Exercise 5-11 (20 minutes)

a.

Case #1

Case #2

Number of units sold ..

15,000

*

4,000

Sales ……………………..

$180,000

*

$12

$100,000

*

$25

Variable expenses …….

120,000

*

8

60,000

15

Contribution margin ….

60,000

$ 4

40,000

$10

*

Fixed expenses ………..

50,000

*

32,000

*

Net operating income..

$ 10,000

$ 8,000

*

Case #3

Case #4

Number of units sold ..

10,000

*

6,000

*

Sales ……………………..

$200,000

$20

$300,000

*

$50

Variable expenses …….

70,000

*

7

210,000

35

Contribution margin ….

130,000

$13

*

90,000

$15

Fixed expenses ………..

118,000

100,000

*

Net operating income (loss)..

$ 12,000

*

$ (10,000)

*

b.

Case #1

Case #2

Sales ……………………..

$500,000

*

100%

$400,000

*

100%

Variable expenses …….

400,000

80%

260,000

*

65%

Contribution margin ….

100,000

20%

*

140,000

35%

Fixed expenses ………..

93,000

100,000

*

Net operating income ..

$ 7,000

*

$ 40,000

Case #3

Case #4

Sales …………………….

$250,000

100%

$600,000

*

100%

Variable expenses ……

100,000

40%

420,000

*

70%

Contribution margin ….

150,000

60%

*

180,000

30%

Fixed expenses………..

130,000

*

185,000

Net operating income (loss).

$ 20,000

*

$ (5,000)

*

*Given

Exercise 5-12 (30 minutes)

1.

Flight Dynamic

Sure Shot

Total Company

Amount

%

Amount

%

Amount

%

Sales ……………..

$150,000

100

$250,000

100

$400,000

100.0

Variable

expenses ………

30,000

20

160,000

64

190,000

47.5

Contribution

margin …………

$120,000

80

$ 90,000

36

210,000

52.5*

Fixed expenses ..

183,750

Net operating

income …………

$ 26,250

*$210,000 ÷ $400,000 = 52.5%

2. The break-even point for the company as a whole is:

Fixed expenses

Dollar sales to =

break even Overall CM ratio

$183,750

= = $350,000

0.525

3. The additional contribution margin from the additional sales is computed

as follows:

Exercise 5-13 (20 minutes)

Total

Per Unit

1.

Sales (20,000 units × 1.15 = 23,000 units) …..

$345,000

$ 15.00

Variable expenses …………………………………..

207,000

9.00

Contribution margin …………………………………

138,000

$ 6.00

Fixed expenses ………………………………………

70,000

Net operating income ………………………………

$ 68,000

2.

Sales (20,000 units × 1.25 = 25,000 units) …..

$337,500

$13.50

Variable expenses …………………………………..

225,000

9.00

Contribution margin …………………………………

112,500

$ 4.50

Fixed expenses ………………………………………

70,000

Net operating income ………………………………

$ 42,500

3.

Sales (20,000 units × 0.95 = 19,000 units) …..

$313,500

$16.50

Variable expenses …………………………………..

171,000

9.00

Contribution margin …………………………………

142,500

$ 7.50

Fixed expenses ………………………………………

90,000

Net operating income ………………………………

$ 52,500

4.

Sales (20,000 units × 0.90 = 18,000 units) …..

$302,400

$16.80

Variable expenses …………………………………..

172,800

9.60

Contribution margin …………………………………

129,600

$ 7.20

Fixed expenses ………………………………………

70,000

Net operating income ………………………………

$ 59,600

Exercise 5-14 (30 minutes)

1. Variable expenses: $40 × (100% – 30%) = $28

2.

a.

Selling price ……………………..

$40

100%

Variable expenses ……………..

28

70%

Contribution margin …………..

$12

30%

Profit

= Unit CM × Q − Fixed expenses

$0

= $12 × Q − $180,000

$12Q

= $180,000

Q

= $180,000 ÷ $12

Q

= 15,000 units

= CM ratio × Sales − Fixed expenses

= 0.30 × Sales − $180,000

= $180,000

= $180,000 ÷ 0.30

= $600,000

Profit

= Unit CM × Q − Fixed expenses

= $12 × Q − $180,000

$12Q

= $60,000 + $180,000

= $240,000

= $240,000 ÷ $12

= 20,000 units

Exercise 5-14 (continued)

Profit

= CM ratio × Sales − Fixed expenses

$60,000

= 0.30 × Sales − $180,000

0.30 × Sales

= $240,000

Sales

= $240,000 ÷ 0.30

Sales

= $800,000

In unit sales: $800,000 ÷ $40 per unit = 20,000 units

Selling price …………………………

$40

100%

Variable expenses ($28 – $4) …..

24

60%

Contribution margin ……………….

$16

40%

Profit

= Unit CM × Q − Fixed expenses

$0

= ($40 − $24) × Q − $180,000

$16Q

= $180,000

Q

= $180,000 ÷ $16 per unit

Q

= 11,250 units

Profit

= CM ratio × Sales − Fixed expenses

$0

= 0.40 × Sales − $180,000

0.40 × Sales

= $180,000

Sales

= $180,000 ÷ 0.40

Sales

= $450,000

Exercise 5-14 (continued)

3. a.

Fixed expenses

Unit sales to =

break even Unit contribution margin

$180,000

= = 15,000 units

$12 per unit

Exercise 5-14 (continued)

c.

Fixed expenses

Unit sales =

to break even Unit contribution margin

$180,000

= =11,250 units

$16 per unit

In dollar sales: 11,250 units × $40 per unit = $450,000

Alternative solution:

Fixed expenses

Break-even point=

in sales dollars CM ratio

$180,000

= =$450,000

0.40

In unit sales: $450,000 ÷ $40 per unit =11,250 units

Exercise 5-15 (15 minutes)

1.

Total

Per

Unit

Sales (15,000 games) ………

$300,000

$20

Variable expenses ……………

90,000

6

Contribution margin …………

210,000

$14

Fixed expenses ……………….

182,000

Net operating income ………

$ 28,000

$210,000

= = 7.5

$28,000

2. a. Sales of 18,000 games represent a 20% increase over last year’s

sales. Because the degree of operating leverage is 7.5, net operating

income should increase by 7.5 times as much, or by 150% (7.5 ×

20%).

Total expected net operating income …………….

$70,000

Exercise 5-16 (30 minutes)

1. The contribution margin per person would be:

Price per ticket ……………………………….

$35

Variable expenses:

Dinner ………………………………………..

$18

Favors and program ………………………

2

20

Contribution margin per person ………….

$15

= ($15) × Q − $6,000

= $6,000

= $6,000 ÷ $15

Variable cost per person ($18 + $2) ……………..

Fixed cost per person ($6,000 ÷ 300 persons) ..

Exercise 5-16 (continued)

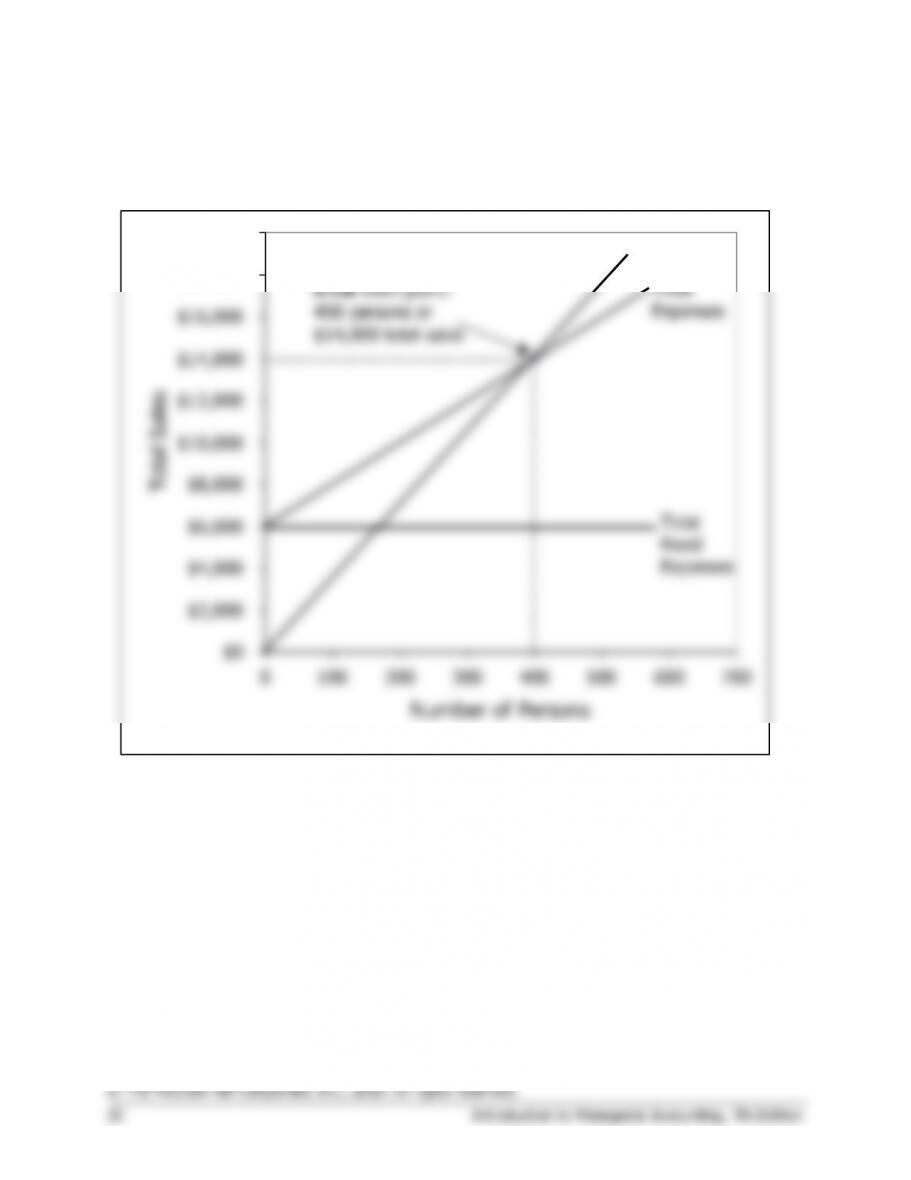

3. Cost-volume-profit graph:

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

$20,000

0100 200 300 400 500 600 700

Number of Persons

Total Sales

Total

Expenses

Total

Fixed

Expenses

Total Sales

Break-even point:

400 persons or

$14,000 total sales

Exercise 5-17 (30 minutes)

1.

Profit

= Unit CM × Q − Fixed expenses

$0

= ($50 − $32) × Q − $108,000

$0

= ($18) × Q − $108,000

$18Q

= $108,000

Q

= $108,000 ÷ $18

Q

= 6,000 stoves, or, at $50 per stove, $300,000 in sales

Alternative solution:

Fixed expenses

Unit sales to =

break even Unit contribution margin

2. An increase in variable expenses as a percentage of the selling price

would result in a higher break-even point. If variable expenses increase

3.

Present:

8,000 Stoves

Proposed:

10,000 Stoves*

Total

Per Unit

Total

Per Unit

Sales ……………………….

$400,000

$50

$450,000

$45

**

Variable expenses ………

256,000

32

320,000

32

Contribution margin ……

144,000

$18

130,000

$13

Fixed expenses ………….

108,000

108,000

Net operating income….

$ 36,000

$ 22,000

Exercise 5-17 (continued)

4.

Profit

= Unit CM × Q − Fixed expenses

$35,000

= ($45 − $32) × Q − $108,000

$35,000

= ($13) × Q − $108,000

$13 × Q

= $143,000

Q

= $143,000 ÷ $13

Q

= 11,000 stoves

Alternative solution:

Target profit + Fixed expenses

Unit sales to attain =

target profit Unit contribution margin

$35,000 + $108,000

=

$13

= 11,000 stoves

Exercise 5-18 (30 minutes)

1.

Profit

= Unit CM × Q − Fixed expenses

$0

= ($30 − $12) × Q − $216,000

$0

= ($18) × Q − $216,000

$18Q

= $216,000

Q

= $216,000 ÷ $18

Q

= 12,000 units, or, at $30 per unit, $360,000

Alternative solution:

Fixed expenses

Unit sales

=

to break even Unit contribution margin

$216,000

= = 12,000 units

$18

or at $30 per unit, $360,000

2. The contribution margin is $216,000 because the contribution margin is

3.

Target profit + Fixed expenses

Units sold to attain

=

target profit Unit contribution margin

$90,000 + $216,000

=$18

= 17,000 units

Total

Unit

Sales (17,000 units × $30 per unit) …….

$510,000

$30

Variable expenses

(17,000 units × $12 per unit) ………….

204,000

12

Contribution margin …………………………

306,000

$18

Fixed expenses ………………………………

216,000

Net operating income ………………………

$ 90,000

Exercise 5-18 (continued)

4. Margin of safety in dollar terms:

Margin of safety = Total sales – Break-even sales

in dollars

= $450,000 – $360,000 = $90,000

$90,000

= = 20%

$450,000

5. The CM ratio is 60%:

Expected total contribution margin: ($500,000 × 60%) ..

$300,000

Present total contribution margin: ($450,000 × 60%) …..

270,000

Increased contribution margin …………………………………

$ 30,000

Alternative solution:

$50,000 incremental sales × 60% CM ratio = $30,000

Given that the company’s fixed expenses will not change, monthly net

operating income will also increase by $30,000.

Problem 5-19A (45 minutes)

1.

Sales (15,000 units × $70 per unit) ………………….

$1,050,000

Variable expenses (15,000 units × $40 per unit) …

600,000

Contribution margin ………………………………………

450,000

Fixed expenses ……………………………………………

540,000

Net operating loss ………………………………………..

$ (90,000)

2.

Fixed expenses

Unit sales to=

break even Unit contribution margin

$540,000

=$30 per unit

=18,000 units

18,000 units × $70 per unit = $1,260,000 to break even

3. See the next page.

4. At a selling price of $58 per unit, the contribution margin is $18 per unit.

Therefore:

Fixed expenses

Unit sales to =

break even Unit contribution margin

$540,000

=

$18

= 30,000 units

30,000 units × $58 per unit = $1,740,000 to break even

This break-even point is different from the break-even point in part (2)

because of the change in selling price. With the change in selling price,

the unit contribution margin drops from $30 to $18, resulting in an

increase in the break–even point.

Problem 5-19A (continued)

3.

Unit

Selling

Price

Unit

Variable

Expense

Unit

Contribution

Margin

Volume

(Units)

Total

Contribution

Margin

Fixed

Expenses

Net operating

income (loss)

$70

$40

$30

15,000

$450,000

$540,000

$ (90,000)

$68

$40

$28

20,000

$560,000

$540,000

$ 20,000

$66

$40

$26

25,000

$650,000

$540,000

$110,000

$64

$40

$24

30,000

$720,000

$540,000

$180,000

$62

$40

$22

35,000

$770,000

$540,000

$230,000

$60

$40

$20

40,000

$800,000

$540,000

$260,000

$58

$40

$18

45,000

$810,000

$540,000

$270,000

$56

$40

$16

50,000

$800,000

$540,000

$260,000

The maximum profit is $270,000. This level of profit can be earned by selling 45,000 units at a price

of $58 each.

Problem 5-20A (75 minutes)

1.

a.

Selling price …………………

$25

100%

Variable expenses …………

15

60%

Contribution margin……….

$10

40%

Profit

= Unit CM × Q − Fixed expenses

$0

= $10 × Q − $210,000

$10Q

= $210,000

Q

= $210,000 ÷ $10

Q

= 21,000 balls

$300,000

= = 3.33 (rounded)

$90,000

2. The new CM ratio will be:

Selling price ………………..

$25

100%

Variable expenses …………

18

72%

Contribution margin ………

$ 7

28%

= Unit CM × Q − Fixed expenses

$0

= $7 × Q − $210,000

Q

= $210,000 ÷ $7

Q

= 30,000 balls

Problem 5-20A (continued)

Alternative solution:

Fixed expenses

Unit sales to =

break even Unit contribution margin

$210,000

$7

= 30,000 balls

3.

Profit

= Unit CM × Q − Fixed expenses

$90,000

= $7 × Q − $210,000

$7Q

= $90,000 + $210,000

Q

= $300,000 ÷ $7

Q

= 42,857 balls (rounded)

Present

Expected

Break-even point (in balls) …………………………...

21,000

30,000

Sales (in balls) needed to earn a $90,000 profit ..

30,000

42,857

Note that if variable costs do increase next year, then the company will

just break even if it sells the same number of balls (30,000) as it did last

year.

Problem 5-20A (continued)

4. The contribution margin ratio last year was 40%. If we let P equal the

new selling price, then:

P =

$18 + 0.40P

0.60P =

$18

P =

$18 ÷ 0.60

P =

$30

To verify:

Selling price ………………..

$30

100%

Variable expenses ………..

18

60%

Contribution margin ……..

$12

40%

Therefore, to maintain a 40% CM ratio, a $3 increase in variable costs

would require a $5 increase in the selling price.

5. The new CM ratio would be:

Selling price ……………………

$25

100%

Variable expenses …………….

9*

36%

Contribution margin ………….

$16

64%

*$15 – ($15 × 40%) = $9

= Unit CM × Q − Fixed expenses

= $16 × Q − $420,000

= $420,000

= $420,000 ÷ $16

= 26,250 balls

Problem 5-20A (continued)

6.

a.

Profit

= Unit CM × Q − Fixed expenses

$90,000

= $16 × Q − $420,000

$16Q

= $90,000 + $420,000

Q

= $510,000 ÷ $16

Q

= 31,875 balls

Sales (30,000 balls × $25 per ball) ………………..

$750,000

Variable expenses (30,000 balls × $9 per ball) …

270,000

Contribution margin ……………………………………

480,000

Fixed expenses ………………………………………….

420,000

Net operating income ………………………………….

$ 60,000

Contribution margin

Degree of =

operating leverage Net operating income

$480,000

= = 8

$60,000