Problem 4-13B (45 minutes)

1.

Equivalent Units of Production

Materials

Conversion

Transferred to next department* ………………….

420,000

420,000

Ending work in process:

Materials: 33,000 units x 80% complete ………

26,400

Conversion: 33,000 units x 20% complete ……

6,600

Equivalent units of production ……………………..

446,400

426,600

* Units transferred to the next department = Units in beginning work in

process + Units started into production − Units in ending work in

process = 73,000 + 380,000 − 33,000 = 420,000

2.

Cost per Equivalent Unit

Materials

Conversion

Cost of beginning work in process …………….

$111,600

$ 55,800

Cost added during the period …………………..

580,320

306,810

Total cost (a) ……………………………………….

$691,920

$362,610

Equivalent units of production (b) …………….

446,400

426,600

Cost per equivalent unit, (a) ÷ (b) ……………

$1.55

$0.85

Problem 4-13B (continued)

3.

Cost of Ending Work in Process Inventory and Units Transferred Out

Materials

Conversion

Total

Ending work in process inventory:

Equivalent units of production

(materials: 33,000 units x 80%

complete; conversion: 33,000

units x 20% complete) …….

26,400

6,600

Cost per equivalent unit …….

$1.55

$0.85

Cost of ending work in process

inventory ………………………

$40,920

$5,610

$46,530

Units completed and transferred out:

Units transferred to the next

department …………………..

420,000

420,000

Cost per equivalent unit …….

$1.55

$0.85

Cost of units completed and

transferred out ……………….

$651,000

$357,000

$1,008,000

4.

Cost Reconciliation

Costs to be accounted for:

Cost of beginning work in process inventory

($111,600 + $55,800) …………………………..

$ 167,400

Costs added to production during the period

($580,320 + $306,810) …………………………

887,130

Total cost to be accounted for …………………..

$1,054,530

Costs accounted for as follows:

Cost of ending work in process inventory ……

$ 46,530

Cost of units completed and transferred out ..

1,008,000

Total cost accounted for ………………………….

$1,054,530

Problem 4-14B (45 minutes)

Weighted-Average Method

1.

Equivalent Units of Production

Materials

Conversion

Transferred to next department ……………………

382,500

382,500

Ending work in process:

Materials: 90,000 units x 75% complete ………

67,500

Conversion: 90,000 units x 25% complete ……

22,500

Equivalent units of production ……………………..

450,000

405,000

2.

Cost per Equivalent Unit

Materials

Conversion

Cost of beginning work in process …………….

$ 31,500

$ 11,300

Cost added during the period …………………..

337,500

239,800

Total cost (a) ……………………………………….

$369,000

$251,100

Equivalent units of production (b) …………….

450,000

405,000

Cost per equivalent unit, (a) ÷ (b) ……………

$0.82

$0.62

3.

Applying Costs to Units

Materials

Conversion

Total

Ending work in process inventory:

Equivalent units of production

67,500

22,500

Cost per equivalent unit …….

$0.82

$0.62

Cost of ending work in process

inventory ………………………

$55,350

$13,950

$69,300

Units completed and transferred out:

Units transferred to the next

department …………………..

382,500

382,500

Cost per equivalent unit …….

$0.82

$0.62

Cost of units completed and

transferred out ……………….

$313,650

$237,150

$550,800

Problem 4-14B (continued)

4.

Cost Reconciliation

Costs to be accounted for:

Cost of beginning work in process inventory

($31,500 + $11,300) …………………………….

$ 42,800

Costs added to production during the period

($337,500 + $239,800) …………………………

577,300

Total cost to be accounted for …………………..

$620,100

Costs accounted for as follows:

Cost of ending work in process inventory ……

$ 69,300

Cost of units completed and transferred out ..

550,800

Total cost accounted for ………………………….

$620,100

Problem 4-15B (45 minutes)

Weighted-Average Method

1.

Equivalent units of production

Materials

Conversion

Transferred to next department* ………………….

307,000

307,000

Ending work in process:

Materials: 88,000 units x 100% complete …….

88,000

Conversion: 88,000 units x 70% complete ……

61,600

Equivalent units of production ……………………..

395,000

368,600

2.

Cost per equivalent unit

Materials

Conversion

Cost of beginning work in process …………….

$219,000

$ 88,000

Cost added during the period …………………..

709,250

280,600

Total cost (a) ……………………………………….

$928,250

$368,600

Equivalent units of production (b) …………….

395,000

368,600

Cost per equivalent unit, (a) ÷ (b) ……………

$2.35

$1.00

3.

Cost of ending work in process inventory and units transferred out

Materials

Conversion

Total

Ending work in process inventory:

Equivalent units of production…

88,000

61,600

Cost per equivalent unit ………..

$2.35

$1.00

Cost of ending work in process

inventory ………………………….

$206,800

$61,600

$268,400

Units completed and transferred out:

Units transferred to the next

department ………………………

307,000

307,000

Cost per equivalent unit ………..

$2.35

$1.00

Cost of units completed and

transferred out …………………..

$721,450

$307,000

$1,028,450

Problem 4-16B (45 minutes)

Weighted-Average Method

1.

a.

Work in Process—Blending ………………………………………

154,600

Work in Process—Bottling ………………………………………..

45,000

Raw Materials …………………………..………………………

199,600

b.

Work in Process—Blending ………………………………………

79,200

Work in Process—Bottling ………………………………………..

17,200

Salaries and Wages Payable ………………………………..

96,400

c.

Manufacturing Overhead …………………………………………

716,000

Accounts Payable ………………………………………………

716,000

d.

Work in Process—Blending ………………………………………

489,000

Manufacturing Overhead …………………………………….

489,000

Work in Process—Bottling ………………………………………..

110,000

Manufacturing Overhead …………………………………….

110,000

e.

Work in Process—Bottling ………………………………………..

632,000

Work in Process—Blending ………………………………….

632,000

f.

Finished Goods ……………………………………………………..

710,000

Work in Process—Bottling ……………………………………

710,000

g.

Accounts Receivable ……………………………………………….

1,360,000

Sales ………………………………………………………………

1,360,000

Cost of Goods Sold …………………………………………………

640,000

Finished Goods …………………………………………………

640,000

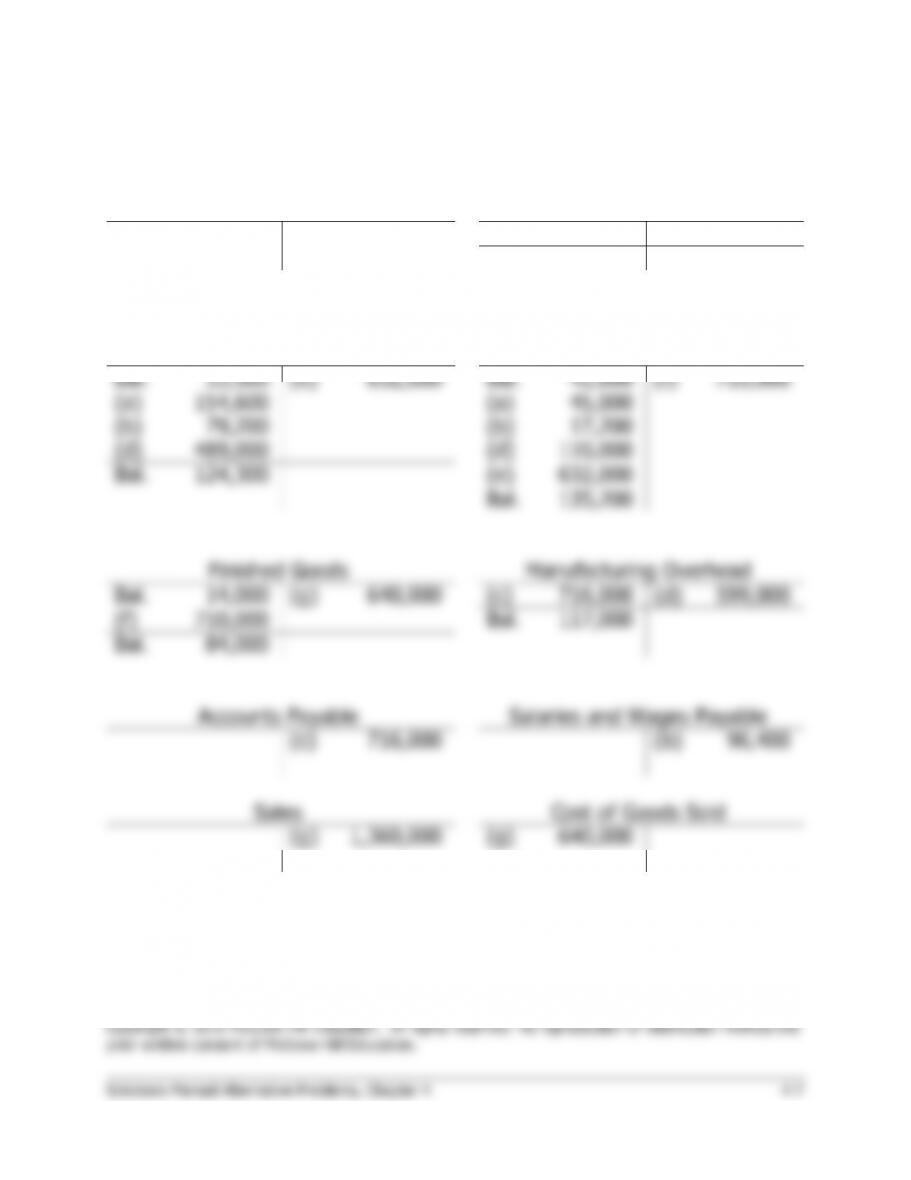

Problem 4-16B (continued)

2.

Accounts Receivable

Raw Materials

(g)

1,360,000

Bal.

214,600

(a)

199,600

Bal.

15,000

Work in Process

Blending Department

Work in Process

Bottling Department

Bal.

33,500

(e)

632,000

Bal.

41,000

(f)

710,000

(a)

154,600

(a)

45,000

(b)

79,200

(b)

17,200

(d)

489,000

(d)

110,000

Bal.

124,300

(e)

632,000

Bal.

135,200

Finished Goods

Manufacturing Overhead

Bal.

14,000

(g)

640,000

(c)

716,000

(d)

599,000

(f)

710,000

Bal.

117,000

Bal.

84,000

Accounts Payable

Salaries and Wages Payable

(c)

716,000

(b)

96,400

Sales

Cost of Goods Sold

(g)

1,360,000

(g)

640,000

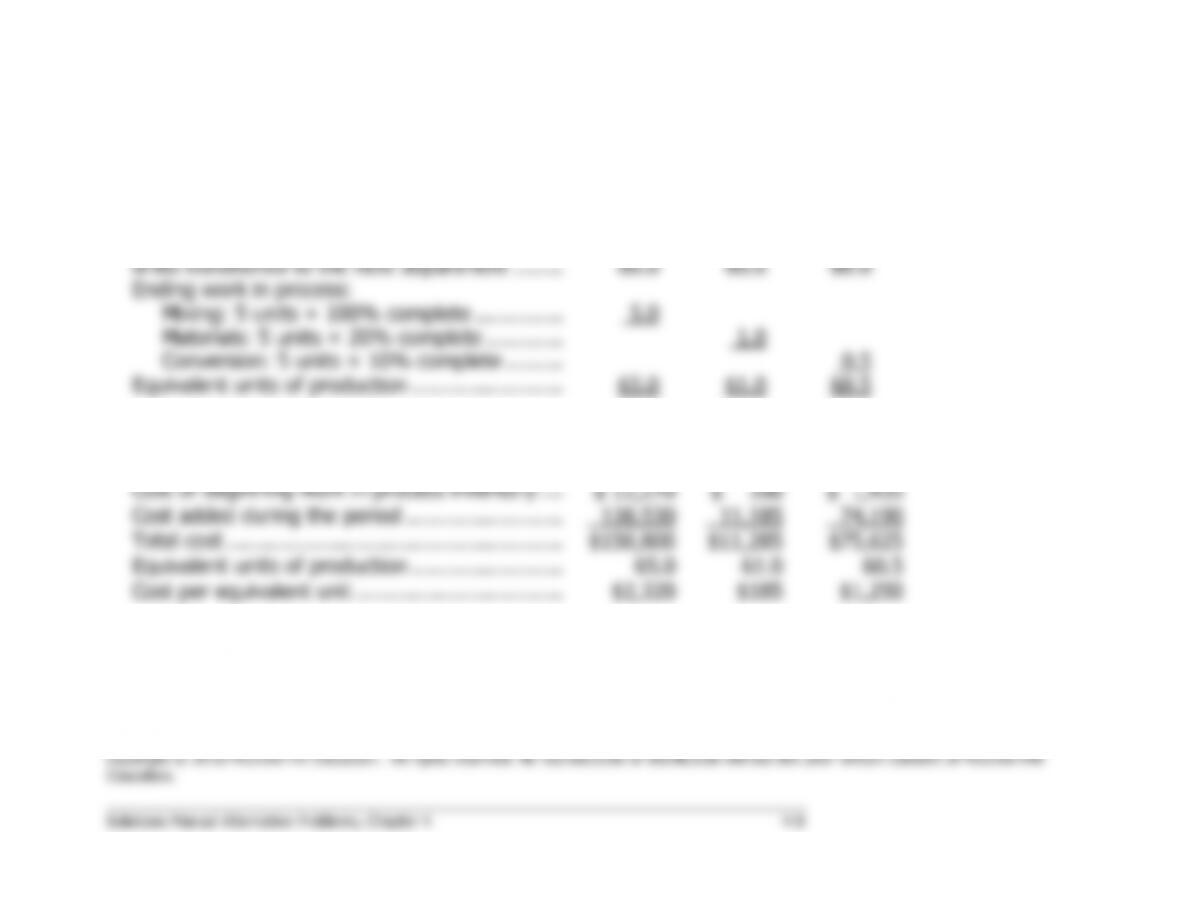

Problem 4-17B (60 minutes)

Weighted-Average Method

1. Computation of equivalent units in ending inventory:

Mixing

Materials

Conversion

Units transferred to the next department ……..

60.0

60.0

60.0

Ending work in process:

Mixing: 5 units × 100% complete …………..

5.0

Materials: 5 units × 20% complete …………

1.0

Conversion: 5 units × 10% complete ………

0.5

Equivalent units of production ……………………

65.0

61.0

60.5

2. Costs per equivalent unit:

Mixing

Materials

Conversion

Cost of beginning work in process inventory ….

$ 12,270

$ 100

$ 1,435

Cost added during the period …………………….

138,530

11,185

74,190

Total cost ………………………………………………

$150,800

$11,285

$75,625

Equivalent units of production ……………………

65.0

61.0

60.5

Cost per equivalent unit …………………………...

$2,320

$185

$1,250

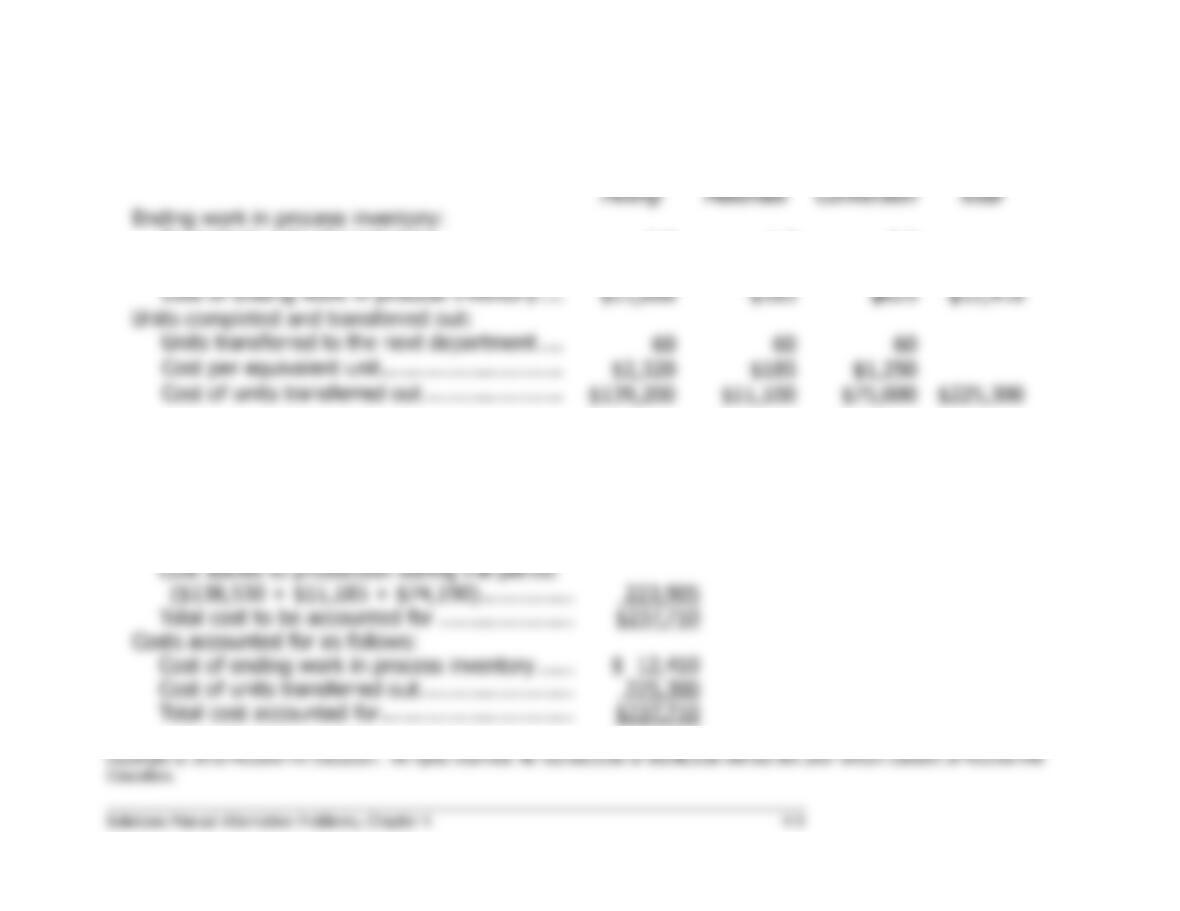

Problem 4-17B (continued)

3. Costs of ending work in process inventory and units transferred out:

Mixing

Materials

Conversion

Total

Ending work in process inventory:

Equivalent units of production ………………..

5.0

1.0

0.5

Cost per equivalent unit ………………………..

$2,320

$185

$1,250

Cost of ending work in process inventory ….

$11,600

$185

$625

$12,410

Units completed and transferred out:

Units transferred to the next department ….

60

60

60

Cost per equivalent unit ………………………..

$2,320

$185

$1,250

Cost of units transferred out ………………….

$139,200

$11,100

$75,000

$225,300

4. Cost reconciliation:

Cost to be accounted for:

Cost of beginning work in process inventory

($12,270 + $100 + $1,435) …………………..

$ 13,805

Cost added to production during the period

($138,530 + $11,185 + $74,190) ……………

223,905

Total cost to be accounted for ………………….

$237,710

Costs accounted for as follows:

Cost of ending work in process inventory ……

$ 12,410

Cost of units transferred out …………………….

225,300

Total cost accounted for ………………………….

$237,710

Solutions Manual Alternative Problems, Chapter 4 4-10

Problem 4-18B (30 minutes)

Weighted-Average Method

1.

Total units transferred to the next department …

41,900

Less units in the May 1 inventory ………………….

11,500

Units started and completed in May……………….

30,400

2.

The equivalent units were:

Materials

Conversion

Transferred to next department ………………

41,900

41,900

Ending work in process:

Materials: 7,600 units x 75% complete …..

5,700

Conversion: 7,600 units x 50% complete ..

3,800

Equivalent units of production ………………..

47,600

45,700

3.

The costs per equivalent unit were:

Materials

Conversion

Cost of beginning work in process …………….

£ 23,460

£12,305

Cost added during the period …………………..

83,164

46,648

Total cost (a) ……………………………………….

£106,624

£58,953

Equivalent units of production (b) …………….

47,600

45,700

Cost per equivalent unit, (a) ÷ (b) ……………

£2.24

£1.29

4.

The ending work in process figure is verified as follows:

Materials

Conversion

Total

Ending work in process inventory:

Equivalent units of production

(see above) …………………………...

5,700

3,800

Cost per equivalent unit ……………..

£2.24

£1.29

Cost of ending work in process

inventory ……………………………….

£12,768

£4,902

£17,670

5. Multiplying the unit cost figure of £3.53 per unit by 1,000 units does

not

provide a valid estimate of the incremental cost of processing an