Problem 8-18B (45 minutes)

1. a.

Standard Quantity Allowed

for Actual Output,

at Standard Price

(SQ × SP)

Actual Quantity

of Input,

at Standard Price

(AQ × SP)

Actual Quantity

of Input,

at Actual Price

(AQ × AP)

28,000 pounds* ×

$2.50 per pound =

$70,000

27,800 pounds ×

$2.50 per pound =

$69,500

33,000 pounds ×

$2.95 per pound =

$97,350

Materials quantity

variance = $500 F

33,000 pounds ×

$2.50 per pound

= $82,500

Materials price variance

= 14,850 U

*8,000 ingots × 3.5 pounds per ingot = 28,000 pounds

Alternatively, the variances can be computed using the formulas:

Materials quantity variance = SP (AQ – SQ)

= $2.50 per pound (28,000 pounds – 27,800 pounds)

= $500 F

Materials price variance = AQ (AP – SP)

= 33,000 pounds ($2.95 per pound – $2.50 per pound)

= $14,850 U

Problem 8-18B (continued)

1. b.

Standard Hours Allowed

for Actual Output,

at Standard Rate

(SH × SR)

Actual Hours of Input,

at Standard Rate

(AH × SR)

Actual Hours of Input,

at Actual Rate

(AH × AR)

3,200 hours* ×

$6.50 per hour

= $20,800

3,800 hours ×

$6.50 per hour

= $24,700

3,800 hours ×

$6.20 per hour

= $23,560

Labor efficiency variance

= $3,900 U

Labor rate variance

= $1,140 F

Spending variance = $2,760 U

*8,000 ingots × 0.4 hour per ingot = 3,200 hours

Alternatively, the variances can be computed using the formulas:

Labor efficiency variance = SR (AH – SH)

= $6.50 per hour (3,200 hours – 3,800 hours)

= $3,900 U

Labor rate variance = AH (AR – SR)

= 3,800 hours ($6.20 per hour – $6.50 per hour)

= $1,140 F

Problem 8-18B (continued)

1. c.

Standard Hours Allowed

for Actual Output,

at Standard Rate

(SH × SR)

Actual Hours of Input,

at Standard Rate

(AH × SR)

Actual Hours of Input,

at Actual Rate

(AH × AR)

1,600 hours* ×

$2.00 per hour

= $3,200

1,900 hours ×

$2.00 per hour

= $3,800

$4,560

Variable overhead

efficiency variance

= $600 U

Variable overhead

rate variance

= $760 U

Spending variance = $1,360 U

*8,000 ingots × 0.2 hours per ingot = 1,600 hours

Alternatively, the variances can be computed using the formulas:

Variable overhead efficiency variance = SR (AH – SH)

= $2.00 per hour (1,900 hours – 1,600 hours)

= $600 U

Variable overhead rate variance = AH (AR – SR)

= 1,900 hours ($2.40 per hour* – $2.00 per hour)

= $760 U

*$4,560 ÷ 1,900 hours = $2.40 per hour

Problem 8-18B (continued)

2. Summary of variances:

Material quantity variance ………………….

$ 500

F

Material price variance ……………………..

14,850

U

Labor efficiency variance …………………..

3,900

U

Labor rate variance ………………………….

1,140

F

Variable overhead efficiency variance …..

600

U

Variable overhead rate variance ………….

760

U

Net variance …………………………………..

$18,470

U

Budgeted cost of goods sold at $11.75 per ingot ..

$ 94,000

Add the net unfavorable variance (as above) …….

18,470

Actual cost of goods sold ………………………………

$112,470

Budgeted net operating income ……………………..

$11,000

Deduct the net unfavorable variance added to

cost of goods sold for the month …………………

18,470

Net operating loss …………………………..………….

$(7,470)

3. The two most significant variances are the materials price variance and

the labor efficiency variance. Possible causes of the variances include:

Materials price variance:

Outdated standards, uneconomical

quantity purchased, higher quality

materials, high-cost method of transport.

Labor efficiency variance:

Poorly trained workers, poor quality

materials, faulty equipment, work

interruptions, inaccurate standards,

insufficient demand.

Problem 8-19B (30 minutes)

1.

Streeterville Pizza

Revenue and Spending Variances

For the Month Ended October 31

Flexible

Budget

Actual

Results

Revenue

and

Spending

Variances

Pizzas (q1) ………………………………..

2,100

2,100

Deliveries (q2) …………………………..

190

190

Revenue ($13.00q1) ……………………

$27,300

$27,840

$540

F

Expenses:

Pizza ingredients ($5.00q1) ………..

10,500

10,550

50

U

Kitchen staff ($5,800) ………………

5,800

5,740

60

F

Utilities ($520 + $0.10q1) ………….

730

855

125

U

Delivery person ($2.90q2) ………….

551

551

0

Delivery vehicle ($680 + $2.10q2) .

1,079

1,233

154

U

Equipment depreciation ($387) …..

387

387

0

Rent ($1,730) …………………………

1,730

1,730

0

Miscellaneous ($730 + $0.01q1) ….

751

743

8

F

Total expenses ………………………….

21,528

21,789

261

U

Net operating income …………………

$ 5,772

$ 6,051

$279

F

Problem 8-19B (continued)

2. The revenue variance of $540 F indicates that the average price per

pizza was higher than expected. Perhaps customers ordered more

toppings on their pizzas than expected. The pizza ingredients variance

Problem 8-20B (45 minutes)

1. a.

Standard Quantity Allowed

for Actual Output,

at Standard Price

(SQ × SP)

Actual Quantity of

Input,

at Standard Price

(AQ × SP)

Actual Quantity of

Input,

at Actual Price

(AQ × AP)

19,800 feet* ×

$3.00 per foot

= $59,400

19,250 feet** ×

$3.00 per foot

= $57,750

19,250 feet** ×

$3.20 per foot

= $61,600

Materials quantity

variance = $1,650 F

Materials price

variance = $3,850 U

Spending variance = $2,200 U

*

11,000 units × 1.80 feet per unit = 19,800 feet

**

11,000 units × 1.75 feet per unit = 19,250 feet

Alternatively, the variances can be computed using the formulas:

Materials quantity variance = SP (AQ – SQ)

= $3.00 per foot (19,250 feet – 19,800 feet)

= $1,650 F

Materials price variance = AQ (AP – SP)

= 19,250 feet ($3.20 per foot – $3.00 per foot)

= $3,850 U

Problem 8-20B (continued)

1. b.

Standard Hours Allowed

for Actual Output,

at Standard Rate

(SH × SR)

Actual Hours of Input,

at Standard Rate

(AH × SR)

Actual Hours of Input,

at Actual Rate

(AH × AR)

11,000 hours* ×

$16.00 per hour

= $176,000

11,550 hours** ×

$16.00 per hour

= $184,800

11,550 hours** ×

$15.40 per hour

= $177,870

Labor efficiency variance

= $8,800 U

Labor rate variance

= $6,930 F

Spending variance = $1,870 U

*

11,000 units × 1.00 hours per unit = 11,000 hours

**

11,000 units × 1.05 hours per unit = 11,550 hours

Alternatively, the variances can be computed using the formulas:

Labor efficiency variance = SR (AH – SH)

= $16.00 per hour (11,550 hours – 11,000 hours)

= $8,800 U

Labor rate variance = AH (AR – SR)

= 11,550 hours ($15.40 per hour – $16.00 per hour)

= $6,930 F

Problem 8-20B (continued)

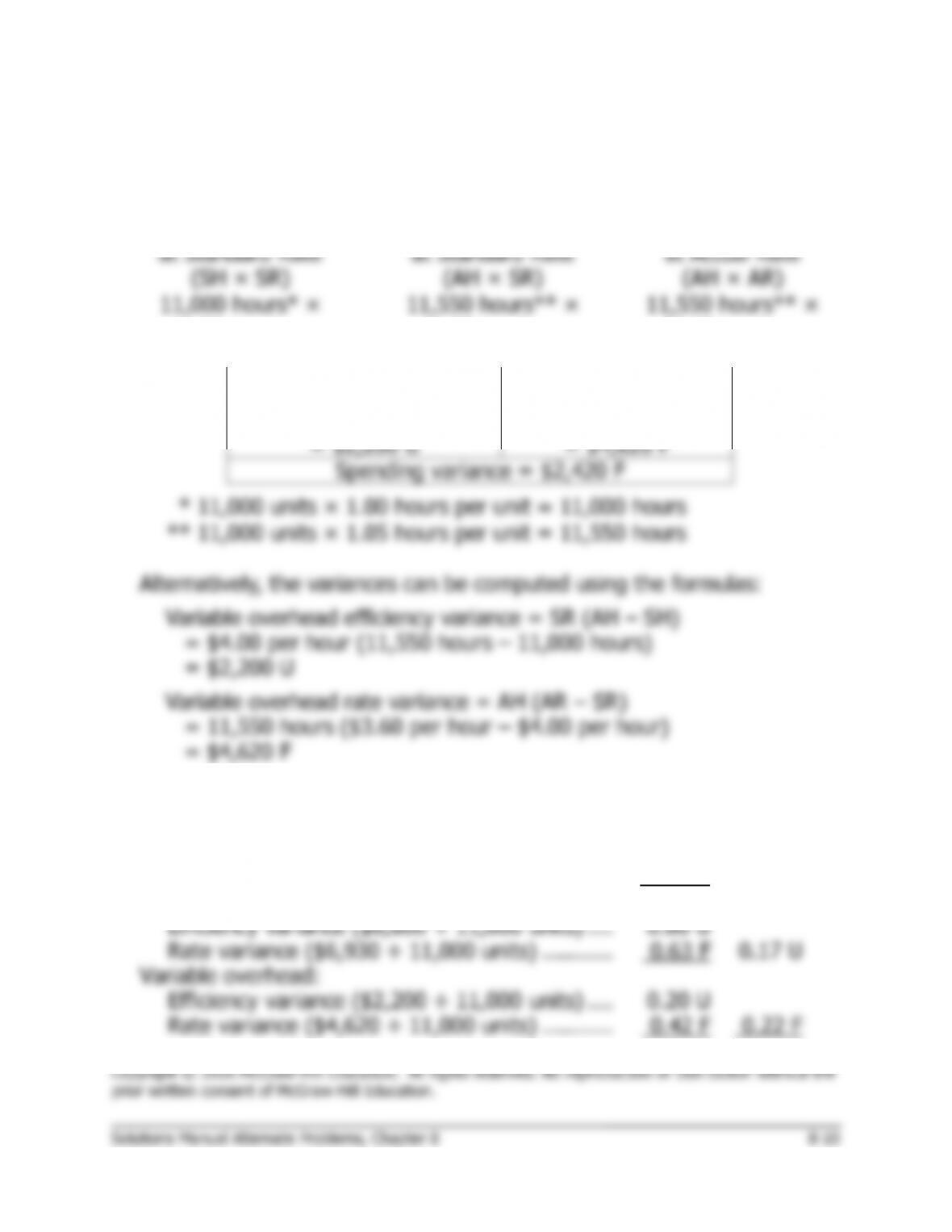

1. c.

Standard Hours Allowed

for Actual Output,

at Standard Rate

(SH × SR)

Actual Hours of Input,

at Standard Rate

(AH × SR)

Actual Hours of Input,

at Actual Rate

(AH × AR)

11,000 hours* ×

$4.00 per hour

= $44,000

11,550 hours** ×

$4.00 per hour

= $46,200

11,550 hours** ×

$3.60 per hour

=$41,580

Variable overhead

efficiency variance

= $2,200 U

Variable overhead

rate variance

= $4,620 F

Spending variance = $2,420 F

*

11,000 units × 1.00 hours per unit = 11,000 hours

**

11,000 units × 1.05 hours per unit = 11,550 hours

Alternatively, the variances can be computed using the formulas:

Variable overhead efficiency variance = SR (AH – SH)

= $4.00 per hour (11,550 hours – 11,000 hours)

= $2,200 U

Variable overhead rate variance = AH (AR – SR)

= 11,550 hours ($3.60 per hour – $4.00 per hour)

= $4,620 F

2.

Materials:

Quantity variance ($1,650 ÷ 11,000 units) ……

$0.15 F

Price variance ($3,850 ÷ 11,000 units) ………..

0.35 U

$0.20 U

Labor:

Efficiency variance ($8,800 ÷ 11,000 units) ….

0.80 U

Rate variance ($6,930 ÷ 11,000 units) ………..

0.63 F

0.17 U

Variable overhead:

Efficiency variance ($2,200 ÷ 11,000 units) ….

0.20 U

Rate variance ($4,620 ÷ 11,000 units) ………..

0.42 F

0.22 F

Excess of actual over standard cost per unit ……..

$0.15 U

Problem 8-20B (continued)

3. Both the labor efficiency and variable overhead efficiency variances are

affected by inefficient use of labor time.

Excess of actual over standard cost per unit …….

$0.15 U

Less portion attributable to labor inefficiency:

Labor efficiency variance ……………………………..

0.80 U

Variable overhead efficiency variance ……………..

0.20 U

1.00 U

Portion due to other variances ………………………

$0.85 F

In sum, had it not been for the apparent inefficient use of labor time,

the total variance in unit cost for the month would have been favorable

by $0.85 rather than unfavorable by $0.15.

4. Although the excess of actual cost over standard cost is only $0.15 per

unit, the total amount of $1,650 (= $0.15 per unit × 11,000 units) is

substantial. Moreover, the details of the variances are significant. The

Problem 8-21B (45 minutes)

1.

Standard

Quantity or

Hours

Standard Price

or Rate

Standard

Cost

Alpha8:

Direct materials—X342 ……

1.5 kilos

$3.40 per kilo

$ 5.10

Direct materials—Y561 ……

2.3 liters

$1.50 per liter

3.45

Direct labor—Sintering …….

0.20 hours

$18.00 per hour

3.60

Direct labor—Finishing …….

0.75 hours

$17.00 per hour

12.75

Total …………………………..

$24.90

Zeta9:

Direct materials—X342 ……

2.7 kilos

$3.40 per kilo

$ 9.18

Direct materials—Y561 ……

4.3 liters

$1.50 per liter

6.45

Direct labor—Sintering …….

0.35 hours

$18.00 per hour

6.30

Direct labor—Finishing …….

0.85 hours

$17.00 per hour

14.45

Total …………………………..

$36.38