Exercise 7-5 (15 minutes)

1.

Yuvwell Corporation

Manufacturing Overhead Budget

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Budgeted direct labor-hours …………………………..

8,000

8,200

8,500

7,800

32,500

Variable manufacturing overhead rate ……………..

× $2.00

× $2.00

× $2.00

× $2.00

× $2.00

Variable manufacturing overhead ……………………

$16,000

$16,400

$17,000

$15,600

$65,000

Fixed manufacturing overhead ……………………….

48,000

48,000

48,000

48,000

192,000

Total manufacturing overhead ……………………….

64,000

64,400

65,000

63,600

257,000

Less depreciation ………………………………………..

16,000

16,000

16,000

16,000

64,000

Cash disbursements for manufacturing overhead .

$48,000

$48,400

$49,000

$47,600

$193,000

2.

Total budgeted manufacturing overhead for the year (a) …

$257,000

Budgeted direct labor-hours for the year (b) …………………

32,500

Predetermined overhead rate for the year (a) ÷ (b) ……….

$7.91

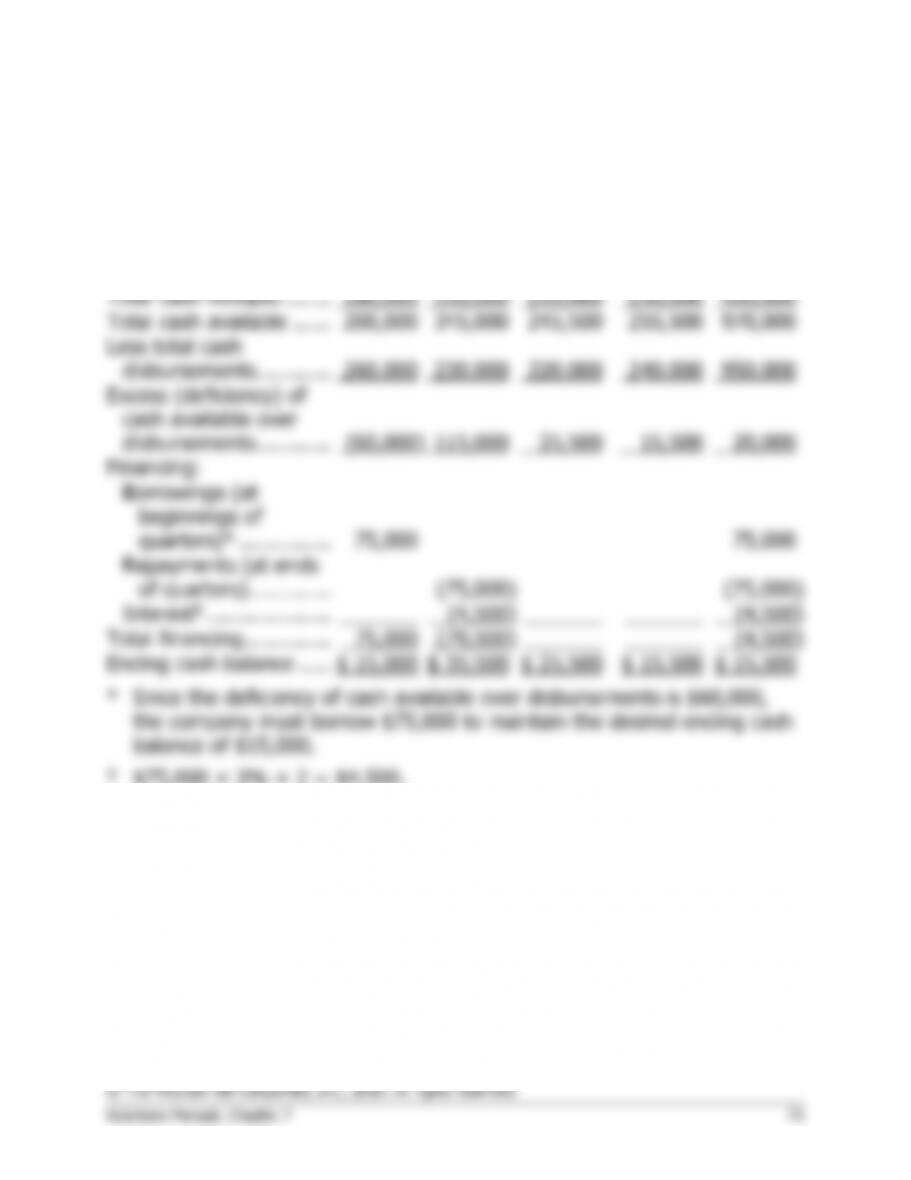

Exercise 7-7 (15 minutes)

Garden Depot

Cash Budget

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Beginning cash balance .

$ 20,000

$ 15,000

$ 35,500

$ 25,500

$ 20,000

Total cash receipts ……..

180,000

330,000

210,000

230,000

950,000

Total cash available ……

200,000

345,000

245,500

255,500

970,000

Less total cash

disbursements …………

260,000

230,000

220,000

240,000

950,000

Excess (deficiency) of

cash available over

disbursements …………

(60,000)

115,000

25,500

15,500

20,000

Financing:

Borrowings (at

beginnings of

quarters)* ……………

75,000

75,000

Repayments (at ends

of quarters) ………….

(75,000)

(75,000)

Interest§ ………………..

(4,500)

(4,500)

Total financing …………..

75,000

(79,500)

(4,500)

Ending cash balance …..

$ 15,000

$ 35,500

$ 25,500

$ 15,500

$ 15,500

* Since the deficiency of cash available over disbursements is $60,000,

the company must borrow $75,000 to maintain the desired ending cash

balance of $15,000.

§ $75,000 × 3% × 2 = $4,500.

Exercise 7-8 (10 minutes)

Gig Harbor Boating

Budgeted Income Statement

Sales (400 units × $1,950 per unit) ………………….

$780,000

Cost of goods sold (400 units × $1,575 per unit) …

630,000

Gross margin ……………………………………………….

150,000

Selling and administrative expenses* ………………..

135,000

Net operating income …………………………………….

15,000

Interest expense …………………………………………..

14,000

Net income ………………………………………………….

$ 1,000

*(400 units × $75 per unit) + $105,000 = $135,000.

Exercise 7-9 (15 minutes)

Mecca Copy

Budgeted Balance Sheet

Assets

Current assets:

Cash* …………………………………………

$10,700

Accounts receivable ……………………….

8,100

Supplies inventory …………………………

3,200

Total current assets …………………………

$22,000

Plant and equipment:

Equipment …………………………………..

34,000

Accumulated depreciation ……………….

(16,000)

Plant and equipment, net ………………….

18,000

Total assets ……………………………………

$40,000

Liabilities and Stockholders’ Equity

Current liabilities:

Accounts payable ………………………….

$ 1,800

Stockholders’ equity:

Common stock ……………………………..

$ 5,000

Retained earnings# ……………………….

33,200

Total stockholders’ equity ………………….

38,200

Total liabilities and stockholders’ equity ..

$40,000

*Plug figure.

#

Retained earnings, beginning balance ..

$28,000

Add net income …………………………….

10,000

38,000

Deduct dividends …………………………..

4,800

Retained earnings, ending balance ……

$33,200

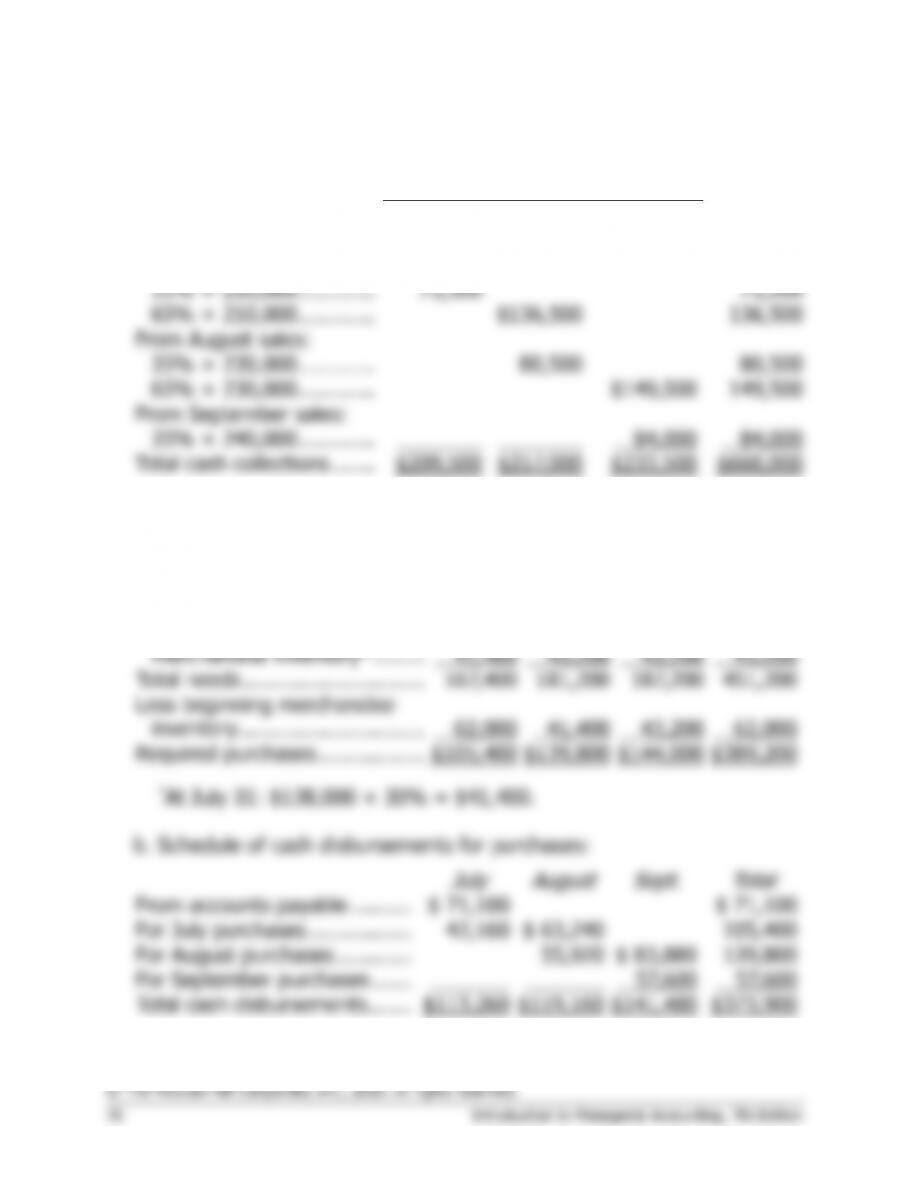

Exercise 7-12 (30 minutes)

1. Schedule of expected cash collections:

Month

July

August

Sept.

Quarter

From accounts receivable .

$136,000

$136,000

From July sales:

35% × 210,000 …………

73,500

73,500

65% × 210,000 …………

$136,500

136,500

From August sales:

35% × 230,000 …………

80,500

80,500

65% × 230,000 …………

$149,500

149,500

From September sales:

35% × 240,000 …………

84,000

84,000

Total cash collections …….

$209,500

$217,000

$233,500

$660,000

2. a. Merchandise purchases budget:

July

August

Sept.

Total

Budgeted cost of goods sold

(60% of sales)………………….

$126,000

$138,000

$144,000

$408,000

Add desired ending

merchandise inventory* ……..

41,400

43,200

43,200

43,200

Total needs ………………………..

167,400

181,200

187,200

451,200

Less beginning merchandise

inventory …………………………

62,000

41,400

43,200

62,000

Required purchases ……………..

$105,400

$139,800

$144,000

$389,200

July

August

Sept.

Total

From accounts payable ……….

$ 71,100

$ 71,100

For July purchases ……………..

42,160

$ 63,240

105,400

For August purchases …………

55,920

$ 83,880

139,800

For September purchases ……

57,600

57,600

Total cash disbursements …….

$113,260

$119,160

$141,480

$373,900

Exercise 7-12 (continued)

3.

Beech Corporation

Income Statement

For the Quarter Ended September 30

Sales ($210,000 + $230,000 + $240,000) ..

$680,000

Cost of goods sold (Part 2a) …………………

408,000

Gross margin ……………………………………..

272,000

Selling and administrative expenses

($60,000 × 3 months) ………………………

180,000

Net operating income…………………………..

92,000

Interest expense ………………………………..

0

Net income ……………………………………….

$ 92,000

4.

Beech Corporation

Balance Sheet

September 30

Assets

Cash ($90,000 + $660,000 – $373,900 – ($55,000 ×

3)) ……………………………………………………………

$211,100

Accounts receivable ($240,000 × 65%) …………………

156,000

Inventory (Part 2a) ……………………………………………

43,200

Plant and equipment, net ($210,000 – ($5,000 ×3)) …

195,000

Total assets ……………………………………………………..

$605,300

Accounts payable ($144,000 × 60%) …………………….

Common stock (Given) ………………………………………

Retained earnings ($99,900 + $92,000) …………………

Total liabilities and stockholders’ equity ………………….

$605,300

Exercise 7-14 (30 minutes)

1.

Jessi Corporation

Sales Budget

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Budgeted unit sales ……………..

11,000

16,000

14,000

13,000

54,000

Selling price per unit …………….

× $25.00

× $25.00

× $25.00

× $25.00

× $25.00

Total sales …………………………

$275,000

$400,000

$350,000

$325,000

$1,350,000

Schedule of Expected Cash Collections

Beginning accounts receivable .

$ 70,200

$ 70,200

1st Quarter sales ………………….

178,750

$ 82,500

261,250

2nd Quarter sales …………………

260,000

$120,000

380,000

3rd Quarter sales …………………

227,500

$105,000

332,500

4th Quarter sales ………………….

211,250

211,250

Total cash collections ……………

$248,950

$342,500

$347,500

$316,250

$1,255,200

Exercise 7-14 (continued)

2.

Jessi Corporation

Production Budget

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Budgeted unit sales ……………..

11,000

16,000

14,000

13,000

54,000

Add desired units of ending

finished goods inventory …….

2,400

2,100

1,950

1,850

1,850

Total needs ………………………..

13,400

18,100

15,950

14,850

55,850

Less units of beginning

finished goods inventory …….

1,650

2,400

2,100

1,950

1,650

Required production in units ….

11,750

15,700

13,850

12,900

54,200

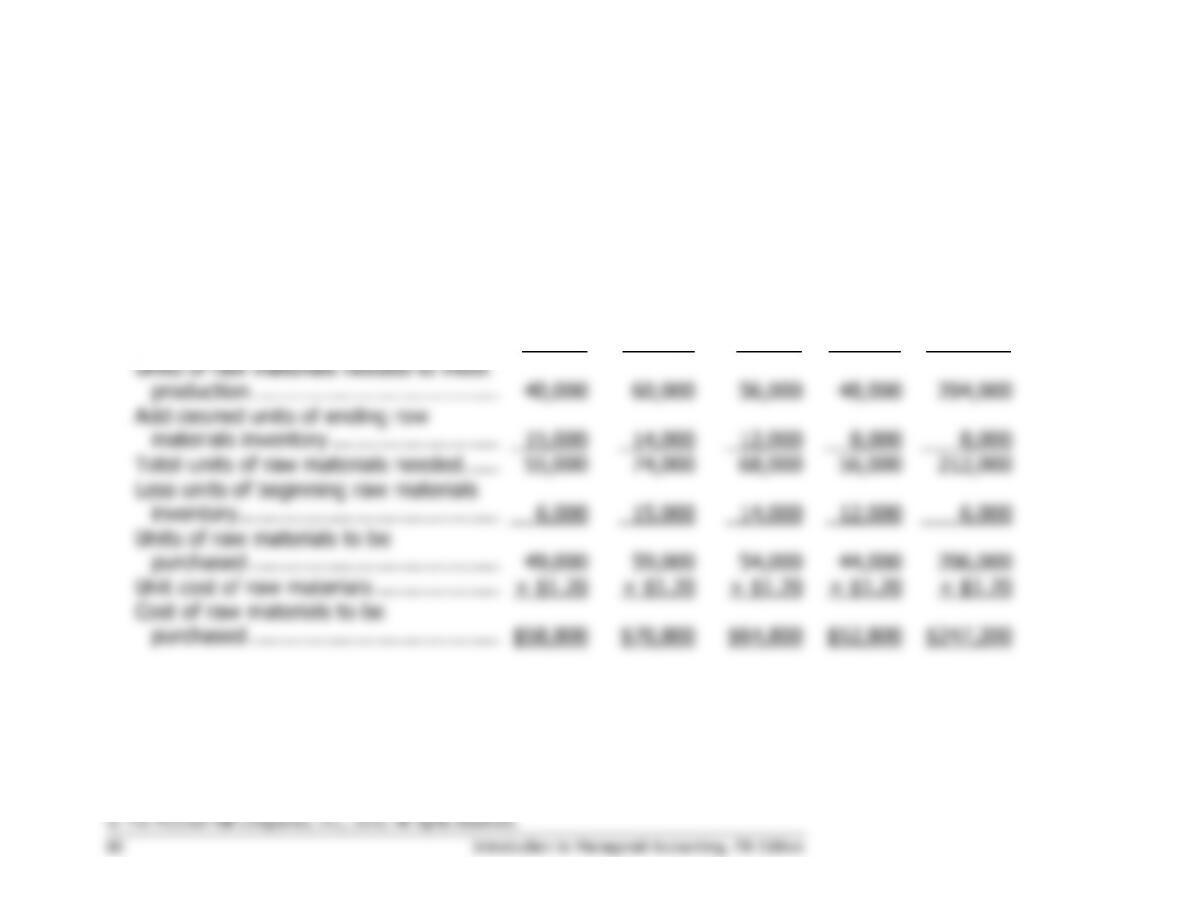

Exercise 7-16 (30 minutes)

1.

Zan Corporation

Direct Materials Budget

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Required production in units of

finished goods …………………………….

5,000

7,500

7,000

6,000

25,500

Units of raw materials needed per unit

of finished goods …………………………

× 8

× 8

× 8

× 8

× 8

Units of raw materials needed to meet

production ………………………………….

40,000

60,000

56,000

48,000

204,000

Add desired units of ending raw

materials inventory ………………………

15,000

14,000

12,000

8,000

8,000

Total units of raw materials needed ……

55,000

74,000

68,000

56,000

212,000

Less units of beginning raw materials

inventory ……………………………………

6,000

15,000

14,000

12,000

6,000

Units of raw materials to be

purchased ………………………………….

49,000

59,000

54,000

44,000

206,000

Unit cost of raw materials ………………..

× $1.20

× $1.20

× $1.20

× $1.20

× $1.20

Cost of raw materials to be

purchased ………………………………….

$58,800

$70,800

$64,800

$52,800

$247,200

Exercise 7-16 (continued)

Schedule of Expected Cash Disbursements for Materials

Beginning accounts payable ………

$ 2,880

$ 2,880

1st Quarter purchases ……………..

35,280

$23,520

58,800

2nd Quarter purchases …………….

42,480

$28,320

70,800

3rd Quarter purchases ……………..

38,880

$25,920

64,800

4th Quarter purchases ……………..

31,680

31,680

Total cash disbursements for

materials …………………………….

$38,160

$66,000

$67,200

$57,600

$228,960

2.

Zan Corporation

Direct Labor Budget

1st Quarter

2nd Quarter

3rd Quarter

4th Quarter

Year

Required production in units ……..

5,000

7,500

7,000

6,000

25,500

Direct labor-hours per unit ………..

× 0.20

× 0.20

× 0.20

× 0.20

× 0.20

Total direct labor-hours needed….

1,000

1,500

1,400

1,200

5,100

Direct labor cost per hour …………

× $11.50

× $11.50

× $11.50

× $11.50

× $11.50

Total direct labor cost ………………

$ 11,500

$ 17,250

$ 16,100

$ 13,800

$ 58,650