Exercise 8B-2 (45 minutes)

1. a.

Actual Quantity

of Input, at

Actual Price

Actual Quantity

of Input, at

Standard Price

Standard Quantity

Allowed for Output,

at Standard Price

(AQ × AP)

(AQ × SP)

(SQ × SP)

10,000 yards ×

$13.80 per yard

10,000 yards ×

$14.00 per yard

7,500 yards* ×

$14.00 per yard

= $138,000

= $140,000

= $105,000

Price Variance =

$2,000 F

8,000 yards × $14.00 per yard

= $112,000

Quantity Variance =

$7,000 U

*3,000 units × 2.5 yards per unit = 7,500 yards

Alternatively, the variances can be computed using the formulas:

Materials price variance = AQ (AP – SP)

10,000 yards ($13.80 per yard – $14.00 per yard) = $2,000 F

Materials quantity variance = SP (AQ – SQ)

$14.00 per yard (8,000 yards – 7,500 yards) = $7,000 U

Exercise 8B-2 (continued)

b. The journal entries would be:

Raw Materials

(10,000 yards × 14.00 per yard) ………………

140,000

Materials Price Variance

(10,000 yards × $0.20 per yard F) ……

2,000

Accounts Payable

(10,000 yards × $13.80 per yard) …….

138,000

Work in Process

(7,500 yards × $14.00 per yard) ………………

105,000

Materials Quantity Variance

(500 yards U × $14.00 per yard) ……………..

7,000

Raw Materials

(8,000 yards × $14.00 per yard) ………

112,000

2. a.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of

Input, at the

Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

5,000 hours ×

$8.00 per hour

4,800 hours* ×

$8.00 per hour

$43,000

= $40,000

= $38,400

Rate Variance =

$3,000 U

Efficiency Variance =

$1,600 U

Spending Variance = $4,600 U

*3,000 units × 1.6 hours per unit = 4,800 hours

Exercise 8B-2 (continued)

Alternative Solution:

Labor rate variance = AH (AR – SR)

5,000 hours ($8.60 per hour* – $8.00 per hour) = $3,000 U

Problem 8B-3A (60 minutes)

1. a.

Actual Quantity of

Input, at Actual Price

Actual Quantity

of Input, at

Standard Price

Standard Quantity

Allowed for Output, at

Standard Price

(AQ × AP)

(AQ × SP)

(SQ × SP)

32,000 feet ×

$4.80 per foot

32,000 feet ×

$5.00 per foot

29,600 feet* ×

$5.00 per foot

= $153,600

= $160,000

= $148,000

Price Variance =

$6,400 F

Quantity Variance =

$12,000 U

Spending Variance = $5,600 U

Problem 8B-3A (continued)

2. a.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of

Input, at the

Standard Rate

Standard Hours

Allowed for Output,

at the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

6,400 hours* ×

$8.00 per hour

6,400 hours ×

$7.50 per hour

7,200 hours** ×

$7.50 per hour

= $51,200

= $48,000

= $54,000

Rate Variance =

$3,200 U

Efficiency Variance =

$6,000 F

Spending Variance = $2,800 F

*

8,000 footballs × 0.8 hours per football = 6,400 hours

**

8,000 footballs × 0.9 hours per football = 7,200 hours

Alternatively, the variances can be computed using the formulas:

Labor rate variance = AH (AR – SR)

6,400 hours ($8.00 per hour – $7.50 per hour) = $3,200 U

Labor efficiency variance = SR (AH – SH)

$7.50 per hour (6,400 hours – 7,200 hours) = $6,000 F

b.

Work in Process (7,200 hours × $7.50 per hour) .

54,000

Labor Rate Variance

(6,400 hours × $0.50 per hour U) ………………..

3,200

Labor Efficiency Variance

(800 hours F × $7.50 per hour) ………….

6,000

Wages Payable

(6,400 hours × $8.00 per hour) …………..

51,200

Problem 8B-3A (continued)

3.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of

Input, at the

Standard Rate

Standard Hours

Allowed for Output,

at the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

6,400 hours ×

$2.75 per hour

6,400 hours ×

$2.50 per hour

7,200 hours ×

$2.50 per hour

= $17,600

= $16,000

= $18,000

Rate Variance =

$1,600 U

Efficiency Variance =

$2,000 F

Spending Variance = $400 F

Alternatively, the variances can be computed using the formulas:

Variable overhead rate variance = AH (AR – SR)

6,400 hours ($2.75 per hour – $2.50 per hour) = $1,600 U

Variable overhead efficiency variance = SR (AH – SH)

$2.50 per hour (6,400 hours – 7,200 hours) = $2,000 F

4. No. He is not correct in his statement. The company has a large,

unfavorable materials quantity variance that should be investigated.

Problem 8B-3A (continued)

5. The variances have many possible causes. Some of the more likely

causes include the following:

Materials variances:

Favorable price variance: Good price, inferior quality materials, unusual

Problem 8B-4A (75 minutes)

1. a. Before the variances can be computed, we must first compute the

standard and actual quantities of material per hockey stick. The

computations are:

Direct materials added to work in process (a) ..

$115,200

Standard direct materials cost per foot (b) ……

$3.00

Standard quantity of direct materials (a) ÷ (b)

38,400

feet

Standard quantity of direct materials (a) ………

38,400

feet

Number of sticks produced (b)……………………

8,000

Standard quantity per stick (a) ÷ (b) …………..

4.8

feet

Actual quantity of direct materials used per stick last year:

4.8 feet + 0.2 feet = 5.0 feet.

With these figures, the variances can be computed as follows:

Actual Quantity

of Input, at

Actual Price

Actual Quantity of

Input, at Standard Price

Standard Quantity

Allowed for Output, at

Standard Price

(AQ × AP)

(AQ × SP)

(SQ × SP)

60,000 feet ×

$3.00 per foot

38,400 feet ×

$3.00 per foot

$174,000

= $180,000

= $115,200

Price Variance =

$6,000 F

40,000 feet* × $3.00 per foot

= $120,000

Quantity Variance =

$4,800 U

*8,000 units × 5.0 feet per unit = 40,000 feet

Problem 8B-4A (continued)

Alternatively, the variances can be computed using the formulas:

Materials price variance = AQ (AP – SP)

60,000 feet ($2.90 per foot* – $3.00 per foot) = $6,000 F

Problem 8B-4A (continued)

2. a. Before the variances can be computed, we must first determine the

actual direct labor hours worked for last year. This can be done

through the variable overhead efficiency variance, as follows:

Variable overhead efficiency variance = SR (AH – SH)

$1.30 per hour × (AH – 16,000 hours*) = $650 U

Problem 8B-4A (continued)

Given these figures, the variances are:

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

16,500 hours ×

$5.00 per hour

16,000 hours ×

$5.00 per hour

$79,200

= $82,500

= $80,000

Rate Variance =

$3,300 F

Efficiency Variance =

$2,500 U

Spending Variance = $800 F

Alternatively, the variances can be computed using the formulas:

Labor rate variance = AH (AR – SR)

16,500 hours ($4.80 per hour* – $5.00 per hour) = $3,300 F

*79,200 ÷ 16,500 hours = $4.80 per hour

Labor efficiency variance = SR (AH – SH)

$5.00 per hour (16,500 hours – 16,000 hours) = $2,500 U

b.

Work in Process

(16,000 hours × $5.00 per hour) …………………

80,000

Labor Efficiency Variance

(500 hours U × $5.00 per hour) ………………….

2,500

Labor Rate Variance

(16,500 hours × $0.20 per hour F) ………….

3,300

Wages Payable

(16,500 hours × $4.80 per hour) …………….

79,200

Problem 8B-4A (continued)

3.

Actual Hours of

Input, at the

Actual Rate

Actual Hours of Input,

at the Standard Rate

Standard Hours

Allowed for Output, at

the Standard Rate

(AH × AR)

(AH × SR)

(SH × SR)

16,500 hours ×

$1.30 per hour

16,000 hours ×

$1.30 per hour

$19,800

= $21,450

= $20,800

Rate Variance =

$1,650 F

Efficiency Variance =

$650 U

Spending Variance = $1,000 F

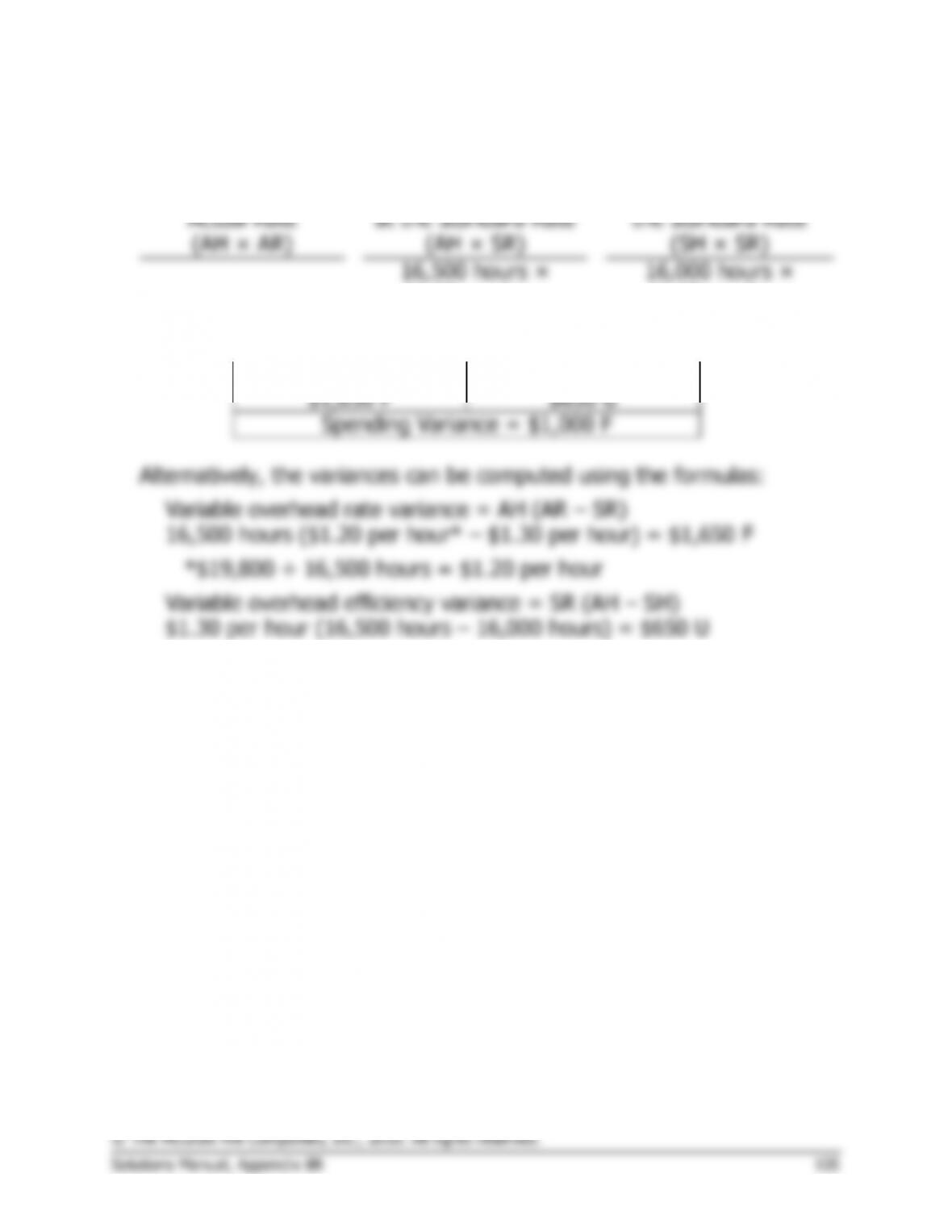

Alternatively, the variances can be computed using the formulas:

Variable overhead rate variance = AH (AR – SR)

16,500 hours ($1.20 per hour* – $1.30 per hour) = $1,650 F

*$19,800 ÷ 16,500 hours = $1.20 per hour

Variable overhead efficiency variance = SR (AH – SH)

$1.30 per hour (16,500 hours – 16,000 hours) = $650 U

Problem 8B-4A (continued)

4.

For materials:

Favorable price variance: Decrease in outside purchase price; fortunate

buy; inferior quality materials; unusual discounts due to quantity

purchased; less costly method of freight; inaccurate standards.

5.

Standard

Quantity or

Hours

Standard Price

or Rate

Standard

Cost

Direct materials …………

4.8 feet

$3.00 per foot

$14.40

Direct labor ………………

2.0 hours

$5.00 per hour

10.00

Variable overhead ………

2.0 hours

$1.30 per hour

2.60

Total standard cost …….

$27.00