Exercise 9-11 (30 minutes)

1.

Net operating income

Margin = Sales

$70,000

= = 5%

$1,400,000

Sales

Turnover = Average operating assets

$1,400,000

= = 4

$350,000

ROI = Margin × Turnover

= 5% × 4 = 20%

2.

Net operating income

Margin = Sales

$70,000 + $18,200

=

$1,400,000 + $70,000

$88,200

= = 6%

$1,470,000

Sales

Turnover = Average operating assets

Exercise 9-11 (continued)

3.

Net operating income

Margin = Sales

$70,000 + $14,000

=

$1,400,000

$84,000

= = 6%

$1,400,000

Sales

Turnover = Average operating assets

$1,400,000

= = 4

$350,000

ROI = Margin × Turnover

= 6% × 4 = 24%

4.

Net operating income

Margin =

Sales

$70,000

= = 5%

$1,400,000

Sales

Turnover = Average operating assets

$1,400,000

= $350,000 – $70,000

$1,400,000

= = 5

$280,000

Exercise 9-12 (30 minutes)

1. ROI computations:

Net operating income Sales

ROI = ×

Sales Average operating assets

$25,000,000 $5,000,000

2.

Division A

Division B

Division C

Average operating assets ………

$3,000,000

$7,000,000

$5,000,000

Required rate of return………….

× 14%

× 10%

× 16%

Required operating income …….

$ 420,000

$ 700,000

$ 800,000

Actual operating income ………..

$ 600,000

$ 560,000

$ 800,000

Required operating income

(above) …………………………..

420,000

700,000

800,000

Residual income ………………….

$ 180,000

$(140,000)

$ 0

Exercise 9-12 (continued)

3. a. and b.

Division A

Division B

Division C

Return on investment (ROI) ………..

20%

8%

16%

Therefore, if the division is

presented with an investment

opportunity yielding 15%, it

probably would ………………………

Reject

Accept

Reject

Minimum required return for

computing residual income ……….

14%

10%

16%

Therefore, if the division is

presented with an investment

opportunity yielding 15%, it

probably would ………………………

Accept

Accept

Reject

If performance is being measured by ROI, both Division A and Division C

probably would reject the 15% investment opportunity. These divisions’

ROIs currently exceed 15%; accepting a new investment with a 15%

rate of return would reduce their overall ROIs. Division B probably would

accept the 15% investment opportunity because accepting it would

increase the division’s overall rate of return.

If performance is measured by residual income, both Division A and

Division B probably would accept the 15% investment opportunity. The

15% rate of return promised by the new investment is greater than their

required rates of return of 14% and 10%, respectively, and would

therefore add to the total amount of their residual income. Division C

would reject the opportunity because the 15% return on the new

investment is less than its 16% required rate of return.

Exercise 9-13 (15 minutes)

1.

Net operating income

Margin = Sales

$150,000

= = 5%

$3,000,000

Sales

Turnover = Average operating assets

$3,000,000

= = 4

$750,000

ROI = Margin × Turnover

= 5% × 4 = 20%

Exercise 9-13 (continued)

3.

Net operating income

Margin = Sales

$150,000 + $200,000

=

$3,000,000 + $1,000,000

$350,000

= = 8.75%

$4,000,000

Sales

Turnover = Average operating assets

$3,000,000 + $1,000,000

= $750,000 + $250,000

$4,000,

= 000 = 4

$1,000,000

ROI = Margin × Turnover

= 8.75% × 4 = 35%

Problem 9-14A (30 minutes)

1. a., b., and c.

Month

1

2

3

4

Throughput time—days:

Process time (x) …………………………...

2.1

2.0

1.9

1.8

Inspection time …………………………….

0.6

0.7

0.7

0.6

Move time …………………………………..

0.4

0.3

0.4

0.4

Queue time …………………………………

4.3

5.0

5.8

6.7

Total throughput time (y) ……………….

7.4

8.0

8.8

9.5

Manufacturing cycle efficiency (MCE):

Process time (x) ÷

Throughput time (y) ……………………

28.4%

25.0%

21.6%

18.9%

Delivery cycle time—days:

Wait time from order to start of

production ………………………………..

16.0

17.5

19.0

20.5

Throughput time …………………………..

7.4

8.0

8.8

9.5

Total delivery cycle time …………………

23.4

25.5

27.8

30.0

2. All of the performance measures display unfavorable trends. Throughput

dropped.

Problem 9-14A (continued)

3. a. and b.

Month

5

6

Throughput time—days:

Process time (x) ……………………………………….

1.8

1.8

Inspection time ………………………………………..

0.6

0.0

Move time ………………………………………………

0.4

0.4

Queue time …………………………………………….

0.0

0.0

Total throughput time (y) …………………………..

2.8

2.2

Manufacturing cycle efficiency (MCE):

Process time (x) ÷ Throughput time (y) ………..

64.3%

81.8%

As a company reduces non-value-added activities, the manufacturing

cycle efficiency increases rapidly. The goal, of course, is to have an

efficiency of 100%. This will be achieved when

all

non-value-added

activities have been eliminated and process time is equal to throughput

time.

Problem 9-15A (20 minutes)

1. Operating assets do not include investments in other companies or in

undeveloped land.

Beginning

Balances

Ending

Balances

Cash …………………………………………….

$ 140,000

$ 120,000

Accounts receivable …………………………

450,000

530,000

Inventory ………………………………………

320,000

380,000

Plant and equipment (net) ………………..

680,000

620,000

Total operating assets ………………………

$1,590,000

$1,650,000

$1,650,000 + $1,590,000

Average operating assets = = $1,620,000

2

Net operating income

Margin = Sales

$405,000

= = 10%

$4,050,000

Sales

Turnover= Average operating assets

$4,050,000

= = 2.5

$1,620,000

ROI = Margin × Turnover

= 10% × 2.5 = 25%

2.

Net operating income ……………………………………

$405,000

Minimum required return (15% × $1,620,000) ……

243,000

Residual income …………………………..………………

$162,000

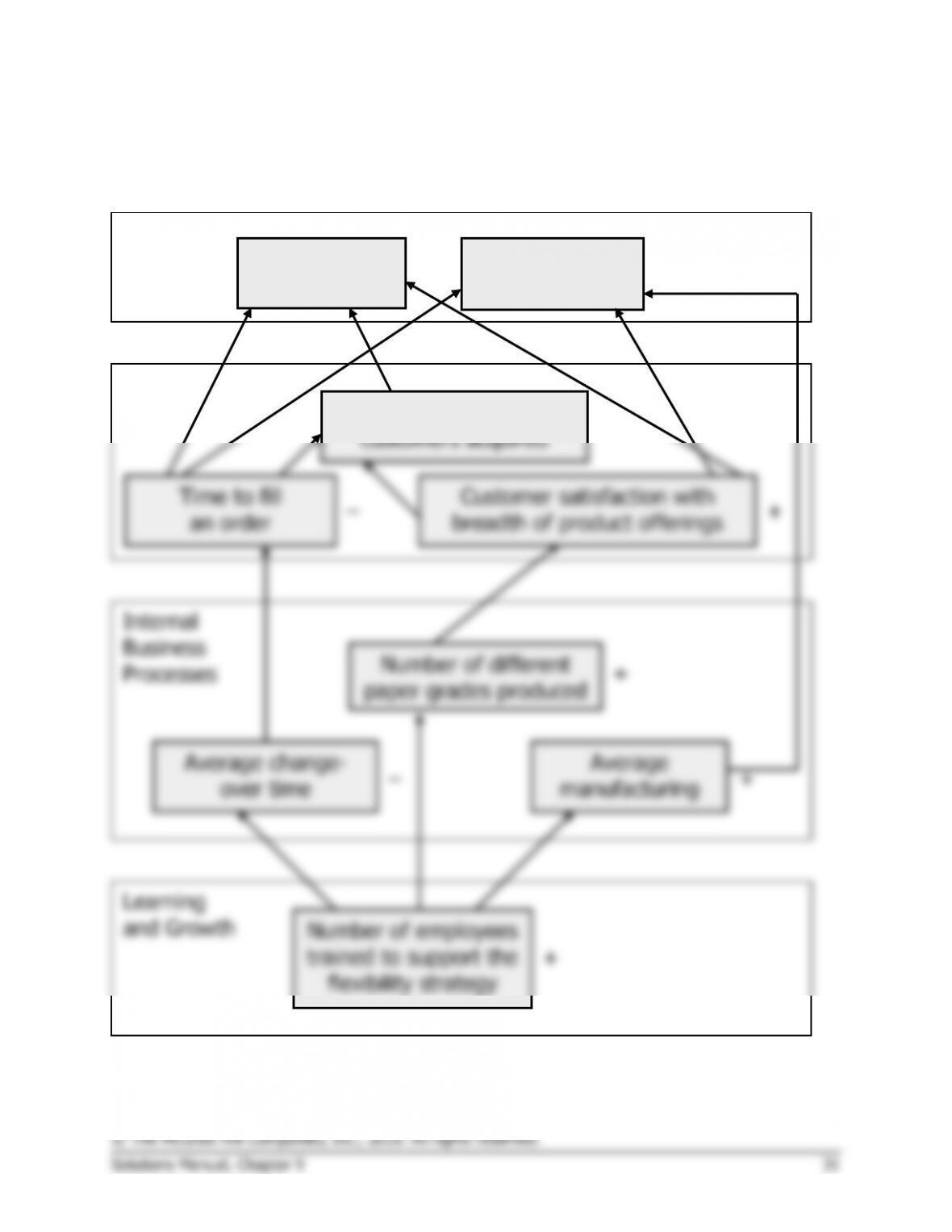

Problem 9-16A (45 minutes)

1. MPC’s previous manufacturing strategy was focused on high–volume

production of a limited range of paper grades. The goal of this strategy

was to keep the machines running constantly to maximize the number

of tons produced. Changeovers were avoided because they lowered

2. Employees focus on improving those measures that are used to evaluate

their performance. Therefore, strategically-aligned performance

measures will channel employee effort towards improving those aspects

of performance that are most important to obtaining strategic

Problem 9-16A (continued)

3. Students’ answers may differ in some details from this solution.

Average

+

+

Sales

Contribution

margin per ton

Financial

Number of new

customers acquired

Customer

+

+

+

Problem 9-16A (continued)

4. The hypotheses underlying the balanced scorecard are indicated by the

arrows in the diagram. Reading from the bottom of the balanced

scorecard, the hypotheses are:

° If the number of employees trained to support the flexibility strategy

increases, then the average changeover time will decrease and the

increase.

° If the customer satisfaction with breadth of product offerings

increases, then the number of new customers acquired, sales, and

the contribution margin per ton will increase.

° If the number of new customers acquired increases, then sales will

increase.

Each of these hypotheses can be questioned. For example, the time to

Problem 9-17A (30 minutes)

1. Breaking the ROI computation into two separate elements reveals

important relationships that otherwise might remain hidden. First, the

importance of asset turnover as a key element to overall profitability is

2. The missing information is as follows:

Companies in the Same Industry

A

B

C

Sales ………………………………

$600,000

*

$500,000

*

$2,000,000

Net operating income …………

$84,000

*

$70,000

*

$70,000

Average operating assets …….

$300,000

*

$1,000,000

$1,000,000

*

Margin …………………………….

14%

14%

3.5%

*

Turnover ………………………….

2.0

0.5

2.0

*

Return on investment (ROI) …

28%

7%

*

7%

Problem 9-17A (continued)

Thus, by including sales specifically in ROI computations the manager is

able to discover possible problems, as well as reasons underlying a

strong or a weak performance. Looking at Company A compared to

Problem 9-18A (30 minutes)

1.

Present

New Line

Total

(1)

Sales ……………………..

$10,000,000

$2,000,000

$12,000,000

(2)

Net operating income ..

$800,000

$160,000

*

$960,000

(3)

Operating assets ………

$4,000,000

$1,000,000

$5,000,000

(4)

Margin (2) ÷ (1) ………

8%

8%

8%

(5)

Turnover (1) ÷ (3) ……

2.5

2.0

2.4

(6)

ROI (4) × (5) …………..

20.0%

16.0%

19.2%

*

Sales ………………………………………………….

$2,000,000

Variable expenses (60% × $2,000,000) …….

1,200,000

Contribution margin ………………………………

800,000

Fixed expenses …………………………………….

640,000

Net operating income …………………………….

$ 160,000

3. The new product line promises an ROI of 16%, whereas the company’s

4.

a.

Present

New Line

Total

Operating assets ………………..

$4,000,000

$1,000,000

$5,000,000

Minimum return required ……..

× 12%

× 12%

× 12%

Minimum net operating

income…………………………..

$ 480,000

$ 120,000

$ 600,000

Actual net operating income …

$ 800,000

$ 160,000

$ 960,000

Minimum net operating

income (above) ……………….

480,000

120,000

600,000

Residual income …………………

$ 320,000

$ 40,000

$ 360,000

b. Under the residual income approach, Dell Havasi would be inclined to

accept the new product line because adding the product line would

increase the total amount of his division’s residual income, as shown

above.

Problem 9-19A (30 minutes)

1. a., b., and c.

Month

1

2

3

4

Throughput time in days:

Process time …………………………….

2.1

2.0

1.9

1.8

Inspection time …………………………

0.8

0.7

0.7

0.7

Move time ……………………………….

0.3

0.4

0.4

0.5

Queue time during production ………

2.8

4.4

6.0

7.0

Total throughput time …………………

6.0

7.5

9.0

10.0

Manufacturing cycle efficiency (MCE):

Process time ÷ Throughput time …..

35.0%

26.7%

21.1%

18.0%

Delivery cycle time in days:

Wait time to start of production ……

9.0

11.5

12.0

14.0

Throughput time ……………………….

6.0

7.5

9.0

10.0

Total delivery cycle time………………

15.0

19.0

21.0

24.0

2. a. Areas where the company is improving:

Quality control.

The number of defects has decreased by over 50% in

the last four months. Moreover, both warranty claims and customer

to 1.8 days over the last four months.

Problem 9-19A (continued)

b. Areas of deterioration:

Material control.

Scrap as a percentage of total cost has tripled over

3. a. and b.

Month

5

6

Throughput time in days:

Process time ……………………………………

1.8

1.8

Inspection time ………………………………..

0.7

0.0

Move time ………………………………………

0.5

0.5

Queue time during production …………….

0.0

0.0

Total throughput time ………………………..

3.0

2.3

Manufacturing cycle efficiency (MCE):

Process time ÷ Throughput time ………….

60.0%

78.3%

As non-value-added activities are eliminated, the manufacturing cycle

efficiency improves. The goal, of course, is to have an efficiency of

100%. This is achieved when all non-value-added activities have been

eliminated and process time equals throughput time.

Problem 9-20A (30 minutes)

1.

Net operating income Sales

ROI = ×

Sales Average operating assets

$360,000 $4,000,000

= ×

$4,000,000 $2,000,000

= 9% × 2 = 18%

2.

$360,000 $4,000,000

ROI = ×

$4,000,000 $1,600,000

= 9% × 2.5 = 22.5%

(Unchanged) (Increase) (Increase)

3.

$392,000 $4,000,000

ROI = ×

$4,000,000 $2,000,000

= 9.8% × 2 = 19.6%

(Increase) (Unchanged) (Increase)

4. Interest is a financing expense and thus it is not used to compute net

operating income.

$380,000 $4,000,000

ROI = ×

$4,000,000 $2,500,000

= 9.5% × 1.6 = 15.2%

(Increase) (Decrease) (Decrease)

Problem 9-20A (continued)

5. The company has a contribution margin ratio of 30% ($24 CM per unit,

divided by the $80 selling price per unit). Therefore, a 20% increase in

sales would result in a new net operating income of:

Sales (1.20 × $4,000,000) …..

$4,800,000

100

%

Variable expenses ………………

3,360,000

70

Contribution margin ……………

1,440,000

30

%

Fixed expenses ………………….

840,000

Net operating income …………

$ 600,000

$600,000 $4,800,000

ROI = ×

$4,800,000 $2,000,000

= 12.5% × 2.4 = 30%

(Increase) (Increase) (Increase)

6.

$320,000 $4,000,000

ROI = ×

$4,000,000 $1,960,000

= 8% × 2.04 = 16.3%

(Decrease) (Increase) (Decrease)

7.

$360,000 $4,000,000

ROI = ×

$4,000,000 $1,800,000

= 9% × 2.22 = 20%

(Unchanged) (Increase) (Increase)

Problem 9-21A (90 minutes)

1. Both companies view training as important; both companies need to

leverage technology to succeed in the marketplace; and both companies

are concerned with minimizing defects. There are numerous differences

between the two companies. For example, Applied Pharmaceuticals is a