Problem 6-23B (60 minutes)

1.

a.

Absorption costing unit product cost is:

Direct materials …………………………………….

$7.40

Direct labor ………………………………………….

3.00

Variable manufacturing overhead ……………..

1.70

Fixed manufacturing overhead

($194,400 ÷ 24,000 units) ……………………

8.10

Absorption costing unit product cost ………….

$20.20

b.

The absorption costing income statement is:

Sales (21,000 units) ………………………………………….

$ 762,300

Cost of goods sold (21,000 units × $20.20 per unit) …

424,200

Gross margin …………………………………………………..

338,100

Selling and administrative expenses

($219,000 + 21,000 units × $7.70 per unit) …………

380,700

Net operating income (loss) ………………………………..

$(42,600)

c.

The reconciliation is as follows:

Variable costing net operating loss ……………………….

$ (66,900)

Add fixed manufacturing overhead cost deferred in

inventory under absorption costing

(3,000 units × $8.10 per unit) …………………………..

24,300

Absorption costing net operating income ……………….

$(42,600)

Problem 6-23B (continued)

2.

a.

The variable costing income statement is:

Sales (27,000 units × $36.30 per unit) ………..

$980,100

Variable expenses:

Variable cost of goods sold

(27,000 units × $12.10 per unit) ……………

$326,700

Variable selling and administrative expenses

(27,000 units × $7.70 per unit) …………….

207,900

534,600

Contribution margin ………………………………..

445,500

Fixed expense:

Fixed manufacturing overhead…………………

194,400

Fixed selling and administrative expense ……

219,000

413,400

Net operating income ………………………………

$ 32,100

b.

The absorption costing income statement would be constructed as

follows:

The absorption costing unit product cost will remain at $20.20, the

same as in part (1).

Sales (27,000 units × $36.30 per unit) ……………………..

$980,100

Cost of goods sold (27,000 units × $20.20 per unit) …….

545,400

Gross margin ………………………………………………………

434,700

Selling and administrative expenses

(27,000 units × $7.70 per unit + $219,000) …………….

426,900

Net operating income ……………………………………………

$ 7,800

c.

The reconciliation is as follows:

Variable costing net operating income ………………………

$32,100

Deduct fixed manufacturing overhead cost released

from inventory under absorption costing (3,000 units

× $8.10 per unit) ……………………………………………….

24,300

Absorption costing net operating income …………………..

$ 7,800

Problem 6-24B (60 minutes)

1. The disadvantages or weaknesses of the company’s version of a

segmented income statement are as follows:

a. The company should include a column showing the combined results

2. Corporate advertising expenses may have apparently been allocated on

the basis of sales dollars although a consistent percentage was not

used. The general administrative expenses have apparently been

Problem 6-24B (continued)

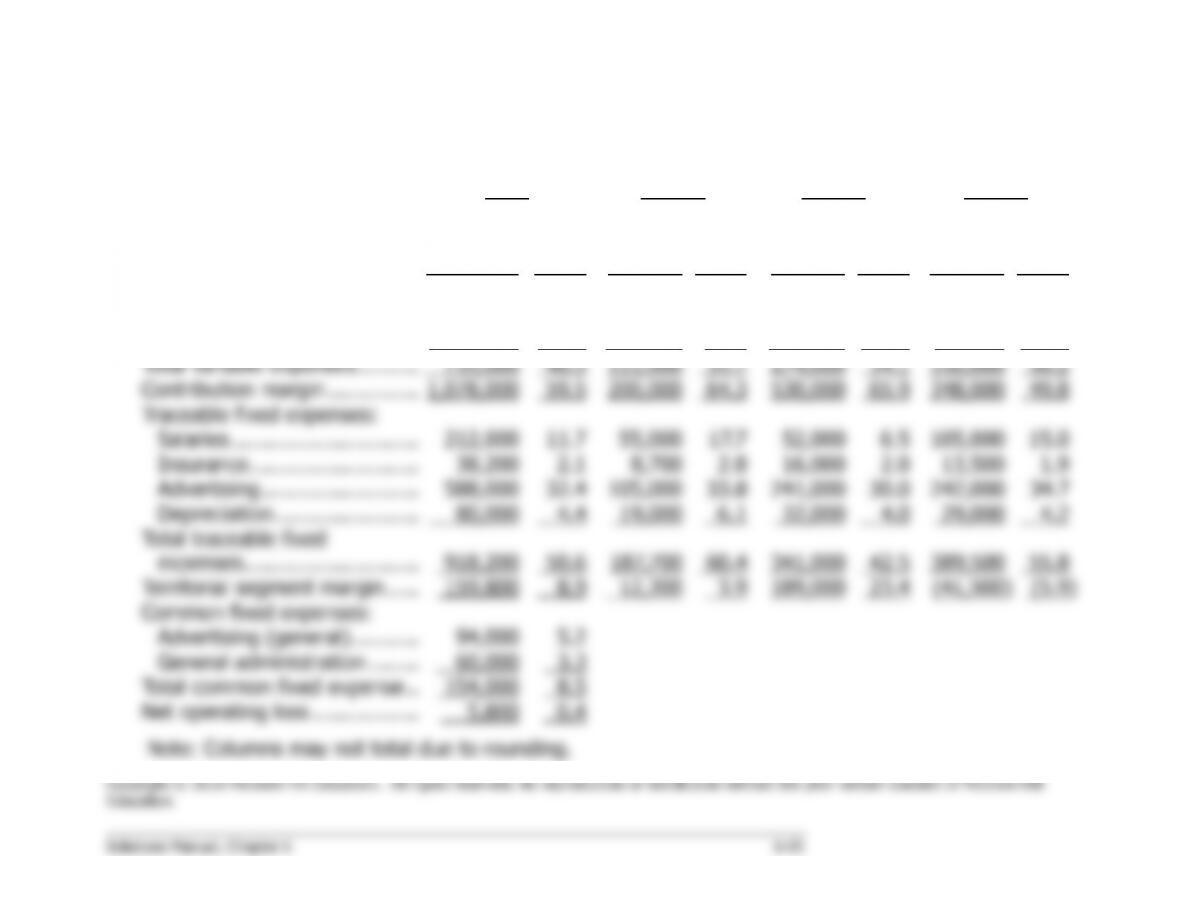

Total

Southern

Europe

Middle

Europe

Northern

Europe

Amount

in €s

%

Amount

in €s

%

Amount

in €s

%

Amount

in €s

%

Sales ……………………………….

1,813,000

100.0

311,000

100.0

804,000

100.0

698,000

100.0

Variable expenses:

Cost of goods sold ……………

649,000

35.8

98,000

31.5

240,000

29.9

311,000

44.6

Shipping expense …………….

86,000

4.7

13,000

4.2

34,000

4.2

39,000

5.6

Total variable expenses ………..

735,000

40.5

111,000

35.7

274,000

34.1

350,000

50.2

Contribution margin …………….

1,078,000

59.5

200,000

64.3

530,000

65.9

348,000

49.8

Traceable fixed expenses:

Salaries ………………………….

212,000

11.7

55,000

17.7

52,000

6.5

105,000

15.0

Insurance ……………………….

38,200

2.1

8,700

2.8

16,000

2.0

13,500

1.9

Advertising ……………………..

588,000

32.4

105,000

33.8

241,000

30.0

242,000

34.7

Depreciation ……………………

80,000

4.4

19,000

6.1

32,000

4.0

29,000

4.2

Total traceable fixed

expenses ………………………..

918,200

50.6

187,700

60.4

341,000

42.5

389,500

55.8

Territorial segment margin ……

159,800

8.9

12,300

3.9

189,000

23.4

(41,500)

(5.9)

Common fixed expenses:

Advertising (general)…………

94,000

5.2

General administration ………

60,000

3.3

Total common fixed expense …

154,000

8.5

Net operating loss ………………

5,800)

0.4)

Note: Columns may not total due to rounding.

Problem 6-24B (continued)

4. The following points should be brought to the attention of management:

a. Sales in Southern Europe are much lower than in the other two

territories. This is not due to lack of salespeople—salaries in Southern

only 49.8%, as compared to 65.9% and 64.3% for the other two

territories.

d. Northern Europe may be overstaffed. Its total salaries are much

company.

Problem 6-25B (75 minutes)

1.

Year 1

Year 2

Year 3

Unit sales ……………………………..

40,000

32,000

40,000

Sales …………………………………..

$1,000,000

$ 800,000

$1,000,000

Variable expenses:

Variable cost of goods sold @

$4 per unit ……………………….

160,000

128,000

160,000

Variable selling and

administrative @ $4 per unit ..

160,000

128,000

160,000

Total variable expenses ……………

320,000

256,000

320,000

Contribution margin ………………..

680,000

544,000

680,000

Fixed expenses:

Fixed manufacturing overhead ..

600,000

600,000

600,000

Fixed selling and administrative

70,000

70,000

70,000

Total fixed expenses ……………….

670,000

670,000

670,000

Net operating income (loss) ……..

$ 10,000

$(126,000)

$ 10,000

Problem 6-25B (continued)

2.

a.

Year 1

Year 2

Year 3

Variable manufacturing cost ………….

$ 4.00

$ 4.00

$ 4.00

Fixed manufacturing cost:

$600,000 ÷ 40,000 units ……………

15.00

$600,000 ÷ 50,000 units ……………

12.00

$600,000 ÷ 32,000 units ……………

18.75

Absorption costing unit product cost .

$19.00

$16.00

$22.75

b.

Variable costing net operating

income (loss) ………………………….

$10,000

$(126,000)

$ 10,000

Add (deduct) fixed manufacturing

overhead cost deferred in

(released from) inventory from

Year 2 to Year 3 under absorption

costing (18,000 units × $12.00

per unit) ………………………………..

216,000

(216,000)

Add fixed manufacturing overhead

cost deferred in inventory from

Year 3 to the future under

absorption costing (10,000 units ×

$18.75 per unit) ………………………

187,500

Absorption costing net operating

income (loss) ………………………….

$10,000

$ 90,000

$(18,500)

3. Production went up sharply in Year 2 thereby reducing the unit product

cost, as shown in (2a). This reduction in cost, combined with the large

4. The fixed manufacturing overhead cost deferred in inventory from Year

2 was charged against Year 3 operations, as shown in the reconciliation

Problem 6-25B (continued)

5. a. With lean production, production would have been geared to sales in

each year so that little or no inventory of finished goods would have

been built up in either Year 2 or Year 3.

b. If lean production had been in use, the net operating income under

absorption costing would have been the same as under variable

Problem 6-26B (45 minutes)

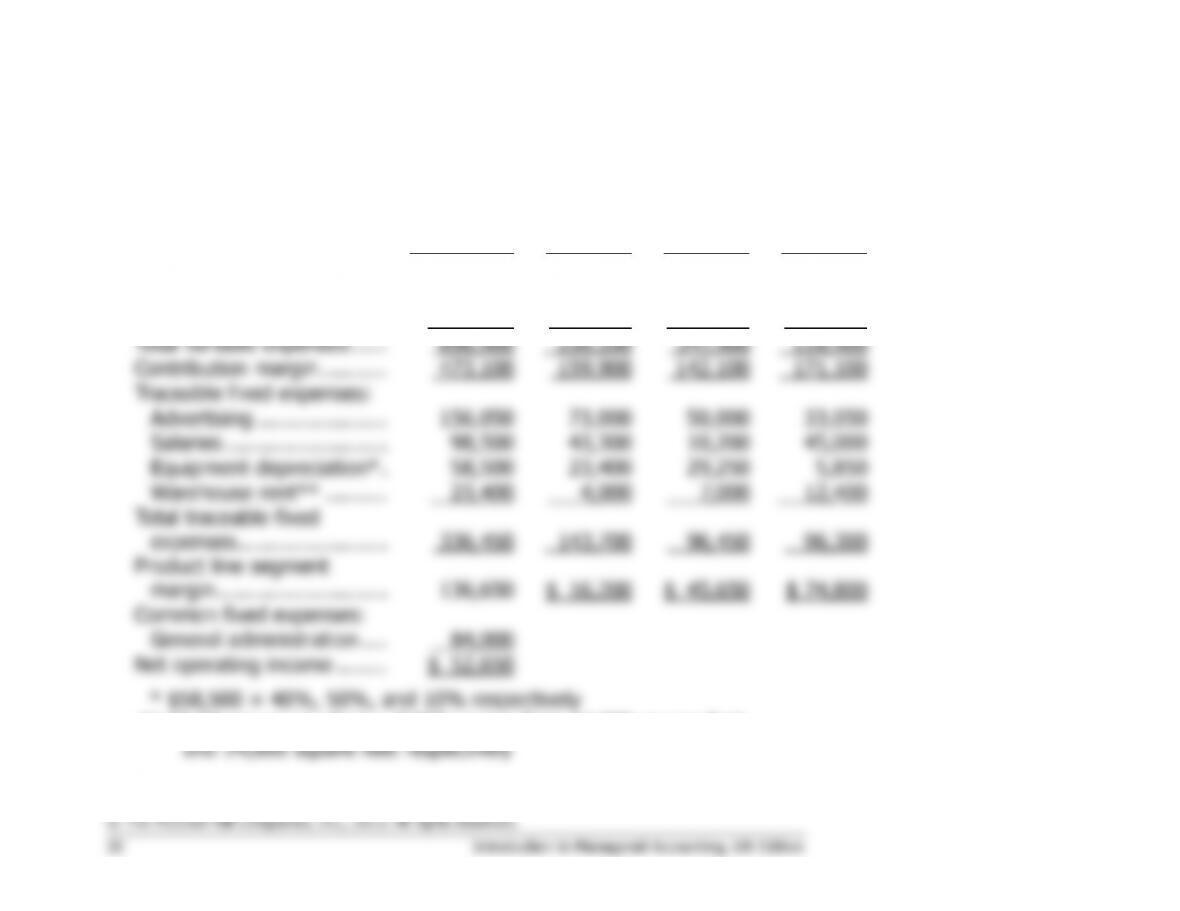

1. The segmented income statement follows:

Total

Company

Wheat

Cereal

Pancake

Mix

Flour

Sales …………………………..

$1,170,000

$390,000

$490,000

$290,000

Variable expenses:

Materials, labor & other …

579,900

191,100

298,900

89,900

Sales commissions ……….

117,000

39,000

49,000

29,000

Total variable expenses ……

696,900

230,100

347,900

118,900

Contribution margin ………..

473,100

159,900

142,100

171,100

Traceable fixed expenses:

Advertising …………………

156,050

73,000

50,000

33,050

Salaries ……………………..

98,500

43,300

10,200

45,000

Equipment depreciation* .

58,500

23,400

29,250

5,850

Warehouse rent** ……….

23,400

4,000

7,000

12,400

Total traceable fixed

expenses ……………………

336,450

143,700

96,450

96,300

Product line segment

margin ………………………

136,650

$ 16,200

$ 45,650

$ 74,800

Common fixed expenses:

General administration ….

84,000

Net operating income ……..

$ 52,650

*

$58,500 × 40%, 50%, and 10% respectively

**

$0.50 per square foot × 8,000 square feet, 14,000 square feet,

and 24,800 square feet respectively

Problem 6-26B (continued)

2. a. No, the wheat cereal should not be eliminated. The wheat cereal product is covering all of its own

costs and is generating a $16,200 segment margin toward covering the company’s common costs

and toward profits. (Note: Problems relating to the elimination of a product line are covered in

more depth in a later chapter.)

b.

Wheat

Cereal

Pancake

Mix

Flour

Contribution margin (a) ……………..

$159,900

$142,100

$171,100

Sales (b) …………………………………

$390,000

$490,000

$290,000

Contribution margin ratio (a) ÷ (b) .

41%

29%

59%

It is probably unwise to focus all available resources on promoting the pancake mix. The company

is already spending nearly as much on the promotion of this product as on the other two products

together. Furthermore, the pancake mix has the lowest contribution margin ratio of the three

products. Therefore, a dollar of sales of the pancake mix generates less profit than a dollar of sales

of either of the two other products. Nevertheless, we cannot say for sure which product should be

emphasized in this situation without more information. The problem states that there is ample

demand for all three products, which suggests that there is no idle capacity. If the equipment is

being fully utilized, increasing the production of any one product would probably require cutting

back production of the other products. In a later chapter we will discuss how to choose the most

profitable product when a production constraint forces such a trade-off among products.