Problem 8-21B (continued)

2. The computations to follow will require the standard quantities allowed

for the actual output for each material.

Standard Quantity Allowed

Material X342:

Production of Alpha8 (1.5 kilos per unit × 1,200 units) ……

1,800 kilos

Production of Zeta9 (2.7 kilos per unit × 1,700 units) ……..

4,590 kilos

Total ……………………………………………………………………

6,390 kilos

Material Y561:

Production of Alpha8 (2.3 liters per unit × 1,200 units) …..

2,760 liters

Production of Zeta9 (4.3 liters per unit × 1,700 units) …….

7,310 liters

Total ……………………………………………………………………

10,070 liters

Direct Materials Variances—Material X342:

Materials quantity variance = SP (AQ – SQ)

= $3.40 per kilo (8,800 kilos – 6,390 kilos)

= $8,194 U

Materials price variance = AQ (AP – SP)

= 13,000 kilos ($3.60 per kilo* – $3.40 per kilo)

= $2,600 U

**$46,800 ÷ 13,000 kilos = $3.60 per kilo

Direct Materials Variances—Material Y561:

Materials quantity variance = SP (AQ – SQ)

= $1.5 per liter (14,000 liters – 10,070 liters)

= $5,895 U

Materials price variance = AQ (AP – SP)

= 18,000 liters ($1.40 per liter* – $1.50 per liter)

= $1,800 F

*$25,200 ÷ 18,000 liters = $1.40 per liter

Problem 8-21B (continued)

3. The computations to follow will require the standard quantities allowed

for the actual output for direct labor in each department.

Standard Hours Allowed

Sintering:

Production of Alpha8 (0.20 hours per unit × 1,200 units) ..

240 hours

Production of Zeta9 (0.35 hours per unit × 1,700 units) ….

595 hours

Total ……………………………………………………………………

835 hours

Finishing:

Production of Alpha8 (0.75 hours per unit × 1,200 units) ..

900 hours

Production of Zeta9 (0.85 hours per unit × 1,700 units) ….

1,445 hours

Total ……………………………………………………………………

2,345 hours

Problem 8-22B (45 minutes)

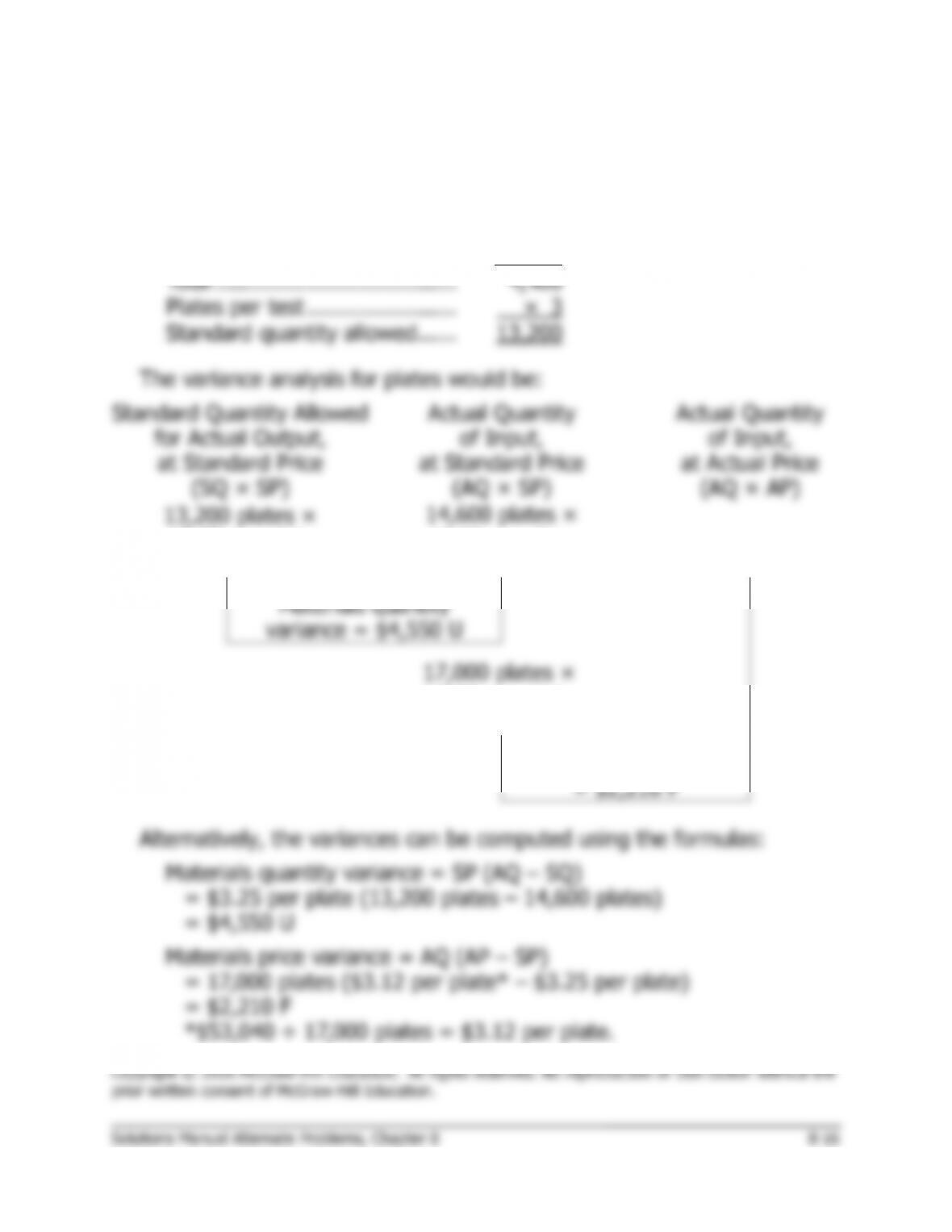

1. The standard quantity of plates allowed for tests performed during the

month would be:

Smears …………………………...

3,400

Blood tests ……………………….

1,000

Total ……………………………….

4,400

Plates per test …………………..

× 3

Standard quantity allowed ……

13,200

The variance analysis for plates would be:

Standard Quantity Allowed

for Actual Output,

at Standard Price

(SQ × SP)

Actual Quantity

of Input,

at Standard Price

(AQ × SP)

Actual Quantity

of Input,

at Actual Price

(AQ × AP)

13,200 plates ×

$3.25 per plate

= $42,900

14,600 plates ×

$3.25 per plate

= $47,450

$53,040

Materials quantity

variance = $4,550 U

17,000 plates ×

$3.25 per plate

= $55,250

Materials price variance

= $2,210 F

Problem 8-22B (continued)

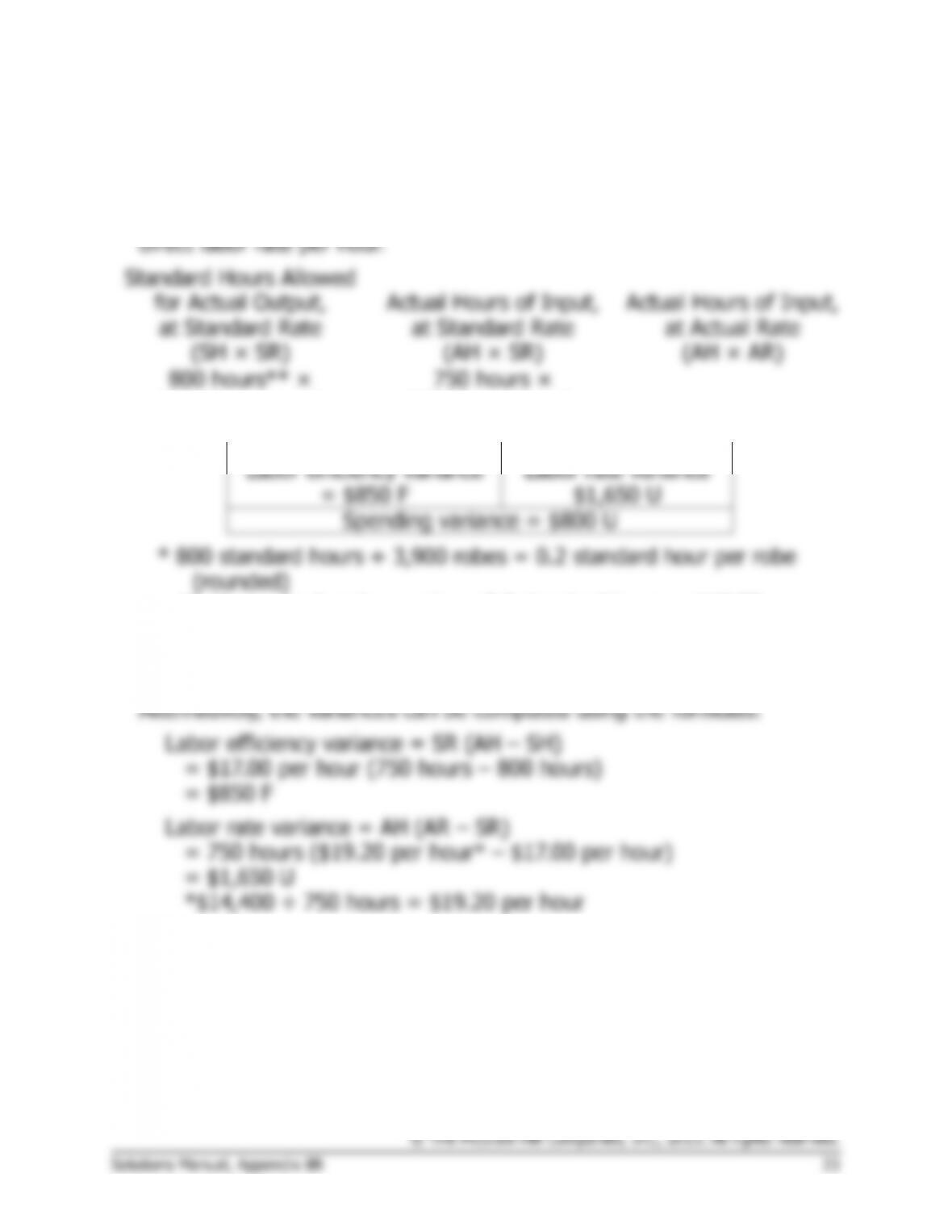

2. a. The standard hours allowed for tests performed during the month

would be:

Smears: 0.4 hour per test × 3,400 tests …..

1,360

Blood tests: 0.8 hour per test × 1,000

tests ………………………………………………

800

Total standard hours allowed ………………….

2,160

The variance analysis of labor would be:

Standard Hours Allowed

for Actual Output,

at Standard Rate

(SH × SR)

Actual Hours of Input,

at Standard Rate

(AH × SR)

Actual Hours of Input,

at Actual Rate

(AH × AR)

2,160 hours ×

$11.60 per hour

= $25,056

2,400 hours ×

$11.60 per hour

= $27,840

= $26,400

Labor efficiency variance

= $2,784 U

Labor rate variance

= $1,440 F

Spending Variance = $1,344 U

Alternatively, the variances can be computed using the formulas:

Labor efficiency variance = SR (AH – SH)

= $11.60 per hour (2,400 hours – 2,160 hours)

= $2,784 U

Labor rate variance = AH (AR – SR)

= 2,400 hours ($11.00 per hour* – $11.60 per hour)

= $1,440 F

*$26,400 ÷ 2,400 hours = $11.00 per hour

Problem 8-22B (continued)

2. b. The policy probably should not be continued. Although the hospital is

saving $0.60 per hour by employing more assistants relative to the

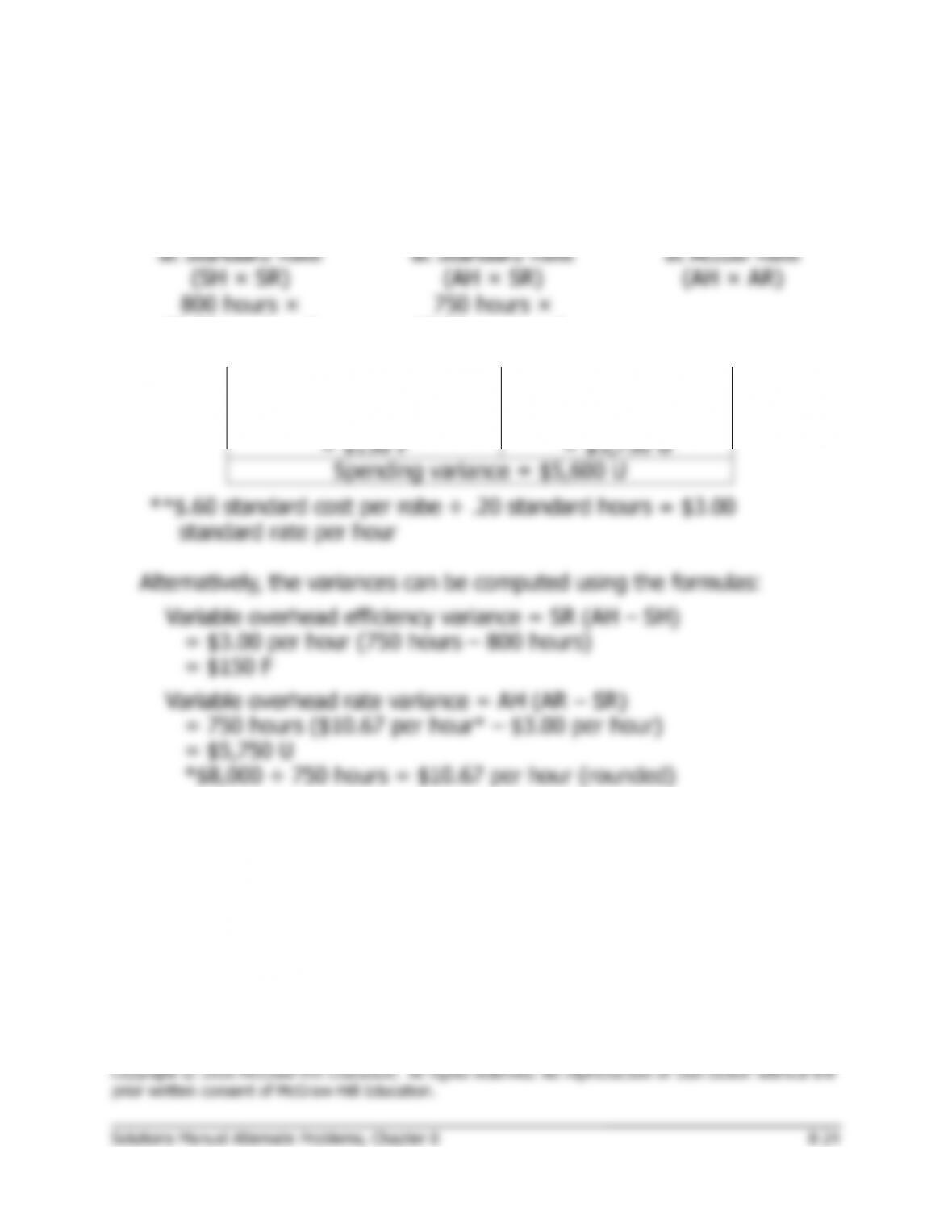

3. The variable overhead variances follow:

Standard Hours Allowed

for Actual Output,

at Standard Rate

(SH × SR)

Actual Hours of Input,

at Standard Rate

(AH × SR)

Actual Hours of Input,

at Actual Rate

(AH × AR)

2,160 hours ×

$7.50 per hour

= $16,200

2,400 hours ×

$7.50 per hour

= $18,000

$19,200

Variable overhead

efficiency variance

= $1,800 U

Variable overhead

rate variance

= $1,200 U

Spending variance = $3,000 U

Alternatively, the variances can be computed using the formulas:

Variable overhead efficiency variance = SR (AH – SH)

= $7.50 per hour (2,400 hours – 2,160 hours)

= $1,800 U

Variable overhead rate variance = AH (AR – SR)

= 2,400 hours ($8.00 per hour* – $7.50 per hour)

= $1,200 U

*$19,200 ÷ 2,400 hours = $8.00 per hour

Yes, the two variances are related. Both are computed by comparing

actual labor time to the standard hours allowed for the output of the

period. Thus, if there is an unfavorable labor efficiency variance, there

Problem 8-23B(20 minutes)

1. The flexible budget is shown below:

OpenDoor Corporation

Flexible Budget

For the Month Ended April 30

Flexible

Budget

Machine-hours (q) ……………………..

17,000

Utilities ($16,800 + $0.18q) …………

$ 19,860

Maintenance ($38,700 + $2.00q) ….

72,700

Supplies ($0.50q) ………………………

8,500

Indirect labor ($94,300 + $1.60q) …

121,500

Depreciation ($67,600) ……………….

67,600

Total ……………………………………….

$290,160

Problem 8-23B (continued)

2. The spending variances are computed below:

OpenDoor Corporation

Spending Variances

For the Month Ended April 30

Flexible

Budget

Actual

Results

Spending

Variances

Machine-hours (q) ……………………..

17,000

17,000

Utilities ($16,800 + $0.18q) …………

$ 19,860

$ 22,020

$2,160

U

Maintenance ($38,700 + $2.00q) ….

72,700

70,500

2,200

F

Supplies ($0.50q) ………………………

8,500

9,300

800

U

Indirect labor ($94,300 + $1.60q) …

121,500

125,600

4,100

U

Depreciation ($67,600) ……………….

67,600

69,300

1,700

U

Total ……………………………………….

$290,160

$296,720

$6,560

U

Problem 8-24B (45 minutes)

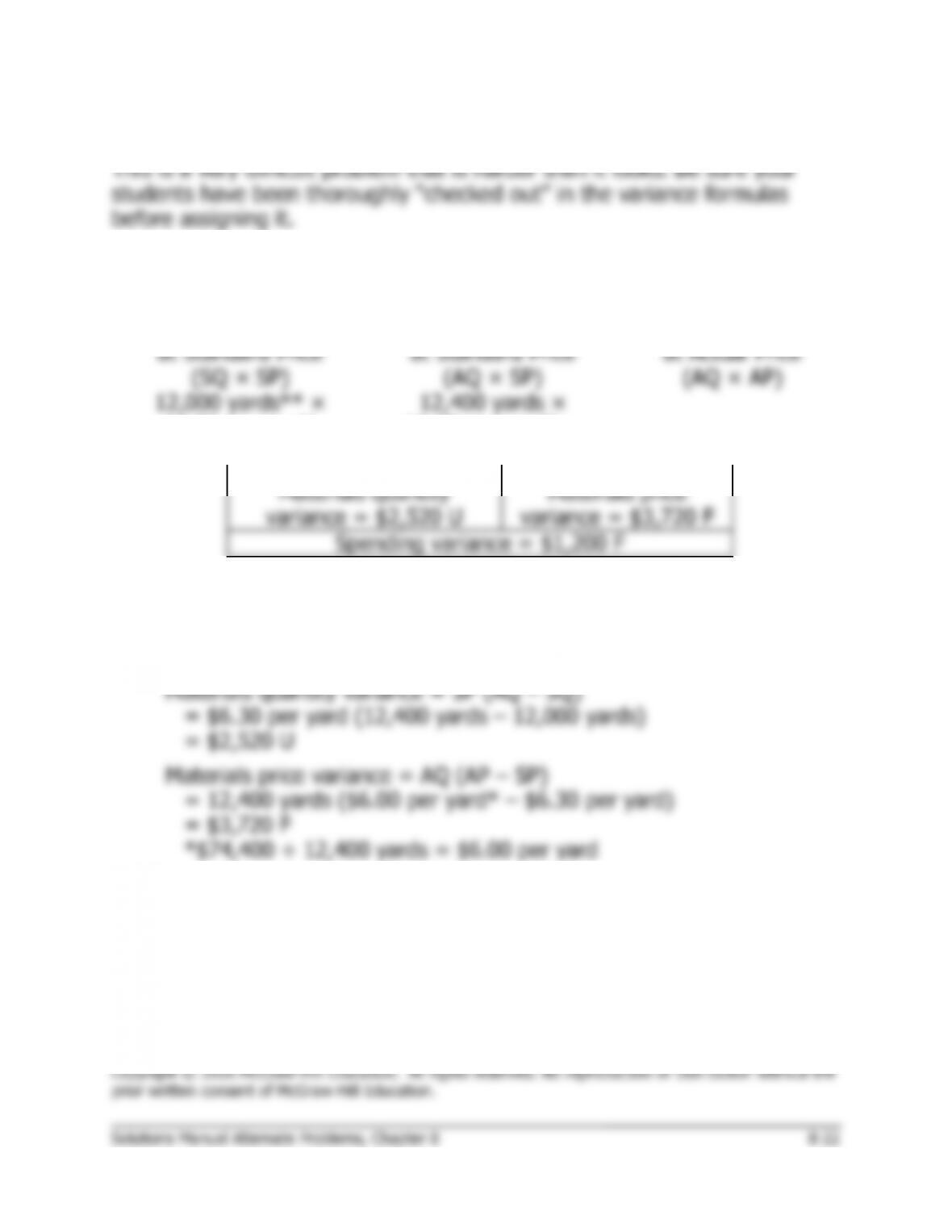

1.

Standard Quantity Allowed

for Actual Output,

at Standard Price

(SQ × SP)

Actual Quantity of

Input,

at Standard Price

(AQ × SP)

Actual Quantity of

Input,

at Actual Price

(AQ × AP)

12,000 yards** ×

$6.30 per yard*

= $75,600

12,400 yards ×

$6.30 per yard* =

$78,120

$74,400

Materials quantity

variance = $2,520 U

Materials price

variance = $3,720 F

Spending variance = $1,200 F

*

*$18.90 ÷ 3.0 yards = $6.3 per yard

**

4,000 units × 3.0 yards per unit = 12,000 yards

Alternatively, the variances can be computed using the formulas:

Problem 8-24B (continued)

2. Many students will miss parts 2 and 3 because they will try to use

product

costs as if they were

hourly

costs. Pay particular attention to the

computation of the standard direct labor time per unit and the standard

Problem 8-24B (continued)

3.

Standard Hours Allowed

for Actual Output,

at Standard Rate

(SH × SR)

Actual Hours of Input,

at Standard Rate

(AH × SR)

Actual Hours of Input,

at Actual Rate

(AH × AR)

800 hours ×

$3.00 per hour*

= $2,400

750 hours ×

$3.00 per hour*

= $2,250

$8,000

Variable overhead

efficiency variance

= $150 F

Variable overhead

rate variance

= $5,750 U

Spending variance = $5,600 U

*

*$.60 standard cost per robe ÷ .20 standard hours = $3.00

standard rate per hour

Alternatively, the variances can be computed using the formulas:

Variable overhead efficiency variance = SR (AH – SH)

= $3.00 per hour (750 hours – 800 hours)

= $150 F

Variable overhead rate variance = AH (AR – SR)

= 750 hours ($10.67 per hour* – $3.00 per hour)

= $5,750 U

*$8,000 ÷ 750 hours = $10.67 per hour (rounded)

Problem 8-25B (45 minutes)

1. a. Materials price variance = AQ (AP – SP)

6,200 pounds ($2.75 per pound* – SP) = $1,550 F**

$17,050 – 6,200 pounds × SP = $1,550***

6,200 pounds × SP = $18,600

SP = $3.00 per pound

*

$17,050 ÷ 6,200 pounds = $2.75 per pound

**

$1,200 U + ? = $350 F; $1,200 U – $350 F = $1,550 F

***

When used with the formula, unfavorable variances are

positive and favorable variances are negative.

b. Materials quantity variance = SP (AQ – SQ)

$3.00 per pound (6,200 pounds – SQ) = $1,200 U

$18,600 – $3.00 per pound × SQ = $1,200*

$3.00 per pound × SQ = $17,400

SQ = 5,800 pounds

*

When used with the formula, unfavorable variances are

positive and favorable variances are negative.

Alternative approach to parts (a) and (b):

Standard Quantity Allowed

for Actual Output,

at Standard Price

(SQ × SP)

Actual Quantity of

Input,

at Standard Price

(AQ × SP)

Actual Quantity of

Input,

at Actual Price

(AQ × AP)

5,800 pounds ×

$3.00 per pound

= $17,400

6,200 pounds* ×

$3.00 per pound

= $18,600

= $17,050*

Materials quantity

variance = $1,200 U*

Materials price

variance = $1,550 F

Spending variance = $350 F*

*Given.

c. 5,800 pounds ÷ 1,300 units = 4.46 pounds per unit.

Problem 8-25B (continued)

2. a. Labor efficiency variance = SR (AH – SH)

$8.50 per hour (AH – 2,730 hours*) = $4,250 F

$8.50 per hour × AH – $23,205 = –$4,250**

$8.50 per hour × AH = $18,955