Chapter 3

Activity-Based Costing

Solutions to Questions

3-1 The most common methods of assigning

overhead costs to products are plantwide over–

3-2 The assumption, implicit in conventional

costing systems, that overhead cost is propor-

tional to direct labor, is being increasingly ques–

tioned. Automation has decreased the amount

3-3 The departmental approach to assigning

overhead cost to products usually assumes that

overhead costs are proportional to direct labor-

hours or machine-hours. However, overhead

3-4 The hierarchical levels are:

1. Unit-level activities, which are performed

2. Batch-level activities, which are per–

3. Product-level activities, which are per–

4. Facility-level activities, which sustain an

organization’s general capabilities.

3-5 Activity-based costing involves two

stages of overhead cost assignments. In the first

3-6 In a conventional costing system, over–

head costs are allocated to products using some

measure of volume such as direct labor-hours or

product will be allocated exactly the same total

overhead as a low-volume product. In contrast,

if a measure of volume like direct labor-hours or

machine-hours were used to allocate this cost,

departmental pools, costs are accumulated for

each major activity. Second, the activity cost

cost pools. In principle, all of the costs in an ac-

costs of many different activities carried out in

changes the bases used to assign overhead

costs to products. Rather than assigning costs

© The McGraw-Hill Companies, Inc., 2016. All rights reserved.

2 Introduction to Managerial Accounting, 7th edition

of the activities that presumably cause overhead

costs.

3-8 While the product costs computed using

activity-based costing are almost certainly more

accurate than those computed using more con–

ventional costing methods, activity-based cost-

ing nevertheless rests on some questionable

assumptions about cost behavior. In particular,

activity-based costing assumes that costs are

proportional to activity. In reality, costs appear

to increase less than in proportion to increases

in activity. This implies that activity-based prod-

uct costs will be overstated for purposes of

making decisions. (The same criticism can be

leveled at conventional product costs.) Second,

the costs of implementing and maintaining an

activity-based costing system can be high and

its benefits may not justify this cost.

The Foundational 15

1. The plantwide overhead rate is computed as follows:

Total estimated overhead cost (a) …………

$684,000

Total expected direct labor-hours (b) ……..

12,000

DLHs

Predetermined overhead rate (a) ÷ (b) ….

$57.00

per DLH

2. The overhead cost assignments to Products Y and Z are as follows:

Product Y

Product Z

Total direct labor hours (a) ………………….

9,000

3,000

Plantwide overhead rate per DLH (b) ……..

$57.00

$57.00

Manufacturing overhead assigned (a) × (b)

$513,000

$171,000

3-6.

The activity rates are computed as follows:

Activity Cost Pool

(a)

Estimated

Overhead

Cost

(b)

Expected

Activity

(a) ÷ (b)

Activity

Rate

Machining ……………

$200,000

10,000

MH

$20

per MH

Machine setups …….

$100,000

200

setups

$500

per setup

Product design ……..

$84,000

2

products

$42,000

per product

General factory …….

$300,000

12,000

DLHs

$25

Per DLH

7. Machine setups is a batch-level activity. A setup is performed to run a

8. The product design activity is a product-level activity. The product

The Foundational 15 (continued)

9-10. Using the ABC system, the total overhead assigned to Products Y and Z is computed as follows:

Product Y

Product Z

Expected

Activity

Amount

Expected

Activity

Amount

Machining, at $20.00 per machine-hour ……………

8,000

$160,000

2,000

$ 40,000

Machine setups, at $500.00 per setup ………………

40

20,000

160

80,000

Product design, at $42,000 per product ……………

1

42,000

1

42,000

General factory, at $25.00 per direct labor-hour …

9,000

225,000

3,000

75,000

Total overhead cost assigned …………………………

$447,000

$237,000

The Foundational 15 (continued)

11–15. The percentages of overhead assigned using the plantwide and ABC approaches are computed

as follows:

Product Y

Product Z

Total

Plantwide Approach

(a)

Amount

(a) ÷ (c)

%

(b)

Amount

(b) ÷ (c)

%

(c)

Amount

Manufacturing overhead ……..

$513,000

75.0%

$171,000

25.0%

$684,000

Activity-Based Costing System

Machining ………………………..

$160,000

80.0%

$ 40,000

20.0%

$200,000

Machine setups …………………

20,000

20.0%

80,000

80.0%

100,000

Product design ………………….

42,000

50.0%

42,000

50.0%

84,000

General factory ………………….

225,000

75.0%

75,000

25.0%

300,000

Total cost assigned to products

$447,000

$237,000

$684,000

The Machining allocation percentages used in the ABC system are similar to the plantwide allocation

percentages because the Machining cost pool uses a unit-level activity measure (machine-hours).

Since the plantwide cost pool also uses a unit-level allocation base (direct labor-hours), it is

reasonable to expect these cost allocations percentages to be comparable.

Under the ABC system, 20% and 80% of the Machine Setups cost is allocated to Products Y and Z,

respectively, whereas the plantwide approach allocates 75% and 25% of all overhead costs to the

two products. These allocation percentages are different because Machine Setups is a batch-level

cost pool. Although Product Y is the high-volume product (14,000 units) and Product Z is the low-

volume product (6,000 units), Product Y only consumes 20% of the total machine setups and Product

The Foundational 15 (continued)

Under the ABC system, 50% of the Product Design cost is allocated to each

product, whereas the plantwide approach allocates 75% and 25% of all

Exercise 3-1 (10 minutes)

a.

Various individuals manage the parts inventories.

Product-level

b.

A clerk in the factory issues purchase orders for a

job.

Batch-level

c.

The personnel department trains new production

workers.

Facility-level

d.

The factory’s general manager meets with other

department heads to coordinate plans.

Facility-level

e.

Direct labor workers assemble products.

Unit-level

f.

Engineers design new products.

Product-level

g.

The materials storekeeper issues raw materials to

be used in jobs.

Batch-level

h.

The maintenance department performs periodic

preventative maintenance on general-use

equipment.

Facility-level

Exercise 3-2 (15 minutes)

1. The activity rates are computed as follows:

Activity Cost Pool

(a)

Estimated

Overhead

Cost

(b)

Expected

Activity

(a) ÷ (b)

Activity

Rate

Labor related …………………

$ 52,000

8,000

DLHs

$ 6.50

per DLH

Machine related ……………..

15,000

20,000

MHs

0.75

per MH

Machine setups ………………

42,000

1,000

setups

42.00

per setup

Production orders ……………

18,000

500

orders

36.00

per order

Product testing ……………….

48,000

2,000

tests

24.00

per test

Packaging ……………………..

75,000

5,000

packages

15.00

per package

General factory ………………

108,800

8,000

DLHs

13.60

per DLH

Total …………………………...

$358,800

2. The predetermined overhead rate based entirely on direct labor-hours would be computed as follows:

Total estimated overhead cost (a) …………

$358,800

Total expected direct labor-hours (b) ……..

8,000

DLHs

Predetermined overhead rate (a) ÷ (b) ….

$ 44.85

per DLH

Exercise 3-3 (30 minutes)

The unit product costs for the products are a combination of direct materials, direct labor, and overhead

costs. The overhead costs assigned to each product would be computed as follows:

J78

B52

Expected

Activity

Amount

Expected

Activity

Amount

Labor related, at $7.00 per direct labor-hour ……..

1,000

$ 7,000

40

$ 280

Machine related, at $3.00 per machine-hour ……..

3,200

9,600

30

90

Machine setups, at $40.00 per setup ……………….

5

200

1

40

Production orders, at $160.00 per order ……………

5

800

1

160

Shipments, at $120.00 per shipment………………..

10

1,200

1

120

General factory, at $4.00 per direct labor-hour …..

1,000

4,000

40

160

Total overhead cost assigned (a) …………………….

$22,800

$ 850

Number of units produced (b) ………………………..

4,000

100

Overhead cost per unit (a) ÷ (b) …………………….

$ 5.70

$8.50

The unit product costs combine direct materials, direct labor, and overhead costs as follows:

J78

B52

Direct materials …………………………..………….

$ 6.50

$31.00

Direct labor ……………………………………………

3.75

6.00

Manufacturing overhead (see above) …………..

5.70

8.50

Unit product cost …………………………..………..

$15.95

$45.50

Exercise 3-4 (30 minutes)

1. Using the company‘s conventional costing system, the overhead costs applied to the products would

be computed as follows:

Product H

Product L

Total

Number of units produced (a) ………..

40,000

8,000

Direct labor-hours per unit (b) ………..

0.40

0.40

Total direct labor-hours (a) × (b) ……

16,000

3,200

19,200

Total manufacturing overhead (a) ………….

$1,632,000

Total direct labor-hours (b) …………………..

19,200

DLHs

Predetermined overhead rate (a) ÷ (b) ……

$ 85.00

per DLH

Product H

Product L

Total

Manufacturing overhead applied per unit

0.40 DLH per unit × $85.00 per DLH ……

$ 34.00

$ 34.00

Number of units produced ……………………

40,000

8,000

Total manufacturing overhead applied ……

$1,360,000

$272,000

$1,632,000

2. Using the proposed ABC system, overhead costs would be assigned as follows:

Product H

Product L

Total

Total manufacturing overhead assigned (a) ……….

$816,000

$816,000

$1,632,000

Number of units produced (b) ………………………..

40,000

8,000

Manufacturing overhead per unit (a) ÷ (b) ………..

$ 20.40

$ 102.00

Exercise 3-4 (continued)

3. Under the company’s old method of allocating overhead costs, the high–

volume product, Product H, was allocated most of the overhead cost.

This occurred simply because the high-volume product is responsible for

Exercise 3-5 (30 minutes)

1. The activity rates are computed as follows:

Activity Cost Pool

(a)

Estimated

Overhead

Cost

(b)

Expected

Activity

(a) ÷ (b)

Activity

Rate

Labor related …………………

$ 156,000

26,000

DLHs

$6.00

per DLH

Purchase orders ……………..

11,000

220

orders

$50.00

per order

Parts management ………….

80,000

100

part types

$800.00

per setup

Board etching ………………..

90,000

2,000

boards

45.00

per board

General factory ………………

180,000

20,000

MHs

9.00

per MH

Total …………………………...

$517,000

Exercise 3-5 (continued)

2. The overhead assigned to each product can be computed as follows:

Product A

Activity Cost Pool

(a)

Activity Rate

(b)

Actual Activity

(a) × (b)

ABC Cost

Labor related ……….

$6

per DLH

6,000

DLHs

$ 36,000

Purchase orders …..

$50

per order

60

orders

3,000

Parts management .

$800

per part type

30

part types

24,000

Board etching ………

$45

per board

500

boards

22,500

General factory …….

$9

per MH

3,000

MHs

27,000

Total ………………….

$112,500

Product B

Activity Cost Pool

(a)

Activity Rate

(b)

Actual Activity

(a) × (b)

ABC Cost

Labor related ……….

$6

per DLH

11,000

DLHs

$ 66,000

Purchase orders …..

$50

per order

30

orders

1,500

Parts management .

$800

per part type

15

part types

12,000

Board etching ………

$45

per board

900

boards

40,500

General factory …….

$9

per MH

8,000

MHs

72,000

Total ………………….

$192,000

Activity Cost Pool

(a)

Activity Rate

(b)

Actual Activity

(a) × (b)

ABC Cost

Labor related ……….

$6

per DLH

4,000

DLHs

$ 24,000

Purchase orders …..

$50

per order

40

orders

2,000

Parts management .

$800

per part type

40

part types

32,000

Board etching ………

$45

per board

600

boards

27,000

General factory …….

$9

per MH

3,000

MHs

27,000

Total ………………….

$112,000

Exercise 3-5 (continued)

Product D

Activity Cost Pool

(a)

Activity Rate

(b)

Actual Activity

(a) × (b)

ABC Cost

Labor related ………..

$6

per DLH

5,000

DLHs

$ 30,000

Purchase orders ……

$50

per order

90

orders

4,500

Parts management ..

$800

per part type

15

part types

12,000

Board etching ……….

$45

per board

0

boards

0

General factory ……..

$9

per MH

6,000

MHs

54,000

Total …………………..

$100,500

Exercise 3-6 (15 minutes)

1. & 2.

Activity

Activity

Classification

Examples of Activity

Measures

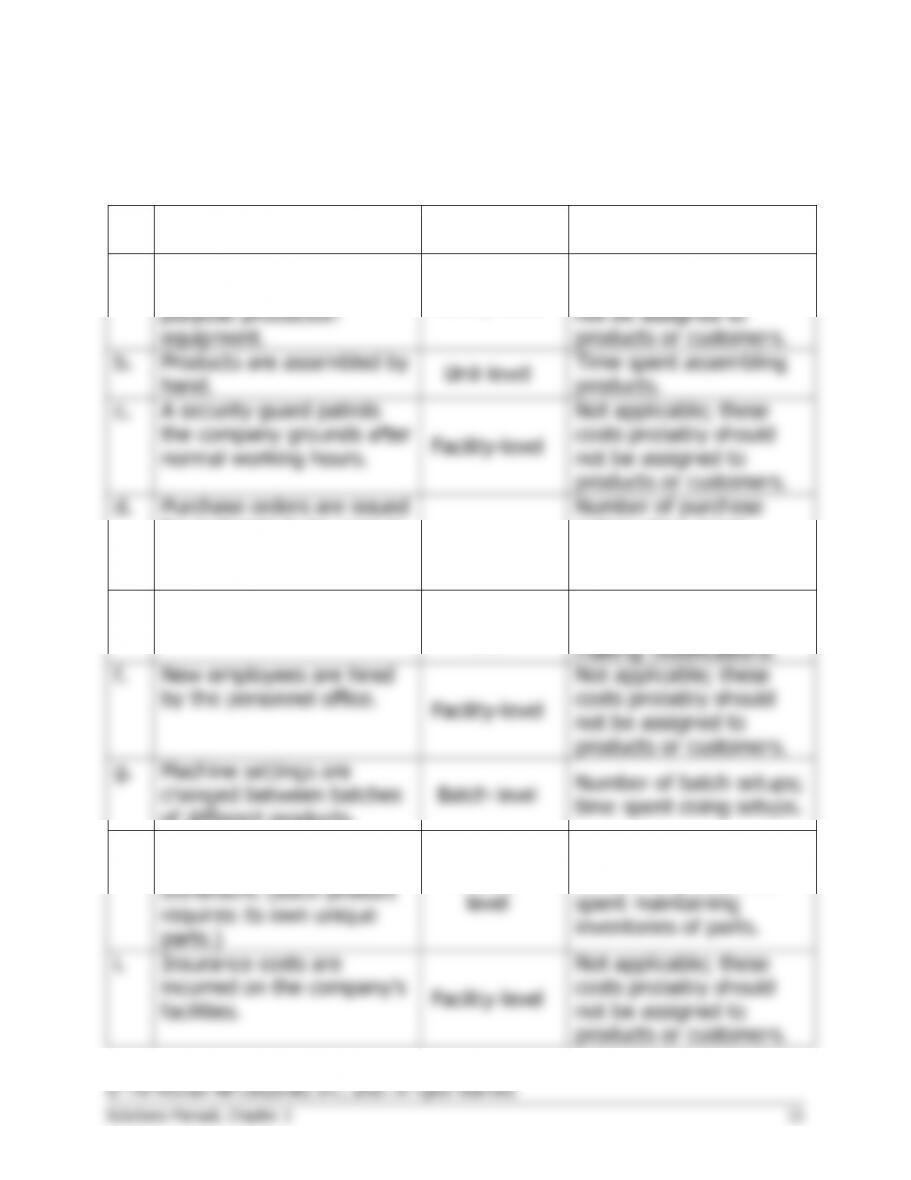

a.

Preventive maintenance is

performed on general-

purpose production

equipment.

Facility-level

Not applicable; these

costs probably should

not be assigned to

products or customers.

b.

Products are assembled by

hand.

Unit-level

Time spent assembling

products.

c.

A security guard patrols

the company grounds after

normal working hours.

Facility-level

Not applicable; these

costs probably should

not be assigned to

products or customers.

d.

Purchase orders are issued

for materials to be used in

production.

Batch-level

Number of purchase

orders; time spent

preparing purchase

orders.

e.

Modifications are made to

product designs.

Product-

level

Number of modifications

made; time spent

making modifications.

f.

New employees are hired

by the personnel office.

Facility-level

Not applicable; these

costs probably should

not be assigned to

products or customers.

g.

Machine settings are

changed between batches

of different products.

Batch-level

Number of batch setups;

time spent doing setups.

h.

Parts inventories are

maintained in the

storeroom. (Each product

requires its own unique

parts.)

Product-

level

Number of products;

number of parts; time

spent maintaining

inventories of parts.

i.

Insurance costs are

incurred on the company’s

facilities.

Facility-level

Not applicable; these

costs probably should

not be assigned to

products or customers.

Exercise 3-7 (45 minutes)

1. The unit product costs under the company’s conventional costing system

would be computed as follows:

Mercon

Wurcon

Total

Number of units produced (a) …………………

10,000

40,000

Direct labor-hours per unit (b) …………………

0.20

0.25

Total direct labor-hours (a) × (b) …………….

2,000

10,000

12,000

Total manufacturing overhead (a) ……………

$336,000

Total direct labor-hours (b) …………………….

12,000

DLHs

Predetermined overhead rate (a) ÷ (b) ……..

$28.00

per DLH

Mercon

Wurcon

Direct materials …………………………..……….

$10.00

$ 8.00

Direct labor …………………………………………

3.00

3.75

Manufacturing overhead applied:

0.20 DLH per unit × $28.00 per DLH ………

5.60

0.25 DLH per unit × $28.00 per DLH ………

7.00

Unit product cost ………………………………….

$18.60

$18.75

Exercise 3-7 (continued)

2. The unit product costs with the proposed ABC system can be computed as follows:

Activity Cost Pool

Estimated

Overhead

Cost*

(b)

Expected

Activity

(a) ÷ (b)

Activity

Rate

Labor related ………….

$168,000

12,000

direct labor-hours

$14.00

per direct labor-hour

Engineering design …..

168,000

8,000

engineering-hours

$21.00

per engineering-hour

$336,000

*The total manufacturing overhead cost is split evenly between the two activity cost pools.

Manufacturing overhead is assigned to the two products as follows:

Mercon

Wurcon

Expected

Expected

Activity

Amount

Activity

Amount

Labor related, at $14.00 per direct labor-hour ……….

2,000

$ 28,000

10,000

$140,000

Engineering design, at $21.00 per engineering-hour .

4,000

84,000

4,000

84,000

Total overhead cost assigned (a)………………………..

$112,000

$224,000

Number of units produced (b) …………………………...

10,000

40,000

Overhead cost per unit (a) ÷ (b) ………………………..

$11.20

$5.60

Exercise 3-7 (continued)

The unit product costs combine direct materials, direct labor, and

Exercise 3-8 (30 minutes)

1. Activity rates can be computed as follows:

Activity Cost Pool

(a)

Estimated

Overhead

Cost

(b)

Expected

Activity

(a) ÷ (b)

Activity Rate

Machine setups …….

$21,600

180

setups

$120

per setup

Special processing …

$180,000

4,000

MHs

$45

per MH

General factory …….

$288,000

24,000

DLHs

$12

per DLH

2. The unit product costs would be computed as follows, starting with the

computation of the manufacturing overhead:

Rims

Posts

Machine setups:

$120 per setup × 100 setups …………

$ 12,000

$120 per setup × 80 setups …………..

$ 9,600

Special processing:

$45 per MH × 4,000 MHs ………………

180,000

$45 per MH × 0 MHs ……………………

0

General factory:

$12 per DLH × 8,000 DLHs ……………

96,000

$12 per DLH × 16,000 DLHs ………….

192,000

Total overhead cost (a) …………………..

$288,000

$201,600

Number of units produced (b) …………..

20,000

80,000

Overhead cost per unit (a) ÷ (b) ……….

$14.40

$2.52

Rims

Posts

Direct materials ……………………………..

$17.00

$10.00

Direct labor:

$16 per DLH × 0.40 DLHs ……………..

6.40

$16 per DLH × 0.20 DLHs ……………..

3.20

Manufacturing overhead (see above) ….

14.40

2.52

Unit product cost …………………………...

$37.80

$15.72

Exercise 3-9 (30 minutes)

1. Activity Rates:

Activity Cost Pool

(a)

Estimated

Overhead

Cost

(b)

Expected

Activity

(a) ÷ (b)

Activity Rate

Customer deliveries …………

$400,000

5,000

deliveries

$80.00

per delivery

Manual order processing …..

$300,000

4,000

orders

$75.00

per manual order

Electronic order processing .

$200,000

12,500

orders

$16.00

per electronic order

Line item picking …………….

$500,000

400,000

line items

$1.25

per line item picked