Exercise 10–11 (20 minutes)

The costs that can be avoided as a result of purchasing from the outside

are relevant in a make-or-buy decision. The analysis is:

Per Unit

Differential

Costs

30,000 Units

Make

Buy

Make

Buy

Cost of purchasing ……………….

$21.00

$630,000

Cost of making:

Direct materials …………………

$ 3.60

$108,000

Direct labor ………………………

10.00

300,000

Variable overhead ……………..

2.40

72,000

Fixed overhead …………………

3.00

*

90,000

Total cost …………………………..

$19.00

$21.00

$570,000

$630,000

*

The remaining $6 of fixed overhead cost would not be relevant,

because it will continue regardless of whether the company makes

or buys the parts.

The $80,000 rental value of the space being used to produce part S-6 is an

opportunity cost of continuing to produce the part internally. Thus, the

complete analysis is:

Make

Buy

Total cost, as above ………………………………….

$570,000

$630,000

Rental value of the space (opportunity cost) …..

80,000

Total cost, including opportunity cost ……………

$650,000

$630,000

Net advantage in favor of buying …………………

$20,000

Profits would increase by $20,000 if the outside supplier’s offer is accepted.

Exercise 10-12 (15 minutes)

The company should accept orders first for Product C, second for Product

A, and third for Product B. The computations are:

Product

A

Product

B

Product

C

(1)

Direct materials required per unit ……

$24

$15

$9

(2)

Cost per pound …………………………..

$3

$3

$3

(3)

Pounds required per unit (1) ÷ (2) ….

8

5

3

(4)

Contribution margin per unit ………….

$32

$14

$21

(5)

Contribution margin per pound of

materials used (4) ÷ (3) …………….

$4.00

$2.80

$7.00

Because Product C uses the least amount of material per unit of the three

products, and because it is the most profitable of the three in terms of its

use of materials, some students will immediately assume that this is an

Exercise 10-13 (10 minutes)

Sales value after further processing

(7,000 units × $12 per unit) ……………………..

$84,000

Sales value at the split-off point

(7,000 units × $9 per unit) ………………………

63,000

Incremental revenue from further processing …

21,000

Cost of further processing ………………………….

9,500

Profit from further processing ……………………..

$11,500

Exercise 10-14 (20 minutes)

1.

Fixed cost per mile ($3,200* ÷ 10,000 miles) …

$0.32

Variable operating cost per mile …………………..

0.14

Average cost per mile ………………………………..

$0.46

*

Depreciation …………………………

$1,600

Insurance …………………………….

1,200

Garage rent ………………………….

360

Automobile tax and license ………

40

Total …………………………………..

$3,200

2. The variable operating cost is relevant in this situation. The depreciation

is not relevant because it is a sunk cost. However, any decrease in the

car.

3. When figuring the incremental cost of the more expensive car, the

relevant costs include the purchase price of the new car (net of the

resale value of the old car) and the increases in the fixed costs of

Exercise 10-15 (30 minutes)

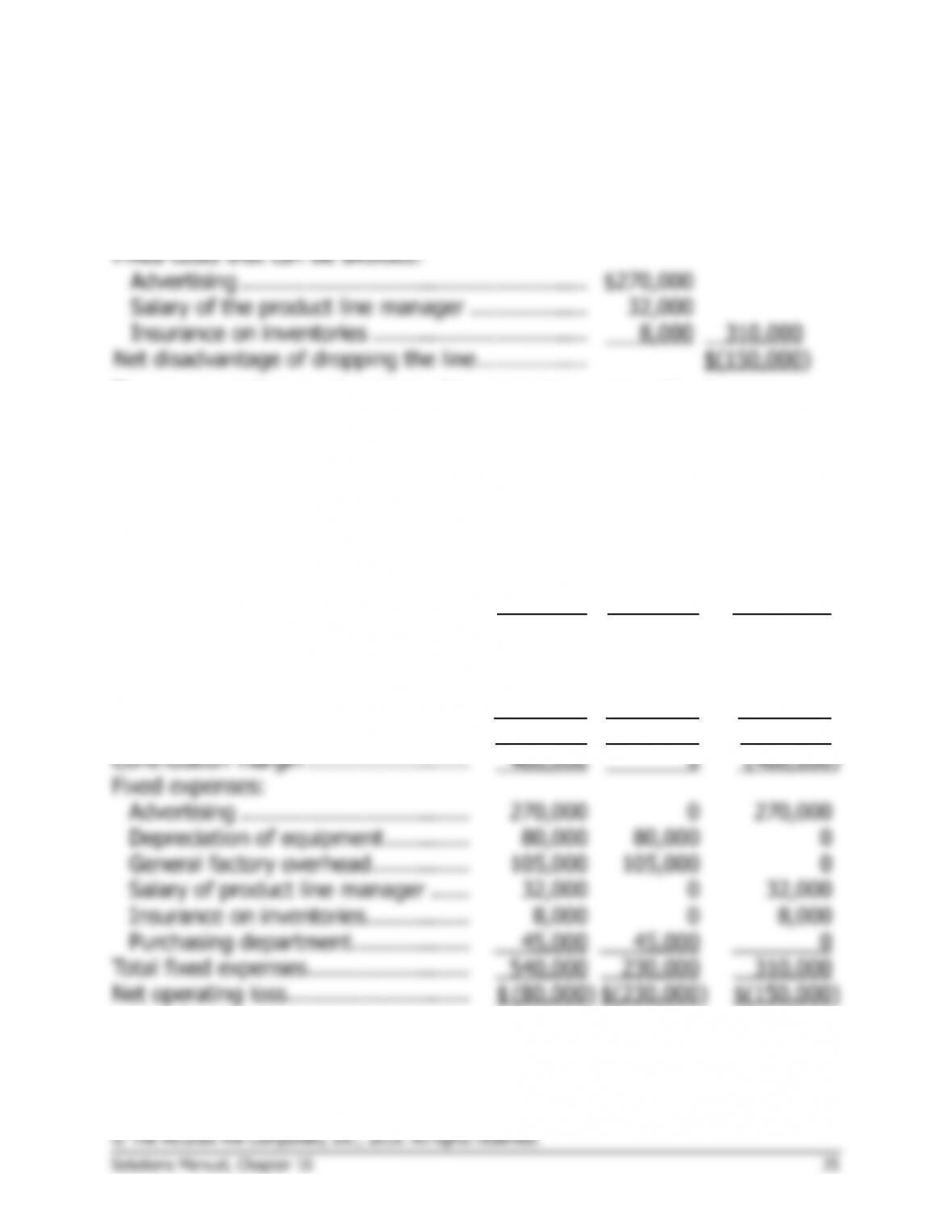

No, the bilge pump product line should not be discontinued. The

computations are:

Contribution margin lost if the line is dropped …..

$(460,000)

Fixed costs that can be avoided:

Advertising ……………………………………………..

$270,000

Salary of the product line manager ………………

32,000

Insurance on inventories …………………………...

8,000

310,000

Net disadvantage of dropping the line ……………..

$(150,000)

The same solution can be obtained by preparing comparative income

statements:

Keep

Product

Line

Drop

Product

Line

Difference:

Net

Operating

Income

Increase or

(Decrease)

Sales ………………………………………..

$850,000

$ 0

$(850,000)

Variable expenses:

Variable manufacturing expenses …

330,000

0

330,000

Sales commissions ……………………

42,000

0

42,000

Shipping …………………………………

18,000

0

18,000

Total variable expenses ………………..

390,000

0

390,000

Contribution margin …………………….

460,000

0

(460,000)

Fixed expenses:

Advertising ……………………………..

270,000

0

270,000

Depreciation of equipment ………….

80,000

80,000

0

General factory overhead ……………

105,000

105,000

0

Salary of product line manager ……

32,000

0

32,000

Insurance on inventories…………….

8,000

0

8,000

Purchasing department ………………

45,000

45,000

0

Total fixed expenses …………………….

540,000

230,000

310,000

Net operating loss ……………………….

$ (80,000)

$(230,000)

$(150,000)

Exercise 10-16 (30 minutes)

1. The relevant costs of a hunting trip would be:

Travel expense (100 miles @ $0.21 per mile) .

$21

Shotgun shells ………………………………………

20

One bottle of whiskey …………………………..…

15

Total ……………………………………………………

$56

This answer assumes that Bill would not be drinking the bottle of

whiskey anyway. It also assumes that the resale values of the camper,

pickup truck, and boat are not affected by taking one more hunting trip.

The money lost in the poker game is not relevant because Bill would

have played poker even if he did not go hunting. He plays poker every

weekend.

The other costs are sunk at the point at which the decision is made to

go on another hunting trip.

2. If Bill gets lucky and bags another two ducks, all of his costs are likely to

be about the same as they were on his last trip. Therefore, it really

doesn’t cost him anything to shoot the last two ducks—except possibly

3. In a decision of whether to give up hunting entirely, more of the costs

listed by John are relevant. If Bill did not hunt, he would not need to

Exercise 10-16 (continued)

These three requirements illustrate the slippery nature of costs. A cost

Exercise 10-17 (10 minutes)

Contribution margin lost if the Linens Department is dropped:

Lost from the Linens Department ……………………………………

$(600,000)

Lost from the Hardware Department (10% × $2,100,000) ……

(210,000)

Total lost contribution margin …………………………………………..

(810,000)

Fixed costs that can be avoided ($800,000 – $340,000) …………

460,000

Decrease in profits for the company as a whole ……………………

$(350,000)

Problem 10-18A (60 minutes)

1.

Selling price per unit ……………………………………..

$32

Variable expenses per unit ……………………………..

18

*

Contribution margin per unit …………………………..

$14

Increased sales in units (60,000 units × 25%) ……

15,000

Contribution margin per unit …………………………..

× $14

Incremental contribution margin ………………………

$210,000

Less added fixed selling expenses …………………….

80,000

Incremental net operating income ……………………

$130,000

Yes, the increase in fixed selling expenses would be justified.

2.

Variable manufacturing cost per unit ………………..

$16.80

*

Import duties per unit …………………………………..

1.70

Permits and licenses ($9,000 ÷ 20,000 units) ……..

0.45

Shipping cost per unit ……………………………………

3.20

Break-even price per unit ……………………………….

$22.15

*$10 + $4.50 + $2.30 = $16.80.

3. The relevant cost is $1.20 per unit, which is the variable selling expense

per Dak. Because the irregular units have already been produced, all

4. If the plant operates at 30% of normal levels, then only 3,000 units will

Problem 10-18A (continued)

Given this information, the simplest approach to the solution is:

Contribution margin lost if the plant is closed

(3,000 units × $14 per unit*) ……………………..

$(42,000)

Fixed costs that can be avoided if the plant is

closed:

Fixed manufacturing overhead cost ($300,000

× 2/12 = $50,000; $50,000 × 40%) ………….

$20,000

Fixed selling cost ($210,000 × 2/12 =

$35,000; $35,000 × 20%) ……………………….

7,000

27,000

Net disadvantage of closing the plant ……………..

$(15,000)

*$32.00 – ($10.00 + $4.50 + $2.30 + $1.20) = $14.00

Some students will take a longer approach such as that shown below:

Continue

to

Operate

Close the

Plant

Sales (3,000 units × $32 per unit) ……………

$ 96,000

$ 0

Variable expenses (3,000 units × $18 per

unit) ………………………………………………..

54,000

0

Contribution margin ………………………………

42,000

0

Fixed expenses:

Fixed manufacturing overhead cost:

$300,000 × 2/12 ……………………………..

50,000

$300,000 × 2/12 × 60% …………………..

30,000

Fixed selling expense:

$210,000 × 2/12 ……………………………..

35,000

$210,000 × 2/12 × 80% …………………..

28,000

Total fixed expenses ……………………………..

85,000

58,000

Net operating income (loss) ……………………

$(43,000)

$(58,000)

Problem 10-18A (continued)

5. The relevant costs are those that can be avoided by purchasing from the

outside manufacturer. These costs are:

Variable manufacturing costs …………………………………

$16.80

Fixed manufacturing overhead cost ($300,000 × 75%

= $225,000; $225,000 ÷ 60,000 units) …………………

3.75

Variable selling expense ($1.20 × 1/3) …………………….

0.40

Total costs avoided ……………………………………………..

$20.95

To be acceptable, the outside manufacturer’s quotation must be

less

than $20.95 per unit.

Problem 10-19A (60 minutes)

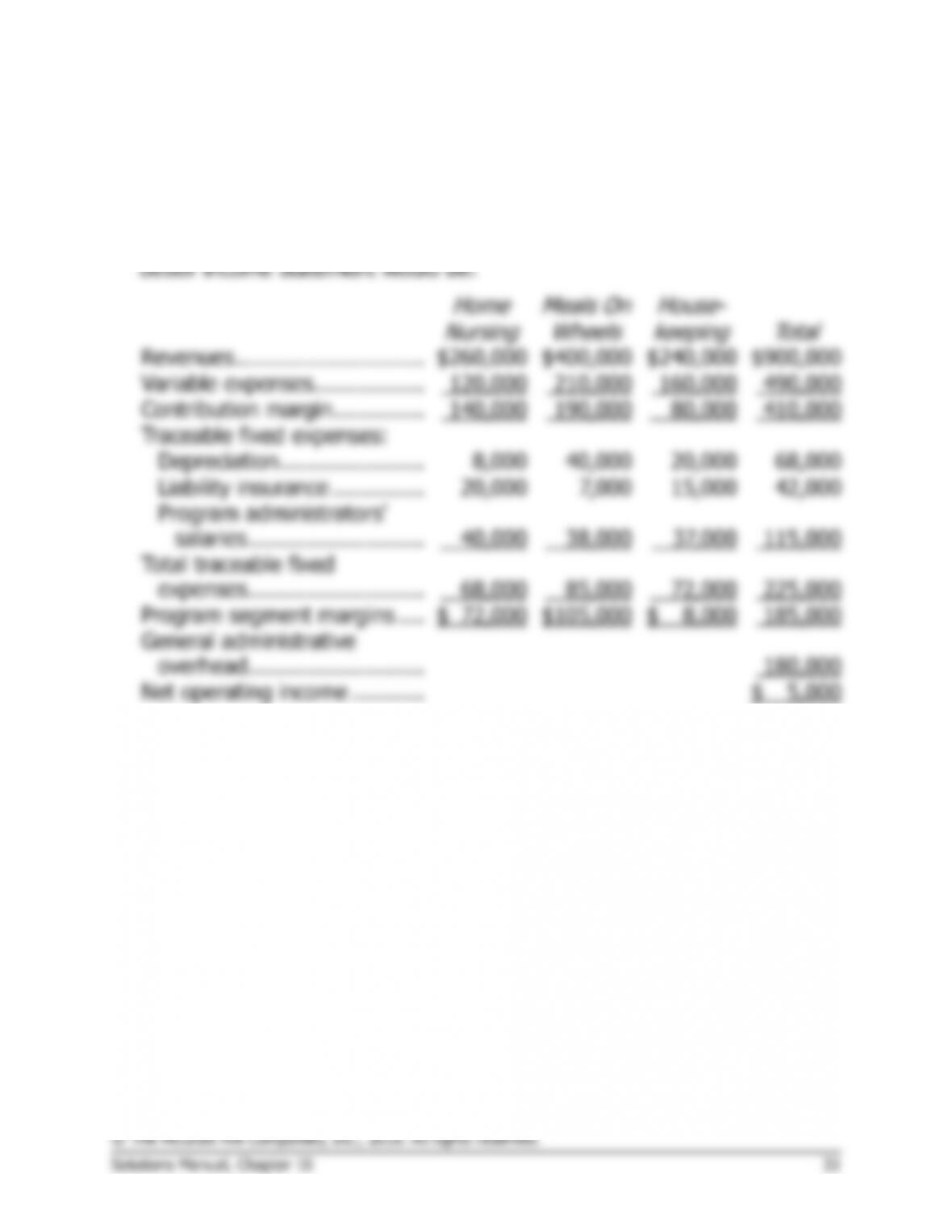

1. No, the Housekeeping program should not be discontinued. It is actually

generating a positive program segment margin and is, of course,

providing a valuable service to seniors. Computations to support this

conclusion follow:

Contribution margin lost if the Housekeeping

program is dropped ……………………………………

$(80,000)

Fixed costs that can be avoided:

Liability insurance ………………………………………

$15,000

Program administrator’s salary ………………………

37,000

52,000

Decrease in net operating income for the

organization as a whole……………………………….

$(28,000)

Depreciation on the van is a sunk cost and the van has no salvage value

since it would be donated to another organization. The general

administrative overhead is allocated and none of it would be avoided if

the program were dropped; thus it is not relevant to the decision.

The same result can be obtained with the alternative analysis below:

Current

Total

Total If

House-

keeping Is

Dropped

Difference:

Net

Operating

Income

Increase or

(Decrease)

Revenues …………………………..….

$900,000

$660,000

$(240,000)

Variable expenses ……………………

490,000

330,000

160,000

Contribution margin …………………

410,000

330,000

(80,000)

Fixed expenses:

Depreciation* ………………………

68,000

68,000

0

Liability insurance …………………

42,000

27,000

15,000

Program administrators’ salaries

115,000

78,000

37,000

General administrative overhead

180,000

180,000

0

Total fixed expenses ………………..

405,000

353,000

52,000

Net operating income (loss) ………

$ 5,000

$(23,000)

$ (28,000)

*Includes pro-rated loss on disposal of the van if it is donated to a

charity.

Problem 10-19A (continued)

2. To give the administrator of the entire organization a clearer picture of

the financial viability of each of the organization’s programs, the general

administrative overhead should not be allocated. It is a common cost

that should be deducted from the total program segment margin. A

Problem 10-20A (15 minutes)

1.

Per 16-Ounce

T-Bone

Sales from further processing:

Sales price of one filet mignon (6 ounces ×

$4.00 per pound ÷ 16 ounces per pound) …..

$1.50

Sales price of one New York cut (8 ounces ×

$2.80 per pound ÷ 16 ounces per pound) …..

1.40

Total revenue from further processing …………….

2.90

Less sales revenue from one T-bone steak ……….

2.25

Incremental revenue from further processing ……

0.65

Less cost of further processing ………………………

0.25

Profit per pound from further processing …………

$0.40

2. The T-bone steaks should be processed further into the filet mignon and

the New York cut. This will yield $0.40 per pound in added profit for the

Problem 10-21A (30 minutes)

1.

Contribution margin lost if the flight is

discontinued ……………………………………………..

$(12,950)

Flight costs that can be avoided if the flight is

discontinued:

Flight promotion ………………………………………..

$ 750

Fuel for aircraft ………………………………………….

5,800

Liability insurance (1/3 × $4,200) ………………….

1,400

Salaries, flight assistants ……………………………..

1,500

Overnight costs for flight crew and assistants …..

300

9,750

Net decrease in profits if the flight is discontinued .

$ (3,200)

The following costs are not relevant to the decision:

Cost

Reason

Salaries, flight crew

Fixed annual salaries, which will

not change.

Depreciation of aircraft

Sunk cost.

Liability insurance (two-thirds)

Two-thirds of the liability insurance

is unaffected by this decision.

Baggage loading and flight

preparation

This is an allocated cost that will

continue even if the flight is

discontinued.

Problem 10-21A (continued)

Alternative Solution:

Keep the

Flight

Drop the

Flight

Difference:

Net

Operating

Income

Increase or

(Decrease)

Ticket revenue ………………………………..

$14,000

$ 0

$(14,000)

Variable expenses …………………………….

1,050

0

1,050

Contribution margin ………………………….

12,950

0

(12,950)

Less flight expenses:

Salaries, flight crew ………………………..

1,800

1,800

0

Flight promotion …………………………...

750

0

750

Depreciation of aircraft ……………………

1,550

1,550

0

Fuel for aircraft ……………………………..

5,800

0

5,800

Liability insurance ………………………….

4,200

2,800

1,400

Salaries, flight assistants …………………

1,500

0

1,500

Baggage loading and flight preparation

1,700

1,700

0

Overnight costs for flight crew and

assistants at destination………………..

300

0

300

Total flight expenses …………………………

17,600

7,850

9,750

Net operating loss …………………………...

$ (4,650)

$ (7,850)

$ (3,200)

2. The goal of increasing the seat occupancy could be obtained by

eliminating flights with a lower-than-average seat occupancy. By

eliminating these flights and keeping the flights with a higher-than-

Problem 10-22A (30 minutes)

1. Because the fixed costs will not change as a result of the order, they are

not relevant to the decision. The cost of the new machine is relevant,

and this cost will have to be recovered by the current order because

there is no assurance of future business from the retail chain.

Unit

Total—

5,000 units

Sales from the order ($50 × 84%) ………………….

$42

$210,000

Less costs associated with the order:

Direct materials ………………………………………..

15

75,000

Direct labor ……………………………………………..

8

40,000

Variable manufacturing overhead ………………….

3

15,000

Variable selling expense ($4 × 25%) ……………..

1

5,000

Special machine ($10,000 ÷ 5,000 units) ……….

2

10,000

Total costs …………………………………………………

29

145,000

Net increase in profits …………………………………..

$13

$ 65,000

2.

Sales from the order:

Reimbursement for costs of production (variable

production costs of $26 plus fixed manufacturing

overhead cost of $9 = $35 per unit; $35 per unit ×

5,000 units) …………………………..………………………

$175,000

Fixed fee ($1.80 per unit × 5,000 units) …………………

9,000

Total revenue ……………………………………………………..

184,000

Less incremental costs—variable production costs

($26 per unit × 5,000 units) ………………………………..

130,000

Net increase in profits …………………………………………..

$ 54,000

3.

Sales:

From the U.S. Army (above) …………………………..……

$184,000

From regular channels ($50 per unit × 5,000 units) ….

250,000

Net decrease in revenue ……………………………………….

(66,000)

Less variable selling expenses avoided if the Army’s

order is accepted ($4 per unit × 5,000 units) ………….

20,000

Net decrease in profits if the Army’s order is accepted …

$(46,000)

Note: This answer assumes that regular customers will return after this

one-time special order rather than buy from a competitor in the future.

Problem 10-23A (60 minutes)

1. The $90,000 in fixed overhead cost charged to the new product is a

common cost that will be the same whether the tubes are produced

internally or purchased from the outside. Hence, it is not relevant. The

variable manufacturing overhead per box of Chap-Off would be $0.50,

as shown below:

Total manufacturing overhead cost per box of Chap-Off ..

$1.40

Less fixed portion ($90,000 ÷ 100,000 boxes) …………….

0.90

Variable overhead cost per box ………………………………..

$0.50

The total variable cost of producing one box of Chap-Off would be:

Direct materials …………………………..……………………….

$3.60

Direct labor …………………………………………………………

2.00

Variable manufacturing overhead …………………………….

0.50

Total variable cost per box ……………………………………..

$6.10

If the tubes for the Chap-Off are purchased from the outside supplier,

then the variable cost per box of Chap-Off would be:

Direct materials ($3.60 × 75%) ……………………………….

$2.70

Direct labor ($2.00 × 90%) …………………………………….

1.80

Variable manufacturing overhead ($0.50 × 90%) ………..

0.45

Cost of tube from outside ………………………………………

1.35

Total variable cost per box ……………………………………..

$6.30

Therefore, the company should reject the outside supplier’s offer. A

savings of $0.20 per box of Chap-Off will be realized by producing the

tubes internally.

Problem 10-23A (continued)

Another approach to the solution would be:

Cost avoided by purchasing the tubes:

Direct materials ($3.60 × 25%) ………………………

$0.90

Direct labor ($2.00 × 10%) …………………………...

0.20

Variable manufacturing overhead ($0.50 × 10%) ..

0.05

Total costs avoided …………………………………………

$1.15

*

Cost of purchasing the tubes from the outside ……..

$1.35

Cost savings per box by making internally ……………

$0.20

*

This $1.15 is the cost of making one box of tubes internally

because it represents the overall cost savings that will be

realized per box of Chap-Off by purchasing the tubes from the

supplier.

2. The maximum purchase price would be $1.15 per box. The company

would not be willing to pay more than this amount because the $1.15

Problem 10-23A (continued)

3. At a volume of 120,000 boxes, the company should buy the tubes. The

computations are:

Cost of making 120,000 boxes:

120,000 boxes × $1.15 per box ……………….

$138,000

Rental cost of equipment ………………………..

40,000

Total cost ………………………………………………

$178,000

Cost of buying 120,000 boxes:

120,000 boxes × $1.35 per box ……………….

$162,000

Or, on a total cost basis, the computations are:

Cost of making 120,000 boxes:

120,000 boxes × $6.10 per box ……………….

$732,000

Rental cost of equipment ………………………..

40,000

Total cost ………………………………………………

$772,000

Cost of buying 120,000 boxes:

120,000 boxes × $6.30 per box ……………….

$756,000

Thus, buying the boxes will save the company $16,000 per year.