$ 67,000

Sales commissions …………………………

64,000

64,000

Depreciation, factory building …………..

101,000

101,000

Depreciation, admin. office equipment .

2,000

2,000

Indirect materials, factory ……………….

19,000

19,000

Factory labor (cutting and assembly) …

87,000

87,000

Advertising …………………………………..

97,000

97,000

Insurance, factory ………………………….

6,000

6,000

Administrative office supplies ……………

4,000

4,000

Property taxes, factory ……………………

16,000

16,000

Utilities, factory …………………………….

44,000

44,000

Total costs …………………………………..

$649,000

$400,000

$278,000

$518,000

$253,000

Problem 1-23B (continued)

2. The average product cost per bookcase will be:

Direct…………………………….

$518,000

Indirect ………………………….

253,000

Total …………………………..…

$771,000

$771,000 ÷ 3,900 bookcases = $198 per bookcase

3. The average product cost per bookcase would increase if the production

4. a. Yes, there probably would be a disagreement. The president is likely

to want a price of at least $198, which is the average cost per unit to

manufacture 3,900 bookcases. He may

expect an even higher price