Problem 11-12B (15 minutes)

Item

Year(s)

Amount

of Cash

Flows

19%

Factor

Present

Value of

Cash

Flows

Cost of equipment required ……

Now

$(800,000)

1.000

$(800,000)

Working capital required ……….

Now

$(225,000)

1.000

(225,000)

Annual net cash receipts ……….

1-11

$305,000

4.486

1,368,230

Cost of road repairs ……………..

10

$(66,000)

0.176

(11,616)

Salvage value of equipment ……

11

$200,000

0.148

29,600

Working capital released ……….

11

$225,000

0.148

33,300

Net present value ………………..

$394,514)

Yes, the project should not be accepted; it has a positive net present value.

This means that the rate of return on the investment is greater than the

company’s required rate of return of 19%.

Problem 11-13B (30 minutes)

1. The formula for the project profitability index is:

Net present value

The index for the projects under consideration would be:

Project 1: $86,080 ÷ $500,000 = 0.172

Project 2: $72,000 ÷ $450,000 = 0.160

Project 3: $46,400 ÷ $220,000 = 0.211

Project 4: $146,650 ÷ $470,000 = 0.312

2. a., b., and c.

Net Present

Value

Project

Profitability

Index

Internal Rate

of Return

First preference ……..

4

4

4

Second preference ….

1

3

3

Third preference …….

2

1

1

Fourth preference …..

3

2

2

3. Which ranking is best will depend on the company’s opportunities for

reinvesting funds as they are released from a project. The internal rate

of return method assumes that any released funds are reinvested at the

internal rate of return. This means that funds released from project #4

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the

prior written consent of McGraw-Hill Education.

Solutions Manual Alternate Problems, Chapter 11 11-3

amount of cash inflow generated for each dollar of investment (as

shown by the project profitability index).

Problem 11-14B (30 minutes)

1. The formula for the project profitability index is:

Net present value

The project profitability index for each project is:

Project A:

$434,360 ÷ $880,000 = 0.49

Project B:

$371,170 ÷ $685,000 = 0.54

Project C:

$223,220 ÷ $580,000 = 0.38

Project D:

$165,060 ÷ $780,000 = 0.21

2. a., b., and c.

Net Present

Value

Project

Profitability

Index

Internal Rate

of Return

First preference ……….

A

B

A

Second preference ……

B

A

D

Third preference ………

C

C

C

Fourth preference …….

D

D

B

3. Which ranking is best depends on the company’s opportunities for

reinvesting funds as they are released from a project. The internal rate

of return method assumes that released funds are reinvested at the

internal rate of return. For example, funds released from project D

required.

Problem 11-15B (30 minutes)

1. The income statement would be:

Sales revenue (70,000 loaves × $1.30 per loaf) …

$91,000

Less cost of ingredients ($91,000 × 40%)…………

36,400

Contribution margin ……………………………………..

54,600

Selling and administrative expenses:

Utilities ……………………………………………………

$ 9,000

Salaries …………………………………………………..

19,000

Insurance ………………………………………………..

4,000

Depreciation* …………………………………………..

10,848

Total selling and administrative expenses ………….

42,848

Net operating income …………………………………..

$11,752

*

$180,800 × 90% = $162,720

$162,720 ÷ 15 years = $10,848 per year.

2. The formula for the simple rate of return is:

Simple rate of return

=

Annual incremental net

operating income

Initial investment

=

$11,752

= 6%

$180,800

Yes, the oven and equipment would be purchased because their return

exceeds the owner’s 5% requirement.

Problem 11-15B (continued)

3. The formula for the payback period is:

Payback period

=

Initial investment

Net annual cash inflow

=

$180,800

= 8 years

$22,600 per year*

*

Net operating income + Depreciation = Annual net cash inflow

$11,752 + $10,848 = $22,600

Yes, the oven and equipment would be purchased. The payback period

is less than the 9-year period required.

Problem 11-16B (20 minutes)

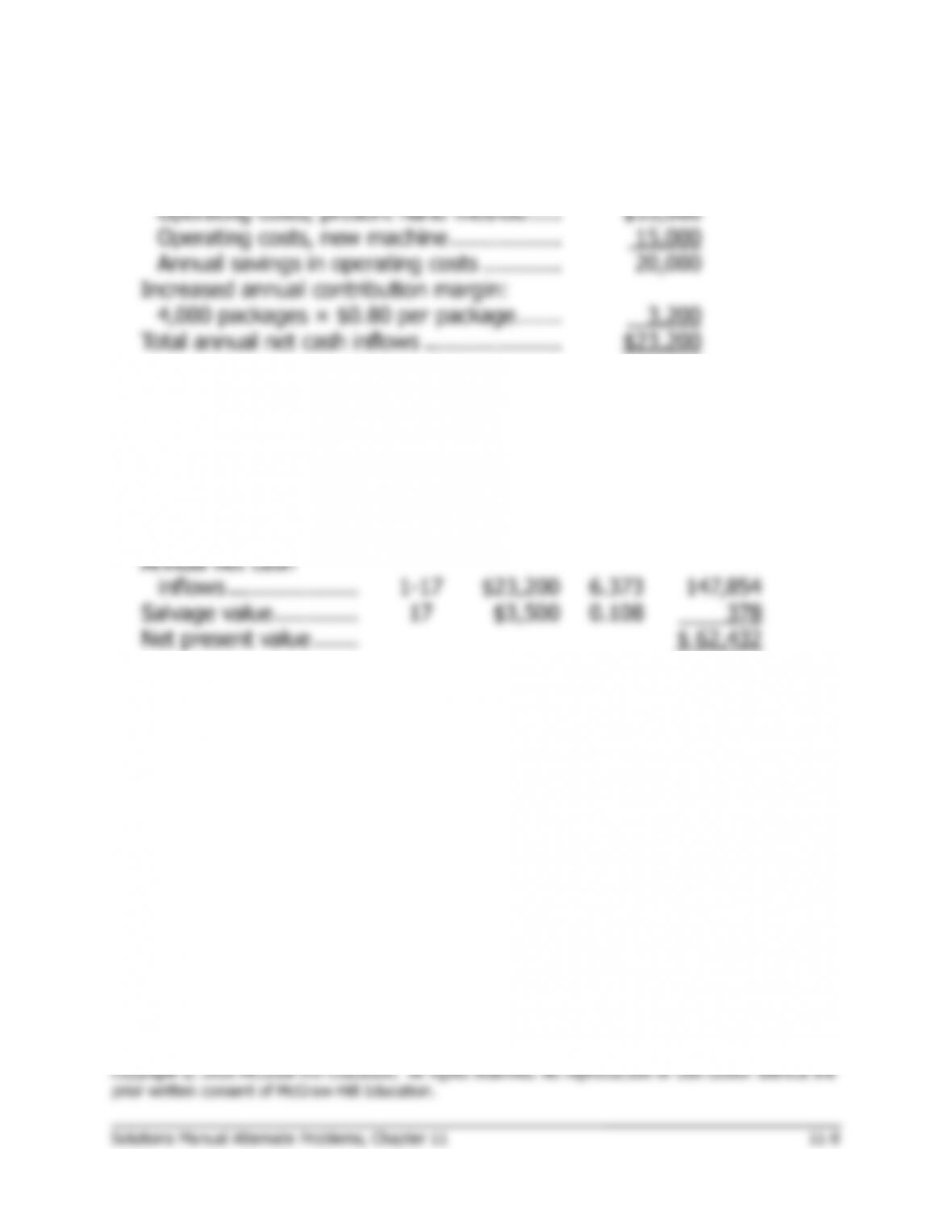

1. The annual net cash inflows would be:

Reduction in annual operating costs:

Operating costs, present hand method …..

$35,000

Operating costs, new machine ……………..

15,000

Annual savings in operating costs …………

20,000

Increased annual contribution margin:

4,000 packages × $0.80 per package …….

3,200

Total annual net cash inflows …………………

$23,200

2.

Item

Year(s)

Amount

of Cash

Flows

14%

Factor

Present

Value of

Cash

Flows

Cost of the machine …

Now

$(85,000)

1.000

$(85,000)

Overhaul required ……

14

$(5,000)

0.160

(800)

Annual net cash

inflows ………………..

1-17

$23,200

6.373

147,854

Salvage value ………….

17

$3,500

0.108

378

Net present value …….

$ 62,432

Problem 11-17B (30 minutes)

1. The present value of cash flows would be:

Item

Year(s)

Amount

of Cash

Flows

10%

Factor

Present

Value of

Cash

Flows

Purchase alternative:

Purchase cost of the plane ….

Now

$(780,000)

1.000

$(780,000)

Annual cost of servicing, etc. .

1-5

$(8,000)

3.791

(30,328)

Repairs:

First three years ……………..

1-3

$(3,000)

2.487

(7,461)

Fourth year ……………………

4

$(5,000)

0.683

(3,415)

Fifth year ………………………

5

$(10,000)

0.621

(6,210)

Resale value of the plane ……

5

$390,000

0.621

242,190

Present value of cash flows …

$(585,224)

Lease alternative:

Damage deposit ……………….

Now

$ (55,000)

1.000

$ (55,000)

Annual lease payments ………

1-5

$(130,000)

3.791

(492,830)

Refund of deposit ……………..

5

$55,000

0.621

34,155

Present value of cash flows …

$(513,675)

Net present value in favor of

leasing the plane ………………

$ 71,549

2. The company should accept the leasing alternative. Even though the

total cash flows for leasing exceed the total cash flows for purchasing,

the leasing alternative is attractive because of the company’s high

Problem 11-18B (60 minutes)

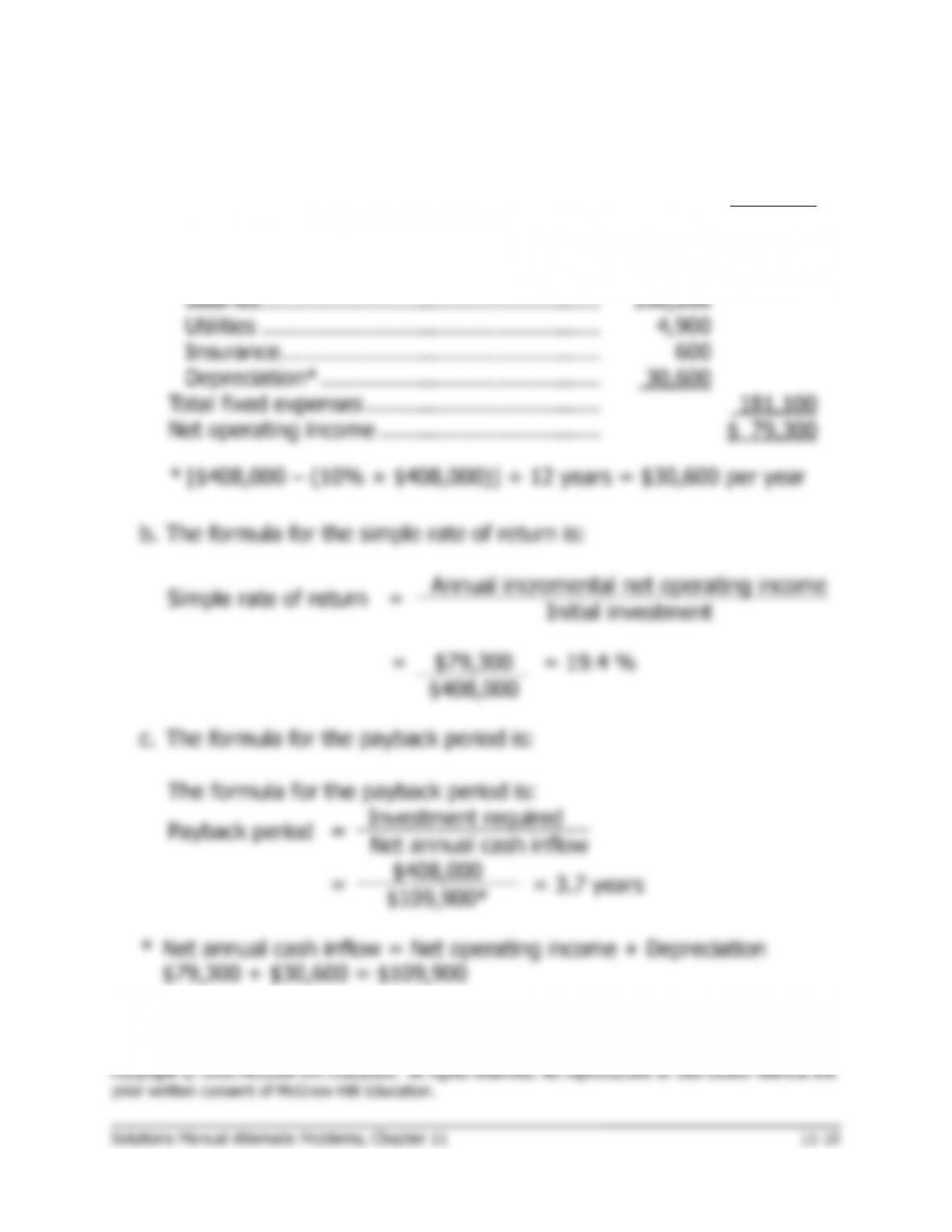

1.

a.

Sales revenue ………………………………………

$310,000

Variable production expenses (@ 16%) ……..

49,600

Contribution margin …………………………..….

260,400

Fixed expenses:

Advertising ………………………………………..

$ 39,000

Salaries …………………………………………….

106,000

Utilities …………………………………………….

4,900

Insurance ………………………………………….

600

Depreciation* …………………………………….

30,600

Total fixed expenses ………………………………

181,100

Net operating income …………………………….

$ 79,300

*

[$408,000 – (10% × $408,000)] ÷ 12 years = $30,600 per year

b. The formula for the simple rate of return is:

Simple rate of return

=

Annual incremental net operating income

Initial investment

=

$79,300

= 19.4 %

$408,000

c. The formula for the payback period is:

The formula for the payback period is:

Payback period

=

Investment required

Net annual cash inflow

=

$408,000

= 3.7 years

$109,900*

*

Net annual cash inflow = Net operating income + Depreciation

$79,300 + $30,600 = $109,900

Problem 11-18B (continued)

2. a. A cost reduction project is involved here, so the formula for the

simple rate of return would be:

3. According to the company’s criteria, machine A should not be purchased

Cost savings – Depreciation

Simple rate of return = Initial Salvage from

–

investment old equipment

Problem 11-19B (30 minutes)

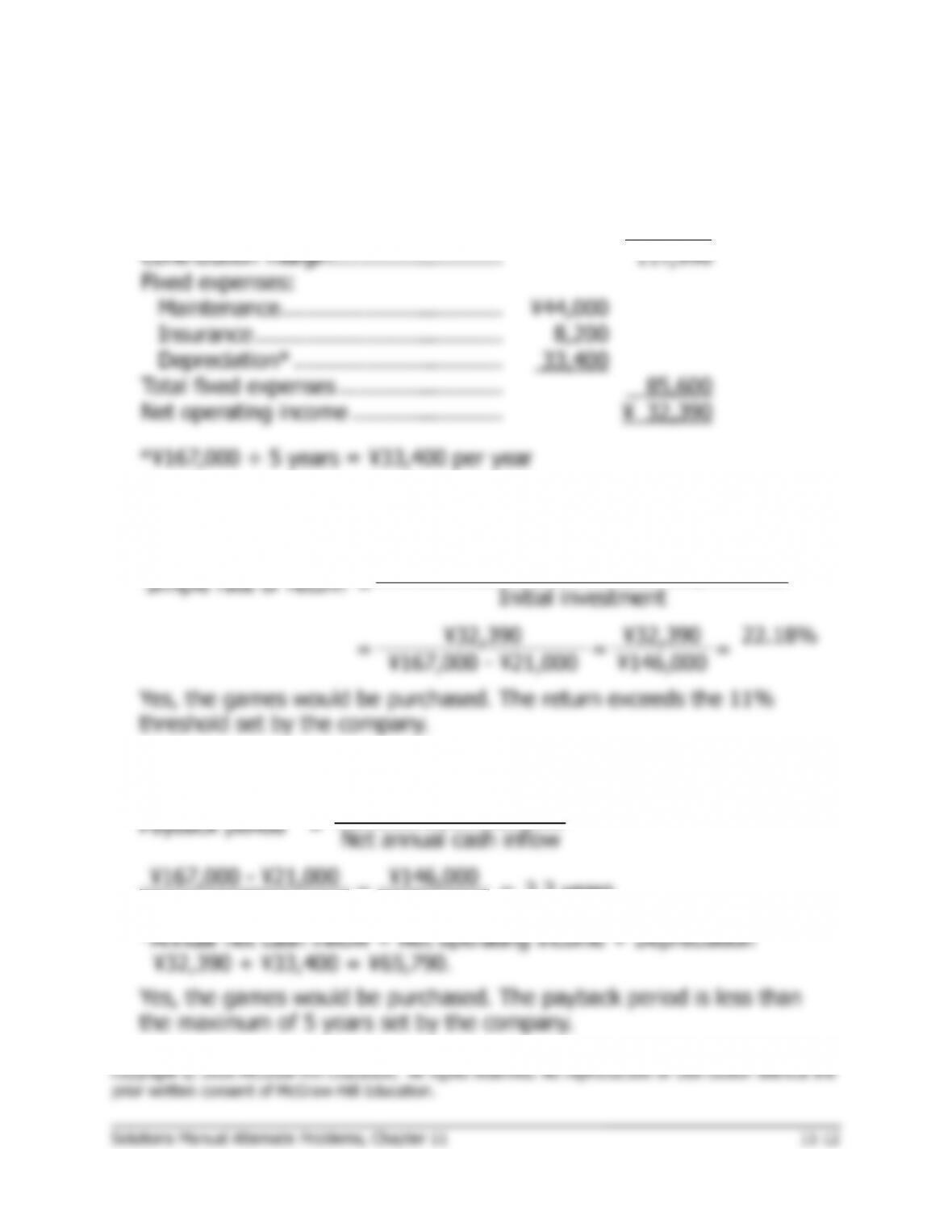

1. The income statement is:

Sales revenue …………………………….

¥207,000

Commissions (43% × ¥207,000) …….

89,010

Contribution margin ……………………..

117,990

Fixed expenses:

Maintenance …………………………….

¥44,000

Insurance ………………………………..

8,200

Depreciation* …………………………..

33,400

Total fixed expenses …………………….

85,600

Net operating income …………………..

¥ 32,390

*¥167,000 ÷ 5 years = ¥33,400 per year

2. The initial investment in the simple rate of return calculations is net of

the salvage value of the old equipment as shown below:

Simple rate of return

=

Annual incremental net operating income

Initial investment

=

¥32,390

=

¥32,390

=

22.18%

¥167,000 – ¥21,000

¥146,000

Yes, the games would be purchased. The return exceeds the 11%

threshold set by the company.

3. The payback period is:

Payback period

=

Investment required

Net annual cash inflow

¥167,000 – ¥21,000

=

¥146,000

=

2.2 years

¥65,790*

¥65,790

Problem 11-20B (30 minutes)

1. The total-cost approach:

Year(s)

Amount

of Cash

Flows

7%

Factor

Present

Value of

Cash

Flows

Purchase the new generator:

Cost of the new generator …….

Now

$(21,000)

1.000

$(21,000)

Salvage of the old generator ….

Now

$3,000

1.000

3,000

Annual cash operating costs ….

1-5

$(6,000)

4.100

(24,600)

Salvage of the new generator ..

5

$4,000

0.713

2,852

Present value of the net cash

outflows ………………………….

$(39,748)

Keep the old generator:

Overhaul needed now …………..

Now

$(7,000)

1.000

$ (7,000)

Annual cash operating costs …..

1-5

$(11,000)

4.100

(45,100)

Salvage of the old generator …..

5

$2,000

0.713

1,426

Present value of the net cash

outflows ………………………….

$(50,674)

Net present value in favor of

purchasing the new generator ..

$ 10,926

The hospital should purchase the new generator because it has the

lowest present value of total cost.

Problem 11-20B (continued)

2.

The incremental-cost approach:

Year(s)

Amount

of Cash

Flows

16%

Factor

Present

Value of

Cash

Flows

Incremental investment—new

generator* ………………………..

Now

$(14,000)

1.000

$(14,000)

Salvage of the old generator ……

Now

$3,000

1.000

3,000

Savings in annual cash operating

costs ………………………………..

1-5

$5,000

4.100

20,500

Difference in salvage value in 8

years ………………………………..

5

$2,000

0.713

1,426

Net present value in favor of

purchasing the new generator .

$ 10,926

*$21,000 – $7,000 = $14,000.

Problem 11-21B (60 minutes)

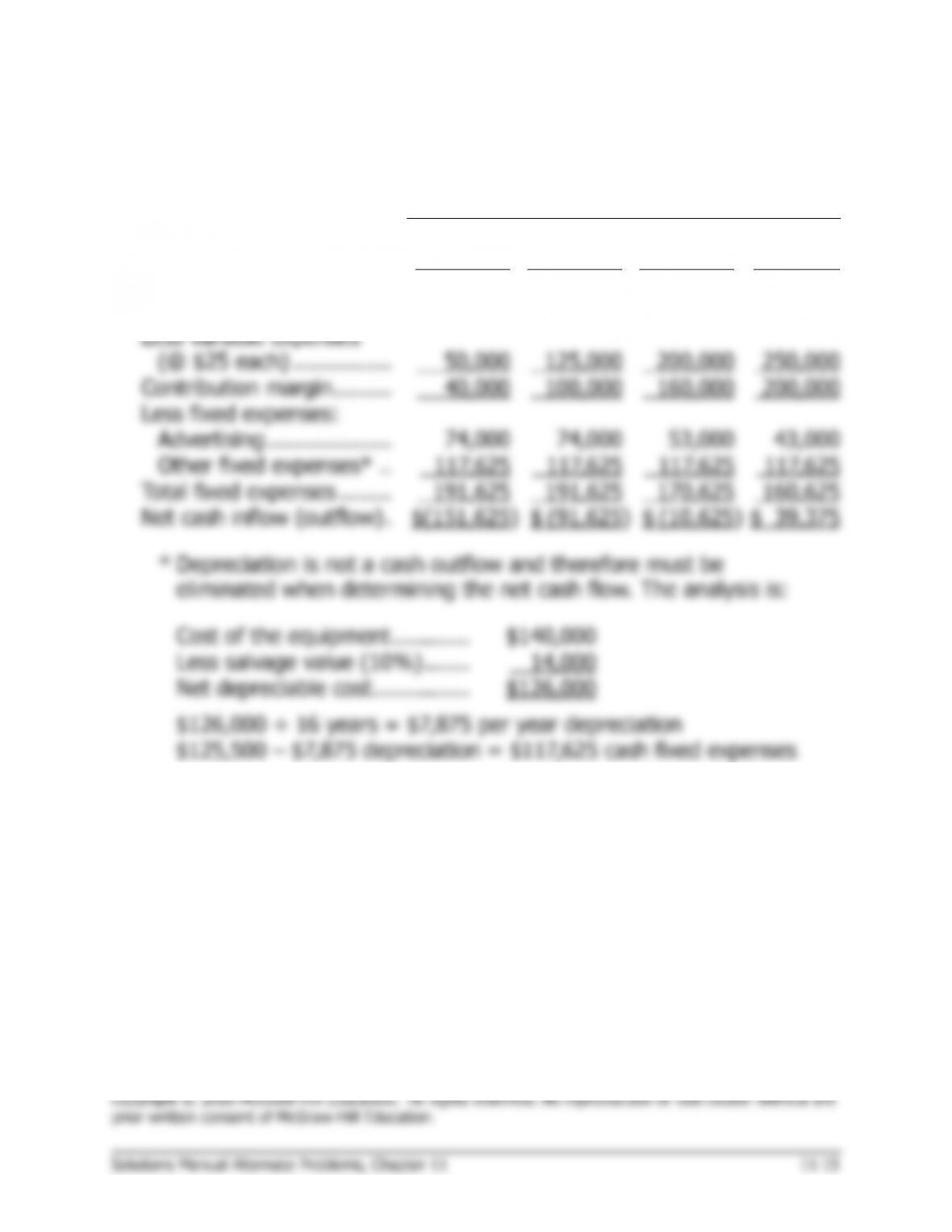

1. The net cash inflow from sales of the detectors for each year would be:

Year

1

2

3

4-12

Sales in units ………………

2,000

5,000

8,000

10,000

Sales in dollars

(@ $45 each) ……………

$ 90,000

$ 225,000

$ 360,000

$450,000

Less variable expenses

(@ $25 each) ……………

50,000

125,000

200,000

250,000

Contribution margin ………

40,000

100,000

160,000

200,000

Less fixed expenses:

Advertising ……………….

74,000

74,000

53,000

43,000

Other fixed expenses* ..

117,625

117,625

117,625

117,625

Total fixed expenses ……..

191,625

191,625

170,625

160,625

Net cash inflow (outflow) .

$(151,625)

$ (91,625)

$ (10,625)

$ 39,375

*

Depreciation is not a cash outflow and therefore must be

eliminated when determining the net cash flow. The analysis is:

Cost of the equipment …………

$140,000

Less salvage value (10%) …….

14,000

Net depreciable cost ……………

$126,000

$126,000 ÷ 16 years = $7,875 per year depreciation

$125,500 – $7,875 depreciation = $117,625 cash fixed expenses

Problem 11-21B (continued)

2. The net present value of the proposed investment would be:

Item

Year(s)

Amount of

Cash

Flows

7%

Factor

Present

Value of

Cash

Flows

Investment in equipment …

Now

$(140,000)

1.000

$(140,000)

Working capital investment

Now

$(44,000)

1.000

(44,000)

Yearly cash flows ……………

1

$(151,625)

0.935

(141,769)

” ” ” …………….

2

$(91,625)

0.873

(79,989)

” ” ” …………….

3

$(10,625)

0.816

(8,670)

” ” ” …………….

4-12

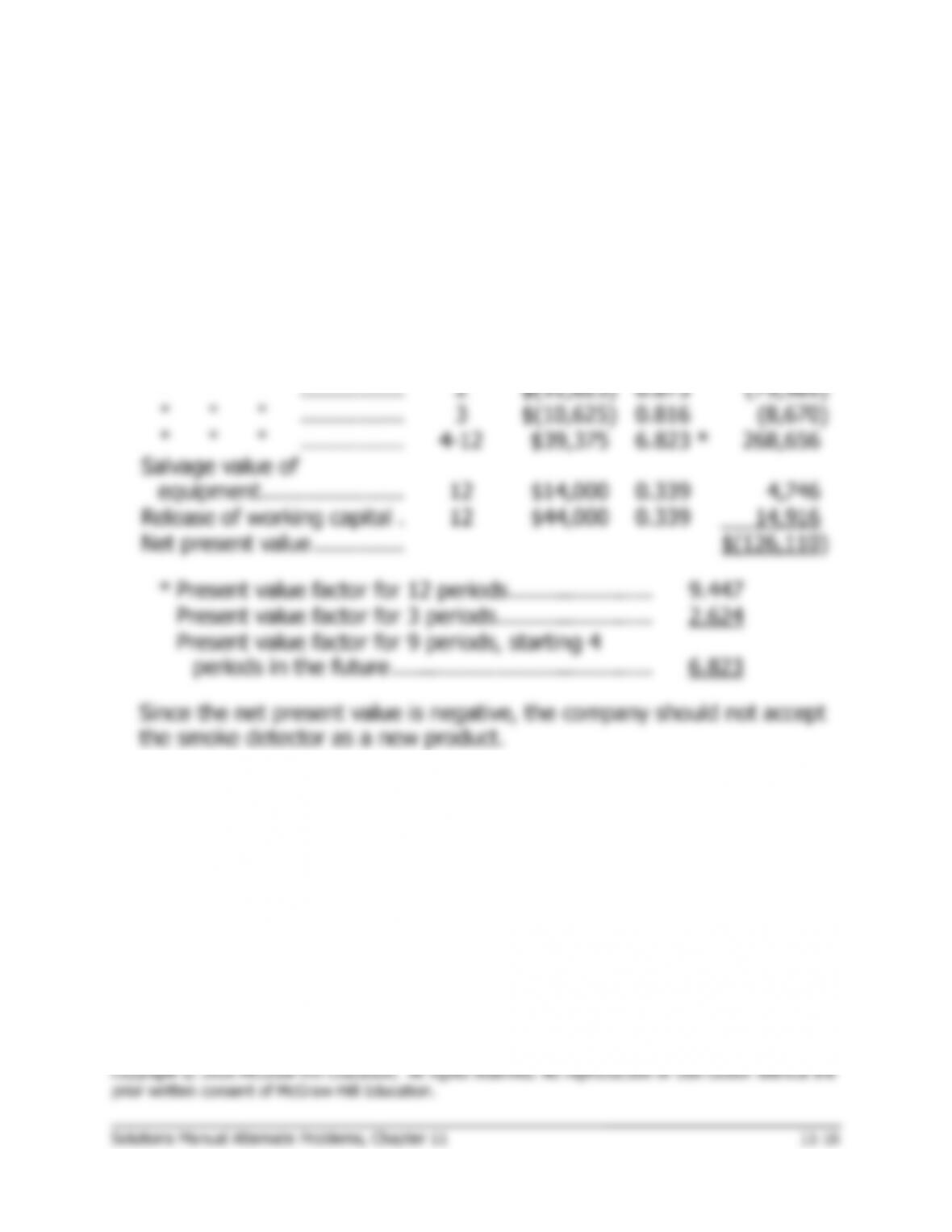

$39,375

6.823

*

268,656

Salvage value of

equipment ………………….

12

$14,000

0.339

4,746

Release of working capital .

12

$44,000

0.339

14,916

Net present value …………..

$(126,110)

*

Present value factor for 12 periods ………………….

9.447

Present value factor for 3 periods ……………………

2.624

Present value factor for 9 periods, starting 4

periods in the future ………………………………….

6.823

Since the net present value is negative, the company should not accept

the smoke detector as a new product.

Problem 11-22B (30 minutes)

1. Average weekly use of the washers and dryers would be:

Washers:

$3,565

= 2,300 uses

$1.55 per use

Dryers:

$2,080

= 2,600 uses

$0.80 per use

The expected annual net cash receipts would be:

Washer cash receipts ($3,565 × 52) ……..

$185,380

Dryer cash receipts ($2,080 × 52) ………..

108,160

Total cash receipts …………………………….

293,540

Less cash disbursements:

Washer: Water and electricity

($0.075 × 2,300 × 52) ………………….

$ 8,970

Dryer: Gas and electricity

($0.09 × 2,600 × 52) ……………………

12,168

Rent ($5,600 × 12) …………………………

67,200

Cleaning ($2,900 × 12) ……………………

34,800

Maintenance and other ($2,015 × 12) …

24,180

147,318

Annual net cash receipts …………………….

$146,222

2.

Item

Year(s)

Amount of

Cash Flows

13%

Factor

Present

Value of

Cash Flows

Cost of equipment ………..

Now

$(155,000)

1.000

$(155,000)

Working capital invested ..

Now

$(8,000)

1.000

(8,000)

Annual net cash receipts ..

1-3

$146,222

2.361

345,230

Salvage of equipment ……

3

$17,050

0.693

11,816

Working capital released ..

3

$8,000

0.693

5,544

Net present value …………

$199,590

Problem 11-23B (45 minutes)

1. A net present value computation for each investment follows:

Item

Year(s)

Amount of

Cash Flows

12%

Factor

Present

Value of

Cash Flows

Common stock:

Purchase of the stock ……..

Now

$(75,000)

1.000

$(75,000)

Sale of the stock ……………

6

$170,000

0.507

86,190

Net present value …………..

$ 11,190

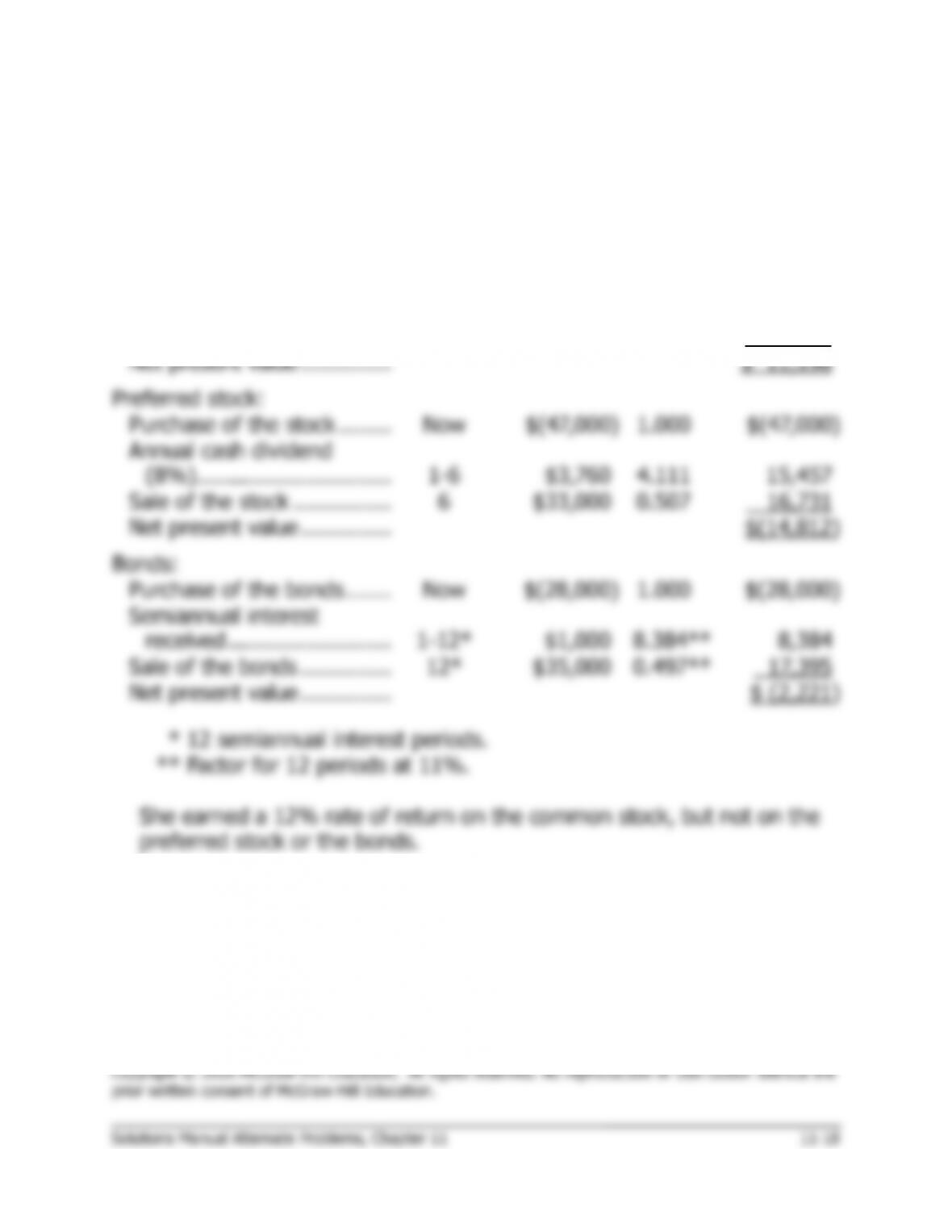

Preferred stock:

Purchase of the stock ……..

Now

$(47,000)

1.000

$(47,000)

Annual cash dividend

(8%)…………………………

1-6

$3,760

4.111

15,457

Sale of the stock ……………

6

$33,000

0.507

16,731

Net present value …………..

$(14,812)

Bonds:

Purchase of the bonds …….

Now

$(28,000)

1.000

$(28,000)

Semiannual interest

received …………………….

1-12*

$1,000

8.384**

8,384

Sale of the bonds …………..

12*

$35,000

0.497**

17,395

Net present value …………..

$ (2,221)

*

12 semiannual interest periods.

**

Factor for 12 periods at 11%.

She earned a 12% rate of return on the common stock, but not on the

preferred stock or the bonds.

Problem 11-23B (continued)

2. Considering all three investments together, she did not earn a 12% rate

of return. The computation is:

Net

Present

Value

Common stock ……………………

$ 11,190

Preferred stock ……………………

(14,812)

Bonds ……………………………….

(2,221)

Overall net present value ………

$ (5,843)

The defect in the broker’s computation is that it does not consider the

time value of money and therefore has overstated the rate of return

earned.

3.

Because the assumption is that the project will yield the same annual

cash inflow every year, the formula for the net present value of the

project is:

Substituting the $238,000 investment and the factor for 9% for 11

periods into this formula and requiring that the net present value be

positive, we get:

6.805 × Annual cash inflow – $238,000 > 0

Net present Present value Annual Investment

value of = factor for × cash – required

the project an annuity inflow

Problem 11-24B (45 minutes)

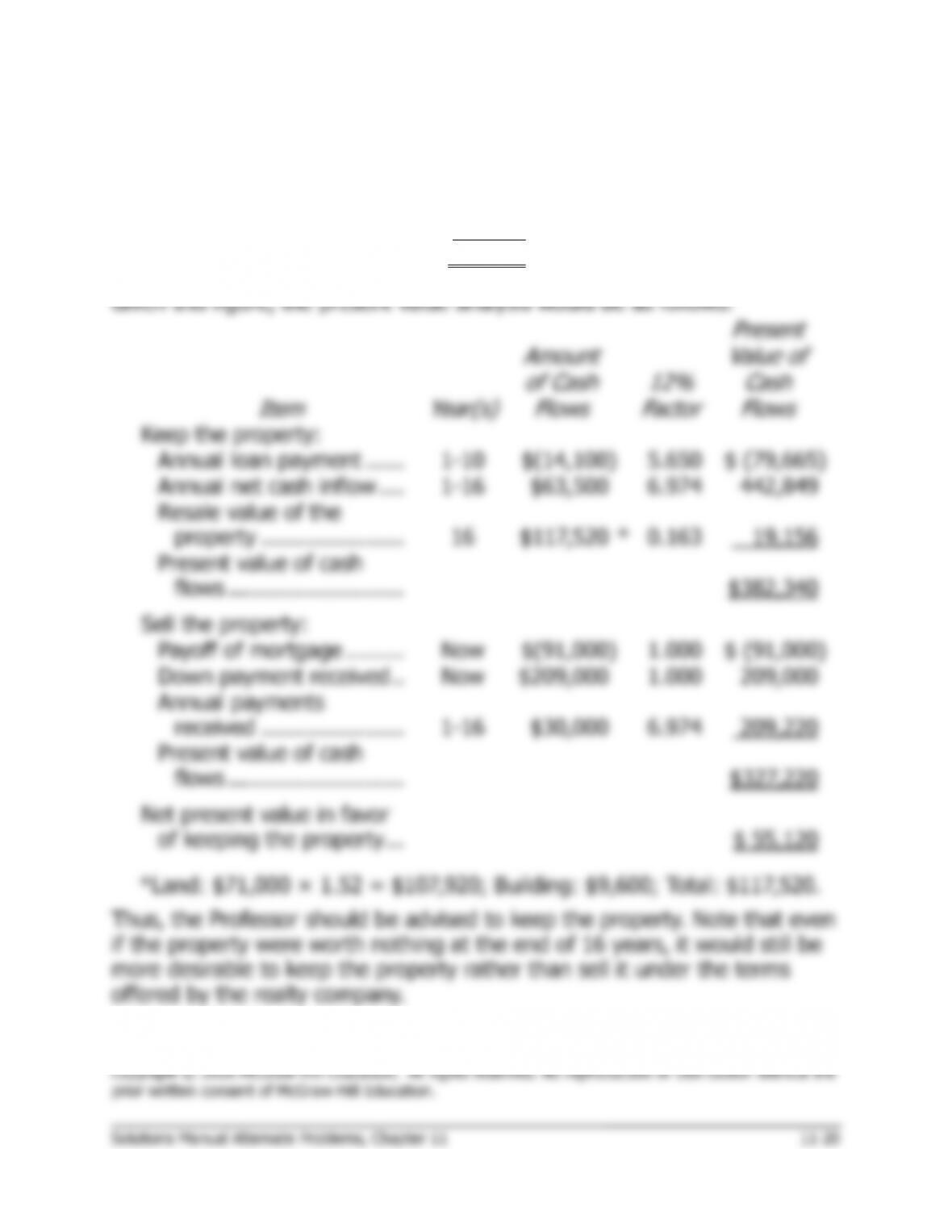

The annual net cash inflow from rental of the property would be:

Net operating income ……….

$43,900

Add back depreciation ………

19,600

Annual net cash inflow ……..

$63,500

Item

Year(s)

Amount

of Cash

Flows

12%

Factor

Present

Value of

Cash

Flows

Keep the property:

Annual loan payment ……

1-10

$(14,100)

5.650

$ (79,665)

Annual net cash inflow ….

1-16

$63,500

6.974

442,849

Resale value of the

property ………………….

16

$117,520

*

0.163

19,156

Present value of cash

flows ………………………

$382,340

Sell the property:

Payoff of mortgage ………

Now

$(91,000)

1.000

$ (91,000)

Down payment received ..

Now

$209,000

1.000

209,000

Annual payments

received ………………….

1-16

$30,000

6.974

209,220

Present value of cash

flows ………………………

$327,220

Net present value in favor

of keeping the property …

$ 55,120