Problem 10-18B (30 minutes)

1.

Contribution margin lost if the tour is discontinued ..

$(2,640)

Less tour costs that can be avoided if the tour is

discontinued:

Tour promotion …………………………………………

$680

Fee, tour guide …………………………………………

720

Fuel for bus ……………………………………………..

160

Overnight parking fee, bus…………………………..

80

Room & meals, bus driver and tour guide ……….

190

1,830

Net decrease in profits if the tour is discontinued ….

$ (810)

The following costs are not relevant to the decision:

Cost

Reason

Salary of bus driver

The drivers are all on salary and there

would be no change in the number of

drivers on the payroll.

Depreciation of bus

Depreciation due to wear and tear is

negligible and there would be no

change in the number of buses in the

fleet.

Liability insurance, bus

There would be no change in the

number of buses in the fleet.

Bus maintenance & preparation

There would be no change in the size

of the maintenance & preparation staff.

Problem 10-18B (continued)

Alternative Solution:

Keep

the

Tour

Drop

the Tour

Difference:

Net

Operating

Income

Increase or

(Decrease)

Ticket revenue …………………………...

$3,300

$ 0

$(3,300)

Less variable expenses …………………

660

0

660

Contribution margin ……………………..

2,640

0

(2,640)

Less tour expenses:

Tour promotion …………………………

680

0

680

Salary of bus driver ……………………

360

360

0

Fee, tour guide …………………………

720

0

720

Fuel for bus ……………………………..

160

0

160

Depreciation of bus ……………………

360

360

0

Liability insurance, bus ……………….

210

210

0

Overnight parking fee, bus ………….

80

0

80

Room & meals, bus driver and tour

guide ……………………………………

190

0

190

Bus maintenance and preparation …

230

230

0

Total tour expenses ……………………..

2,990

1,160

1,830

Net operating loss ……………………….

$ (350)

$(1,160)

$ (810)

2. The goal of increasing average seat occupancy could be accomplished

by dropping tours like the Historic Mansions tour with lower-than-

average seat occupancies. This could reduce profits in at least two ways.

tours.

Problem 10-19B (15 minutes)

1.

Per 16-

Ounce T–

Bone

Revenue from further processing:

Selling price of one filet mignon (6 ounces × $3.60

per pound/16 ounces per pound) ……………………..

$1.35

Selling price of one New York cut (8 ounces × $3.20

per pound/16 ounces per pound) ……………………..

1.60

Total revenue from further processing ……………………

2.95

Less revenue from one T-bone steak ……………………..

2.40

Incremental revenue from further processing …………..

0.55

Less cost of further processing ……………………………..

0.15

Profit per pound from further processing ………………..

$0.40

2. The T-bone steaks should be processed further into filet mignon and the

New York cuts. This will yield $.40 per pound in added profit for the

Problem 10-20B (45 minutes)

1. Product MJ-7 has a contribution margin of $16 per gallon ($36 – $20 =

$16). If the plant closes, this contribution margin will be lost on the

28,000 gallons (14,000 gallons per month × 2 = 28,000 gallons) that

could have been sold during the two-month period. However, the

company will be able to avoid some fixed costs as a result of closing

down. The analysis is:

Contribution margin lost by closing the plant for

two months ($16 per gallon × 28,000 gallons) .

$(448,000)

Costs avoided by closing the plant for two months:

Fixed manufacturing overhead cost

($60,000 × 2 months = $120,000) …………….

$120,000

Fixed selling costs

($320,000 × 12% × 2 months) …………………

76,800

196,800

Net disadvantage of closing, before start-up

costs ……………………………………………………..

(251,200)

Add start-up costs ………………………………………

(12,000)

Disadvantage of closing the plant …………………..

$(263,200)

No, the company should not close the plant; it should continue to

operate at the reduced level of 14,000 gallons produced and sold each

month. Closing will result in a $263,200 greater loss over the two-month

period than if the company continues to operate. Additional factors are

the potential loss of goodwill among the customers who need the

14,000 gallons of MJ-7 each month and the adverse effect on employee

morale. By closing down, the needs of customers will not be met (no

inventories are on hand), and their business may be permanently lost to

another supplier.

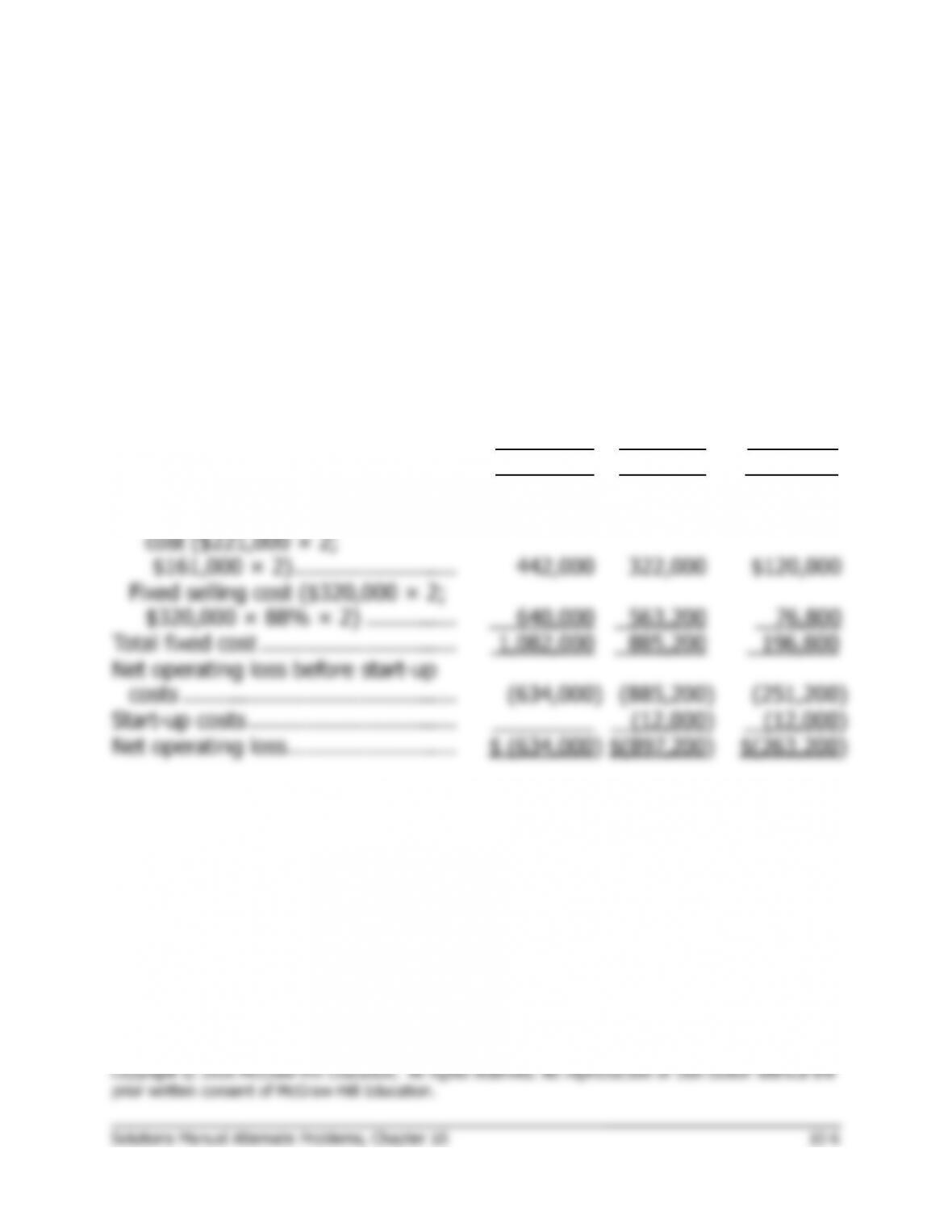

Problem 10-20B (continued)

Alternative Solution:

Plant Kept

Open

Plant

Closed

Difference—

Net

Operating

Income

Increase

(Decrease)

Sales (14,000 gallons × $36 per

gallon × 2) …………………………...

$1,008,000

$ 0

$(1,008,000)

Less variable expenses (14,000

gallons × $20 per gallon × 2) ……

560,000

0

560,000

Contribution margin …………………..

448,000

0

(448,000)

Less fixed costs:

Fixed manufacturing overhead

cost ($221,000 × 2;

$161,000 × 2) …………………….

442,000

322,000

$120,000

Fixed selling cost ($320,000 × 2;

$320,000 × 88% × 2) …………..

640,000

563,200

76,800

Total fixed cost …………………………

1,082,000

885,200

196,800

Net operating loss before start-up

costs ……………………………………

(634,000)

(885,200)

(251,200)

Start-up costs …………………………..

(12,000)

(12,000)

Net operating loss ……………………..

$ (634,000)

$(897,200)

$(263,200)

Problem 10-20B (continued)

2. Ignoring the additional factors cited in part (1) above, the company

should be indifferent between closing down or continuing to operate if

the level of sales drops to 11,550 gallons (5,775 gallons per month)

over the two-month period. The computations are:

Cost avoided by closing the plant for two months

(see above) …………………………………………………

$196,800

Less start-up costs ………………………………………….

12,000

Net avoidable costs …………………………………………

$184,800

Sales (11,550 gallons × $36 per gallon) …….

Less variable expenses (11,550 gallons ×

Contribution margin ………………………………

Less fixed expenses:

Total fixed expenses ………………………………

Start-up costs ………………………………………

Total costs …………………………………………..

Net operating loss …………………………..…….

Problem 10-21B (30 minutes)

1.

Incremental revenue:

Fixed fee (9,300 pairs × €5 per pair) ……………

€ 46,500

Reimbursement for costs of production:

(Variable production cost of €14 plus fixed

overhead cost of €4 equals €18 per pair;

9,300 pairs × €18 per pair) ………………………

167,400

Total incremental revenue ………………………….

213,900

Incremental costs:

Variable production costs (9,300 pairs × €14

per pair) ………………………………………………

130,200

Increase in net operating income …………………..

€ 83,700

2.

Sales revenue through regular channels

(9,300 pairs × €34 per pair)* ……………………..

€316,200

Sales revenue from the army (above) ……………..

213,900

Decrease in revenue received ………………………..

102,300

Less variable selling expenses avoided if the

army’s offer is accepted (9,300 pairs × €2 per

pair) ……………………………………………………..

18,600

Net decrease in net operating income with the

army’s offer …………………………………………….

€ 83,700

*This assumes that the sales through regular channels can be recovered

after the special order has been fulfilled. This may not happen if regular

customers who are turned away to fill the special order are permanently

lost to competitors.

Problem 10-22B (60 minutes)

1. The fixed overhead costs are common and will remain the same

regardless of whether the cartridges are produced internally or

purchased outside. Hence, they are not relevant. The variable

manufacturing overhead cost per box of pens is $0.30, as shown below:

Total manufacturing overhead cost per box of pens …

$0.60

Less fixed manufacturing overhead ($30,000 ÷

100,000 boxes) …………………………..…………………

0.30

Variable manufacturing overhead cost per box ………..

$0.30

Direct materials ……………………………………………….

$1.30

Direct labor …………………………………………………….

1.10

Variable manufacturing overhead …………………………

0.30

Total variable cost per box ………………………………….

$2.70

Direct materials ($1.30 × 80%) …………………………..

$1.04

Direct labor ($1.10 × 90%) ………………………………..

0.99

Variable manufacturing overhead ($0.30 × 90%) …….

0.27

Purchase of cartridges ……………………………………….

0.60

Total variable cost per box ………………………………….

$2.90

Cost avoided by purchasing the cartridges:

Direct materials ($1.30 × 20%) …………………………

$0.26

Direct labor ($1.10 × 10%) ………………………………

0.11

Variable manufacturing overhead ($0.30 × 10%) ….

0.03

Total costs avoided …………………………………………

$0.40

Cost of purchasing the cartridges …………………………

$0.60

Cost savings per box by making cartridges internally ..

$0.20

Problem 10-22B (continued)

2. The company would not want to pay any more than $0.40 per box

3. The company has three alternatives for obtaining the necessary

cartridges. It can:

#1

Produce all cartridges internally.

#2

Purchase all cartridges externally.

#3

Produce the cartridges for 100,000 boxes internally and purchase

the cartridges for 50,000 boxes externally.

The costs under the three alternatives are:

Alternative #1—Produce all cartridges internally:

Variable costs (150,000 boxes × $0.40 per box) ……….

$60,000

Fixed costs of adding capacity ………………………………

39,000

Total cost …………………………………………………………

$99,000

Alternative #2—Purchase all cartridges externally:

Variable costs (150,000 boxes × $0.60 per box) …………

$90,000

Alternative #3—Produce 100,000 boxes internally, and

purchase 50,000 boxes externally:

Variable costs:

100,000 boxes × $0.40 per box …………………………

$40,000

50,000 boxes × $0.60 per box ………………………….

30,000

Total cost …………………………………………………………

$70,000

Problem 10-22B (continued)

Or, in terms of total cost per box of pens, the answer would be:

Alternative #1—Produce all cartridges internally:

Variable costs (150,000 boxes × $2.70 per box) ……….

$405,000

Fixed costs of adding capacity ………………………………

39,000

Total cost …………………………………………………………

$444,000

Alternative #2—Purchase all cartridges externally:

Variable costs (150,000 boxes × $2.90 per box) ……….

$435,000

Alternative #3—Produce the cartridges for 100,000

boxes internally, and purchase the cartridges for

50,000 boxes externally:

Variable costs:

100,000 boxes × $2.70 per box ……………………….

$270,000

50,000 boxes × $2.90 per box …………………………

145,000

Total cost ……………………………………………………….

$415,000

Thus, the company should accept the outside supplier’s offer, but only

for the cartridges for 50,000 boxes.

4. In addition to cost considerations, the company should take into account

the following factors:

a) The ability of the supplier to meet required delivery schedules.

Problem 10-23B (60 minutes)

1. The simplest approach to the solution is:

Gross margin lost if the store is closed …….

$(241,000)

Less costs that can be avoided:

Direct advertising ……………………………..

$42,000

Sales salaries …………………………………..

42,000

Delivery salaries ……………………………….

9,500

Store rent ……………………………………….

63,000

Store management salaries (new

employee would not be hired to fill

vacant position at another store) ……….

21,000

General office salaries ……………………….

9,000

Utilities …………………………………………..

32,000

Insurance on inventories (0.67 × $8,800)

5,867

Employment taxes* …………………………..

12,225

236,592

Decrease in company net operating income

if the Downtown Store is closed …………..

$ (4,408)

*Salaries avoided by closing the store:

Sales salaries ……………………………………………….

$42,000

Delivery salaries ……………………………………………

9,500

Store management salaries ……………………………..

21,000

General office salaries …………………………………….

9,000

Total salaries ………………………………………………..

81,500

Employment tax rate ……………………………………..

× 15%

Employment taxes avoided ………………………………

$12,225

2. The Downtown Store should not be closed. If the store is closed, overall

Problem 10-23B (continued)

3. The Downtown Store should be closed if $400,000 of its sales are picked

up by the Uptown Store. The net effect of the closure will be an increase

in overall company net operating income by $171,592 per quarter:

Gross margin lost if the Downtown Store is closed …………..

$(241,000)

Gross margin gained at the Uptown Store:

$400,000 × 44% …………………………………………………..

176,000

Net loss in gross margin …………………………………………….

(65,000)

Costs that can be avoided if the Downtown Store is closed

(part 1) …………………………..…………………………………..

236,592

Net advantage of closing the Downtown Store ……………….

$171,592

Problem 10-24B (60 minutes)

1.

Selling price per unit …………………..

$40

Variable expenses per unit* …………

29

Contribution margin per unit ………..

$11

Increased unit sales (87,000 × 30%) ………………..

26,100

Contribution margin per unit …………………………..

× $11

Incremental contribution margin ………………………

$287,100

Less added fixed selling expense ……………………..

130,000

Incremental net operating income ……………………

$157,100

2.

Variable production cost per unit ……………………..

$24.30

Import duties, etc. ($13,050 ÷ 26,100 units) ……..

0.50

Shipping cost per unit ……………………………………

1.30

Break-even price per unit ……………………………….

$26.10

3. If the plant operates at 25% of normal levels, then only 5,438 units will

be produced and sold during the three-month period:

87,000 units per year × 3/12 = 21,750 units.

21,750 units × 25% = 5,438 units produced and sold.

Fixed costs that can be avoided if the plant is closed:

Net disadvantage of closing the plant ……………