Problem 13-13B (60 minutes)

This Year

Last Year

1.

a.

Current assets (a) …………………………….

$1,493,000

$1,055,000

Current liabilities (b) ………………………….

803,000

442,000

Working capital (a) − (b) ……………………

$ 690,000

$ 613,000

b.

Current assets (a) …………………………….

$1,493,000

$1,055,000

Current liabilities (b) ………………………….

$803,000

442,000

Current ratio (a) ÷ (b) ……………………….

1.86

2.39

c.

Quick assets (a) ……………………………….

$528,000

$443,000

Current liabilities (b) ………………………….

$803,000

$442,000

Acid-test ratio (a) ÷ (b) ……………………..

0.66

1.00

d.

Sales on account (a) …………………………

$5,015,000

$4,357,000

Average receivables (b) ……………………..

$379,000

$268,500

Accounts receivable turnover (a) ÷ (b) ….

13.2

16.2

Average collection period: 365 days ÷

accounts receivable turnover …………….

27.6 days

22.5 days

e.

Cost of goods sold (a) ……………………….

$3,866,000

$3,430,000

Average inventory (b) ………………………..

$767,000

$546,000

Inventory turnover ratio (a) ÷ (b) ………..

5.0

6.3

Average sale period:

365 days ÷ inventory turnover ………….

72.4 days

58.1 days

f.

Total liabilities (a) ……………………………..

$1,418,000

$1,057,000

Stockholders’ equity (b) ……………………..

$1,713,620

$1,541,580

Debt–to-equity ratio (a) ÷ (b) ………………

0.83

0.69

g.

Net income before interest and taxes (a) .

$496,000

$393,000

Interest expense (b) ………………………….

$49,200

$49,200

Times interest earned (a) ÷ (b) …………..

10.1

8.0

Problem 13-13B (continued)

2.

a.

Crowley Building Supply

Common-Size Balance Sheets

This Year

Last Year

Current assets:

Cash ………………………………

1.8%

5.4%

Marketable securities …………

0.0%

0.7%

Accounts receivable, net …….

15.1%

11.0%

Inventory ………………………..

30.2%

22.6%

Prepaid expenses ……………..

0.6%

1.0%

Total current assets ……………..

47.7%

40.6%

Plant and equipment, net ……..

52.3%

59.4%

Total assets ……………………….

100.0%

100.0%

Liabilities:

Current liabilities ………………

25.6%

17.0%

Bonds payable, 12% ………….

19.6%

23.7%

Total liabilities …………………….

45.3%

40.7%

Stockholders’ equity:

Preferred stock, $50 par, 8% .

10.0%

12.1%

Common stock, $10 par ……..

16.2%

19.5%

Retained earnings ……………..

28.5%

27.7%

Total stockholders’ equity ……..

54.7%

59.3%

Total liabilities and equity ……..

100.0%

100.0%

Note: Columns may not total down due to rounding.

Problem 13-13B (continued)

b.

Crowley Building Supply

Common-Size Income Statements

This Year

Last Year

Sales ………………………………………..

100.0%

100.0%

Cost of goods sold ……………………….

77.1%

78.7%

Gross margin …………………………..…

22.9%

21.3%

Selling and administrative expenses ..

13.0%

12.3%

Net operating income …………………..

9.9%

9.0%

Interest expense …………………………

1.0%

1.1%

Net income before taxes ……………….

8.9%

7.9%

Income taxes ……………………………..

3.1%

2.8%

Net income ………………………………..

5.8%

5.1%

3. The following points can be made from the analytical work in parts (1)

and (2) above:

a. The company has improved its profit margin from last year. This is

attributable primarily to an increase in gross margin, which is offset

Problem 13-13B (continued)

c. The drain on the cash account seems to be a result mostly of a large

buildup in accounts receivable and inventory. Notice that the average

collection period has increased by 5.1 days since last year, and that it

is now 9.6 days over the industry average. Many of the company’s

Problem 13-14B (60 minutes)

1.

a.

This Year

Last Year

Net income ……………………………………

$306,040

$222,040

Less preferred dividends …………………..

19,425

19,425

Net income remaining for common (a) …

$286,615

$202,615

Average number of common shares (b) .

50,400

50,400

Earnings per share (a) ÷ (b) ……………..

$5.69

$4.02

b.

Dividends per share (a)* …………………..

$1.90

$1.40

Market price per share (b) …………………

$38.00

$33.00

Dividend yield ratio (a) ÷ (b) ……………..

5.0%

4.2%

* $95,760 ÷ 50,400 shares = $1.90;

$70,560 ÷ 50,400 shares = $1.40

c.

Dividends per share (a) ……………………

$1.90

$1.40

Earnings per share (b) ……………………..

$5.69

$4.02

Dividend payout ratio (a) ÷ (b) ………….

33.4%

34.8%

d.

Market price per share (a) ………………..

$38.00

$33.00

Earnings per share (b) ……………………..

$5.69

$4.02

Price-earnings ratio (a) ÷ (b) …………….

6.6

8.2

Investors regard Kris Building Supply less favorably than other

companies in the industry. This is evidenced by the fact that they are

willing to pay only 6.6 times current earnings for a share of the

company’s stock, as compared to 9 times current earnings for other

companies in the industry. If investors were willing to pay 9 times

current earnings for Kris Building Supply’s stock, then it would be

selling for about $51.21 per share (9 × $5.69), rather than for only

$38 per share.

Problem 13-14B (continued)

This Year

Last Year

e.

Total stockholders’ equity ……………….

$1,687,410

$1,496,555

Less preferred stock ………………………

277,500

277,500

Common stockholders’ equity (a) ……..

$1,409,910

$1,219,055

Number of common shares

outstanding (b) ………………………….

50,400

50,400

Book value per share (a) ÷ (b) ………..

$27.97

$24.19

2.

a.

Net income ………………………………….

$ 306,040

$ 222,040

Add after-tax cost of interest paid:

[$55,800 × (1 – 0.30)] ………………..

39,060

39,060

Total (a) ……………………………………..

$ 345,100

$ 261,100

Average total assets (b) ………………….

$2,835,982

$2,384,778

Return on total assets (a) ÷ (b) ……….

12.2%

10.9%

b.

Net income ………………………………….

$ 306,040

$ 222,040

Less preferred dividends …………………

19,425

19,425

Net income remaining for common (a)

$ 286,615

$ 202,615

Average total stockholders’ equity* …..

$1,591,983

$1,382,778

Less average preferred stock …………..

277,500

277,500

Average common stockholders’ equity

(b) …………………………………………..

$1,314,483

$1,105,278

*1/2($1,687,410 + $1,496,555); 1/2($1,496,555 + $1,269,000)

Return on common stockholders’

equity (a) ÷ (b) ………………………….

21.8%

18.3%

Problem 13-14B (continued)

c. Financial leverage is positive in both years because the return on

3. We would recommend keeping the stock. The stock’s downside risk

seems small because it is selling for only 6.6 times current earnings as

12.2% compares well with that of the industry. The risk, of course, is

whether the company can get its cash problem under control.

Conceivably, the cash problem could worsen, leading to an eventual

Problem 13-15B (30 minutes)

a. It is becoming more difficult for the company to pay its bills as they

come due. Although the current ratio has improved over the three years,

the acid-test ratio is down. Also notice that the accounts receivable and

inventory are both turning more slowly, indicating that an increasing

increasing. With sales increasing (and undoubtedly cost of goods sold

also increasing), the average level of inventory must be increasing as

well to service the larger volume of sales.

e. The market price is going down. The dividends paid per share over the

three-year period are unchanged, but the dividend yield is going up.

Problem 13-16B (30 minutes)

1. a. Computation of working capital:

Current assets:

Cash ………………………………….

$ 73,000

Marketable securities …………….

13,500

Accounts receivable, net…………

357,200

Inventory …………………………...

467,800

Prepaid expenses ………………….

10,100

Total current assets (a) …………….

921,600

Current liabilities:

Accounts payable ………………….

205,400

Accrued liabilities ………………….

62,700

Notes due in one year ……………

106,000

Total current liabilities (b) …………

374,100

Working capital (a) − (b) ………….

$547,500

b. Computation of the current ratio:

Current ratio

=

Current

assets

=

$921,600

= 2.46

Current

liabilities

$374,100

c. Computation of the acid-test ratio:

Acid-test

ratio

=

Cash + Marketable securities +

Accounts receivable + Short-term notes

Current liabilities

=

$73,000 + $13,500 + $357,200

=

$443,700

= 1.19

$374,100

$374,100

Problem 13-16B (continued)

2.

The Effect on

Working

Current

Acid-Test

Transaction

Capital

Ratio

Ratio

(a)

Declared a cash dividend ……………..

Decrease

Decrease

Decrease

(b)

Paid accounts payable …………………

None

Increase

Increase

(c)

Collected accounts receivable ………..

None

None

None

(d)

Purchased equipment for cash ………

Decrease

Decrease

Decrease

(e)

Paid a cash dividend previously

declared …………………………………

None

Increase

Increase

(f)

Borrowed on a short-term note ……..

None

None

Decrease

(g)

Sold inventory at a profit ……………..

Increase

Increase

Increase

(h)

Wrote off uncollectible accounts …….

None

None

None

(i)

Sold marketable securities at a loss

Decrease

Decrease

Decrease

(j)

Issued common stock for cash ………

Increase

Increase

Increase

(k)

Paid off short-term notes ……………..

None

Increase

Increase

Problem 13-17B (45 minutes)

Effect on

Ratio

Reason for Increase, Decrease, or No Effect

1.

Decrease

Declaring a cash dividend will increase current liabilities,

but have no effect on current assets. Therefore, the

current ratio will decrease.

2.

Increase

A sale of inventory on account will increase the quick

assets (cash, accounts receivable, marketable securities)

but have no effect on the current liabilities. For this

reason, the acid-test ratio will increase. The same effect

would result regardless of whether the inventory was sold

at cost, at a profit, or at a loss. That is, the acid-test ratio

would increase in all cases; the only difference would be

the amount of the increase.

3.

Increase

The interest rate on the bonds is only 9%. Since the

company’s assets earn at a rate of 12%, positive leverage

would come into effect, increasing the return to the

common stockholders.

4.

Decrease

A decrease in net income would mean less income

available to cover interest payments. Therefore, the

times-interest-earned ratio would decrease.

5.

Increase

Payment of a previously declared cash dividend will

reduce both current assets and current liabilities by the

same amount. An equal reduction in both current assets

and current liabilities will always result in an increase in

the current ratio, so long as the current assets exceed the

current liabilities.

6.

No Effect

The dividend payout ratio is a function of the dividends

paid per share in relation to the earnings per share.

Changes in the market price of a stock have no effect on

this ratio.

7.

Increase

A write-off of inventory will reduce the inventory balance,

thereby increasing the turnover in relation to a given level

of sales.

Problem 13-17B (continued)

Effect on

Ratio

Reason for Increase, Decrease, or No Effect

8.

Decrease

Sale of inventory at a profit will increase the assets of a

company. The increase in assets will be reflected in an

increase in retained earnings, which is part of stockholders’

equity. An increase in stockholders’ equity will result in a

decrease in the ratio of assets provided by creditors as

compared to assets provided by owners.

9.

Decrease

Extended credit terms for customers means that customers

on the average will be taking longer to pay their bills. As a

result, the accounts receivable will “turn over,” or be

collected, less frequently during a given year.

10.

Decrease

A common stock dividend will result in a greater number of

shares outstanding, with no change in the underlying

assets. The result will be a decrease in the book value per

share.

11.

No Effect

Book value per share is dependent on historical costs of

already completed transactions as reflected on a company’s

balance sheet. It is not affected by current market prices

for the company’s stock.

12.

No Effect

Payments on account reduce cash and accounts payable by

equal amounts; thus, the net amount of working capital is

not affected.

13.

Decrease

The stock dividend will increase the number of common

shares outstanding, thereby reducing the earnings per

share.

14.

Decrease

Payments to creditors will reduce the total liabilities of a

company, thereby decreasing the ratio of total debt to total

equity.

15.

Decrease

A purchase of inventory on account will increase current

liabilities, but will not increase the quick assets (cash,

accounts receivable, marketable securities). Therefore, the

ratio of quick assets to current liabilities will decrease.

Problem 13-17B (continued)

Effect on

Ratio

Reason for Increase, Decrease, or No Effect

16.

No Effect

Write-off of an uncollectible account against the Allowance

for Bad Debts will have no effect on total current assets.

For this reason, the current ratio will remain unchanged.

17.

Increase

The price-earnings ratio is obtained by dividing the market

price per share by the earnings per share. If the earnings

per share remains unchanged, and the market price goes

up, then the price-earnings ratio will increase.

18.

Decrease

The dividend yield ratio is obtained by dividing the dividend

per share by the market price per share. If the dividend per

share remains unchanged and the market price goes up,

then the yield will decrease.

Problem 13-18B (90 minutes)

1.

a.

This Year

Last Year

Net income ……………………………………

$ 470,400

$ 309,400

Add after-tax cost of interest:

$128,000 × (1 – 0.30) …………………..

89,600

$108,000 × (1 – 0.30) …………………..

75,600

Total (a) ……………………………………….

$ 560,000

$ 385,000

Average total assets (b) ……………………

$5,551,600

$4,690,700

Return on total assets (a) ÷ (b) …………

10.1%

8.2%

b.

Net income ……………………………………

$ 470,400

$ 309,400

Less preferred dividends …………………..

48,000

48,000

Net income remaining for common (a) ..

$ 422,400

$ 261,400

Average total stockholders’ equity ………

$3,371,600

$3,855,293

Less average preferred stock …………….

600,000

600,000

Average common equity (b) ………………

$2,771,600

$3,255,293

Return on common stockholders’ equity

(a) ÷ (b) …………………………………….

15.2%

8.0%

c.

Leverage is positive for this year because the return on common

equity (15.2%) is greater than the return on total assets (10.1%).

For last year, leverage is negative because the return on the common

equity (8.0%) is less than the return on total assets (8.2%).

2.

a.

Net income remaining for common [see

above] (a) …………………………………..

$422,400

$261,400

Average number of common shares

outstanding (b) …………………………...

50,000

50,000

Earnings per share (a) ÷ (b) ……………..

$8.45

$5.23

b.

Dividends per share (a) ……………………

$1.24

$0.62

Market price per share (b) ………………..

$54.00

$38.00

Dividend yield ratio (a) ÷ (b) …………….

2.3%

1.6%

Problem 13-18B (continued)

This Year

Last Year

c.

Dividends per share (a) ……………………

$1.24

$0.62

Earnings per share (b) ……………………..

$8.45

$5.23

Dividend payout ratio (a) ÷ (b) ………….

14.7%

11.9%

d.

Market price per share (a) ………………….

$54.00

$38.00

Earnings per share (b) ……………………….

$8.45

$5.23

Price-earnings ratio (a) ÷ (b) ………………

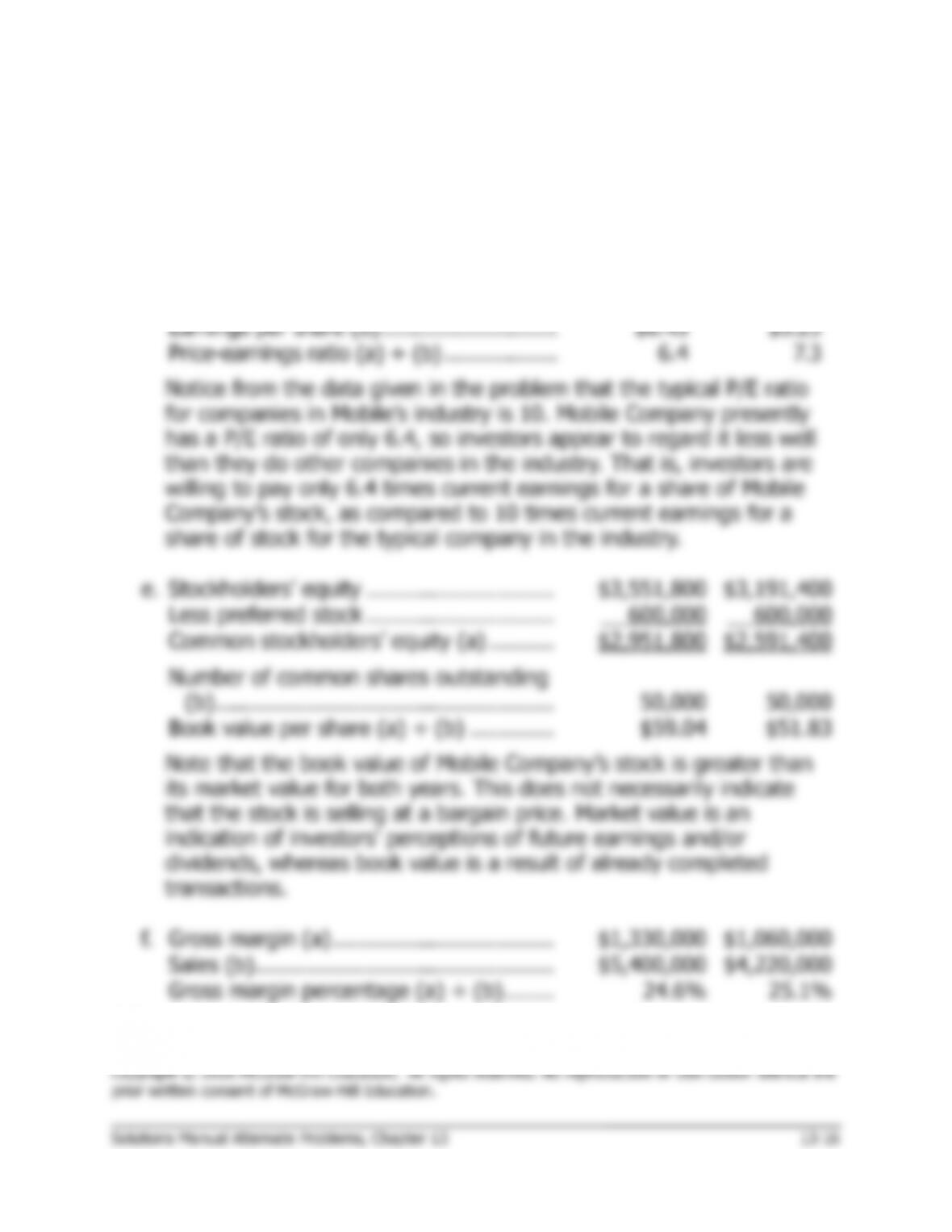

6.4

7.3

Notice from the data given in the problem that the typical P/E ratio

for companies in Mobile’s industry is 10. Mobile Company presently

has a P/E ratio of only 6.4, so investors appear to regard it less well

than they do other companies in the industry. That is, investors are

willing to pay only 6.4 times current earnings for a share of Mobile

Company’s stock, as compared to 10 times current earnings for a

share of stock for the typical company in the industry.

e.

Stockholders’ equity ………………………..

$3,551,800

$3,191,400

Less preferred stock ………………………..

600,000

600,000

Common stockholders’ equity (a) ……….

$2,951,800

$2,591,400

Number of common shares outstanding

(b) …………………………………………….

50,000

50,000

Book value per share (a) ÷ (b) ………….

$59.04

$51.83

f.

Gross margin (a) …………………………….

$1,330,000

$1,060,000

Sales (b) ……………………………………….

$5,400,000

$4,220,000

Gross margin percentage (a) ÷ (b) ……..

24.6%

25.1%

Problem 13-18B (continued)

This Year

Last Year

3.

a.

Current assets (a) …………………………….

$2,646,000

$1,930,000

Current liabilities (b) ………………………….

1,250,000

750,000

Working capital (a) − (b) ……………………

$1,396,000

$1,180,000

b.

Current assets (a) …………………………….

$2,646,000

$1,930,000

Current liabilities (b) ………………………….

$1,250,000

$750,000

Current ratio (a) ÷ (b) ……………………….

2.12

2.57

c.

Quick assets (a) ……………………………….

$1,231,000

$1,130,000

Current liabilities (b) ………………………….

$1,250,000

$750,000

Acid-test ratio (a) ÷ (b) ……………………..

0.98

1.51

d.

Sales on account (a) …………………………

$5,400,000

$4,220,000

Average receivables (b) ……………………..

$755,500

$563,500

Accounts receivable turnover (a) ÷ (b) ….

7.15

7.49

Average collection period: 365 days ÷

accounts receivable turnover …………….

51 days

49 days

e.

Cost of goods sold (a) ……………………….

$4,070,000

$3,160,000

Average inventory balance (b) …………….

$1,030,000

$690,000

Inventory turnover ratio (a) ÷ (b) ………..

3.95

4.58

Average sales period: 365 days ÷

inventory turnover ratio …………………..

92 days

80 79 days

f.

Total liabilities (a) ……………………………..

$2,530,000

$1,830,000

Stockholders’ equity (b) ……………………..

$3,551,800

$3,191,400

Debt–to-equity ratio (a) ÷ (b) ………………

0.71

0.57

g.

Net income before interest and income

taxes (a) ………………………………………

$800,000

$550,000

Interest expense (b) ………………………….

$128,000

$108,000

Times interest earned (a) ÷ (b) …………..

6.2

5.1

Problem 13-18B (continued)

4. As stated by Loretta Young, both net income and sales are up from last

10.1% this year, and the return on common equity is up to 15.2% from

8.0% the year before. But this appears to be the only bright spot.

Virtually all other ratios are below what is typical for the industry, and,

more important, they are trending downward. The deterioration in the

gross margin percentage, while not large, is worrisome. Sales and

Problem 13-19B (30 minutes)

1.

Automart Company

Comparative Balance Sheets

This Year

Last Year

Current assets:

Cash ………………………………………

5.7%

8.3%

Marketable securities ………………….

0.0%

1.9%

Accounts receivable, net ……………..

15.3%

11.9%

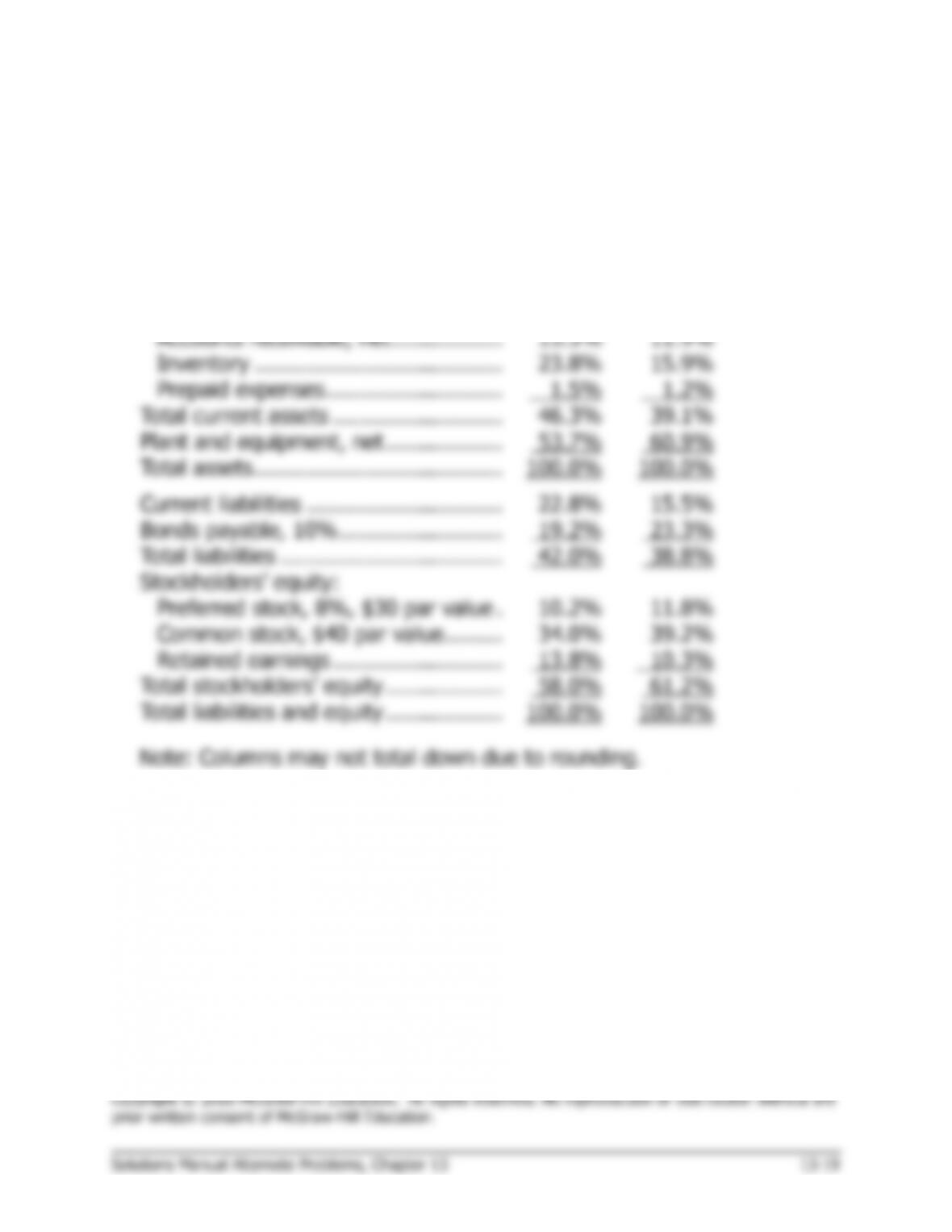

Inventory ………………………………..

23.8%

15.9%

Prepaid expenses ………………………

1.5%

1.2%

Total current assets ……………………..

46.3%

39.1%

Plant and equipment, net ………………

53.7%

60.9%

Total assets ………………………………..

100.0%

100.0%

Current liabilities …………………………

22.8%

15.5%

Bonds payable, 10% …………………….

19.2%

23.3%

Total liabilities …………………………….

42.0%

38.8%

Stockholders’ equity:

Preferred stock, 8%, $30 par value .

10.2%

11.8%

Common stock, $40 par value ………

34.0%

39.2%

Retained earnings ……………………..

13.8%

10.3%

Total stockholders’ equity ………………

58.0%

61.2%

Total liabilities and equity ………………

100.0%

100.0%

Note: Columns may not total down due to rounding.

Problem 13-19B (continued)

2.

Automart Company

Comparative Income Statements

This Year

Last Year

Sales ………………………………………..

100.0%

100.0%

Cost of goods sold ………………………..

77.1%

76.7%

Gross margin ……………………………….

22.9%

23.3%

Selling and administrative expenses ….

9.7%

12.0%

Net operating income …………………….

13.2%

11.3%

Interest expense …………………………..

2.1%

2.8%

Net income before taxes ………………..

11.1%

8.5%

Income taxes (30%) ……………………..

3.3%

2.5%

Net income ………………………………….

7.8%

5.9%

*Due to rounding, figures may not fully reconcile down a column.

3. The company’s current position has declined substantially between the

two years. Cash this year represents only 5.7% of total assets, whereas

it represented 10.2% last year (Cash + Marketable Securities). In

addition, both accounts receivable and inventory are up from last year,